US TSYS: Post-Powell Losses Pared, Jobless Claims & Trump-Starmer Presser Ahead

Sep-18 10:43

- Treasuries have pared around half of yesterday’s sell-off, which had on balance continued after Fed Chair Powell’s press conference following after an initially sharp dovish reaction to the SEP.

- Jobless claims headline the data docket, with last week’s Texas-driven spike since linked at least partly to ID fraud, whilst President Trump has a press conference with UK PM Starmer at 0920ET on the final day of his trip.

- Cash yields are 3-4bp lower on the day with the front end lagging slightly.

- 10Y yields are at 4.049% (-3.8bps) having yesterday briefly cleared 4.00% for the first time since Sep 11 and before that early April around reciprocal tariff announcements.

- TYZ5 has lifted to 113-10+ (+06+) off an overnight low of 113-00, on limited cumulative volumes of 285k considering it will include Asian and European reflection of Fed communications.

- Yesterday saw a fleeting high of 113-25+ on the initial dovish reaction to the dot plot although it didn’t trouble resistance at cycle highs of 113-29 (Sep 11 high). The overnight low of 113-00 did however come close to support at 112-28 (20-day EMA) after which lies 112-05+ (50-day EMA).

- Data: Weekly jobless claims (0830ET), Philly Fed mfg Sep (0830ET), Leading index Aug (1000ET), TIC Flows Jul (1600ET)

- Fedspeak: Media blackout remains until Friday 0001ET

- Coupon issuance: US Tsy $19B 10Y TIPS auction (1300ET)

- Bill issuance: US Tsy $100B 4W & $85B 8W bill auctions (1130ET)

- Politics: Trump in Business Leaders Reception with UK PM Starmer (0745ET), Trump-Starmer press conference (0920ET), Trump departs UK en route to White House (1205ET)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Aug19 NY cut 1000ET (Source DTCC)

Aug-19 10:32

- EUR/USD: $1.1600(E731mln), $1.1620-25(E2.3bln), $1.1650-65(E682mln), $1.1700(E1.3bln)

- USD/JPY: Y148.30-35($709mln)

- AUD/USD: $0.6515(A$745mln)

- USD/CAD: C$1.3750-70($646mln)

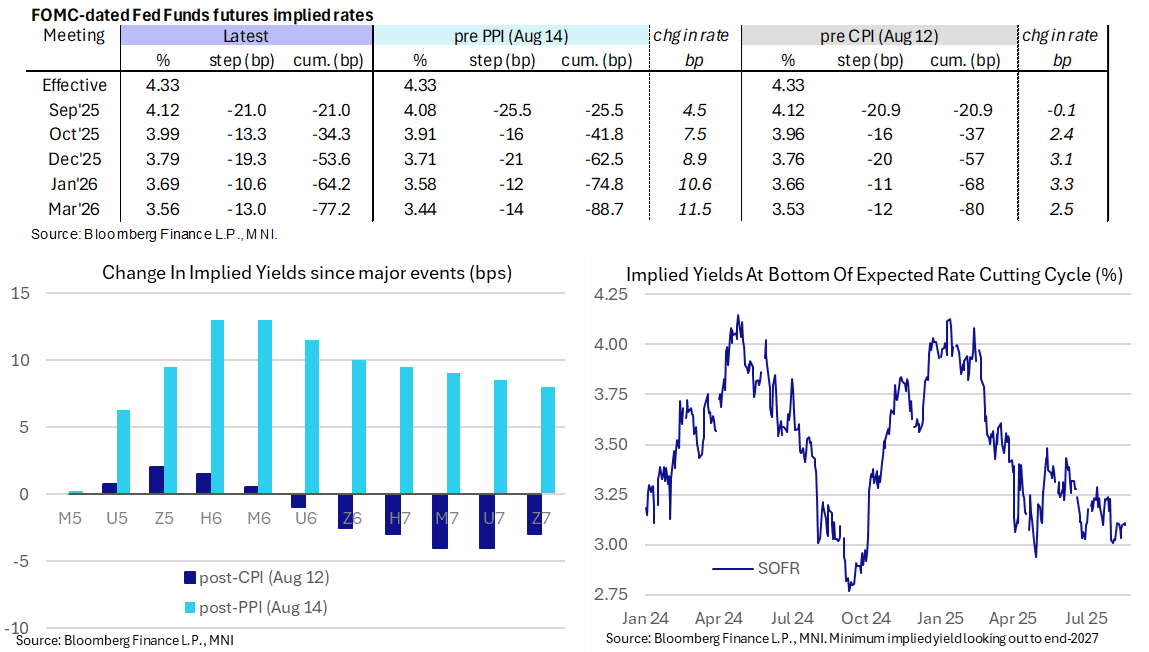

STIR: Sept Fed Cut Still No Longer Fully Locked In, A Dovish Bowman Ahead

Aug-19 10:32

- Fed Funds implied rates are unchanged on the day, with 21bp of cuts priced for next month’s FOMC meeting.

- Cumulative cuts from 4.33% effective: 21bp Sep, 34.5bp Oct, 53.5bp Dec, 64bp Jan and 77bp Mar.

- The SOFR implied terminal yield of 3.11% (SFRH7) is essentially unchanged from the past two closes, holding the +/-5bp of 125bp of cuts from current levels range seen since the Aug 1 payrolls report.

- Fed VC Supervision Bowman (permanent voter, dove) speaks on Bloomberg TV at 1000ET before at a Blockchain Symposium at 1410ET (text only), with greater scope for market moving comments at the former. We suspect it might be hard to generate a dovish reaction though unless she canvasses larger cuts, something other FOMC colleagues have pushed back on.

- These will be her first remarks since last week’s mixed inflation data. She said on Aug 9 that she favors three cuts this year (unsurprising having dissented in July) and saw recent labor data as reinforcing this view.

- Tomorrow then sees the FOMC minutes before Powell’s Jackson Hole address on Friday. However, when it comes to Sept cut prospects, the August payrolls and CPI releases plus QCEW details (for preliminary payroll benchmark revision estimates) are all still to come before the next FOMC decision on Sep 17.

ESM ISSUANCE: 6-month ESM-Bill

Aug-19 10:32

| Type | 6-month bills |

| Maturity | Feb 19, 2026 |

| Amount | E1.082bln |

| Target | E1.1bln |

| Previous | E1.089bln |

| Avg yield | 1.947% |

| Previous | 1.923% |

| Bid-to-cover | 2.64x |

| Previous | 2.41x |

| Previous date | Jul 15, 2025 |