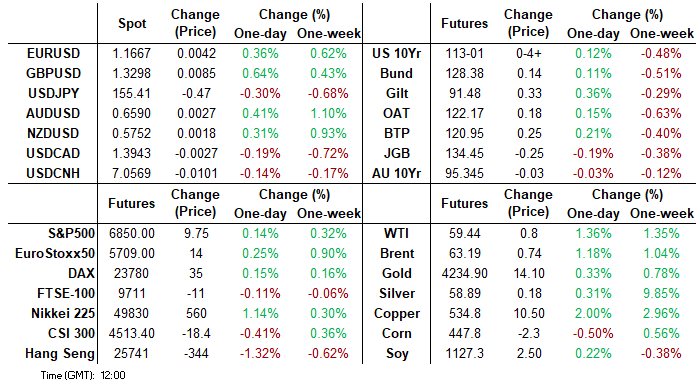

MNI US MARKETS ANALYSIS - USD Index Tests Support into Data

Highlights:

- Treasury curve sits modestly bull steeper into timely private sector data

- GBP outperforms as PMI tops expectations

- USD Index edges to new December low, on track to close below 50-dma

US TSYS: Modestly Bull Steeper Ahead Of A More Important Data Docket

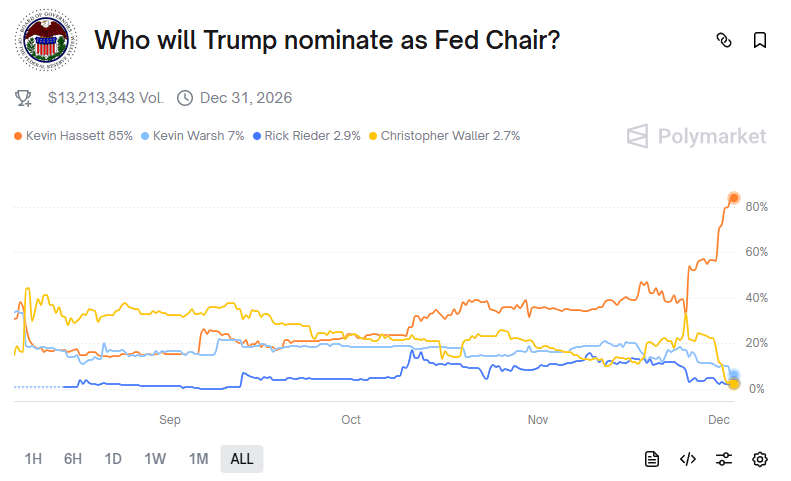

Treasuries trade modestly bull steeper, partly better reflecting the latest increase in the likelihood that NEC’s Hassett is chosen as the next Fed Chair. Volumes are thin however ahead of the start of this week’s more notable labor releases plus ISM services for November before next week’s FOMC decision and new economic forecasts.

- Cash yields are 1-2bp lower on the day.

- 5s30s has extended yesterday’s steepening, currently at 109.7bp having earlier nudged 110bps to test steepest levels since the first half of September.

- TYH6 trades at 113-01 (+04+) on very thin cumulative volumes of 215k, steadily rising off yesterday’s latest low of 112-22 but still some way from reversing Monday’s losses attributed to rate locks and speculative selling.

- Support is seen at that 112-22 before 112-10+ (Nov 20 low), having already breached an important support at the 50-day EMA, whilst resistance is seen at 113-11 (Dec 1 high) before 113-22+ (Nov 25 high).

- Data: Weekly MBA mortgage data (0700ET), ADP employment Nov (0815ET), Import/export prices Sep (0830ET, shutdown catch-up), IP/Cap Util Sep (0915ET, shutdown catch-up), S&P Global US services PMI Nov final (0945ET), ISM Services Nov (1000ET)

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump to make an announcement (1430ET)

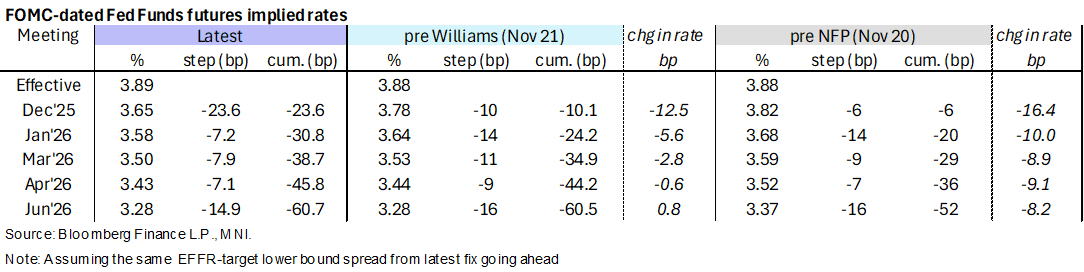

STIR: US Rates Reflect Latest Leg Higher In Hassett Fed Chair Probability

- Overnight rate moves chime with another tick higher in odds that NEC’s Hassett will be the next Fed chair, even if there was little initial reaction to Trump explicitly referring to him as potential chair yesterday when the likelihood in betting markets increased from 65-70% to 85%.

- WSJ reporting has since helped solidify the modest rally, led by mid-2026/early-2027 contracts, noting that the Trump administration cancelled a slate of interviews set to start on Wed with a group of finalists. A person familiar with the matter said the cancellation was because of a scheduling conflict for the vice president.

- Fed Funds implied rates are unchanged through March after which they sit a touch lower on the day.

- Cumulative cuts from 3.89% effective: 23.5bp Dec, 31bp Jan, 38.5bp Mar, 46bp Apr and 60.5bp Jun.

- SOFR futures are up to +0.02 on the day, with the terminal implied yield of 3.035% (H7) extending the week’s decline back towards the 3% seen since NY Fed’s Williams’ dovish guidance on Nov 21.

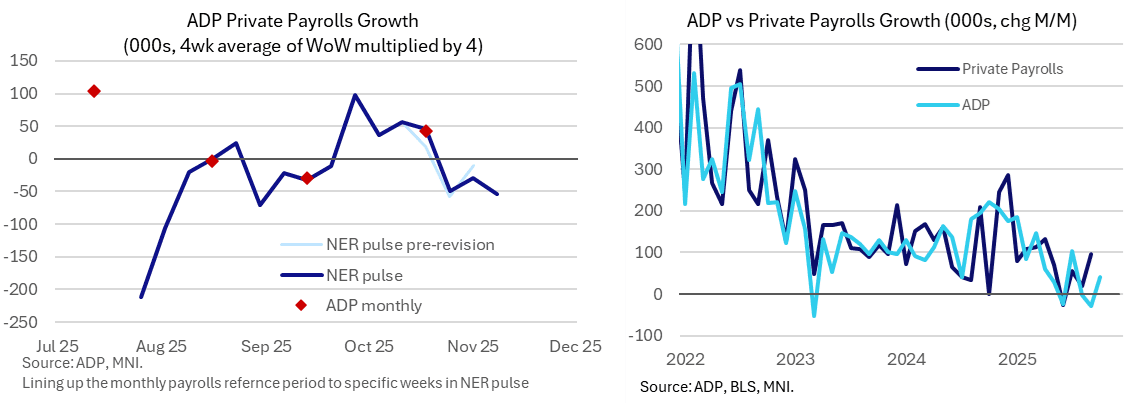

US OUTLOOK/OPINION: Weekly Tracking Suggests ADP Downside Surprise

ADP private employment is expected to have increased by a mild 10k in November although weekly tracking points to a non-trivial decline. It should be an important update on labor demand with the FOMC going into next week’s meeting and a new forecast round with the last BLS payrolls report only for September.

- Ahead of today's 0815ET release, Bloomberg consensus sees ADP employment growth of 10k in November after 42k in October although the former looks optimistic compared to recent weekly ADP tracking.

- Last week’s ADP NER Pulse update saw an average weekly change of -13.5k in the four weeks up to Nov 8, i.e. closer to a -55k decline on a rolling monthly basis.

- In theory, this monthly report should offer limited new information from that in the weekly series as, broadly mimicking the BLS payrolls report, its reference period is the week including the 12th of the month.

- The weekly series is prone to revisions although we’d be surprised if they were strong enough to materially alter a weak trend that has seen three weeks averaging -11k (on the same four-week rolling basis, i.e. closer to -45k in monthly terms).

- For context of last month’s release, monthly ADP employment increased 42k in October vs latest weekly data at the time showing 57k and Bloomberg consensus of 30k. Since then, the current vintage for the weekly tracker points to a ~46k increase.

- If we do indeed see a negative ADP employment print for November, it would mark a third monthly decline in the latest four months of data, with -3k in Aug, -29k in Sep and +42k in Oct.

- The broader momentum in the series should be viewed as an important indicator for jobs growth, with the three-month average slowing through the year to date (200k in Dec 2024, 139k in Mar, 22k in Jun, 24k in Sep and just 3k most recently in Oct).

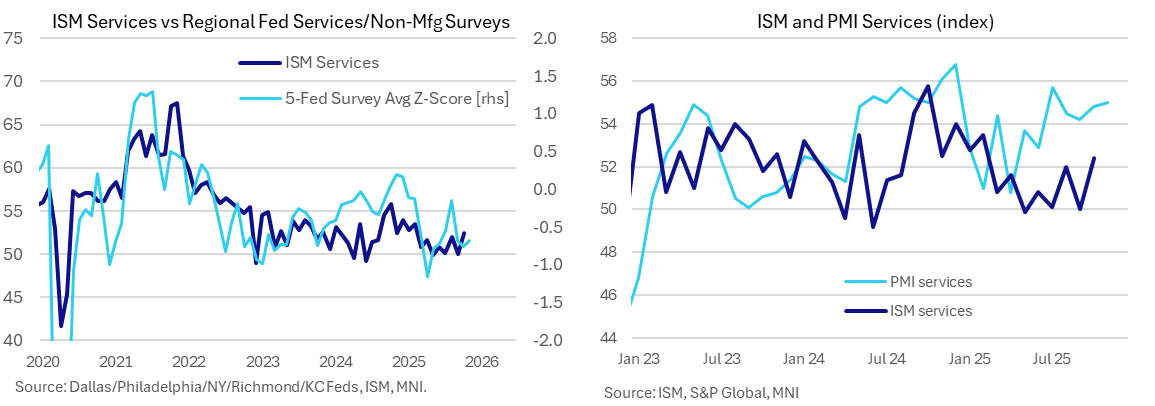

US OUTLOOK/OPINION: ISM Services Seen Dipping In Nov Despite More Optimistic PMI

- The ISM services index is seen dipping to 52.0 in November to only modestly ease after a stronger than expected eight-month high of 52.4 in October.

- The index has ranged between 49.9 (May) and 53.5 (Feb) so far this year and more recently oscillated between 50 and 52 handles since July.

- Alternate indicators on balance point to some limited upside but that’s mainly from the services PMI, which is typically much more optimistic and by notably differing amounts month-to-month.

- S&P Global PMI: upside. The services PMI ticked up further to 55.0 in the flash November release from 54.8 in October for a fresh high since July and before that Dec 2024. As such, it points to both directional and level upside risk but, just as with the manufacturing survey, it has been far more optimistic than its ISM counterpart. It has averaged 3.4pts higher than ISM services in the latest six months but with a range of 2.1-5.6pts which means its predictive power should be viewed cautiously.

- Regional Fed surveys: neutral. The average of five regional Fed service/non-manufacturing surveys ticked down from -12.2 to -12.5 whilst the z-score inched higher from -0.8 to -0.7. The latter points to a small directional improvement on the month but is starting from a relatively lower level – see chart. The combination sees little conviction on risks to the ISM reading this month.

- There’s no consensus for new orders although we’ll watch them closely to see if it’s possible to decipher a trend after what has been a particularly noisy few months (56.2 in Oct, technically a twelve-month high, after 50.4 in Sep and 56.0 in Aug). The flash PMI (link) encouragingly noted the “largest rise in new business so far this year” along with its “strongest output gain since July”.

- The employment index meanwhile steadily increased in Sept and Oct to 48.2, still contractionary but a five-month high nevertheless. With no more BLS payrolls data due before the Dec 9-10 FOMC meeting, that should carry greater weight than usual.

SOFR: Net Short Cover Dominated In Futures On Tuesday

OI data points to short cover dominating through the blues as SOFR futures ticked higher on Tuesday.

- There were fairly isolated pockets of net long setting, although all of the net pack OI swings tilted comfortably into cover territory.

- A further increase in betting market odds of Kevin Hassett succeeding Powell as Fed Chair provided background support for SOFR futures through the session.

| 02-Dec-25 | 01-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,354,634 | 1,348,937 | +5,697 | Whites | -31,493 |

SFRZ5 | 1,649,640 | 1,699,622 | -49,982 | Reds | -12,581 |

SFRH6 | 1,351,490 | 1,327,743 | +23,747 | Greens | -4,353 |

SFRM6 | 1,148,140 | 1,159,095 | -10,955 | Blues | -6,500 |

SFRU6 | 1,069,118 | 1,085,894 | -16,776 |

|

|

SFRZ6 | 1,127,362 | 1,123,333 | +4,029 |

|

|

SFRH7 | 854,715 | 842,615 | +12,100 |

|

|

SFRM7 | 777,161 | 789,095 | -11,934 |

|

|

SFRU7 | 840,338 | 822,650 | +17,688 |

|

|

SFRZ7 | 836,677 | 851,757 | -15,080 |

|

|

SFRH8 | 427,868 | 444,845 | -16,977 |

|

|

SFRM8 | 417,312 | 407,296 | +10,016 |

|

|

SFRU8 | 371,814 | 375,126 | -3,312 |

|

|

SFRZ8 | 320,429 | 325,213 | -4,784 |

|

|

SFRH9 | 195,784 | 193,545 | +2,239 |

|

|

SFRM9 | 208,037 | 208,680 | -643 |

|

|

EUROPE ISSUANCE UPDATE

UK auction results

- Average gilt auction. The bid-to-cover was strong at 3.10x but the lowest accepted price of 100.446 was marginally below the pre-auction mid-price of 100.447.

- We have seen the price of the 4.00% May-29 gilt move marginally lower in the minutes after the results being published.

- Gilt futures also down around 3-4 ticks during that time. However, we've also seen Bund futures move a couple of ticks lower.

- GBP4.75bln of the 4.00% May-29 Gilt. Avg yield 3.855% (bid-to-cover 3.10x, tail 0.4bp).

Italy buyback auction results

- E1.115bln of the 3.20% Jan-26 BTP Short Term (ISIN: IT0005584302) at 100.120

- E1.020bln of the 4.50% Mar-26 BTP (ISIN: IT0004644735) at 100.577

- E1.112bln of the 3.80% Apr-26 BTP (ISIN: IT0005538597) at 100.585

- E1.015bln of the 3.10% Aug-26 BTP Short Term (ISIN: IT0005607269) at 100.681

- E1.264bln of the 3.85% Sep-26 BTP (ISIN: IT0005556011) at 101.305

- E0.720bln of the 0.55% May-26 BTP Italia (ISIN: IT0005332835) at 99.549

- E0.754bln of the 0.50% Apr-26 CCTeu (ISIN: IT0005428617) at 100.222

FOREX: Greenback Tilts Lower amid Risk Optimism/Hasset Chair Expectations

- The risk backdrop remains stable Wednesday, allowing the major indices and crypto markets to edge higher and provide a negative tilt to the US dollar. The greenback tone was also set late last night as President Trump’s nod towards Kevin Hassett potentially becoming the next Fed Chair confirms the dovish bias to market Fed pricing for 2026.

- These dynamics have prompted GBP and the Scandies to outperform on the session. For GBPUSD specifically, spot has edged to a fresh recovery and post-budget high, with momentum building on the better-than-expected PMI print. Prices are now meeting an uptrendline drawn off the Nov13 high on the 15min candle chart - meaning further strength here could trigger more on the follow through. A close back above the 50-day EMA for cable would also be the first since early October. Mirroring the move, EURGBP has firmly rejected the test of 0.88 overnight, erasing the majority of Monday's rally.

- For EURUSD, we are currently testing above key resistance and the bull trigger at 1.1656. The moves come despite the latest Kremlin commentary pouring cold water on the prospects of a peace deal, with prediction markets' odds for a ceasefire by the end of '26 falling below 50%.

- Despite a weaker-than-expected Q3 GDP print, stronger domestic demand growth is likely to keep the RBA in cautious mode, underpinning the firm AUD recovery. Elsewhere, softer-than-expected Swiss CPI figures did little to move the Swiss needle.

- A wide set of US data is scheduled for today, including weekly MBA Mortgage Applications, November ADP, September import / export prices, September IP, and ISM Services.

OPTIONS: Expiries for Dec03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E611mln), $1.1625(E697mln)

- EUR/GBP: Gbp0.8885(E505mln)

- NZD/USD: $0.5730(N$622mln)

COMMODITIES: Recent Gains for WTI Futures Still Considered Corrective

- Recent gains in WTI futures are considered corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- The trend condition in Gold is unchanged and remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4009.2. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

EQUITIES: Climb Higher for Eurostoxx Futures Undermining a Bearish Theme

- Recent gains in Eurostoxx 50 futures undermine a recent bearish theme and the contract is holding on to its gains. Price has cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. A continuation would open 5742.40 next, a Fibonacci retracement point. For bears, a reversal lower would instead expose the key short-term support and bear trigger at 5475.00, the Nov 21 low. First support lies at 5609.26, the 50-day EMA.

- S&P E-Minis are holding on to their recent gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

| Date | GMT/Local | Impact | Country | Event |

| 03/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 03/12/2025 | 1315/0815 | *** | ADP Employment Report | |

| 03/12/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 03/12/2025 | 1330/1430 | ECB Lagarde Statement at ECON Hearing | ||

| 03/12/2025 | 1415/0915 | *** | Industrial Production | |

| 03/12/2025 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 03/12/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 03/12/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 03/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 03/12/2025 | 1530/1630 | ECB Lagarde Statement at ECON Hearing (as ESRB Chair) | ||

| 03/12/2025 | 1700/1700 | BOE Mann in Panel on Reserve Currencies | ||

| 04/12/2025 | 0030/1130 | ** | Trade Balance | |

| 04/12/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 04/12/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 04/12/2025 | 0800/0900 | ** | Unemployment | |

| 04/12/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/12/2025 | 0930/0930 | BOE Decision Maker Panel Data | ||

| 04/12/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/12/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 04/12/2025 | 1245/1245 | BOE Mann Panel at European and Global Issues Conference | ||

| 04/12/2025 | 1300/1400 | ECB Cipollone Chairs Panel on Fiscal Policy | ||

| 04/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 04/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 04/12/2025 | 1500/1000 | * | Ivey PMI | |

| 04/12/2025 | 1500/1600 | ECB Lane at Fiscal Policy Conference | ||

| 04/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 04/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/12/2025 | 1700/1200 | Fed Vice Chair Michelle Bowman | ||

| 04/12/2025 | 1800/1900 | ECB de Guindos Speech at Business Innovation Awards | ||

| 05/12/2025 | 2330/0830 | ** | Household spending |