US OUTLOOK/OPINION: Weekly Tracking Suggests ADP Downside Surprise

ADP private employment is expected to have increased by a mild 10k in November although weekly tracking points to a non-trivial decline. It should be an important update on labor demand with the FOMC going into next week’s meeting and a new forecast round with the last BLS payrolls report only for September.

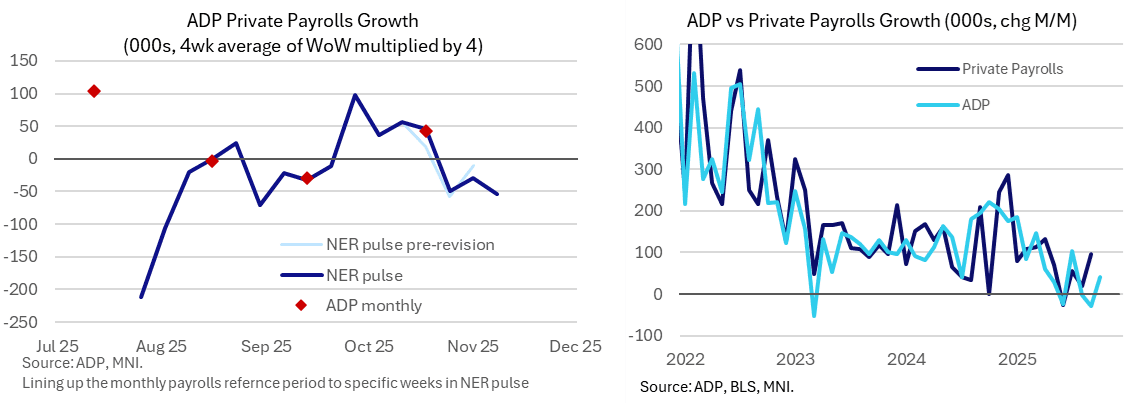

- Ahead of today's 0815ET release, Bloomberg consensus sees ADP employment growth of 10k in November after 42k in October although the former looks optimistic compared to recent weekly ADP tracking.

- Last week’s ADP NER Pulse update saw an average weekly change of -13.5k in the four weeks up to Nov 8, i.e. closer to a -55k decline on a rolling monthly basis.

- In theory, this monthly report should offer limited new information from that in the weekly series as, broadly mimicking the BLS payrolls report, its reference period is the week including the 12th of the month.

- The weekly series is prone to revisions although we’d be surprised if they were strong enough to materially alter a weak trend that has seen three weeks averaging -11k (on the same four-week rolling basis, i.e. closer to -45k in monthly terms).

- For context of last month’s release, monthly ADP employment increased 42k in October vs latest weekly data at the time showing 57k and Bloomberg consensus of 30k. Since then, the current vintage for the weekly tracker points to a ~46k increase.

- If we do indeed see a negative ADP employment print for November, it would mark a third monthly decline in the latest four months of data, with -3k in Aug, -29k in Sep and +42k in Oct.

- The broader momentum in the series should be viewed as an important indicator for jobs growth, with the three-month average slowing through the year to date (200k in Dec 2024, 139k in Mar, 22k in Jun, 24k in Sep and just 3k most recently in Oct).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (Z5) Key Support Remains Exposed

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-06 20-day EMA

- PRICE: 112-25+ @ 10:48 GMT Nov 3

- SUP 1: 112-16 Low Oct 30

- SUP 2: 112-14 Low Oct 9

- SUP 3: 112-06 Low Sep 25 and a reversal trigger

- SUP 4: 111-30 Trendline support drawn from the May 22 low

Recent weakness in Treasuries undermines a bullish theme. The contract has traded through the 50-day EMA, at 112-26+, highlighting potential for a deeper retracement near-term. A continuation lower would open 112-06, the Sep 25 low and the next key support. On the upside, the contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

EQUITY OPTIONS: Large Deutsche Bank Put Option

DBK (21st Nov) 30.5p, traded for 0.57 in 10k.

FOREX: GBP Selloff Consolidating, BOE Decision Due Thursday

- UK fiscal developments have been key in shaping the short-term trajectory for sterling, however, there might be greater focus this week on the BOE decision, of which the outcome is far from certain. Indeed, we would categorise our own view as 50/50 between a 25bp cut and a hold given the downside surprises to inflation and wage growth.

- Despite Friday’s GBPUSD close above, last week’s breach of key 1.3142 support is a meaningful development for the pair, strengthening current bearish conditions. Last week’s low at 1.3097 represents the immediate level of note, while more meaningful support is at 1.3041, the Apr 14 low. Below here, support appears scant until 1.2709, the April 07 low.

- EURGBP has weakened a touch to start the week, with the cross returning to the prior breakout point of 0.8769. Note that the overall trend is overbought, and this pullback is considered corrective at this juncture, with initial support coming in at 0.8751, the Sep 25 high. Topside targets for the broader rally include 0.8835 and 0.8875, the April 2023 high.

- Another cross that will remain in focus is GBPAUD, especially given the RBA decision on Tuesday. A break of the recent cycle lows at 2.0244 significantly boosted downside momentum, with the cross printing below 2.00 last week, the lowest level in 8 months. Consolidating weakness may signal scope for an extension lower towards the year’s lows around 1.96.

- Elsewhere this week, DMP data is scheduled after the BOE, which could hint at whether December is in play, while markets will also pay attention to final services PMI figures.