MNI US MARKETS ANALYSIS - USD Index Looks for Fresh Catalysts

Highlights:

- Treasuries pare midweek support ahead of weekly jobless claims

- USD Index needs fresh catalysts for conviction in either direction

- Trump's targeting of Brazil triggers acute BRL sell-off

US TSYS: Bonds Pare Midweek Support, Weekly Claims Ahead, MNI Hosts SF Daly

- Treasuries are trading near steady to mixed, curves twist mildly steeper with bonds unwinding a fraction of Wednesday's rally. Similar moves in EGBs overnight, Gilts off Asia hour highs, while a bearish theme in Bunds remains intact.

- Currently, the Sep'25 10Y contract trades -.5 at 111-08 (111-05 low / 111-13.5 high), initial technical support below at 110-21.5/17 (Low Jul 8 / 61.8% of the May 22 - Jul 1 bull leg), resistance to watch is at 111-28, the Jul 3 high.

- Economic data limited to weekly jobless claims at 0830ET, est 235k vs 233k prior, continuing claims est 1.965M from 1.964M prior.

- Scheduled Fed speakers: StL Fed President Musalem moderated discussion on the economy (livestreamed) at 0900ET. Meanwhile, MNI hosts a moderated discussion with SF Fed President Mary Daly at 1430ET.

- Treasury auctions include $80B 4W & $70B 8W bills at 1130ET, $22B 30Y Bond auction re-open (912810UK2) at 1300ET.

- Projected rate cuts through year end remain largely steady after yesterday's rally, Dec'25 holding just above -50bp.

US TSY FUTURES: Mix Of Long Setting & Short Cover Seen Wednesday

OI data points to net long setting in the intermediate zone (FV, TY & UXY futures) during Wednesday’s uptick in futures, which was largely offset (from a curve-wide DV01 perspective) by net short cover in the wings (TU, US & WN).

- Net long setting in FV futures provided the only DV01 shift of any real note, with the remainder of the net positioning swings seemingly modest on the day.

| 09-Jul-25 | 08-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,346,779 | 4,354,255 | -7,476 | -284,422 |

FV | 7,038,671 | 7,006,881 | +31,790 | +1,372,446 |

TY | 4,915,690 | 4,915,665 | +25 | +1,652 |

UXY | 2,415,922 | 2,415,810 | +112 | +9,783 |

US | 1,825,583 | 1,829,771 | -4,188 | -580,001 |

WN | 1,959,556 | 1,960,806 | -1,250 | -229,330 |

|

| Total | +19,013 | +290,129 |

SOFR: Net Long Setting In The Whites Dominated On Wednesday

I data points to relatively meaningful net long setting in white SOFR futures on Wednesday, with net long setting also dominating in the greens and blues.

- Positioning in the reds went against the broader theme, with net short cover seen in 3 of the 4 contracts, biasing the net pack positioning move in that direction.

| 09-Jul-25 | 08-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,321,291 | 1,302,860 | +18,431 | Whites | +73,322 |

SFRU5 | 1,200,529 | 1,180,825 | +19,704 | Reds | -5,425 |

SFRZ5 | 1,300,814 | 1,282,502 | +18,312 | Greens | +9,380 |

SFRH6 | 999,445 | 982,570 | +16,875 | Blues | +19,438 |

SFRM6 | 843,423 | 849,186 | -5,763 |

|

|

SFRU6 | 831,330 | 817,888 | +13,442 |

|

|

SFRZ6 | 886,699 | 899,590 | -12,891 |

|

|

SFRH7 | 719,950 | 720,163 | -213 |

|

|

SFRM7 | 671,356 | 668,274 | +3,082 |

|

|

SFRU7 | 471,018 | 471,345 | -327 |

|

|

SFRZ7 | 418,566 | 414,134 | +4,432 |

|

|

SFRH8 | 316,971 | 314,778 | +2,193 |

|

|

SFRM8 | 232,456 | 230,689 | +1,767 |

|

|

SFRU8 | 200,893 | 199,159 | +1,734 |

|

|

SFRZ8 | 201,583 | 185,482 | +16,101 |

|

|

SFRH9 | 140,918 | 141,082 | -164 |

|

|

FOREX: Tariff Letters Show Trump Not Shy of Surprising Markets

- As more tariff letters dropped late yesterday, markets were again caught offguard at Trump's willingness to surprise markets - this time by inflicting a 50% tariff rate on Brazil due to the country's pursuit of former President Bolsonaro, a key Trump ally. The local currency sold off aggressively, putting USD/BRL at new July highs - although the spillover into G10 FX was much more muted - however the brief spell of USD sales in response to the headline persists headed through to the NY crossover.

- For now, this keeps broader market conditions in step with the themes from earlier this week. AUD/USD remains firm, with an underlying bull trend aided by the recovery off weekly lows and the firm hold of 50-dma support at 0.6483. Further strength here would need to top 0.6590 resistance, a break above which puts the pair at YTD highs and resumes the underlying bull trend.

- While the USD Index is softer, it is still operating above the base in prices established earlier this month. The dominance of the USD downtrend posted off the early February has helped define price action across Trump's term so far - and that remains the order of markets for now. Any fresh catalysts this month (US CPI on July 15th, Fed decision on July 30th) will need to press the USD either back below the downtrendline (today at 97.083) or above the 50-dma at 98.913 to trigger fresh price action here.

- Weekly jobless claims data are the sole US data release due Thursday, with markets watching for another tick higher in initial jobless claims to 235k. The central bank speaker slate is busier, with ECB's Villeroy, BoE's Breeden and Fed's Musalem & Daly all set to speak.

BRAZIL: Trump’s 50% Tariff Announcement Sparks Punchy BRL Selloff

- The Brazilian real had already been under pressure late Wednesday as President Trump stated that “Brazil has not been good to us” in comments that preceded the significant announcement of 50% tariffs to be imposed from August 01. The second leg of BRL weakness prompted a dramatic spike for USDBRL to 5.60, extending the pair’s advance to 2.88% before settling around 5.57 into the close.

- This announcement represents a major escalation from the 10% rate imports from Brazil to the US have faced since April and while the potential economic impact is clear, it is the political angle to Trump’s latest action that might be particularly poignant for markets.

- Trump’s opening paragraph detailing the “witch hunt” surrounding former president Jair Bolsonaro, who remains barred from running in the next election, is likely to have unnerved investors who have enjoyed a stellar performance across Brazilian assets in 2025. With an already fragile fiscal backdrop and the upcoming election in 2026, Trump’s latest actions are likely to stoke domestic political uncertainty significantly.

- Sure enough, Lula’s initial response has been resolute, announcing that “Brazil is a sovereign nation with independent institutions and will not accept any form of tutelage,” posting on X. “Any measure to increase tariffs unilaterally will be responded to in light of Brazil’s Law of Economic Reciprocity,” the Brazilian President added.

- JP Morgan have said that if this 50% tariff scenario becomes long-lasting, Brazil's GDP could potentially be reduced by 0.8%-1.2% of GDP. However, JPM are not changing their GDP growth or trade balance forecasts at present given the uncertainty around both tariff levels and their timing as experienced by other countries.

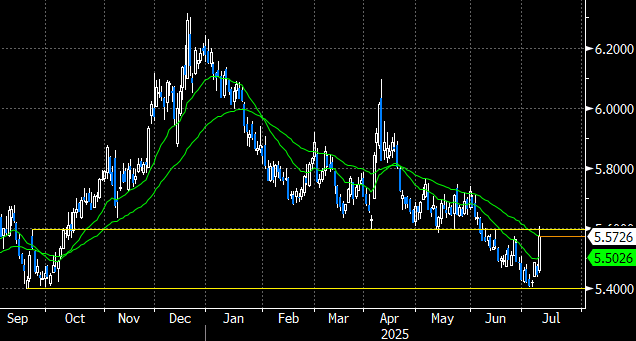

BRAZIL: 5.60 Pivot Point Remains Key Short-Term Parameter for USDBRL

- While very much a fundamental swing, USDBRL’s bounce has been assisted by a firmer US dollar in recent sessions and the notable hold of a key medium-term support level, residing at 5.40. This cluster of daily lows from Sep/Oct last year were a focus point before the powerful rally to 6.30 in December that prompted multiple bouts of intervention from the BCB.

- Earlier in the year, 5.60 had proved an important support level, which after breaking, exacerbated USDBRL’s decline across June. Yesterday’s spike into the close retested this level, as well as the 50-day EMA, which now intersects around 5.5750. A sustained break above 5.60 in coming session would be a meaningful bullish development and initially target a move to firm resistance at 5.7632, the May 7 high.

- Goldman Sachs point out that while the political inclination may be to retaliate, they anticipate local exporters to urge the administration to de-escalate. This would likely be required to allow markets to focus on the positive attributes of the BRL outlook once again.

- HSBC believe this is a near-term game changer for the BRL that puts a firm end to the recent rally. That said, it is important to remember that we have been here before - similar escalation with Colombia in January was swiftly resolved through diplomatic back channels - but until this happens, they expect BRL to remain on the back foot.

Source: Bloomberg Finance L.P. / MNI

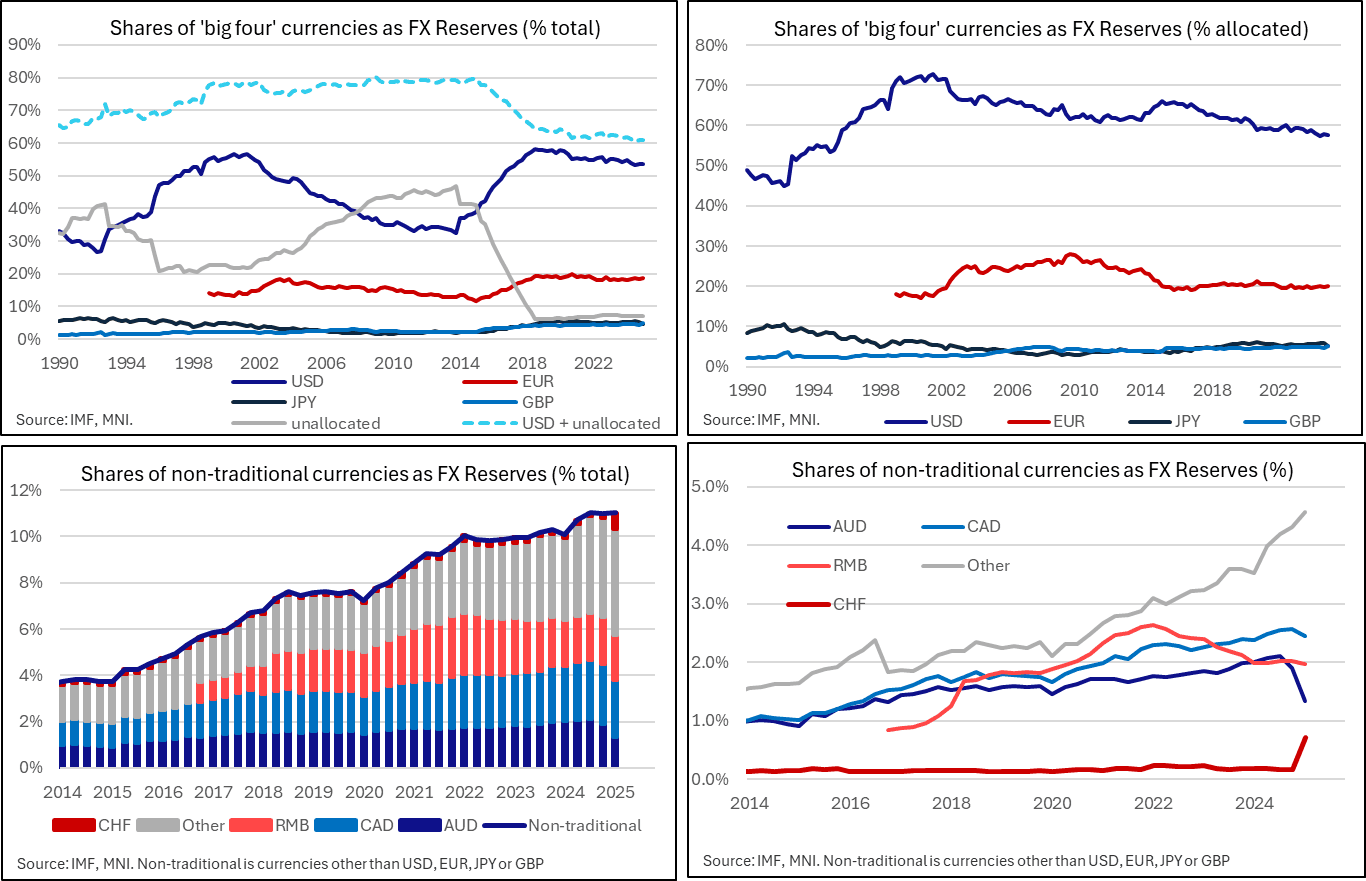

FOREX: USD Share Of Global FX Reserves Steady In Q1, Larges Swings In AUD, CHF

Latest IMF COFER data for Q1 2025 showed the US dollar’s share of total global FX reserves unchanged at 53.6%, the lowest level since Q2 2017. The USD’s share of “allocated” reserves (i.e. those reported in sufficient detail) was similarly little changed at 57.7% (vs 57.8% In Q4). A reminder that this data does not capture any US Liberation Day-induced changes in reserves.

- Looking at the other “big four” currencies, the EUR’s share of allocated reserves ticked up to 20.1% (vs 19.8% in Q4, 20.0% in Q3). In its annual report on the Euro, the ECB noted that “further shifts may be underway in the landscape of international currencies. The tariffs imposed by the US Administration have led to highly unusual cross-asset correlations. This could strengthen the global role of the euro and underscores the importance for European policymakers of creating the necessary conditions for this to occur.”

- The JPY saw a more notable fall in its allocated share to 5.1%, from 5.8% in Q4. Meanwhile, GBP’s share ticked up to 5.2% (vs 4.7% in Q4, 5.0% in Q3).

- More interesting developments were seen amongst non-traditional (i.e. not USD, EUR, JPY, GBP) currencies. CHF’s share of allocated reserves shot up to 0.8% from 0.2% in Q4. That’s a quarterly increase worth ~7% GDP after converting to local currency.

- Meanwhile, AUD’s share of allocated reserves dropped to 1.4% from 2.1% prior, the lowest since reporting began in Q4 2012.

FOREX: Analysts Caution Over-interpretation Of AUD/CHF FX Reserve Swings

Some analysts have emphasised the need for caution when interpreting the IMF COFER data though, particularly with respect to the swings in CHF and AUD (and to a lesser extent JPY) reserves.

- Goldman Sachs: “The curious drop in AUD (-68bn) and JPY (-68bn) reserves, with a corresponding surge in CHF (+68bn) reserves is puzzling. This marks the largest 1-quarter change for each currency, and by some margin. Given the magnitude, and no clear market catalyst, we think this most likely indicates a shift in strategy from one large reserve manager rather than a broader adjustment”.

- “But, we do not see a corresponding entry in other financial flow data, like the BoP for these countries. The lack of price impact is the most noticeable, and leaves us skeptical that this represented a genuine shift in final currency exposure”.

- “To give a sense of the magnitude, the SNB intervened by roughly this amount in the aftermath of the Brexit Referendum in 2016. It seems unlikely that these flows could have gone through with little discernible impact on CHF in Q1. We expect to investigate further, but for now take these sharp shifts with a large grain of salt”.

- Standard Chartered: “The IMF data show changes of more than 30% in holdings of AUD and CHF reserves. These are very large, and we would not be surprised if they are revised. We would treat the COFER data cautiously, and would want to be confident in all of the reserve numbers before drawing strong conclusions”.

- Additionally, it's worth remembering that changes in FX reserve shares do not account for other methods of reserve diversification, for example in Gold. 95% of respondent's to the World Gold Council's 2025 Central Bank Gold Reserves Survey believe total central bank gold reserves will rise over the next 12 months. In a similar vein, "a record 43% of respondents believe that their own gold reserves will also increase over the same period", while "none of our respondents anticipate a decline in their gold reserves."

- That report also noted a “majority of respondents (73%) see moderate or significantly lower US dollar holdings within global reserves over the next five years. Respondents also believe that the share of other currencies, such as the euro and renminbi, as well as gold, will increase over the same period"

OPTIONS: Expiries for Jul10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E2.5bln), $1.1685-00(E1.5bln), $1.1710-20(E616mln), $1.1735-50(E1.5bln), $1.1800(E1.3bln)

- USD/JPY: Y143.95-15($1.0bln), Y144.70-90($1.3bln), Y146.50-55($681mln), Y147.00($832mln)

- GBP/USD: $1.3490-10(Gbp529mln), $1.3570(Gbp540mln)

- EUR/GBP: Gbp0.8595-00(E815mln)

- AUD/USD: $0.6440-55(A$954mln), $0.6500(A$599mln), $0.6415-25(A$589mln), $0.6600(A$634mln)

- NZD/USD: $0.6000(N$517mln)

- USD/CAD: C$1.3625-35($1.0bln)

EQUITIES: Eurostoxx 50 Futures Narrow Gap to Key Resistance and Bull Trigger

- Eurostoxx 50 futures have traded higher this week as the contract extends the recovery that started Jun 23. This exposed key resistance and the bull trigger at 5486.00, the May 20 high. It has been pierced, a clear break would confirm a resumption of the medium-term bull cycle that began Apr 7, and would open the 5500.00 handle. On the downside key support has been defined at 5194.00, the Jun 23 low.

- The trend condition in S&P E-Minis remains bullish and the contract is trading closer to its recent highs. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This was followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6032.93.

COMMODITIES: Gold 50-Day EMA Support Holding for Now

- WTI futures maintain a bearish tone following the reversal from the Jun 23 high, and recent gains are considered corrective. Support to watch is the 50-day EMA, at $65.22. The average has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high.

- Recent weakness in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5, May 29 low. Note, the recovery from the Jun 30 low also highlights a possible false t-line break. A resumption of gains would refocus attention on $3451.3, Jun 16 high. The bear trigger is $3248.7, Jun 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 10/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 10/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 10/07/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 10/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 10/07/2025 | 1500/1600 | BOE Breeden On Climate Change | ||

| 10/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 10/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 10/07/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 10/07/2025 | 1715/1315 | Fed Governor Christopher Waller | ||

| 10/07/2025 | 1830/1430 | Fed's Mary Daly at MNI | ||

| 11/07/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 11/07/2025 | 0600/0700 | ** | Trade Balance | |

| 11/07/2025 | 0600/0700 | ** | Index of Services | |

| 11/07/2025 | 0600/0700 | ** | Index of Production | |

| 11/07/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 11/07/2025 | 0645/0845 | *** | HICP (f) | |

| 11/07/2025 | 1130/1330 | ECB Cipollone At Ukraine Recovery Conference | ||

| 11/07/2025 | - | *** | Money Supply | |

| 11/07/2025 | - | *** | New Loans | |

| 11/07/2025 | - | *** | Social Financing | |

| 11/07/2025 | 1230/0830 | *** | Labour Force Survey | |

| 11/07/2025 | 1230/0830 | * | Building Permits | |

| 11/07/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1800/1400 | ** | Treasury Budget |