MNI US MARKETS ANALYSIS - US30YY Rebuts Test of 5.00%

Highlights:

- JOLTS data in focus, markets look for clues into Friday NFP

- UK Chancellor fixes November 26th for Autumn Budget; Tax-and-spend in focus

- Long-end yields remain sensitive, although US 30y holds below 5.00%

US TSYS: 30Y Test Of 5.00% Rebutted, JOLTS In Focus

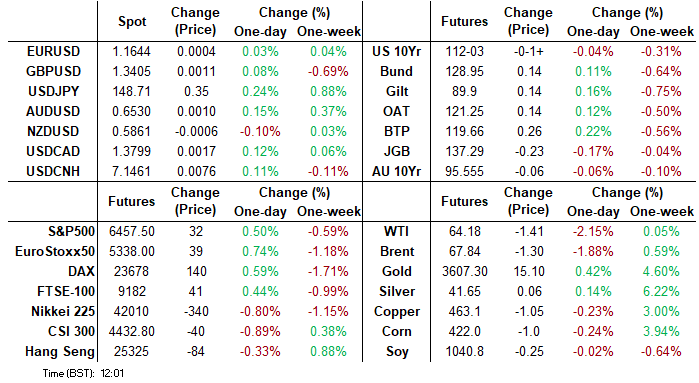

- Treasuries are modestly lower across the curve, for the most part having remained within yesterday’s range although with 30s earlier extending lows as yields briefly tried to test 5.00%.

- Today sees focus on the JOLTS report but with Musalem and the Beige Book also worth watching from a Fed angle as well as potential headlines from President Trump from 1100ET onwards.

- Cash yields are 1.2-2.8bp higher on the day, with increases led by the belly and 30s lagging.

- 30Y yields earlier topped out at 4.9997% (currently 4.974%) having last exceeded 5.00% on Jul 18.

- Curves again saw fresh ytd steeps overnight before pulling back, with 5s30s hitting 124.6bps and currently at session lows of 122.5bps ahead of the US session.

- TYZ5 trades at 112-03 (-01+) on mild volumes of 270k, having coming close to yesterday’s low of 111-31 but remained within range throughout.

- Yesterday’s low probed support at 111-31+ (20-day EMA) after which lies 111-19 (50-day EMA) with the recent pullback deemed corrective. Resistance is seen at 112-20+ (Aug 28/29 high).

- Data: MBA mortgage applications (0700ET), JOLTS Jul (1000ET), Factory orders Jul (1000ET), Wards vehicle sales Aug

- Fedspeak: Musalem on economy and policy (0900ET), Beige Book (1400ET)

- Bill issuance: US Tsy $65B 17W bill auction (1130ET)

- Politics: Trump in bilateral meeting with President of the Republic of Poland (1120ET, WH press pool)

- Note that the District Court-level decision in Fed Gov Cook's lawsuit didn't materialize yesterday as the judge gave the Justice Department until Thursday to file another brief.

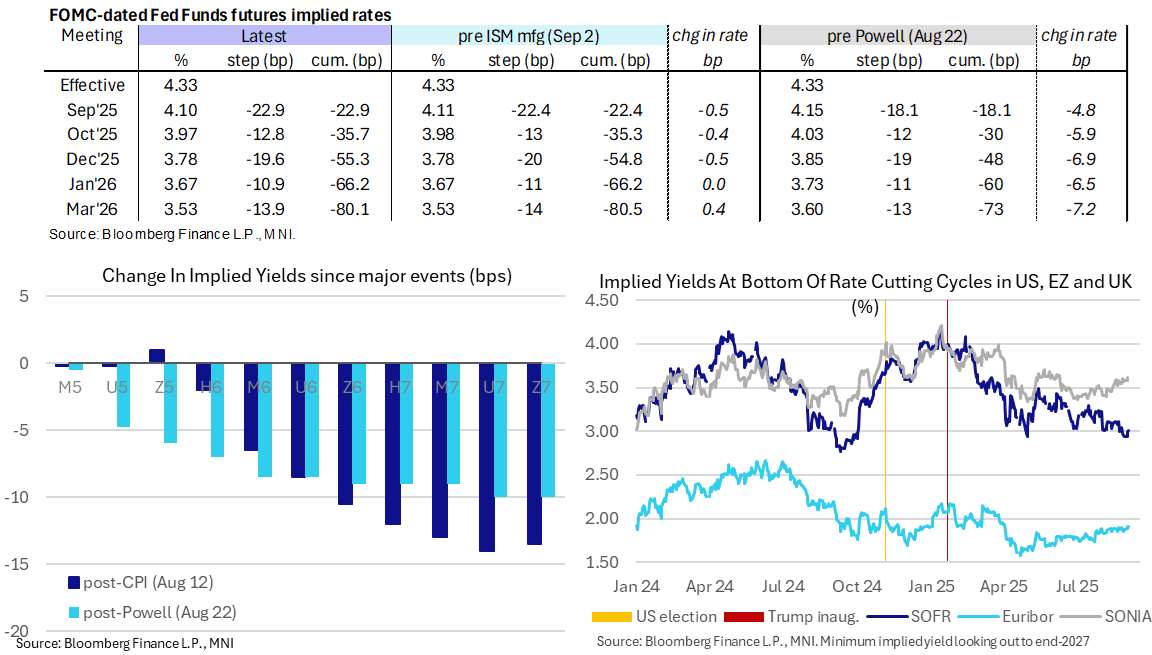

STIR: 55bp Of Fed Cuts To Year-End Ahead Of Musalem, JOLTS and Then Beige Book

- Fed Funds implied rates are up to 1bp higher on the day for meetings out to Mar 2026 but hold within recent ranges ahead, with little sign of net impact from crude oil futures sliding on Reuters suggesting OPEC is considering further supply hikes.

- Today’s JOLTS report sees the start of the week’s labor data build up to payrolls on Friday, with ADP coming tomorrow owing to a Labor Day delay.

- Cumulative cuts from 4.33% effective: 23bp Sep, 35.5bp Oct, 55.5bp Dec, 66bp Jan and 80bp Mar.

- SOFR futures are up to 1.5 ticks lower on the day out through 2027 contracts.

- The SOFR implied terminal yield of 3.01% (still SFRH7) is 1bp higher, off last week’s multi-month lows of ~2.95% but still pointing to more than 130bp of cuts from current levels.

- St Louis Fed’s Musalem (’25 voter, hawk) speaks on the economy and policy at the Peterson Institute at 0900ET (text tbd, Q&A). We imagine risks are skewed to the dovish side considering his usually hawkish stance. He said Aug 14 that inflation seems to be running close to 3%, he expects the tariff inflation impact to fade in 2-3 quarters but that there was a reasonable possibility it could be more persistent. He saw the labor market at full employment but with risks to the downside.

- Fed Beige Book (1400ET). With a focus on labor developments ahead of Friday’s payrolls report, recall that July’s Beige Book characterized the labor market in fairly mixed fashion, though generally stable to slightly-positive across most Fed Districts compared with the June beige book. It was arguably the most solid Beige Book on the employment front since the start of the year.

SOFR: Mix Of Short Setting & Long Cover Seen In Most Futures On Tuesday

OI data suggests that a mix of net short setting and long cover was seen in most SOFR futures on Tuesday, with net short setting dominating in the whites and greens, while net long cover was slightly more prominent in the reds.

| 02-Sep-25 | 01-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,166,953 | 1,160,164 | +6,789 | Whites | +62,253 |

SFRU5 | 1,454,004 | 1,443,674 | +10,330 | Reds | -9,943 |

SFRZ5 | 1,546,924 | 1,523,850 | +23,074 | Greens | +57,548 |

SFRH6 | 1,147,888 | 1,125,828 | +22,060 | Blues | +865 |

SFRM6 | 939,376 | 922,771 | +16,605 |

|

|

SFRU6 | 890,464 | 903,283 | -12,819 |

|

|

SFRZ6 | 962,548 | 961,579 | +969 |

|

|

SFRH7 | 724,472 | 739,170 | -14,698 |

|

|

SFRM7 | 817,855 | 798,278 | +19,577 |

|

|

SFRU7 | 638,904 | 637,480 | +1,424 |

|

|

SFRZ7 | 647,815 | 623,292 | +24,523 |

|

|

SFRH8 | 414,910 | 402,886 | +12,024 |

|

|

SFRM8 | 336,559 | 339,727 | -3,168 |

|

|

SFRU8 | 221,803 | 218,161 | +3,642 |

|

|

SFRZ8 | 246,786 | 245,819 | +967 |

|

|

SFRH9 | 162,024 | 162,600 | -576 |

|

|

EUROPE ISSUANCE UPDATE:

Lithuania dual tranche syndication: Update

- EUR benchmark (MNI pencils in E1bln) of the new long 10-year Mar-30 LITHUN. Guidance revised to MS + 95-100bp (WPIR) (Initial guidance was MS+105bp area)

- EUR benchmark (MNI pencils in E1bln) of the new 20-year Sep-45 LITHUN. Spread set at MS +140bp (guidance was MS+145bp area)

German auction results

- E5bln (E3.81bln allotted) of the 2.60% Aug-35 Bund. Avg yield 2.77% (bid-to-offer 1.10x; bid-to-cover 1.45x).

UK FISCAL: Reeves Claims "UK Economy Is Not Broken" As 26 Nov Budget Confirmed

In a video clip posted to X announcing the date of the budget (26 Nov), Chancellor of the Exchequer Rachel Reeves claims "Britain's economy isn't broken, but I do know that it's not working well enough for working people. Bills are too high and you feel that you're putting in but you're getting less out."

- Reeves: "...But there are still challenges. The cost of living pressures I know are still very real. We need to bring inflation and borrowing costs down. We do that by keeping a tight grip on day-to-day spending and by enforcing my non-negotiatble fiscal rules."

- Reeves: "Renewal is our mission, and growth is our challenge. Investment and reform are our tools..."

- Politically, the chancellor and wider gov't remain in a very difficult position. It faces an increasingly sceptical gilt market, a decades-high tax burden that risks deterring investment, manifesto pledges not to raise income tax, VAT or employee National Insurance contributions, and a sizeable wing of the parliamentary Labour party fully opposed to any further gov't spending cuts.

BOE: Four MPC Members to Testify Ahead of TSC This Afternoon

- Four BOE MPC members will testify ahead of the Treasury Select Committee with regards to the August MPR on Wednesday. We will hear from Governor Bailey, Deputy Governor Lombardelli as well as external members Greene and Taylor.

- The main focus will be on Governor Bailey's remarks,. We think that he is the key swing voter and his vote is likely a necessity if we are to see a November or December cut (which at the time of writing only had 5bp and 10bp cumulatively priced). Therefore any comments he makes on his views of the economy, the need for an imminent cut or the rationale for skipping a quarterly cut would be hugely important for the market.

- Lombardelli gave little away regarding her personal view at the MPR press conference early in August but noted that she would elaborate on her rationale for a hawkish dissent (to keep Bank Rate on hold) in this forum. It's not clear how committed she is to Bank Rate remaining on hold (although there is nothing since the August decision has indicated that a change in view that a "skip" would not be favoured). If she sounds clearly open to a November cut that would be a dovish development. We would expect her to at least say that the future path of rates is down but that timing is uncertain for the next move - if she does not say this then it would be a hawkish signal.

- Similarly Greene has not made any notable public comments since her dissent in August either. She is still considered one of the more hawkish members, so unless she changes tone considerably it is unlikely her comments will be market moving unless she warns that there is the potential Bank Rate may have reached its lowest level and that no further cuts would likely in her opinion.

- Taylor is also known to be a dove - and favoured a larger 50bp cut in August (cementing him as the most dovish member of the Committee). As he is clearly a bit of an outlier in terms of his views, again his comments are unlikely to be that market moving.

- Breeden is due to speak separately this morning, but is unlikely to discuss monetary policy.

FOREX: JPY Underperforms For Second Session

- JPY is the poorest performer in G10 - as was the case ahead of the US open yesterday - as yawning yield spreads against the US and further stress in longer-end global yields favours USD/JPY. The pair crossed the 200-dma overnight at 148.86 - pierced for the first time since early August.

- GBP trades poorly again Wednesday, as the UK government confirmed the date of the Autumn Budget - November 26th - which should shift focus to potential policy leaks and trial balloons from the Chancellor as she looks to gauge market response to future plans to plug the hole in public finances, likely via further tax revenue raising measures (likely targeting property), although further speculation that the government could ditch their manifesto pledge of not raising national insurance, income tax or VAT rather than raising indirect taxes.

- The growing negative correlation between longer-end yields and GBP extending this morning. The recent drop in spot and renewed fiscal concerns are supporting a bid in vols: 3m implied has been marked higher to 8 points this morning, erasing the summer lull and returning above the YTD average of 7.8 points. This raises the risk of GBP/USD downside in the coming months, isolating 1.3144/42 as key support - the 38.2% retracement for the YTD upleg, as well as the August 1st low.

- US JOLTs data is the market focus for the US session - and as was the case for the ISM data yesterday, markets will be looking to gauge labour market strength into this Friday's payrolls report. Fed's Musalem is set to speak on the economy and policy ahead of the later release of the Beige Book, while BoE MPC members appear in front of the Treasury Select Committee at 1415BST/0915ET.

GBP: Options Augur Against GBP, Highlighting S/T Downside Risks

- The growing negative correlation between longer-end yields and GBP is extending this morning. The recent drop in spot and renewed fiscal concerns are supporting a bid in vols: 3m implied has been marked higher to 8 points this morning, erasing the summer lull and returning above the YTD average of 7.8 points (which is already well above 2024's 6.9 points).

- In tandem, the front end of the GBP risk reversals curve has deteriorated: dropping to lowest since March against USD and lowest since July against EUR - signalling decent demand for GBP downside insurance covering the rest of 2025 - despite the continued pricing-out of further rate cuts into year-end 2025.

- GBP options activity was ahead of average yesterday, and that trend's persisted into Wednesday: decent demand for downside exposure is the driver here. So far today, close to $4 in puts have traded for every $1 in calls, with 1.31 and 1.29 put strikes garnering the most notable interest. Some of the more sizeable trades across these strikes are consistent with put spreads targeting an October/November expiry - so rolling off just prior to the UK Budget on November 26th with a break-even below ~1.3025 at expiry.

- As a result, the GBPUSD vol surface is leaning further in favour of OTM puts, tipping the GBPUSD SMILE to its sharpest skew since the April Liberation Day vol episode. This raises the risk of GBP/USD downside in the coming months, isolating 1.3144/42 as key support - the 38.2% retracement for the YTD upleg, as well as the August 1st low.

- Scrutiny over UK press will now increase: policy proposals are usually floated in the media ahead of the Budget - allowing ministers to phase-in any fiscal bad news and retain rabbit-in-the-hat style positive policy surprises on Budget Day itself.

OPTIONS: Expiries for Sep03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1455(E2.2bln), $1.1525(E919mln), $1.1575-95(E1.5bln), $1.1600(E825mln), $1.1645-50(E792mln), $1.1675-80(E1.1bln), $1.1700(E1.1bln)

- USD/JPY: Y145.00($865mln), Y145.50($976mln), Y146.50($1.4bln), Y147.15-30($1.6bln), Y148.00($595mln), Y149.00($508mln)

- GBP/USD: $1.3500(Gbp507mln)

- AUD/USD: $0.6475(A$570mln)

EQUITIES: Tuesday's Pullback for E-Mini S&P Considered Corrective

- The primary trend set-up in Eurostoxx 50 futures is bullish and the pullback from the Aug 22 high appears corrective. However, the contract has breached 5372.85, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5392.75, the 20-day EMA.

- A bull cycle in S&P E-Minis remains intact and the latest pullback is - for now - considered corrective. Price has traded through the 20-day EMA. The key support to watch lies at the 50-day EMA, at 6336.02. A clear break of this EMA is required to signal scope for a deeper retracement. This would open 6239.50, the Aug 1 low and a key support. Moving average studies still highlight a dominant uptrend. The bull trigger is 6523.00, the Aug 28 high.

COMMODITIES: Gold Remains in a Clear Bull Cycle

- A bear cycle in WTI futures remains intact and the latest bull phase appears to be a correction. This short-term corrective cycle remains in play and Tuesday’s rally reinforces this theme. Initial resistance to watch is $66.56, the Aug 4 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. A resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

- Gold remains in a clear bull cycle. This week’s gains have resulted in a breach of key resistance at $3500.1, the Apr 22 high, and delivered a fresh all-time high in the yellow metal. The break confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is the $3600.00 handle. Initial firm support to watch lies at $3396.2, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 03/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 03/09/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/09/2025 | 1300/0900 | St. Louis Fed's Alberto Musalem | ||

| 03/09/2025 | 1315/1415 | BOE testify at TSC: Bailey, Greene, Lombardelli, Taylor | ||

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1730/1330 | Minneapolis Fed's Neel Kashkari | ||

| 03/09/2025 | 1800/1400 | Fed Beige Book | ||

| 04/09/2025 | 0130/1130 | ** | Trade Balance | |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0630/0830 | *** | CPI | |

| 04/09/2025 | 0700/0900 | ** | Unemployment | |

| 04/09/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/09/2025 | 0830/0930 | Decision Maker Panel data | ||

| 04/09/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/09/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 04/09/2025 | 0900/1100 | ** | EZ Retail Sales | |

| 04/09/2025 | 0930/1130 | ECB Cipollone Speaks at Digital Euro Hearing, European Parliament | ||

| 04/09/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 04/09/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/09/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/09/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/09/2025 | 1400/1000 | Fed nominee Stephen Miran | ||

| 04/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 04/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/09/2025 | 1600/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 04/09/2025 | 1600/1200 | ** | US DOE Petroleum Supply | |

| 04/09/2025 | 1605/1205 | New York Fed's John Williams |