MNI US MARKETS ANALYSIS - US Data Run in Focus

Highlights:

- Markets await strong run of US data, with advance GDP, MNI Chicago PMI and PCE price indices all due

- USD/JPY struggles to muster rally as markets remain in tariff limbo

- Treasury's Quarterly Refunding Announcement to be watched carefully for details on borrowing

US TSYS: Modestly Twist Flatter On Low Volumes Ahead Of An Important Docket

- Treasuries trade twist flatter as the front end modestly pares latest gains whilst the long end consolidates and in the case of 2-s and 30s builds upon prior gains.

- Weaker than expected Caterpillar results have weighed on equities but with little sign of spillover into Treasuries.

- Futures volumes have been subdued overnight ahead of a particularly heavy docket before further risk events after the equity cash close with results from Meta and Microsoft.

- Today sees the Treasury QRA at 0830ET (MNI preview) along with multiple data releases that include Q1 GDP (mini preview here) and March PCE (here).

- Cash yields are 1bp higher (2s and 3s) to 2bp lower (20s and 30s).

- 10Y yields at 4.162% eye 4.15% for the first time since early Apr 8, i.e. comfortably pre-tariff pause levels.

- TYM5 trades at 112-06 (+01) in a narrow range, consolidating yesterday’s rally with an overnight high of 112-09.

- Prior clearance of 111-25 (50% retrace of Apr 7-11 bear leg) has undermined a prior bearish theme and the contract has again stepped closer to latest resistance at 112-12 (61.8% retrace of the same bear leg). To the downside, support at 111-07+ (20-day EMA).

- Data: Weekly MBA data (0700ET), ADP employment Apr (0815ET), GDP Q1 advance (0830ET), Employment Cost Index Q1 (0830ET), MNI Chicago PMI Apr (0945ET), PCE report Mar (1000ET), Pending home sales Mar (1000ET)

- Bill issuance: US Tsy $60B 17W bill auction (1130ET)

- Full Treasury Quarterly Refunding Announcement (0830ET). Recent market volatility has reduced the possibility that Treasury will adjust its guidance that it will keep nominal coupon auction sizes unchanged for "at least the next several quarters", as changing this would signal an intention to increase bond supply in the near future. That view was further boosted by details in Monday's borrowing estimates.

STIR: US Rates Modestly Pare Yesterday’s Latest Rally Ahead Of Data Deluge

- Fed Funds implied rates are 0-2bp higher on the day for 2025 meetings, in a similar pattern to yesterday’s overnight session with a modest paring of the previous day’s large rally.

- Cumulative cuts from 4.33% effective: 2.5bp for next week, 17bp Jun, 38.5bp Jul and 95.5bp Dec.

- The ~96bp of cuts is off yesterday’s low of 98bps that marked its lowest since Apr 11.

- Further out the curve, SOFR futures have given back little of yesterday’s gains: SFRU6 (where the terminal yield currently sits at 2.985%) is just 1 tick higher on the day at 97.015 (overnight high 97.045) having returned to pre-tariff pause levels on Monday.

- Today sees a heavy data docket, including ADP employment, Q1 GDP, Q1 ECI, MNI Chicago PMI and the monthly PCE report in chronological order.

EUROPEAN INFLATION: German HICP/CPI Y/Y Expected To Decelerate By 0.1pp

German April inflation is scheduled for 13:00 BST / 14:00 CEST today - however, we will receive state-level data likely amounting to 89.1% of the national basked briefly after 09:00 BST / 10:00 CEST. We will provide analysis on that, drawing signals for the later, national print.

- BBG Consensus (national level):

- HICP 2.1% Y/Y (vs 2.3% prior); 0.4% M/M

- CPI 2.0% Y/Y prior (vs 2.2% prior); 0.3% M/M

- Analyst views:

- Goldman Sachs sees HICP 2.2% headline, 3.1% core. “Services inflation to increase, driven by a notable contribution from travel-related services due to the timing of Easter this year. We expect package holidays to print close to 6%mom nsa, and airfares to come in at 11%mom nsa but see scope for a stronger print.” They expect “unprocessed food inflation to increase to 7.1%, mostly driven by a base effect.”

- Barclays sees German package holidays at 5.6% Y/Y, accommodation at 2.6% and airfares at 16.0% (all Y/Y). They see NRW headline CPI at 0.38% M/M.

- Morgan Stanley sees energy CPI/HICP at -5.4% Y/Y “on lower inflation in fuels, as well as electricity and gas” but “core inflation to rise on the positive base effect from Easter” (core CPI at 2.9%, core HICP 3.3%)

- The Bundesbank highlights in their April monthly report: “The inflation outlook is currently characterised by particular uncertainty. Prices on the energy markets have tended to decline recently, amid high volatility, and the euro has tended to appreciate against the US dollar. Based on the oil price path derived from forward prices and on the US dollar/euro exchange rate as this report went to press, the inflation rate is expected to be even somewhat lower in the near future."

- The April flash PMI noted “a slight uptick in the rate of inflation in average prices charged for goods and services. The acceleration from March’s four-month low was driven by a first – albeit marginal – increase in factory gate charges in almost two years. Services firms continued to display the stronger pricing power, although the latest increase in services output charges was the weakest since last October.”

EUROPEAN INFLATION: German HICP/CPI Y/Y Expected To Decelerate By 0.1pp

Recap: German final March HICP was unrevised from the flash readings at 2.3% Y/Y (2.6% prior) and 0.4% M/M (0.5% prior). The final reading of national CPI was also unrevised at 2.2% Y/Y (2.3% prior) and 0.3% M/M (0.4% prior). Core CPI printed at 2.6% Y/Y (0.1pp upwardly revised, 2.7% prior), the lowest rate since June 2021.

- Overall, the CPI data confirmed a notable deceleration in services Y/Y inflation (a -0.13pp smaller contribution than in February) but with a caveat that it was mostly driven by airfares with the Easter holidays in April this year vs March last year.

- Goods inflation slightly accelerated (+0.04pp contribution vs prior) as softer energy was not quite able to cancel out firmer food / core goods inflation.

- The March CPI report highlighted differing Y/Y trends in services-heavy CPI subcategories:

- The mixed-weight transport category (i.e. across goods & services) was key in March at 0.88% Y/Y (state-level data had implied 0.9-1.0%) after 2.4% in Feb. It confirmed that energy (-2.77% vs -1.6% in Feb) and travel services (airfares -8.04% Y/Y vs 9.26% prior) acted in tandem here.

- Within the services-heavy CPI subcategories, there were some considerable differences in the Y/Y pace since December. Moderation was seen in education (4.67% Y/Y vs 5.0% Feb), restaurants and hotels (3.84% vs 4.2%) and recreation & culture (1.05% vs 1.1%). To the upside however, communications at -1.10% Y/Y (vs -1.2%) and healthcare at 2.98% (vs 2.8%).

- A material acceleration in food inflation was also confirmed, at 3.4% Y/Y after 2.8% in Feb.

- Categories associated with the core goods sector appear also firmer than before - clothing and footwear came in at 1.0% (after 0.5% prior) and furnishings and household Equipment at -0.25 (after -0.7%).

EUROZONE DATA: Q1 GDP Flattered By Rounding, Irish Exports

As we suspected, the Eurozone flash Q1 GDP release was flattered by rounding, coming in at 0.352% unrounded. That’s still well above the 0.2% projected by consensus and the ECB, but the data was nonetheless skewed by tariff-front loading, particularly in Ireland. Sentiment data points to weak growth momentum in Q2, as US tariffs start to kick in and associated uncertainty continues to weigh.

- Irish GDP rose 3.2% Q/Q, with the stats office noting that “this was driven by an increase in the multinational dominated sectors in Q1 2025 with a more modest increase in the domestic sectors”. Irish February goods trade data showed a 211% Y/Y increase in exports to the US, which largely comprised of medical and pharmaceutical products - an obvious indication of front-loading amongst major US Pharma companies based in Ireland.

- Ireland contributed 0.11p to the Eurozone-wide quarterly reading, despite only making up 4% of total GDP.

- Across the four major economies, detailed information on the Q1 data is lacking. However, we note that domestic demand appears to have been a positive contributor in Germany, Spain and Italy, while net trade was a negative contributor to France and Italy. Net trade was not mentioned in the German press release, suggesting a flat/negative contribution there too.

- Summarising the main quarterly GDP prints released yesterday/this morning:

- Eurozone: 0.4% Q/Q vs 0.2% cons, 0.2% prior.

- Germany: 0.2% Q/Q vs 0.2% cons, -0.2% prior.

- France: 0.1% Q/Q vs 0.1% cons, -0.1% prior.

- Italy: 0.3% Q/Q vs 0.2% cons, 0.2% prior.

- Spain: 0.6% Q/Q vs 0.7% cons, 0.7% prior.

US TSY FUTURES: Mix Of Long Setting & Short Cover Seen Tuesday

OI data points to a mix of net long setting (FV, UXY & US) and short cover (TU, TY & WN) during yesterday’s rally.

- The positioning swings largely offset in curve-wide terms, leaving a modest bias towards net long setting.

| 29-Apr-25 | 28-Apr-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,080,854 | 4,092,993 | -12,139 | -451,459 |

FV | 6,832,963 | 6,827,138 | +5,825 | +252,299 |

TY | 4,863,710 | 4,866,159 | -2,449 | -157,588 |

UXY | 2,284,980 | 2,271,750 | +13,230 | +1,182,868 |

US | 1,799,444 | 1,789,402 | +10,042 | +1,310,072 |

WN | 1,879,911 | 1,887,856 | -7,945 | -1,520,799 |

|

| Total | +6,564 | +615,394 |

STIR: Long Setting Seen Further Out The SOFR Strip On Tuesday

OI data points to a mix of net long setting and short cover during Tuesday’s uptick in SOFR futures, with the most meaningful positioning adjustment seemingly coming via net long setting across the greens and blues (only modest net short cover in SFRH8 broke the wider theme in those 2 packs).

| 29-Apr-25 | 28-Apr-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,103,977 | 1,102,450 | +1,527 | Whites | -13,375 |

SFRM5 | 1,269,822 | 1,270,258 | -436 | Reds | -14,350 |

SFRU5 | 981,404 | 990,585 | -9,181 | Greens | +41,686 |

SFRZ5 | 1,099,641 | 1,104,926 | -5,285 | Blues | +5,189 |

SFRH6 | 723,289 | 725,138 | -1,849 |

|

|

SFRM6 | 689,143 | 703,967 | -14,824 |

|

|

SFRU6 | 692,978 | 692,368 | +610 |

|

|

SFRZ6 | 846,220 | 844,507 | +1,713 |

|

|

SFRH7 | 625,220 | 614,938 | +10,282 |

|

|

SFRM7 | 545,070 | 532,413 | +12,657 |

|

|

SFRU7 | 359,039 | 355,449 | +3,590 |

|

|

SFRZ7 | 397,852 | 382,695 | +15,157 |

|

|

SFRH8 | 267,903 | 270,878 | -2,975 |

|

|

SFRM8 | 188,797 | 185,924 | +2,873 |

|

|

SFRU8 | 150,450 | 147,204 | +3,246 |

|

|

SFRZ8 | 165,858 | 163,813 | +2,045 |

|

|

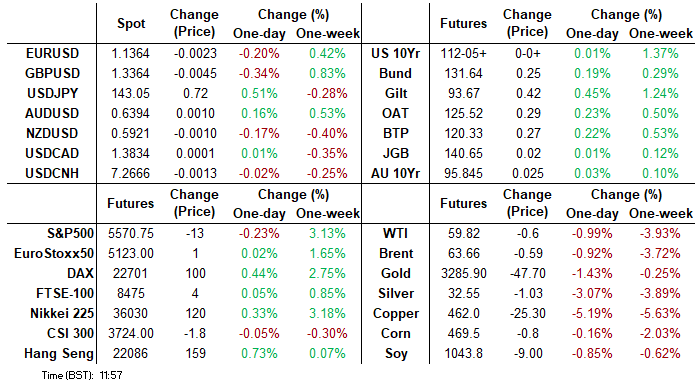

FOREX: USD/JPY Drifts Back Above 143.00 as US Data/BOJ Awaited

- Lower US yields this week prompted a resumption of USDJPY weakness, exacerbated by the bearish technical conditions and 144.00 capping the recovery well. Weaker-than-expected US data on Tuesday saw USDJPY test 142.00 a couple of times before potential month end related flows, position squaring ahead of US GDP and stability for global equities have proved supportive.

- Weaker-than-expected IP and retail sales data from Japan may also be providing a USDJPY tailwind, as the pair has been steadily grinding higher across the APAC session and through the European morning. 20-day EMA resistance has moved down, coinciding with last week’s highs around the 144.00 mark. Support is seen at 141.97 and 141.49, the Apr 23 low.

- US GDP & ECI, MNI Chicago PMI and PCE will provide the primary impulse for USDJPY Wednesday, however, the close proximity to month-end and Thursday’s BOJ decision may provide obstacles to a meaningful breakout.

- Given the significant shifts in external conditions, particularly the U.S. tariff policy changes since the last MPM in March, the BoJ is likely to adopt a cautious, wait-and-see stance at this meeting. Our full preview with analyst views is here: https://mni.marketnews.com/42YfUk9

FOREX: USD/JPY Struggles on Approach to Recovery High Ahead of GDP

- JPY is weaker against all others early Wednesday, however USD/JPY is yet to make any meaningful test on the Friday recovery high at 144.03. With tariff limbo still in place, and no trade negotiations to speak of between the US and China, G10 currencies are awaiting the next macro cue or headline to trade with any real conviction. That said, EUR/GBP continues its losing streak, with the cross hitting a new lower low of 0.8482 in overnight trade.

- Moves follow the cross trading through a major support area we flagged last week at 0.8520-31 - marking both the early April pullback low as well as the 50% retracement of the tariff-inspired upleg off 0.8323.

- Meanwhile, Australian CPI for Q1 came in toward the upper-end of expectations, helping AUD/USD recover well into the European morning. Spot faltered on the approach toward yesterday's 0.6450 highs, however, meaning the pair has traded either side of the 0.64 handle for eight consecutive sessions. The 200-dma defines the first topside level, at 0.6460.

- US data picks up Wednesday, with MNI Chicago PMI for April seen moderating further to 45.9 from 47.6 previously. Advance GDP, Personal income, spending and the latest PCE stats for March are also due. Central bank speak sees BoE's Lombardelli, ECB's Villeroy & Makhlouf as well as the BoC minutes. The Fed remain inside their pre-decision media blackout period.

OPTIONS: Expiries for Apr30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1375-95(E2.7bln), $1.1425(E500mln)

- USD/JPY: Y140.50($1.9bln), Y142.00($1.8bln), Y144.40-50($959mln), Y145.00($1.5bln), Y148.50($716mln)

- AUD/USD: $0.6115(A$1.1bln), $0.6250(A$702mln)

- NZD/USD: $0.5950(N$521mln)

EQUITIES: Corrective Bull Cycle in E-Mini S&P in Play, Resistance at 50-Day EMA

- Eurostoxx 50 futures maintain a positive tone and are holding on to their recent gains. The contract has cleared the 20-day EMA and pierced the 50-day EMA, at 5102.56. A clear break of this average would strengthen the current bull cycle and signal scope for a continuation of the corrective uptrend. This would open 5165.00 next, the Apr 3 high. Support to watch lies at 4812.00, the Apr 16 low. Clearance of this level would highlight a reversal.

- A corrective bull cycle in S&P E-Minis that started on Apr 7, remains in play. The contract has breached a number of important short-term resistance points. Price has cleared the 20-day EMA and pierced 5528.75, the Apr 10 high. The next key resistance is 5618.25, the 50-day EMA. A clear breach of this EMA would strengthen a bull theme. Initial key support lies at 5127.25, the Apr 21 low. A break would be bearish.

COMMODITIES: WTI Futures Approaching Initial Support at $58.29, Apr 29 Low

- A medium-term bearish theme in WTI futures remains intact and the latest move down reinforces this theme, signalling the end of the correction between Apr 9 - 23. The correction allowed an oversold trend condition to unwind. A clear resumption of the bear cycle would open $53.72, a Fibonacci projection. Initial support to watch is at $58.29, the Apr 29 low. Resistance to watch is $65.38, the 50-day EMA.

- Gold is unchanged and the yellow metal continues to trade below its recent highs. The trend needle points north and the latest move down appears corrective. The retracement has allowed an overbought condition to unwind. Moving average studies are in a bull-mode position highlighting a dominant uptrend. The next objective is $3547.9, a Fibonacci projection. Initial firm support to watch lies at 3239.5, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 30/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 30/04/2025 | 1200/1400 | *** | HICP (p) | |

| 30/04/2025 | 1215/0815 | *** | ADP Employment Report | |

| 30/04/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/04/2025 | 1230/0830 | *** | GDP | |

| 30/04/2025 | 1230/0830 | *** | Employment Cost Index | |

| 30/04/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/04/2025 | 1230/0830 | *** | Treasury Quarterly Refunding | |

| 30/04/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/04/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 30/04/2025 | 1400/1000 | *** | Personal Income and Consumption | |

| 30/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 30/04/2025 | 1530/1630 | BOE Lombardelli At New Economics Teacher Training Launch | ||

| 30/04/2025 | 1730/1330 | BOC Meeting Minutes | ||

| 01/05/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/05/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/05/2025 | 0130/1130 | ** | Trade price indexes | |

| 01/05/2025 | 0130/1130 | ** | Trade Balance | |

| 01/05/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 01/05/2025 | 0630/0830 | ** | Retail Sales | |

| 01/05/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 01/05/2025 | 0830/0930 | ** | BOE M4 | |

| 01/05/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/05/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 01/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 01/05/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/05/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/05/2025 | 1400/1000 | * | Construction Spending | |

| 01/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 01/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 01/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result |