MNI US MARKETS ANALYSIS - Tsys Maintain Bullish Setup into CPI

Highlights:

- US CPI to have lingering seasonals, may cloud clarity of read on inflation pressures

- Treasuries maintain a bullish set-up into Friday trade; Presidents' Day on Monday

- Oil skids lower on report that OPEC+ could resume output hikes from April

US TSYS: TYH6 Bullish Phase Intact Ahead Of January CPI

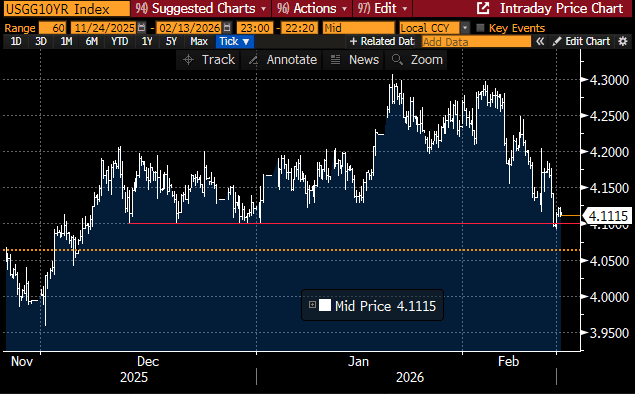

Treasuries have seen a modest paring of yesterday’s gains driven by risk-off stemming from AI and precious metal space, in moves that have seen a temporary drop below 4.10% 10Y yields. Near-term attention is now firmly on today’s January CPI report including annual seasonal adjustment revisions.

- Cash yields are 1.1-1.7bp higher across the curve.

- The 10Y yield opened at a new recent low of 4.0942% after tentatively clearing 4.10% yesterday, but has since lifted to 4.112%. Having last been sub-4.10% on Dec 5, that 4.10% level had then provided decent support on multiple occasions through December.

- TYH6 trades at 112-24+ (-01) on strong cumulative overnight volumes of 435k, pulling back off a latest high of 112-28 seen early in Asia trade before keeping to narrow ranges.

- It has breached resistance at 112-25 (61.8% retrace of Nov 25-Jan 20 bear leg) to open a key short-term resistance at 112-31 (Dec 18 high).

- Some yield-focused resistance to also bear in mind, 10Y yields at 4.10% equate to 112-27 and 4.05% to 113-04+.

- NY Fed’s deputy SOMA manager Remache reiterated yesterday (link) the Fed will continue its balance-sheet expansion with $40bn of securities per month until mid-April when it will likely be reduced substantially. That’s a continuation of Dec 10 statement (link) that: “The Desk anticipates that the pace of RMPs will remain elevated for a few months to offset expected large increases in non-reserve liabilities in April. After that, the pace of total purchases will likely be significantly reduced in line with expected seasonal patterns in Federal Reserve liabilities.”

- Data: CPI Jan (0830ET), Real av earnings Jan (0830ET)

- Politics: Trump delivers remarks to Fort Bragg military families (1330ET)

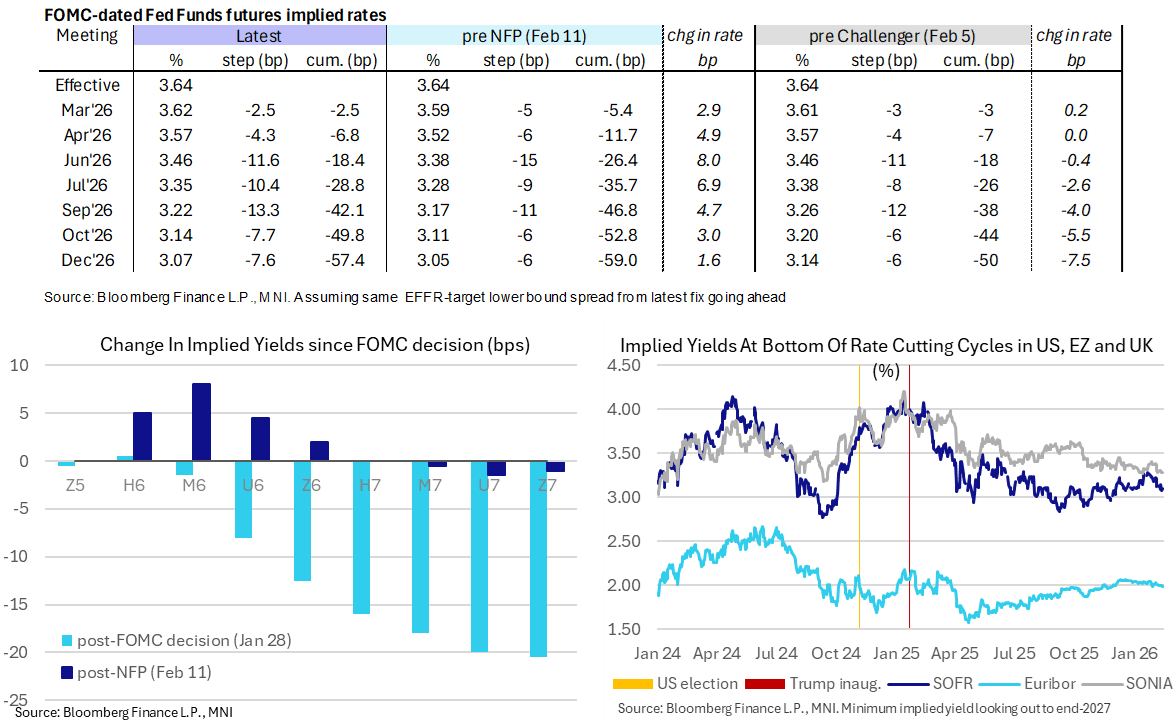

STIR: Fed Cuts Seen In July and October Ahead Of January CPI Report

- A next Fed cut is still expected only in July, holding most of its hawkish shift after Wednesday’s payrolls report, but yesterday’s risk-off increasingly weighed further out the curve ahead of today’s CPI release.

- MNI US CPI Preview: https://mni.marketnews.com/3OayQs6

- FF cumulative cuts from 3.64% effective: 2.5bp Mar (vs 5.5bp pre-NFP), 7bp Apr, 18.5bp Jun (vs 26.5bp), 29bp Jul, 42bp Sep (vs 47bp), 50bp Oct and 57.5bp Dec (vs 59bp)

- SOFR futures are up to 2 ticks lower in 2H27, with the implied terminal yield at 3.095% (H7, +1.5bp) after yesterday’s 3.08% poked to its lowest close since Dec 18 (after a soft Nov CPI report with its many caveats).

- Fedspeak: Gov. Miran (voter, dove) late yesterday said “The biggest risk to the economy is that we’re misconstruing just how tight monetary policy is”. Next Fedspeak isn’t scheduled until VC Supervision Bowman on Monday (Presidents Day).

- Bloomberg yesterday reported that Republican Senator Tillis rejected a suggestion that the Senate Banking Committee conduct its own investigation into Fed Chair Powell. Tillis has vowed to hold up any Fed nominees until the DOJ investigation into Powell is resolved, which could block Kevin Warsh from getting a confirmation vote.

SOFR: Net Long Setting In Front Of Reds On Thursday

OI data points to relatively contained net positioning adjustments as most SOFR futures rallied on Thursday. The most concentrated round of positioning swings came via net long setting SFRZ6-M7 futures, with a mix of net long setting and short cover seen across the remainder of the strip.

| 12-Feb-26 | 11-Feb-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,347,476 | 1,344,870 | +2,606 | Whites | -7,792 |

SFRH6 | 1,305,492 | 1,310,681 | -5,189 | Reds | +39,966 |

SFRM6 | 1,434,588 | 1,433,790 | +798 | Greens | -9,132 |

SFRU6 | 1,401,977 | 1,407,984 | -6,007 | Blues | +5,096 |

SFRZ6 | 1,447,556 | 1,430,582 | +16,974 |

|

|

SFRH7 | 959,849 | 953,176 | +6,673 |

|

|

SFRM7 | 941,410 | 921,232 | +20,178 |

|

|

SFRU7 | 865,833 | 869,692 | -3,859 |

|

|

SFRZ7 | 1,032,379 | 1,037,340 | -4,961 |

|

|

SFRH8 | 534,097 | 534,981 | -884 |

|

|

SFRM8 | 466,268 | 462,688 | +3,580 |

|

|

SFRU8 | 394,754 | 401,621 | -6,867 |

|

|

SFRZ8 | 383,157 | 383,531 | -374 |

|

|

SFRH9 | 228,344 | 223,420 | +4,924 |

|

|

SFRM9 | 198,976 | 199,699 | -723 |

|

|

SFRU9 | 172,028 | 170,759 | +1,269 |

|

|

US TSY FUTURES: Net Long Setting Dominated On Thursday

OI data points to net long setting dominating as weakness in tech shares & oil, along with strong demand at the latest 30-Year auction, helped drive Treasury futures higher on Thursday.

- ~$7.6mln DV01 of net fresh long exposure was set in curve-wide terms.

- Only modest net short cover in FV futures interrupted the wider theme.

| 12-Feb-26 | 11-Feb-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,673,885 | 4,645,782 | +28,103 | +1,025,507 |

FV | 6,846,494 | 6,863,899 | -17,405 | -744,805 |

TY | 5,453,541 | 5,437,581 | +15,960 | +1,052,489 |

UXY | 2,551,260 | 2,535,703 | +15,557 | +1,394,500 |

US | 1,753,963 | 1,742,071 | +11,892 | +1,666,001 |

WN | 2,208,568 | 2,190,986 | +17,582 | +3,232,742 |

|

| Total | +71,689 | +7,626,435 |

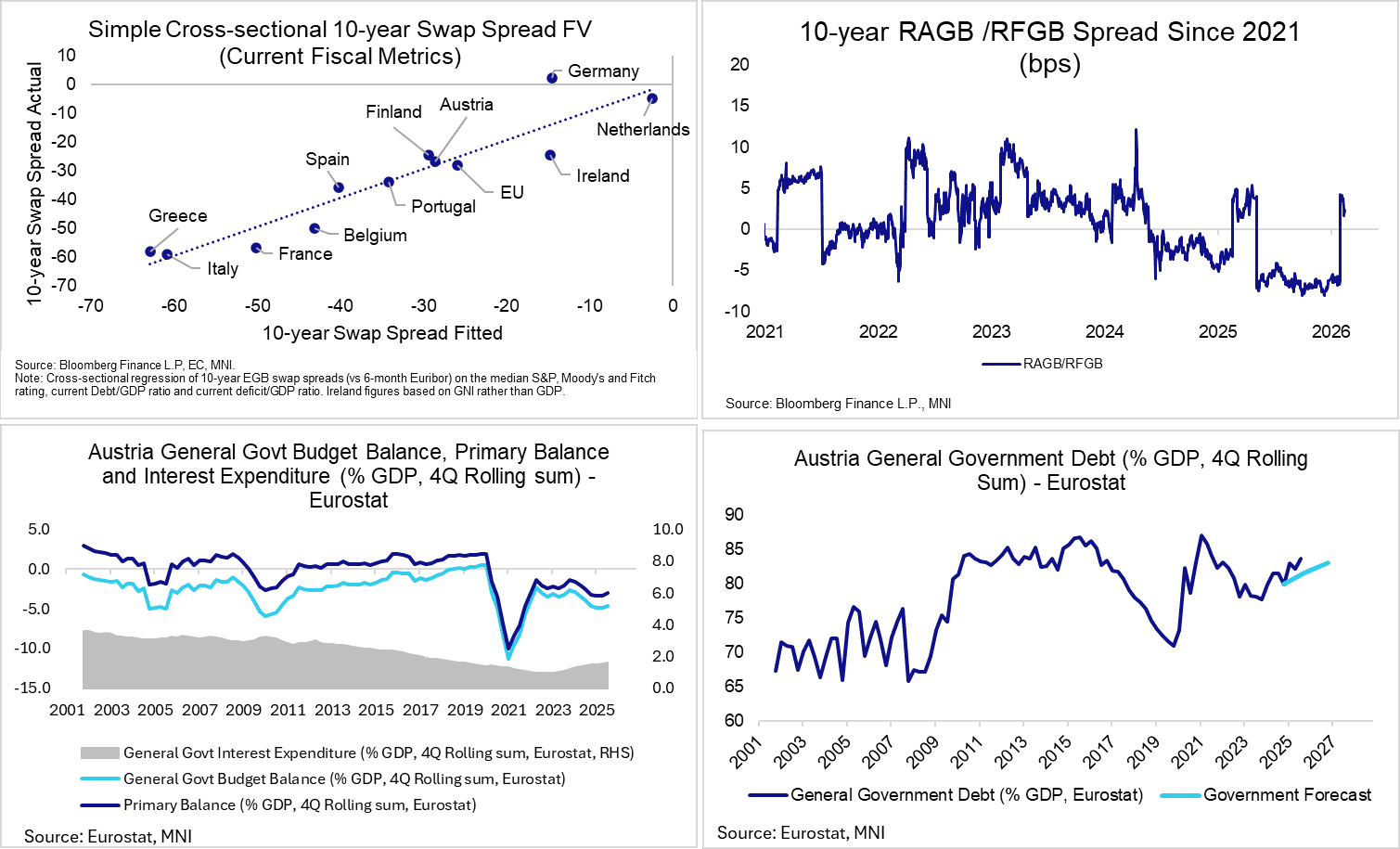

AUSTRIA: Moody's Downgrade To Aa2 Likely, But Not Assured

Moody’s is scheduled to review Austria’s sovereign rating after hours (current rating: Aa1; Outlook Negative). We think a downgrade should be considered the base case, as current fiscal balances seem inconsistent with an Aa1 sovereign rating. Such a move would bring Austria’s rating in line with Fitch (AA, Outlook Stable). However, primary balance improvements in the latest fiscal data and the Government’s consolidatory plans over the next few years could yet see Austria escape a downgrade for now.

- Given Austria’s negative outlook, we don’t expect significant underperformance for RAGBs in the event of a downgrade. A cross-sectional regression of 10-year EGB swap spreads versus debt/GDP, deficit/GDP and the median of S&P, Moody’s and Fitch ratings places RAGBs as roughly fairly valued. The results are similar if we use the EC’s 2027 fiscal forecasts instead of latest readings.

- In August 2025, Moody’s downgraded Austria’s outlook to negative, citing “the prospect of a sustained and material weakening in Austria's fiscal strength, which would reflect weaker fiscal policy effectiveness than we have previously assessed”. The agency noted that a downgrade would be likely if there was evidence of a continued weakening in these fiscal metrics.

- As of Q3 2025, the deficit was tracking at 4.6% GDP, below the 4.9% seen in Q1 and Q2. Moody’s may thus argue that a “continued weakening” in fiscal balances has not been realised. However, the current deficit is still well above the 2.5-4.0% range seen between 2022-2024, and has seen debt/GDP rise to almost 84% (vs 80% in Q4 2024).

- Austria is currently under an EDP with the EU, and aims to reduce its deficit to 4.5% in 2025 and to 4.2% in 2026. The EC’s autumn forecasts look for a 4.4% deficit in 2025, falling to 4.1% in 2026 before rising back to 4.3% in 2027.

- One counter to still-elevated fiscal deficits is that real GDP growth is estimated to have been 0.6% in 2025, above EC and Government expectations of 0.3%.

SWAPS: EUR Swap Rates Follow Bond Yields Lower, Dutch Flows Still Eyed

30- & 50-Year EUR swap rates are nearly 10bp lower on the week, alongside the rally in bonds, EUR10s30s curve is little changed.

- While cross-market inputs are eyed, most of the focus remains on the Dutch pension transition.

- We have previously flagged the crowded nature of paid/steepener positioning in the long end as markets look to profit from the Dutch switch to defined contribution from defined benefit schemes.

- The trade fared well for much of ’25, before disappointment surrounding the lack of meaningful market footprint related to the January transition and one of the larger funds (PFZW) declaring higher-than-expected hedging intentions helped long end swap rates and curves back from cycle highs.

- Looking forwards, structural pay-side & steepener risks remain evident in the long end, but any such moves are unlikely to come in a straight line, with positioning seemingly remaining heavy.

- ING remind us that for “PMT (~EUR80bln of assets), the transition period is planned for H126 and should still bring some flows. PFZW (~EUR250bln assets), is more secretive about its transition strategy”.

- Further out, ING note that “almost EUR1tln of Dutch pension assets are scheduled to transition in ‘27, but we should start seeing the impact on markets this year”. They touch on this year’s example, with a Dutch pension news vendor suggesting that many smaller funds rebalanced in December ‘25 (or earlier) instead of waiting until their transition date in January. One interviewee noted that “the reduction of our interest rate hedge went very smoothly, at much lower costs than anticipated".

- Regulatory guidance had already pointed to a greater degree of flexibility re: the adjustments.

- The piece noted that the hedge unwind wasn’t as large as many had assumed, with some funds actually increasing their hedging provision, seemingly owing to the move higher in rates in late ’25.

- The article also notes that peer-to-peer OTC exposure switches lessened some of the market impact.

EUROPE ISSUANCE UPDATE

GILT SYNDICATION: Syndicate appointed for green gilt transaction

- The DMO has announced the appointment of syndicate for the new green gilt maturing on 7 March 2037 which is due for the W/C 9 March 2026 (ISIN: GB00BVP99905).

- The joint Bookrunners will be Barclays, BNP Paribas, Citi, HSBC, J.P. Morgan, and NatWest.

- MNI pencils in a GBP6.5bln transaction size.

GILT AUCTION PREVIEW: On offer via tender on Tuesday

The DMO has announced that it will be looking to sell two gilts via its tender on Tuesday 17 February.

- GBP500mln of the 0.125% Jan-28 Gilt (ISIN: GB00BMBL1G81)with the bidding window ending 10:00GMT

- GBP750mln of the 4.25% Jun-32 Gilt (ISIN: GB0004893086) with the bidding window ending 11:30GMT

RUSSIA: Kremlin Confirms New Rus-US-Ukr Talks Next Week

State-run Tass reports comments from Kremlin spox Dmitry Peskov. Says that a new round of peace talks on Ukraine will take place next week. On 12 Feb, Ukrainian President Volodymyr Zelenskyy had raised the prospect of tripartite talks between the US, Ukraine, and Russia taking place in the US on 17 or 18 Feb, but said it was unclear if Russia would accept. Peskov said, "There's an agreement that it will indeed take place next week. We'll let you know the location and exact dates. But it will indeed be next week,"

- There is no comment from Peskov on reports that European countries could look to hold separate talks with Russia. Speaking to Le Monde earlier in the week, French President Emmanuel Macron said "It is important to structure the resumption of a European discussion with the Russians, without naivety, without putting pressure on the Ukrainians, but so as not to depend on a third party." These efforts have made little progress to date, with France's E3 partners, Germany and the UK, both wary of resuming talks with Russia with concerns it could undermine the US and Ukrainian efforts to reach a peace deal.

- Following on from reports on 12 Feb that Russia could embrace the US dollar again in an effort to boost economic ties with Washington, Peskov says that the two countries have discussed trade and economic cooperation, but that "it's unlikely that such discussions will move beyond talk before the conflict in Ukraine is settled." Nevertheless, following the reports Peskov says "it's obvious that Moscow is proposing cooperation", and that "Russia did not decide to stop using the dollar, the US imposed restrictions."

EU: Move Towards 'Enhanced Cooperation' Could Spur Action, But Risks Schisms

Following an informal meeting of EU leaders on 12 Feb, there is an increased prospect of a group of member states using the "enhanced cooperation model" in an effort to speed up decision-making processes at the top of the EU. The idea would be a multi-speed Europe, with Commission President Ursula von der Leyen noting in a presser on Thursday evening that “Often we move forward with the speed of the slowest, the enhanced cooperation model avoids that.”

- MNI's Policy team reported ahead of the meeting that such a development was likely to be a prominent outcome of the discussions (see 'MNI: Draghi's 'Pragmatic Federalism' Gains Support- Official).

- Enhanced cooperation, contained within the Treaty on European Union and Treaty on the Functioning of the EU, "is a procedure where a minimum of 9 EU Member States are allowed to set up advanced integration or cooperation in a particular field within the EU, when it has become clear that the EU as a whole cannot achieve the goals of such cooperation within a reasonable period."

- The move towards more widespread use of enhanced cooperation could progress at the March European Council summit.

- The use of enhanced cooperation presents two very different scenarios. For its proponents, it encourages laggard countries to join in with those pushing for reform or action for fear of being left behind or not having a say. For its critics, it risks schisms within the EU or smaller countries being dominated by larger ones, something the unanimity and qualified majority rules were designed to avoid.

SECURITY: Key Speakers On First Day Of Munich Security Conference

The Munich Security Conference is underway at the Hotel Bayerischer Hof in the Bavarian capital. Below we outline the key political speakers on day one of the event, with timings. Livestreams will be available here or here.

- 06:45ET/11:45GMT/12:45CET- German Chancellor Friedrich Merz

- 07:30ET/12:30GMT/13:30CET- European High Representative for Foreign Affairs and Security Policy Kaja Kallas, Saudi Foreign Minister Prince Faisal bin Farhan Al Saud, US Ambassador to the UN Michael Waltz, Colombian Minister of Defence Pedro Arnulfo Sánchez (Panel disc: 'Breaking Point: The International Order Between Reform and Destruction')

- 08:10ET/13:10GMT/14:10CET- Japanese Defence Minister Shinjirō Koizumi

- 08:30ET/13:30GMT/14:30CET - German Finance Minister Lars Klingbeil, WTO Director-General Ngozi Okonjo-Iweala, Finnish President Alexander Stubb, US Senator Thom Tillis (R-SC) (Panel disc: Tariff-fying Times: Managing the Weaponisation of Trade)

- 10:30ET/15:30GMT/16:30CET - Swedish PM Ulf Kristersson, Moldovan President Maia Sandhu, Chair of the NATO Military Committee Adm. Giuseppe Cavo Dragone (Panel disc: 'Destructive Ambiguity: Deterring and Countering Hybrid Warfare')

- 11:30ET/16:30GMT/17:30CET - Ukrainian Minister of Foreign Affairs Andrii Sybiha, French Minister of Europe and Foreign Affairs Jean-Noël Barrot, British Secretary of State for Foreign, Commonwealth and Development Affairs Yvette Cooper, Dutch Minister of Foreign Affairs David van Weel, US Sen. Jeanne Shaheen (D-NH) (Panel disc: Spotlight on Security Guarantees for Ukraine)

- 12:00ET/17:00GMT/18:00CET - French President Emmanuel Macron

- 15:00ET/20:00GMT/21:00CET - US Permanent Representative to NATO Matthew Whitaker, Michigan Gov. Gretchen Whitmer (D), Rep. Alexandria Ocasio-Cortez (D-NY) (Panel disc: Breaking (With) the Past: Seismic Shifts in US Foreign Policy)

FOREX: DXY Consolidates Ahead Of US CPI

- FX markets await US CPI later today with major pairs consolidating recent ranges. More attention may be on equities after yesterday's sharp selloff which also filtered through to precious metals, and slightly extended overnight.

- JPY underperforms moderately on the session after PM Takaichi's advisor Honda stated there is scope for the BoJ to raise rates this year, but the next move is unlikely to come in March. This keeps USDJPY set to close the week sharply lower with a 2.2% loss since last Friday at typing.

- With next week's inauguration of PM Takaichi incoming, a major focus point for JPY will be on any additional intel on financing of the food tax suspension, with higher usage of FX account proceeds likely not sufficient to cover the funding gap. From a technical standpoint, a bearish tone in USDJPY remains intact, with key short-term support at 152.10, the Jan 27 low and bear trigger, in close range with trendline support at 151.78. Initial resistance to watch is at 155.62, the 20-day EMA.

- Weaker risk sentiment pressured AUDUSD after the pair came within 11 pips of the 0.7158 2023 highs yesterday. AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are in scope. Clearance of the 2023 highs would put attention on 0.7208, a Fibonacci projection.

- In an otherwise light data calendar, US CPI is a key test of whether tariff-related pressures, early‑year price adjustments, and lingering category‑specific normalization are beginning to exert more persistent influence—an issue several FOMC participants have highlighted as central to judging the underlying inflation trajectory.

- BoE's Pill, ECB's Guindos and BoJ's Tamura are scheduled to speak. For Pill, we will be watching for any indication on the neutral rate in his comments today.

OPTIONS: Expiries for Feb13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1750(E2.1bln), $1.1775(E1.3bln), $1.1800(E3.2bln),$1.1820-25(E1.6bln), $1.1850(E4.8bln), $1.1875(E1.6bln), $1.1900(E2.3bln), $1.1950-55(E3.9bln)

- USD/JPY: Y152.00($1.7bln), Y153.15-20($875mln), Y154.00($1.6bln), Y155.00($1.4bln), Y156.00($1.4bln), Y158.00($1.3bln), Y158.50($1.6bln), Y159.00($2.0bln), Y160.00($3.1bln);

- GBP/USD: $1.3470-75(Gbp1.0bln), $1.3600(Gbp532mln)

- EUR/GBP: Gbp0.8675(E531mln), Gbp0.8736-45(E1.0bln), Gbp0.8770-75(E680mln)

- AUD/USD: $0.6800(A$1.6bln), $0.7110-15(A$755mln)

- USD/CAD: C$1.3500($826mln), C$1.3600($1.1bln), C$1.3770-75($1.0bln)

- USD/CNY: Cny6.9000($1.2bln), Cny6.9700($1.2bln)

EQUITIES: Recent Sharp Sell-Off for E-Mini S&P Reinstates Bearish Threat

- The medium-term trend condition in EuroStoxx 50 futures remains bullish and this week’s fresh cycle highs reinforce the bull theme. The initial move higher yesterday delivered a print above the 6100.00 handle. A clear breach of this hurdle would open 6134.00, a Fibonacci projection point. Key support to watch lies at the 50-day EMA, at 5901.38. Clearance of this average would highlight a short-term top. For now, a move down is considered corrective.

- A sharp sell-off yesterday in S&P E-Minis reinstates a potential bearish threat with key resistance at 7043.00 intact, the Jan 28 high and bull trigger. Attention turns to the key support at 6751.50, the Feb 6 low, where a break would highlight a top and a stronger short-term reversal. This would open 6691.56, a Fibonacci retracement point. Initial resistance to watch is at 6922.20, the 50-day EMA.

COMMODITIES: WTI Futures Test 20-Day EMA Support

- A bull cycle in WTI futures remains intact. However, the move lower from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $62.58 (pierced). The 50-day EMA lies at $60.87. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high. Clearance of it would resume the uptrend.

- Recent gains in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high still highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

| Date | GMT/Local | Impact | Country | Event |

| 13/02/2026 | 1200/1300 | ECB's de Guindos Remarks and Q&A At Círculo de Confianza | ||

| 13/02/2026 | 1200/1200 | BOE's Pill Fireside Chat At Santander Macro Event | ||

| 13/02/2026 | - | BOE MPG Minutes Released | ||

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1330/0830 | ** | US CPI Annual Revised | |

| 13/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/02/2026 | 1630/1730 | ECB Lagarde Roundtable on Trade Dependencies and Global Supply Chains |