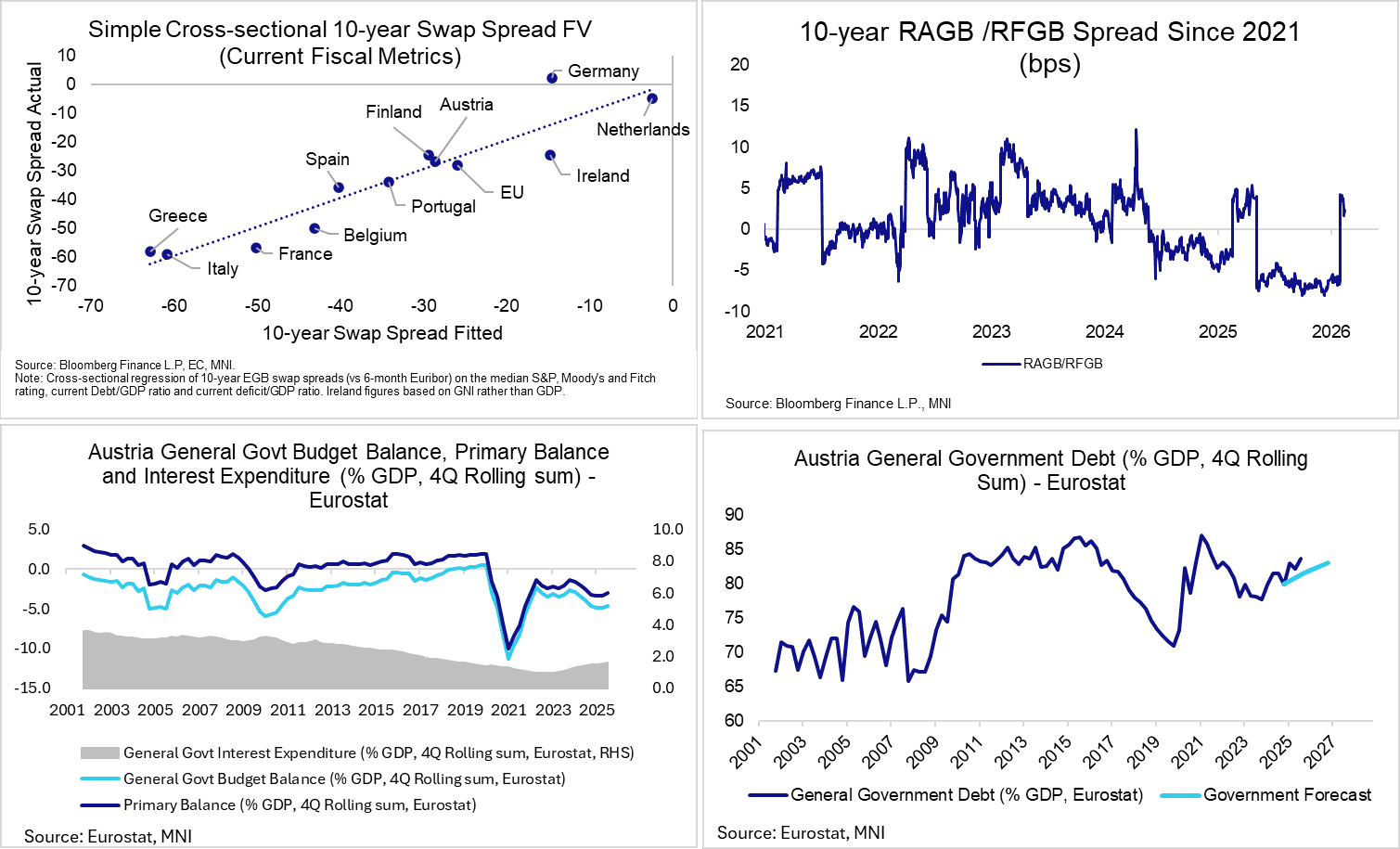

AUSTRIA: Moody's Downgrade To Aa2 Likely, But Not Assured

Moody’s is scheduled to review Austria’s sovereign rating after hours (current rating: Aa1; Outlook Negative). We think a downgrade should be considered the base case, as current fiscal balances seem inconsistent with an Aa1 sovereign rating. Such a move would bring Austria’s rating in line with Fitch (AA, Outlook Stable). However, primary balance improvements in the latest fiscal data and the Government’s consolidatory plans over the next few years could yet see Austria escape a downgrade for now.

- Given Austria’s negative outlook, we don’t expect significant underperformance for RAGBs in the event of a downgrade. A cross-sectional regression of 10-year EGB swap spreads versus debt/GDP, deficit/GDP and the median of S&P, Moody’s and Fitch ratings places RAGBs as roughly fairly valued. The results are similar if we use the EC’s 2027 fiscal forecasts instead of latest readings.

- In August 2025, Moody’s downgraded Austria’s outlook to negative, citing “the prospect of a sustained and material weakening in Austria's fiscal strength, which would reflect weaker fiscal policy effectiveness than we have previously assessed”. The agency noted that a downgrade would be likely if there was evidence of a continued weakening in these fiscal metrics.

- As of Q3 2025, the deficit was tracking at 4.6% GDP, below the 4.9% seen in Q1 and Q2. Moody’s may thus argue that a “continued weakening” in fiscal balances has not been realised. However, the current deficit is still well above the 2.5-4.0% range seen between 2022-2024, and has seen debt/GDP rise to almost 84% (vs 80% in Q4 2024).

- Austria is currently under an EDP with the EU, and aims to reduce its deficit to 4.5% in 2025 and to 4.2% in 2026. The EC’s autumn forecasts look for a 4.4% deficit in 2025, falling to 4.1% in 2026 before rising back to 4.3% in 2027.

- One counter to still-elevated fiscal deficits is that real GDP growth is estimated to have been 0.6% in 2025, above EC and Government expectations of 0.3%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Ireland 10-year Jun-36 : Launched

- Size: E5bln (above MNI's E3-4bln expectation)

- Books closed in excess of E43bln (inc E2.2bln JLM interest)

- Spread set: MS + 26bp (guidance was MS +28bps area)

- Coupon: Short first

- Maturity: 18 June 2036

- ISIN: IE000O6GBYC9

- Bookrunners: Barclays (B&D/DM), BofA Securities, Cantor Fitzgerald Ireland, Goodbody, J.P. Morgan and NatWest

- Settlement: 21 January 2026 (T+5)

- Timing: Allocations and pricing to follow

From market source / MNI colour

POLITICAL RISK: Trump-Anything Less Than Greenland In US Hands 'Unacceptable'

US President Donald Trump posts on Truth Social: "The United States needs Greenland for the purpose of National Security. It is vital for the Golden Dome that we are building. NATO should be leading the way for us to get it. IF WE DON’T, RUSSIA OR CHINA WILL, AND THAT IS NOT GOING TO HAPPEN! Militarily, without the vast power of the United States, much of which I built during my first term, and am now bringing to a new and even higher level, NATO would not be an effective force or deterrent - Not even close! They know that, and so do I. NATO becomes far more formidable and effective with Greenland in the hands of the UNITED STATES.

Anything less than that is unacceptable. Thank you for your attention to this matter! President DJT"

- Later today, US VP JD Vance and Secretary of State Marco Rubio are set to meet with Danish Foreign Minister Lars Lokke Rasmussen and Greenlandic Foreign Minister Vivian Motzfeldt at the White House to discuss the tense situation.

- Political figures from Denmark, Greenland, NATO and the EU have all sought to reaffirm Greenland's position as a part of the Danish kingdom, and that any US military action in a fellow NATO member would be unacceptable. However, this has done little (if anything) to temper rhetoric from the White House.

- Legislation submitted to the US Congress intended to stop the US from operating militarily in other NATO states is seen as unlikely to become law.

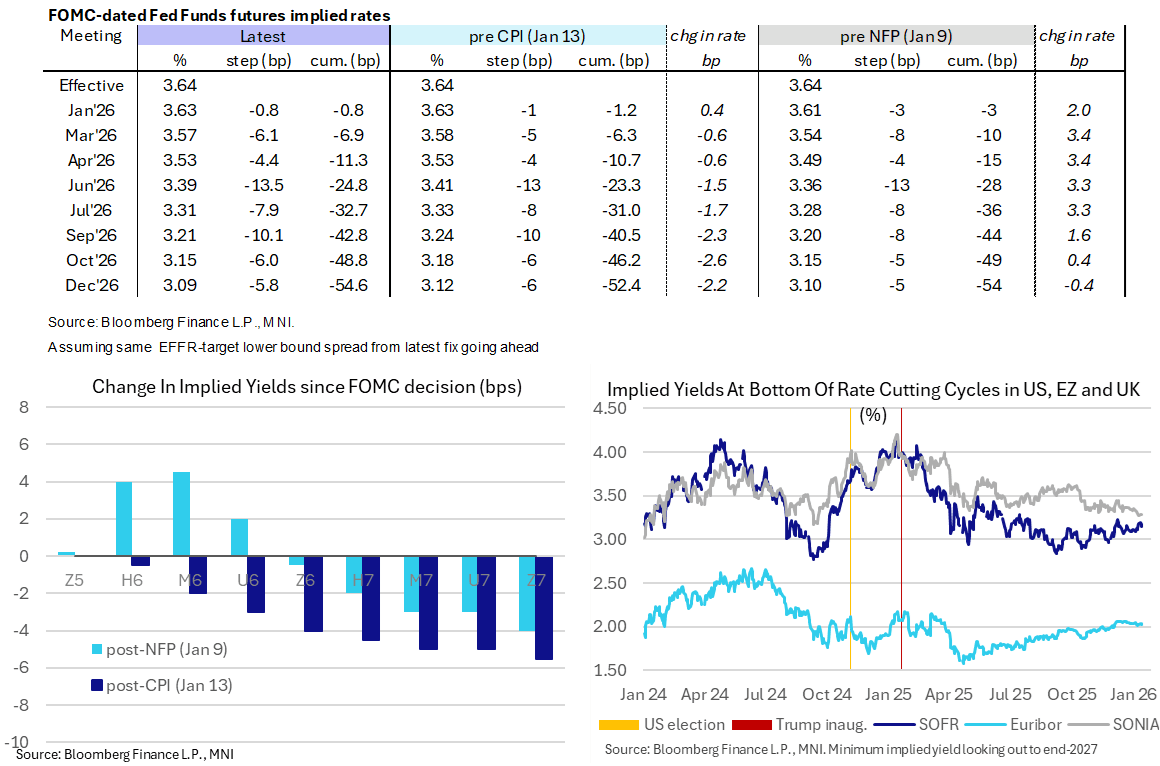

STIR: Modest Dovish CPI Impact Maintained Ahead Of Important Docket

- Fed Funds implied rates are as much as 2bp lower for end-2026 meetings, unwinding a small increase late yesterday to marginally extend a modest dovish move on yesterday’s December CPI release.

- It’s ahead of an important docket with data highlighted by two months of PPI for Oct-Nov and Nov retail sales, six Fedspeakers scheduled and a potential SCOTUS ruling on IEEPA tariffs (1000ET most likely if there is one).

- FF cumulative cuts from 3.64% effective: 1bp Jan, 7bp Mar, 11.5bp Apr, 25bp Jun, 43bp Sep and 54.5bp Dec.

- SOFR futures are up to 2.5 ticks firmer in 2H27 contracts, with a terminal implied yield of 3.145% (H7, -2bp) easing back further from Monday’s highest close since the Dec FOMC (3.19%).