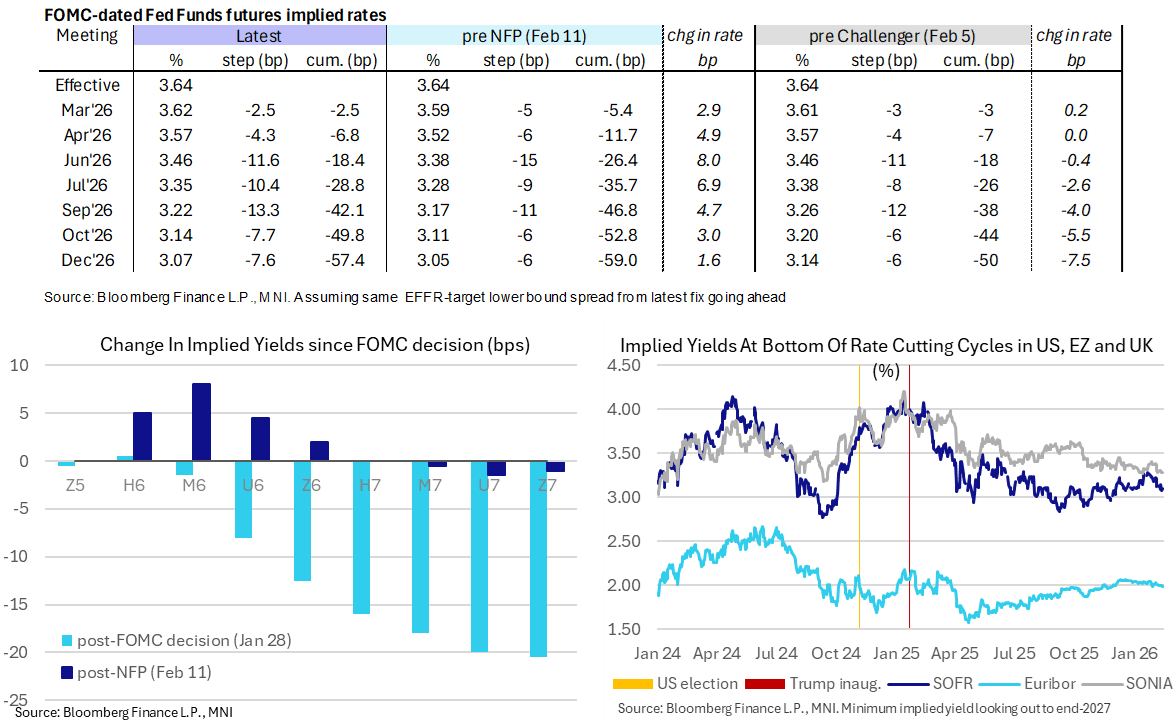

STIR: Fed Cuts Seen In July and October Ahead Of January CPI Report

Feb-13 11:14

- A next Fed cut is still expected only in July, holding most of its hawkish shift after Wednesday’s payrolls report, but yesterday’s risk-off increasingly weighed further out the curve ahead of today’s CPI release.

- MNI US CPI Preview: https://mni.marketnews.com/3OayQs6

- FF cumulative cuts from 3.64% effective: 2.5bp Mar (vs 5.5bp pre-NFP), 7bp Apr, 18.5bp Jun (vs 26.5bp), 29bp Jul, 42bp Sep (vs 47bp), 50bp Oct and 57.5bp Dec (vs 59bp)

- SOFR futures are up to 2 ticks lower in 2H27, with the implied terminal yield at 3.095% (H7, +1.5bp) after yesterday’s 3.08% poked to its lowest close since Dec 18 (after a soft Nov CPI report with its many caveats).

- Fedspeak: Gov. Miran (voter, dove) late yesterday said “The biggest risk to the economy is that we’re misconstruing just how tight monetary policy is”. Next Fedspeak isn’t scheduled until VC Supervision Bowman on Monday (Presidents Day).

- Bloomberg yesterday reported that Republican Senator Tillis rejected a suggestion that the Senate Banking Committee conduct its own investigation into Fed Chair Powell. Tillis has vowed to hold up any Fed nominees until the DOJ investigation into Powell is resolved, which could block Kevin Warsh from getting a confirmation vote.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (H6) Gains Appear Corrective

Jan-14 11:13

- RES 4: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 112-31 High Dec 18 and key short-term resistance

- RES 2: 112-25+ High Dec 30 / 31

- RES 1: 112-22 High Jan 7

- PRICE: 112-12 @ 11:01 GMT Jan 14

- SUP 1: 111-29 Low Dec 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

A bear threat in Treasuries remains present and for now, short-term gains are considered corrective. Attention is on support at 111-29, the Dec 10 low and bear trigger. A break of it would confirm a continuation of the bear cycle. Note too that a head and shoulders reversal pattern on the daily chart also highlights a bearish threat. Scope is seen for a move towards 111-19 initially, a Fibonacci projection. Key short-term resistance is 112-31, the Dec 18 high.

EGB SYNDICATION: France 20-year May-46: Launched

Jan-14 11:06

- Size: E10bln (top of the E8-10bln range MNI expected)

- Books closed in excess of E106bln pre-rec (inc E4bln JLM interest)

- Spread set: 3.25% May-45 OAT + 5bp (guidance was + 8bp area)

- Maturity: 25 May 2046

- Coupon: First full

- ISIN: TBC

- Settlement: 21 January 2026 (T+5)

- Bookrunners: BNPP, Citi (B&D), HSBC, JPM, SocGen

- Timing: Books closed. Allocations and pricing later today.

From market source / MNI colour

SWAPS: EUR 10s30s Curve & 50s Re-Anchor To Round Numbers

Jan-14 11:02

The EUR swap curve bull flattens alongside the recent move lower in yields.

- Some have suggested that the comments from Iran, noting that the country’s missile stockpile has increased since June and indicating a willingness to respond to attacks from any external sources, provided the bid for wider core global FI and weakness for equities.

- EUR swap rates last flat to 1.5bp lower on the day. 50s have re-anchored to 3.00% after PFZW’s Monday announcement revealed higher post-transition hedging requirements than previously envisaged, while the 10s30s curve has re-anchored to 30bp.

- Sensitivity to headlines related to the Dutch pension transition remain evident, with the move to a defined contribution setup from defined benefit presenting well-documented medium-term structural pay-side & steepening risks for the space.

- Commerzbank note that their analysis of the rate sensitivity of the Dutch pension funds swap book remains unchanged, still implying DV01 of ~EUR730mln at the 20-Year point after accounting for FX hedges.