MNI US MARKETS ANALYSIS - Tsys Extend Spell of Weakness

Highlights:

- Treasuries extend spell of weakness as market looks ahead to EU-US deal

- Prelim PMIs paint mixed picture of European economic performance

- ECB decision seen ending with no change in rates, sizeable downside EUR interest via options

US TSYS: Modest Sell-Off On Trade Deal Optimism Extends, TYA Back Near Support

- Treasuries have slowly extended yesterday’s sell-off, which was aided by reports that a US-EU trade deal was getting closer despite White House adviser Navarro saying to take the reports with a "grain of salt".

- Treasuries lagged the sell-off in EGBs at the time of those reports and continue to do so today.

- Yesterday’s well-received 20Y auction could also have fed into outperformance although 20s lead losses today.

- Today sees weekly jobless claims including a payrolls reference period for continuing claims, flash July PMIs and President Trump visiting the Fed. There is also potential spillover from the ECB if Lagarde surprises on the balance of risks.

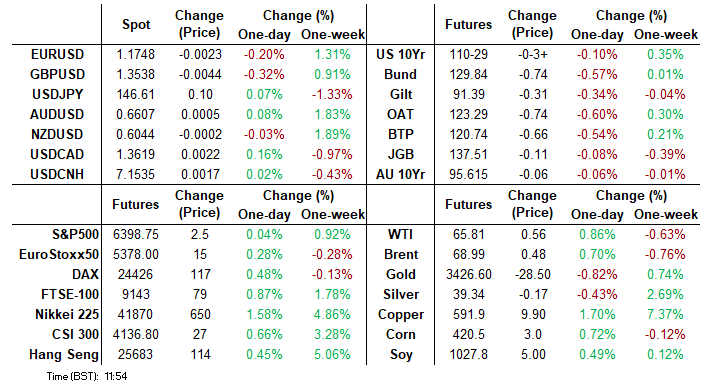

- Cash yields are 1.3-3.0bp higher on the day, with 2s lagging increases.

- Curves are mildly steeper on the day after a sizeable flattening yesterday: 2s10s at 51.3bps (last week’s high 62.7bp), 5s30s at 101.5bp (108.5bp).

- TYU5 trades at 110-29 (-03+) off an earlier low of 110-28+ on thin cumulative volumes of 220k.

- It returns close to support at 110-24 (Jul 21 low) after which lies 110-08+ (Jul 14/16 lows), continuing a pullback from Tuesday’s high of 111-14+ (now initial resistance).

- Data: Weekly jobless claims (0830ET), Chicago Fed national activity Jun (0830ET), S&P Global US flash PMIs Jul (0945ET), New home sales Jun (1000ET), KC Fed mfg Jul (1100ET)

- Coupon issuance: US Tsy $21B 10Y TIPS auction - 91282CNS6 (1300ET)

- Bill issuance: US Tsy $95B 4W & $85B 8W bill auctions (1130ET)

- Politics: Trump signs Executive Orders and Congressional Bills, closed press (1500ET), Trump visits the Federal Reserve after recent criticism including $2.5bn renovation (1600ET)

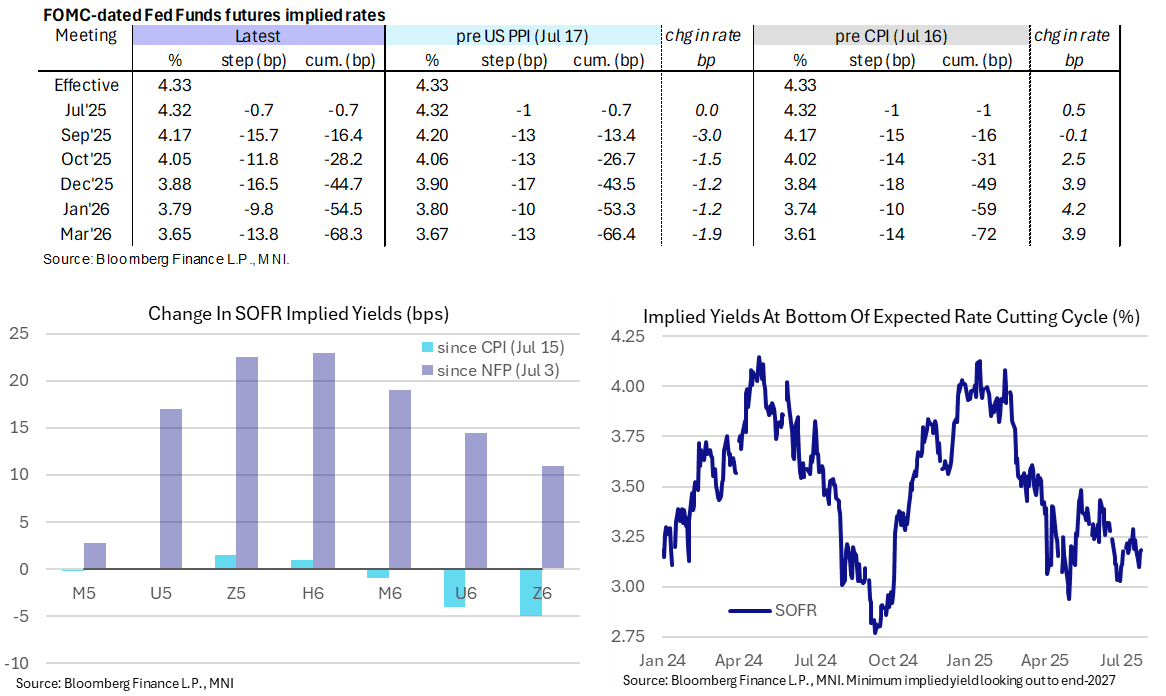

STIR: US Rates At Hawkish End of Week’s Narrow Range

- Fed Funds implied rates sit towards the hawkish end of the week’s narrow range, holding yesterday’s modest lift on reports that a US-EU trade deal was getting closer despite White House adviser Navarro saying to take the reports with a “grain of salt”.

- Cumulative cuts from 4.33% effective: 0.5bp Jul 30, 16.5bp Sep, 28bp Oct, 44.5bp Dec, 54.5bp Jan and 68.5bp Mar.

- The SOFR implied terminal yield of 3.185% (SFRZ6, +1bp) also remains within recent ranges.

- Today sees data headlined by weekly jobless claims covering a payrolls reference period for continuing claims before flash PMIs for July. The ECB decision should also be watched in case there are any surprises in the balance of risks.

SOFR: Mix Of Short Setting & Long Cover Seen In Futures On Wednesday

OI data points to net short setting dominating in the white SOFR futures on Wednesday (although it is hard to be certain when it comes to SFRM5 & U5 given their unchanged price status on the day).

- Net long cover then came to the fore further out the strip.

| 23-Jul-25 | 22-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,262,337 | 1,252,384 | +9,953 | Whites | +78,384 |

SFRU5 | 1,310,123 | 1,276,110 | +34,013 | Reds | -20,544 |

SFRZ5 | 1,324,014 | 1,300,313 | +23,701 | Greens | -16,592 |

SFRH6 | 1,031,490 | 1,020,773 | +10,717 | Blues | -6,638 |

SFRM6 | 865,176 | 873,125 | -7,949 |

|

|

SFRU6 | 837,493 | 840,898 | -3,405 |

|

|

SFRZ6 | 921,868 | 915,984 | +5,884 |

|

|

SFRH7 | 732,011 | 747,085 | -15,074 |

|

|

SFRM7 | 711,544 | 724,221 | -12,677 |

|

|

SFRU7 | 519,028 | 522,698 | -3,670 |

|

|

SFRZ7 | 448,865 | 454,197 | -5,332 |

|

|

SFRH8 | 332,080 | 326,993 | +5,087 |

|

|

SFRM8 | 227,083 | 228,292 | -1,209 |

|

|

SFRU8 | 205,451 | 208,309 | -2,858 |

|

|

SFRZ8 | 205,272 | 206,514 | -1,242 |

|

|

SFRH9 | 146,457 | 147,786 | -1,329 |

|

|

US TSY FUTURES: Net Long Cover Dominated On Wednesday

OI data points to net long cover dominating across much of the curve on Wednesday, only broken by a very modest round of net short setting in TY futures.

| 23-Jul-25 | 22-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,371,240 | 4,378,179 | -6,939 | -258,772 |

FV | 6,969,131 | 6,976,221 | -7,090 | -303,286 |

TY | 4,808,286 | 4,806,137 | +2,149 | +141,004 |

UXY | 2,406,654 | 2,414,002 | -7,348 | -637,144 |

US | 1,772,420 | 1,784,125 | -11,705 | -1,604,898 |

WN | 1,935,869 | 1,945,297 | -9,428 | -1,703,841 |

|

| Total | -40,361 | -4,366,937 |

JAPAN: Tokyo CPI Watched for Implications on Underlying Inflation

In light of the US-Japan trade deal struck this week, as well as the political uncertainty surrounding Ishiba's standing as PM after the weekend's upper house election results - vols have been sold into this Friday's Tokyo CPI print from Japan. The headline is projected to remain close to 3.0% y/y across the headline and core metrics. This would be down slightly from the June pace, but only marginally. Focus is likely to be services inflation, after the June nation wide CPI print showed slightly firmer pressures in this space.

- Food and energy costs are expected to continue to support the headline - however anecotal evidence of relief in rice prices (the government has released rice reserves this year) could contain inflationary pressures here.

- Any implications for underlying inflation and the BoJ's hiking path will be of interest. Markets remain partially priced for a BoJ rate hike this year - but differences remain over the likelihood of a hike at either the October or December meeting (priced at +17bps and +22bps respectively).

CHINA-EU: Die Welt Reports VdL Plans "Surprise" On Tariffs

(MNI) London-Following an earlier meeting with Chinese President Xi Jinping, European Commission President Ursula von der Leyen and Council President Antonio Costa have held talks with Premier Li Qiang as part of the China-EU summit in Beijing. Reuters reports Li as saying, "China and the EU share extensive common interest and have no fundamental conflicts of interest...Partnership is the correct positioning." Li: "China and Europe should cooperate more closely."

- VdL: "...our trade relationship today needs more balance [...] What needs to be done to achieve rebalancing: Increase market access for European companies in China, limit the external impact of overcapacity, reduce export controls are important steps forward. On each of these topics, when our concerns are not addressed, our industry and citizens will demand that we defend our interests."

- Germany's Die Welt reports that, despite expectations being low due to the truncation of the summit, "...von der Leyen is planning a surprise. Due in part to pressure from Berlin, the EU Commission has been negotiating for weeks about lifting the tariffs so hated in Beijing, provided Chinese companies are simultaneously willing to make so-called price undertakings." This would see Chinese firms voluntarily increase prices in order to avoid anti-dumping levies.

- Finbarr Bermingham at SCMP posts on X: "Nobody I have asked seems to know anything about this. VDL's right-hand man Bjoern Seibert is not in China. Nor is her trade advisor Thomas Baert. Nor is trade commissioner Sefcovic, whose call with Wang Wentao on Tues did not resolve the EV issue. So it would be a huge shock."

US-EU: Commission Spox-No Countermeasures Pre Aug 1, Prepared For All Scenarios

Reuters reports comments from European Commission spox Olof Gill regarding US-EU tariff talks. Nothing new in terms of talks, says that "the EU continues to engage intensively with the US on tariffs...Our focus is on finding a negotiated outcome with the US...We believe such an outcome is within reach." Says that "We have no intention to bring additional countermeasures between now and August 1...But we remain prepared for all scenarios." Livestream here. Spox indicates that the 'anti-coercion instrument' is intended to act primarily as a "deterrent", and that it has many "off ramps" that would allow for a de-escalation.

THAILAND: Acting PM-Fighting Has To Stop Before Negotiations w/Cambodia

Reuters reports comments from Acting Prime Minister Phumtham Wechayachai regarding the escalation in military skirmishes between Thai and Cambodian forces. Says that "Cambodia fired heavy weapons into Thailand without specific targets so civilians were killed." Acting PM: "There has been no declaration of war." Acting PM: "The conflict with Cambodia has not spread to more provinces." Acting PM: "Fighting has to stop first before there are any negotiations with Cambodia".

- As noted earlier (see 'THAILAND: Border Clashes With Cambodia Escalate, Both Sides Pledge To Fight Back', 09:15BST), "The latest exchange of fire marks a significant escalation in a decades-long conflict after Thailand downgraded its diplomatic relations with Cambodia to the lowest possible level."

- Tita Sanglee, a Thailand-based associate fellow at the ISEAS–Yusof Ishak Institute think tank told the Daily Telegraph, "...the pressure on Thai political as well as military leaders is mounting. Continued restraint may no longer be viable as it risks escalating a crisis of public trust.” She added that there are a number of people in Thailand [...] who feel the government has “been too slow and too soft compared to Cambodia’s swift and tough approach. “So, as things stand, I don’t see de-escalation coming soon. The real question is how far the fighting might go.”

FOREX: GBP/AUD Slips on Contrasting PMIs

- AUD is once again top of G10 FX Thursday, continuing to benefit from the buoyant price action for major equity indices, greater optimism surrounding China and the resumption of dollar weakness this week. Additionally, the July flash composite PMI rose to 53.6 from 51.6 in June, representing the highest reading since April 2022 and offsetting concerns following the weaker-than-expected labour market report last week. RBA Governor Bullock stated in overnight remarks that the labour market has eased only gradually and the rise in the unemployment rate was not a shock for the central bank. She confirmed a measured, gradual approach to policy is appropriate.

- Meanwhile, the weaker-than-expected services PMI in the UK weighs moderately on sterling after the release, prompting a brief test back below 1.3550 for GBPUSD, currently down 0.2% on the session. The renewed dollar weakness this week has allowed cable to recover well from recent pullback lows, negating the prior break below trendline support, drawn from the January lows.

- This keeps more of a focus on EURGBP, which has risen back above 0.8680 and narrows in on a cluster of daily highs across July, just below the 0.8700 handle. A break through here would place the focus on key resistance at 0.8738, the Apr 11 high. A dominant uptrend remains in place for the cross.

- The ECB rate decision takes focus going forward. President Lagarde last month signaled that policy was in a good place after a cut to the mid-point of neutral estimates of 1.75-2.25% - and given there haven't been any significant data surprises in the intervening period and some Governing Council members have talked of a higher bar to cut rates. We expect today’s communication to be as non-committal as possible, maintaining flexibility and buying time for a fresh forecast round in time for the Sep 11 meeting.

- Canadian retail sales, weekly US jobless claims and the prelim US PMI numbers are the data highlights Thursday. The Fed remain inside their pre-meeting media blackout period.

OPTIONS: Sizeable Options Strikes Skewed Lower for Spot Into Post-ECB Cut

A sizeable post-ECB decision options pipeline worth monitoring, with strikes skewed lower - in particular layered between 1.1620-60, summing to near E7bln. Full list here:

- EUR/USD: $1.1500-10(E1.4bln), $1.1550(E908mln), $1.1620-30(E4.3bln), $1.1645-60(E2.2bln), $1.1700(E2.0bln), $1.1750-60(E1.7bln), $1.1800(E985mln)

- USD/JPY: Y146.00-05($570mln), Y147.00-10($1.1bln), Y147.50($1.6bln)

- AUD/USD: $0.6600(A$886mln), $0.6625-30(A$596mln)

- USD/CAD: C$1.3785($617mln)

EQUITIES: Eurostoxx 50 Futures Narrow Gap to Key Resistance and Bull Trigger

- The trend condition in Eurostoxx 50 futures remains bullish and recent weakness appears to have been a correction. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of this level would strengthen a bearish threat. Sights are on key resistance and bull trigger at 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00.

- S&P E-Minis have once again traded to a fresh cycle high this week. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. With the 6400.00 handle cleared, sights are on 6439.88, a Fibonacci projection. Key support is at the 50-day EMA, at 6131.47. Support at the 20-day EMA is at 6277.23.

COMMODITIES: Recent Pullback for Gold Considered Corrective

- A bearish theme in WTI futures remains intact and the recovery since Jun 24 still appears corrective. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower. Support to watch is the 50-day EMA, at $64.70. The average has been pierced, a clear break of it would expose $58.17, the May 30 low. On the upside, Initial resistance to monitor is $69.41, the 50.0% retracement of the Jun 23 - 24 high-low range.

- A bull cycle in Gold that started Jun 30 remains intact, and the latest pullback is - for now - considered corrective. Resistance at $3395.1, the Jun 23 high, has been cleared. A continuation higher would open $3451.3, the Jun 16 high. Note that moving average studies are in a bull-mode position highlighting a dominant uptrend. The bear trigger is $3248.7, the Jun 30 low. An initial firm support to watch is 3282.8, the Jul 9 low.

| Date | GMT/Local | Impact | Country | Event |

| 24/07/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 24/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1245/1445 | ECB Press Conference | ||

| 24/07/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/07/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/07/2025 | 1400/1000 | *** | New Home Sales | |

| 24/07/2025 | 1400/1000 | *** | New Home Sales | |

| 24/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 24/07/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 24/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 24/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 24/07/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 25/07/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 25/07/2025 | 2330/0830 | ** | Tokyo CPI | |

| 25/07/2025 | 0600/0800 | ** | PPI | |

| 25/07/2025 | 0600/0800 | ** | Unemployment | |

| 25/07/2025 | 0600/0700 | *** | Retail Sales | |

| 25/07/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/07/2025 | 0800/1000 | ** | M3 | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 25/07/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 25/07/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |