MNI US MARKETS ANALYSIS - Tsy Curve Flatter into Busy Session

Highlights:

- Treasury curve sits bull flatter into busy session with Treasury supply, big data prints and heavy Fed schedule

- UK political uncertainty here to stay, leaves GBP structurally volatile over medium-term

- JGB stability helping facilitate a JPY rebound

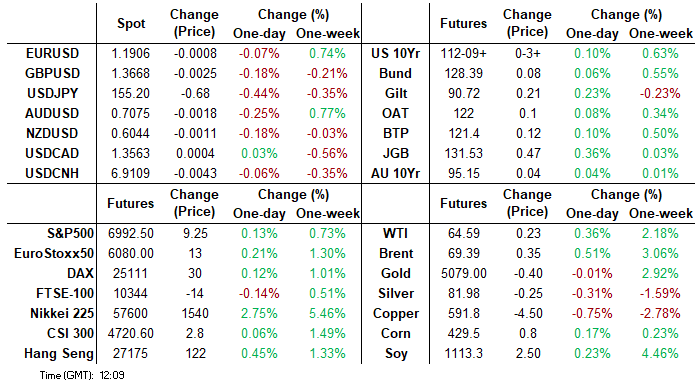

US TSYS: Bull Flatter Before A Busy Docket w/ Retail Sales, Fedspeak 3Y Supply

Treasuries are bull flatter ahead of a busy docket, continuing to pull off a low for Treasuries in yesterday’s overnight session that came as China was said to have asked banks to limit their holdings of US Treasuries. Yesterday’s additional early downward pressure from JGBs following Takaichi’s victory on Sunday reversed today. Note that in addition to a heavy data docket headlined by retail sales and likely hawkish Fedspeak, 3Y supply will be watched for signs of broader appetite after last month's drop in indirect take-up.

- Cash yields are 0.8-2.9bp lower, with declines led by 30s and the front-end still somewhat pinned ahead of NFPs on Wednesday and CPI on Friday.

- TYH6 trades at 112-09 (+03) close to earlier highs of 112-10+, on reasonable cumulative volumes of 320k.

- Resistance is seen at 112-16+ (Feb 6 high) before 112-22 (Jan 7 high). However, a bearish medium-term condition should still see some attention on support at the bear trigger of 111-09 (Jan 20 low) after yesterday’s drop to 111-26.

- Data: NFIB Jan (0600ET – 99.3 vs 99.8 expected), Weekly ADP (0815ET), Retail sales Dec (0830ET), Import/export prices Dec (0830ET), ECI Q4 (0830ET), Weekly Redbook (0855ET), Business inventories Nov (1000ET)

- Fedspeak: Hammack (1200ET), Logan (1300ET) – see STIR bullet

- Coupon issuance: US Tsy $58B 3Y Note auction - 91282CQA2 (1300ET). Last month's 3Y traded almost in-line with a 0.1bp stop thrhough and steady bid-to-cover at 2.65x. The most interesting aspect was a drop in the indirect take-up from 72.0% to 56.5%, its lowest since Jul/Aug 2025 and before thath Dec 2023.

- Bill issuance: US Tsy $90B 6W bill auction (1130ET)

- Politics: WH Press Sec Leavitt press briefing (1300ET), Trump in signing time (1630ET), Trump in policy meeting (1730ET), Trump in private dinner (1900ET)

STIR: Fed Path At Dovish End Of Ytd Range Before Retail Sales & FOMC Hawks

- Fed Funds implied rates are up to another 1.5bp lower overnight in a move that slowly extends yesterday’s dovish shift on NEC’s Hassett saying not to panic about lower jobs numbers (coming ahead of Wednesday’s NFP report) despite appearing to talk on broader trends.

- Today sees a solid data docket headlined by retail sales where core sales are expected to have remained solid at year-end.

- Cumulative cuts from 3.64% effective: 5bp Mar, 10.5bp Apr, 26bp Jun, 34.5bp Jul, 46.5bp Sep, 53bp Oct and 58.5bp Dec.

- SOFR futures are 0.5-1 tick firmer, with a terminal implied yield of 3.115% (Z6, -0.5bp) remaining at the low end of a ytd range of 3.095-3.285% looking at closes.

- Today’s Fedspeak comes from two of the most hawkish FOMC members, both with current year voting roles, in first updates since Nov/Dec.

- 1200ET - Cleveland Fed’s Hammack (’26 voter, hawk) on the banking and economic outlook (text + Q&A). She said on Dec 12 that she would prefer a slightly more restrictive policy stance and that Trump legislation will add a “decent” stimulus in 2026.

- 1300ET – Dallas Fed’s Logan (’26 voter, hawk) in moderated discussion (text). She said in November that she was going to find it hard to support a December rate cut and that she’s not convinced that there are signs that inflation is moving back to 2%.

US PREVIEW: ICYMI- MNI US Payrolls Preview: Watch The Forest, Not Just The Trees

In case missed late yesterday, we've published our preview of the upcoming US Employment Report. Refer to the publication (link) for the following:

- Dispersion of analyst views across nonfarm payrolls growth, the unemployment rate and wage growth

- Pertinent detailed comments from analysts across the spectrum of views

- MNI analysis of a range of alternate labor indicators

- A dovish build-up to the release after last week's soft labor updates and Hassett comments

In addition to the usual areas covered in the preview, this month we also discuss:

- Annual benchmark revision estimates

- A new birth/death model

- Seasonality and seasonal factor revisions covering the past five years of data

US TSY FUTURES: Net Long Setting Most Prominent On Monday

OI data points to net long setting (TU, TY, UXY & WN) outweighing instances of net short cover (FV & US) as Tsy futures ticked higher on Monday, with ~$3.5mln DV01 of fresh net exposure added in curve-wide terms.

| 09-Feb-26 | 06-Feb-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,703,036 | 4,688,031 | +15,005 | +552,313 |

FV | 6,866,716 | 6,887,141 | -20,425 | -875,532 |

TY | 5,476,440 | 5,445,362 | +31,078 | +2,045,373 |

UXY | 2,576,899 | 2,551,238 | +25,661 | +2,288,330 |

US | 1,707,852 | 1,715,980 | -8,128 | -1,125,299 |

WN | 2,178,856 | 2,175,525 | +3,331 | +612,457 |

|

| Total | +46,522 | +3,497,641 |

SOFR: Mix Of Net Long Setting & Short Cover Seen In Futures On Monday

OI data points to a mix of net long setting and short cover as most SOFR futures ticked higher on Monday, albeit with little in the way of meaningful net positioning swings to note.

| 09-Feb-26 | 06-Feb-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,354,313 | 1,351,185 | +3,128 | Whites | -1,443 |

SFRH6 | 1,351,188 | 1,349,037 | +2,151 | Reds | -15,303 |

SFRM6 | 1,437,385 | 1,438,394 | -1,009 | Greens | +10,849 |

SFRU6 | 1,423,611 | 1,429,324 | -5,713 | Blues | +6,206 |

SFRZ6 | 1,402,351 | 1,405,902 | -3,551 |

|

|

SFRH7 | 962,171 | 970,215 | -8,044 |

|

|

SFRM7 | 889,050 | 889,700 | -650 |

|

|

SFRU7 | 838,768 | 841,826 | -3,058 |

|

|

SFRZ7 | 913,516 | 906,834 | +6,682 |

|

|

SFRH8 | 520,117 | 521,210 | -1,093 |

|

|

SFRM8 | 441,580 | 438,339 | +3,241 |

|

|

SFRU8 | 394,983 | 392,964 | +2,019 |

|

|

SFRZ8 | 374,845 | 374,838 | +7 |

|

|

SFRH9 | 216,867 | 217,631 | -764 |

|

|

SFRM9 | 213,087 | 209,487 | +3,600 |

|

|

SFRU9 | 177,374 | 174,011 | +3,363 |

|

|

SWAPS: Long End UK Swap Spreads Extend Recovery As Political Noise Slows

Long end UK swap spreads continue to rally from Friday’s year-to-date lows, with public ministerial support for PM Starmer (albeit with questions over how long such support will ultimately last) helping remove some of the acute repricing of UK fiscal & political risk premia that dominated both last week and in early Monday trade.

- A reminder that the presence of a by-election (later this month) and local elections (in May) are seemingly prolonging Starmer’s stay in office at this stage.

- The 10-Year swap spread is already within 1bp of year-to-date highs, while the outright 10s30s gilt curve failed to challenge November highs during the recent gilt sell off (a reminder that the DMO has skewed the WAM of its issuance profile shorter in recent times, which allowed the super long end to outperform in ’26).

- We had previously warned that political and fiscal risk premia could come back to the fore for gilts, although that played out much sooner than we anticipated.

- Note that markets remained orderly during the sell off, with the reforms that came in the wake of the LDI crisis/Truss moment and BoE liquidity provisions removing some of the risks of disorderly market function.

- Still, recent sessions remind us how quickly the situation can change and provide some insight into how the UK long end would react is PM Starmer is replaced by a more left-leaning successor (bear steepening pressure for gilts and underperformance vs. swaps on the assumption that fiscal policy would be looser).

- Late last week Morgan Stanley suggested that “30-Year ASW screens somewhat rich” vs. their regression of fair value, although they did not issue any trade recommendation based on that view.

UK: Political Uncertainty Here to Stay, What Does This Mean for Markets?

We see the political machinations in the UK over the past few weeks as becoming much more well-priced. While yesterday’s resilience from Starmer is unlikely to reverse the tide of his premiership (Polymarket odds are against Starmer retaining office beyond the end of June – reaching 70% this week), it does mean the fiscal and political approach of the UK is likely to shift to the left in the second half of this parliament, regardless of who leads the party.

- This likely means a re-correlation between UK bond and currency prices, and a change in leadership (whether it’s Rayner, Streeting or, slightly less likely, Burnham) will introduce fiscal uncertainty – playing into the broader views of structural uncertainty for GBP (see more here: https://www.mnimarkets.com/articles/currency-strength-is-latest-sign-that-leftward-shift-is-well-priced-1770642155124 ).

- What’s slipped out of market focus is the possibility that Starmer not only survives both by-election and May local election risks, but throughout the rest of the year. While a swift recovery in his public popularity from current low levels is unlikely – there is a tangible sequence of events where lasts into 2027 – and beyond:

- A narrow Labour hold in Gorton and Denton, expectations management in May (“could have been worse”), no path to becoming an MP for Burnham, a false start for Streeting’s leadership bid (his ties to Mandelson and right-of-Starmer policies) and sufficient market volatility that could scare MPs off any Rayner attempt to become leader.

UK: Market implications of current spell of uncertainty

Near-term, GBPUSD is once again in an area of indecision. Following yesterday’s recovery, spot prices are coalescing around 1.3663 – conveniently the 38.2% retracement of the YTD range. In fact, this chart pattern has helped define pivot points, support and resistance for the pair so far this month – which should raise focus on these levels through any incoming price action.

Source: MNI / Bloomberg Finance L.P.

Longer-term, GBPUSD looks prime to be re-rated should there be an extended spell of uncertainty. Consensus looks for a rise to 1.39 into 2027 from 1.36 at the end of Q2 this year, a view that may be challenged should the increasingly positive analyst and technical view on EURGBP so far in 2026 continue to play out. Our broader technical view on EURGBP here:

Source: MNI / Bloomberg Finance L.P.

This leaves GBP implied vols looking particularly lumpy over the medium-term, with 6m vols narrowing in on 8 points this week. Notably, this puts outright vol at levels comparable with early July last year and, in particular, the rally that coincided with Chancellor Reeves’ appearance in the Commons that triggered questions about Starmer's leadership and the sustainability of his government.

JPY: JGB Stability Facilitates Yen Rebound, March BOJ Decision Eyed

- Japanese assets have firmed on Tuesday, bolstered by comments from Finance Minister Katayama, who appears to have successfully calmed the markets on the timing and financing of the sales tax cut. Katayama said that PM Sanae Takaichi has made it clear that the tax cut is strictly limited to two years, will not rely on debt issuance and will apply only to food and beverages.

- Stabilisation across the JGB curve has facilitated an extension of the Japanese yen rebound, with the USDJPY pullback from yesterday’s post-election high briefly reaching 1.72% at today’s 155.05 low. Price action increasingly blurs the technical picture, as spot is cleanly below through the 50-day EMA which may bolster the short-term bearish outlook. The 100-day MA intersects at 154.52.

- While the broader dollar weakness may have played its part in exacerbating the USDJPY price action, analysts have noted that the next meaningful leg lower might require a BOJ tightening impulse. We pointed out last week that JP Morgan read the latest BOJ minutes as hawkish, and that with some political stability post-election they believed the BOJ could hike in March, which could also lead to some shift in local flow dynamics.

- A BOJ rate hike in March remains feasible as real interest rates remain low and the risk of falling behind the curve persists, former BOJ chief economist Toshitaka Sekine told MNI on Friday. Furthermore, PM Takaichi has been taking market concerns over inflation and fiscal sustainability seriously and will not interfere with the BOJ’s gradual policy tightening from the current 0.75%, MNI understands.

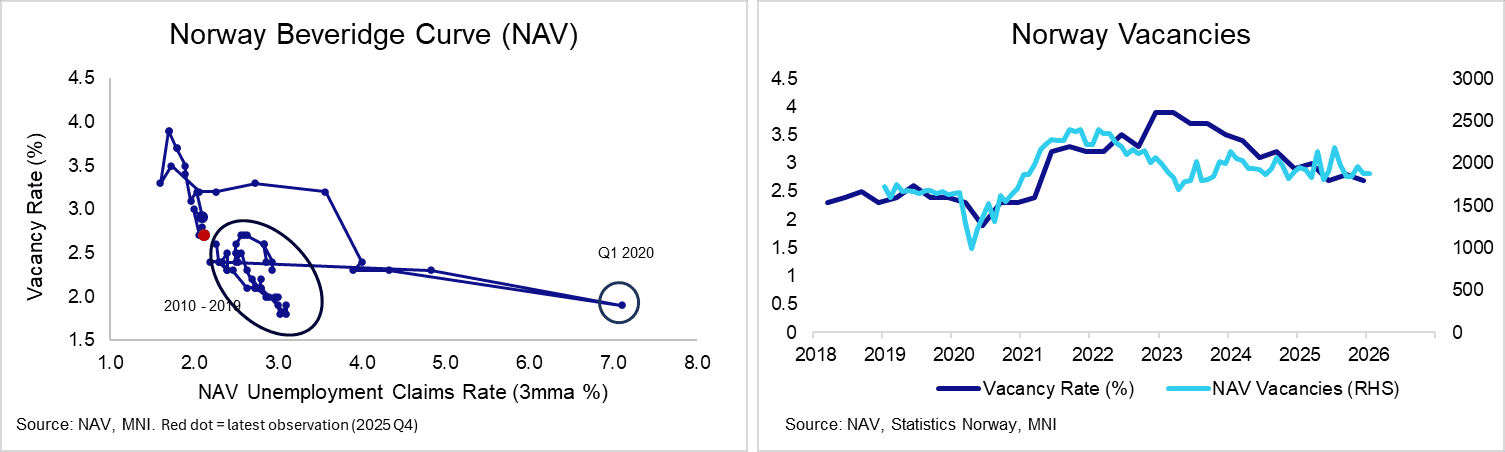

NORWAY: No Cut Scenario For 2025 Should Not Be Underappreciated

The NOK Mar27-Jun27 FRA rate has risen a notable 21.5bps following this morning’s higher-than-expected January inflation data. The contract now trades at 4.11%, just 4bps below last Friday’s 3m NIBOR fixing. Norges Bank has previously guided for “one or two” cuts this year, but the resurgence of inflation pressures, alongside the marginally hawkish signals from yesterday’s national accounts, suggest a no-cut scenario should not be underappreciated.

- We’ve already seen some hawkish forecast revisions since the data. Both DNB and Handelsbanken have removed calls for a June rate cut, now seeing no more easing in the immediate term. A number of analysts had also been calling for a March cut – we wouldn’t be surprised to see these calls revised in the coming days.

- Elsewhere, the job vacancy rate fell back to 2.7% in Q4 (vs 2.8% in Q3, 2.7% in Q2). This dynamic had been well signalled in monthly NAV data, and so doesn’t impact the Norges Bank stance.

- The Norwegian Beveridge curve has approached the 2010-2019 area in recent quarters, but the low registered unemployment rate signals continued labour market tightness. This tightness has contributed to persistent wage pressures. Annual earnings growth of 5.0% for 2025 was well above the ~1% mainland productivity growth, and thus remains inconsistent with the 2% inflation target.

EUROPE ISSUANCE UPDATE:

EU Dual-Tranche Syndication: Spread/size set

- E6bln from E5bln guidance (MNI expected E4-5bln) tap of the 2.75% Dec-32 EU-bond. Books in excess of E75bln, Spread set at MS + 17bp (guidance was MS +19bps area).

- E5bln confirmed (MNI expected E4-5bln) tap of the 3.75% Oct-45 EU-bond. Books in excess of E69bln, Spread set at MS + 70bp (guidance was MS +72bps area).

France 30-year Syndication: Mandate

- France has sent a mandate "on an upcoming new 30 year OAT benchmark, due 25 May 2057. The transaction will be launched by syndication in the near future, subject to market conditions."

- This is not a surprise. We had written in our Issuance Deep Dive: "New 30-year OATs have been launched in February in each of 2025, 2024 and 2023 (as well as in January 2022). We think it highly likely that this pattern will continue and note that there is just over E20bln outstanding of the current 3.75% May-56 OAT (similar to the amount outstanding of the 3.25% May-55 OAT ahead of last year's syndication). Our base case is that the launch syndication is sized at E8bln (in line with the two previous 30-year launches)."

- We look for the transaction to take place tomorrow.

Slovakia 20-year Syndication: Mandate

- Slovakia has sent a mandate on a "new Reg S Bearer EUR benchmark offering, with a 20-year maturity, will follow in the near future subject to market conditions."

- This is in line with our expectations. We had written in our Issuance Deep Dive: "We expect the 12-20-year SlovGB to launch via syndication in February, but don't rule out a late January syndication. There has been a February syndication in each of the past three years... we think a 2045 or 2046 maturity is most likely (the bonds maturing in Feb-43 and Oct-47 are both still available for tapping). We pencil in a transaction size of E2.0-3.0bln (although the guidance from ARDAL is for E2.0-2.5bln)."

- We look for the transaction to take place tomorrow.

Netherlands auction results:

- E1.845bln of the 3.25% Jan-44 Green DSL. Avg yield 3.388%.

Gilt auction results

- Decent gilt auction with 0.2bp tail (as in the past two auctions). The bid-to-cover at 3.94x was high, but that is largely due to the amount on offer being lower at GBP3.75bln rather than GBP4.25bln today. The volume of bids is actually a little lower than the previous auction.

- The LAP (lowest accepted price) was in excess of any seen during the bidding window and the 4.125% Mar-31 gilt moved higher on the results. Gilt futures also moved over 5 ticks higher to their intraday highs on the results.

- GBP3.75bln of the 4.125% Mar-31 Gilt. Avg yield 4.001% (bid-to-cover 3.94x, tail 0.2bp).

Austria auction results:

- E978mln (E850mln allotted) of the 0% Feb-31 RAGB. Avg yield 2.52% (bid-to-cover 3.67x; bid-to-issue 3.19x).

- E748mln (E650mln allotted) of the 3.20% Feb-36 RAGB. Avg yield 3.098% (bid-to-cover 4.74x; bid-to-issue 4.12x).

Germany auction results:

- E5bln (E3.811bln allotted) of the 2.50% Apr-31 Bobl. Avg yield 2.4% (bid-to-offer 1.26x; bid-to-cover 1.65x).

FOREX: Japanese Yen Extends Post-Election Recovery

- The Japanese yen has strengthened after Finance Minister Katayama calmed markets on the timing and financing of the sales tax cut for food. Downside momentum for USDJPY has picked up pace, extending the reversal from yesterday’s post-election high to around 1.6%, and printing a pullback low of 155.09.

- Price action increasingly blurs the technical picture for USDJPY as spot is cleanly below through the 50-day EMA which may bolster the short-term bearish outlook. The 100-day MA intersects at 154.52.

- The January acceleration in Norwegian CPI-ATE looks broad-based, with start-of-year price resets in the likes of rents and insurance highlighted. Any scope for payback in February won't be enough to ease Norges Bank concerns around inflation persistence, which leads EURNOK 0.35% lower with initial support at the Jan 29 low of 11.3610.

- Last week’s stabilisation and then subsequent recovery for risk have spurred an impressive 2.9% AUDUSD rebound from Friday’s low. This culminated in AUDUSD printing a fresh cycle high late Thursday, at 0.7099, the highest level since February 2023. While the 0.71 handle has capped the price action overnight, the session range has remained narrow, allowing the pair to consolidate the solid bounce.

- GBP consolidates its recovery seen yesterday afternoon following PM Starmer securing the public support of every cabinet minister after his future came under threat for his involvement with former ambassador Mandelson. Any market caution around Starmer's future has two legs as the fiscal angle adds to political instability. 1.37 has been capping short-term gains for GBPUSD.

- Separately, downside momentum for EURCHF has extended on Tuesday, resulting in fresh lows at 0.9120 today, the lowest level since the removal of the peg in 2015.

- US retail sales, ECI, import and export prices, redbook retail sales, and business inventories are on the calendar ahead of US payrolls (Wed) and CPI (Fri).

OPTIONS: Expiries for Feb10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1850(E1.1bln), $1.1875(E787mln), $1.1900-10(E1.9bln), $1.1945(E567mln), $1.2000(E1.5bln

- USD/JPY: Y157.00($884mln)

- AUD/USD: $0.6900(A$1.2bln), $0.7100(A$1.2bln)

EQUITIES: E-Mini S&P Trading Just Below the Late-January Highs

- The medium-term trend condition in EuroStoxx 50 futures remains bullish and the latest pullback through the 50-day EMA appears corrective. A clear break below this average would undermine the bull theme and signal scope for a deeper retracement. The bull trigger is at 6086.00, the Jan 3 high. A move through this hurdle would resume the primary uptrend.

- A short-term bearish theme in S&P E-Minis resulted in a break last week of 6814.50, the Jan 21 low and a bear trigger. This proved short-lived, however, with prices rising swiftly back above to begin this week. Note this puts the contract back above the 20- and 50-day EMAs. Any continuation lower would open 6691.56, a Fibonacci retracement point. The contract has recovered today. Initial firm resistance now is 7025.43, the 1.0% 10-dma envelope. A break of this hurdle would be bullish.

COMMODITIES: WTI Futures Bull Cycle Intact, Remains Above 20-, 50-Day EMAs

- A bull cycle in WTI futures remains intact. However, the reversal from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $62.16. The 50-day EMA lies at $60.50. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high.

- The latest bounce in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

| Date | GMT/Local | Impact | Country | Event |

| 10/02/2026 | 1200/0700 | ** | Brazil Final CPI | |

| 10/02/2026 | - | *** | New Loans | |

| 10/02/2026 | - | *** | Money Supply | |

| 10/02/2026 | - | *** | Social Financing | |

| 10/02/2026 | 1330/0830 | *** | Employment Cost Index | |

| 10/02/2026 | 1330/0830 | ** | Import/Export Price Index | |

| 10/02/2026 | 1330/0830 | *** | Retail Sales | |

| 10/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 10/02/2026 | 1500/1000 | * | Business Inventories | |

| 10/02/2026 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 10/02/2026 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 10/02/2026 | 1800/1300 | Dallas Fed's Lorie Logan | ||

| 10/02/2026 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 11/02/2026 | 0130/0930 | *** | CPI | |

| 11/02/2026 | 0130/0930 | *** | Producer Price Index | |

| 11/02/2026 | 0900/1000 | * | Industrial Production | |

| 11/02/2026 | 1020/1120 | ECB's Cipollone In Digital Finance Conference Fireside Chat | ||

| 11/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 11/02/2026 | 1330/0830 | * | Building Permits | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1510/1010 | Kansas City Fed's Jeff Schmid | ||

| 11/02/2026 | 1515/1015 | Fed Vice Chair Michelle Bowman | ||

| 11/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 11/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/02/2026 | 1700/1800 | ECB's Schnabel Lecture At Austrian Academy of Sciences | ||

| 11/02/2026 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/02/2026 | 1830/1330 | Bank of Canada meeting minutes | ||

| 11/02/2026 | 1900/1400 | ** | Treasury Budget | |

| 11/02/2026 | 2100/1600 | Cleveland Fed's Beth Hammack |