STIR: Fed Path At Dovish End Of Ytd Range Before Retail Sales & FOMC Hawks

Feb-10 11:32

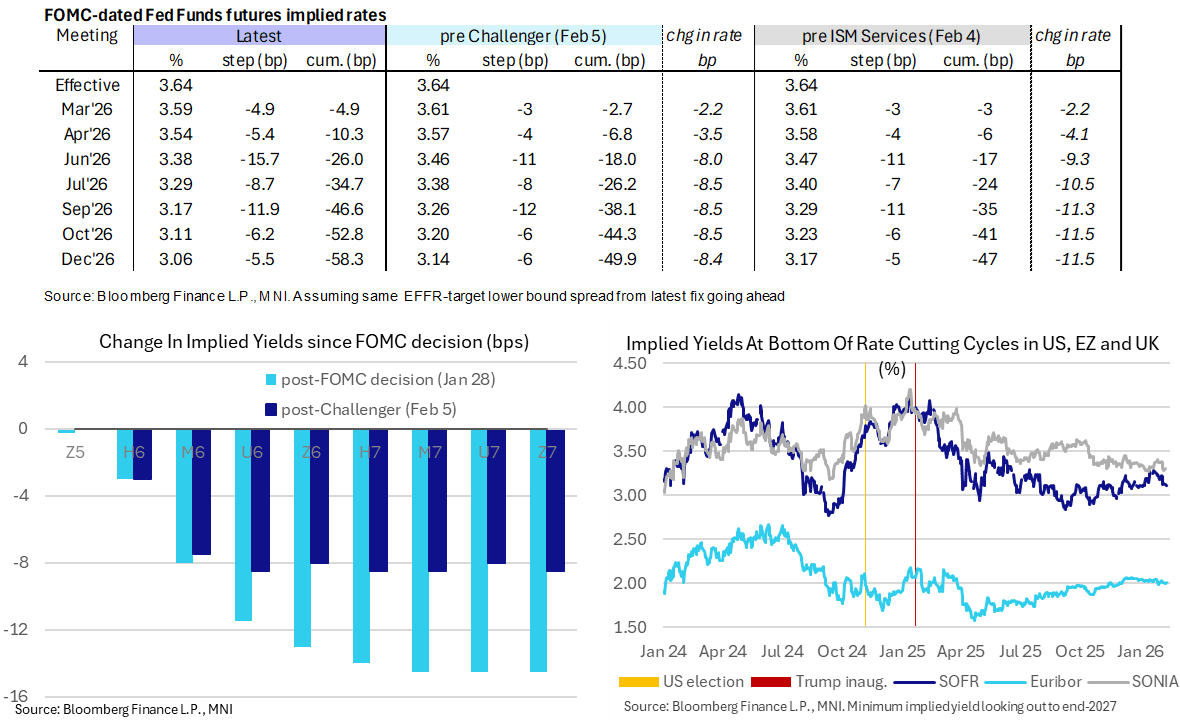

- Fed Funds implied rates are up to another 1.5bp lower overnight in a move that slowly extends yesterday’s dovish shift on NEC’s Hassett saying not to panic about lower jobs numbers (coming ahead of Wednesday’s NFP report) despite appearing to talk on broader trends.

- Today sees a solid data docket headlined by retail sales where core sales are expected to have remained solid at year-end.

- Cumulative cuts from 3.64% effective: 5bp Mar, 10.5bp Apr, 26bp Jun, 34.5bp Jul, 46.5bp Sep, 53bp Oct and 58.5bp Dec.

- SOFR futures are 0.5-1 tick firmer, with a terminal implied yield of 3.115% (Z6, -0.5bp) remaining at the low end of a ytd range of 3.095-3.285% looking at closes.

- Today’s Fedspeak comes from two of the most hawkish FOMC members, both with current year voting roles, in first updates since Nov/Dec.

- 1200ET - Cleveland Fed’s Hammack (’26 voter, hawk) on the banking and economic outlook (text + Q&A). She said on Dec 12 that she would prefer a slightly more restrictive policy stance and that Trump legislation will add a “decent” stimulus in 2026.

- 1300ET – Dallas Fed’s Logan (’26 voter, hawk) in moderated discussion (text). She said in November that she was going to find it hard to support a December rate cut and that she’s not convinced that there are signs that inflation is moving back to 2%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

Jan-10 22:45

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Jan-09 23:36

Test Test TEST

MNI: MNI Test, Please Ignore

Jan-09 23:30

Test, ignore