NORWAY: No Cut Scenario For 2025 Should Not Be Underappreciated

The NOK Mar27-Jun27 FRA rate has risen a notable 21.5bps following this morning’s higher-than-expected January inflation data. The contract now trades at 4.11%, just 4bps below last Friday’s 3m NIBOR fixing. Norges Bank has previously guided for “one or two” cuts this year, but the resurgence of inflation pressures, alongside the marginally hawkish signals from yesterday’s national accounts, suggest a no-cut scenario should not be underappreciated.

- We’ve already seen some hawkish forecast revisions since the data. Both DNB and Handelsbanken have removed calls for a June rate cut, now seeing no more easing in the immediate term. A number of analysts had also been calling for a March cut – we wouldn’t be surprised to see these calls revised in the coming days.

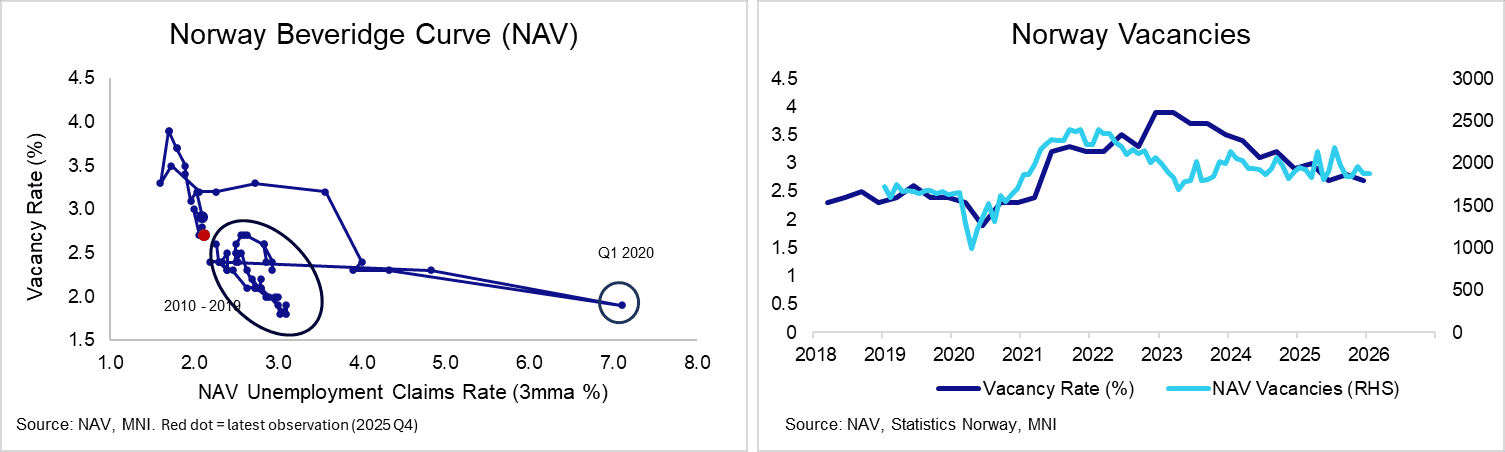

- Elsewhere, the job vacancy rate fell back to 2.7% in Q4 (vs 2.8% in Q3, 2.7% in Q2). This dynamic had been well signalled in monthly NAV data, and so doesn’t impact the Norges Bank stance.

- The Norwegian Beveridge curve has approached the 2010-2019 area in recent quarters, but the low registered unemployment rate signals continued labour market tightness. This tightness has contributed to persistent wage pressures. Annual earnings growth of 5.0% for 2025 was well above the ~1% mainland productivity growth, and thus remains inconsistent with the 2% inflation target.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Test Test TEST

MNI: MNI Test, Please Ignore

Test, ignore