MNI US MARKETS ANALYSIS - Trump's Tariff Streak Continues

Highlights:

- Trump tariff streak continues; EU letter due, proposes 35% levy on Canadian goods

- CAD volatility in focus ahead of jobs report, market expects unemployment rate to reach new post-COVID high

- Equity futures softer, but remain well within range of record highs

US TSYS: Off Overnight Highs, Trump Proposes 35% Tariff on Canada, Details TBA

- Tariff headlines buoyed Treasuries briefly overnight -- gaining after Pres Trump announced a 35% tariff on Canada starting August 1, while considering 15%-20% tariffs on most other trading partners.

- Support for Treasuries gradually faded as exact tariff details still to be annc'd (whether USMC trade exemptions will still apply). Rates ignored Trump to make a "major statement" on Russia Monday while stocks retreated.

- Currently, Sep'25 10Y futures trade -8 at 110-31 vs. 110-29 low (10Y yld tapped 4.3914% high), breaching the 50-day EMA, at 110-31+. This undermines a recent bull theme and exposes 110-17 next, a Fibonacci retracement point and a key support. Resistance to watch is at 111-28, the Jul 3 high.

- Curves rebound from Thursday's lows, 2s10s +2.083 at 49.641, 5s30s +1.481 at 94.835.

- Projected rate cut pricing consolidate slightly vs late Thursday (*) levels: Jul'25 at -1.7bp, Sep'25 at -17.8bp (-18.8bp), Oct'25 at -32.7bp (-34.2bp), Dec'25 at -50.9bp (-52.6bp).

- Data limited to Federal Budget Balance (-$316.0B prior, -$33.5B est) at 1400ET. Focus on next week's CPI, PPI, Retail Sales and UofM inflation/sentiment data.

- Scheduled Fed speaker: Chicago Fed Pres Goolsbee podcast at 1300ET: Moody's Talks: Inside Economics.

US TSY FUTURES: Mix Of Positioning Swings Thursday, Bias Towards Cover

OI data points to a mix of net long cover (TU, FV & TY), short setting (UXY) and short cover (US & WN) as the curve twist flattened on Thursday.

- There was a bias towards cover when it came to curve-wide net positioning, although the largest DV01 swing came via the net short setting in UXY futures.

| 10-Jul-25 | 09-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,332,272 | 4,346,457 | -14,185 | -536,993 |

FV | 7,039,048 | 7,040,447 | -1,399 | -60,165 |

TY | 4,896,968 | 4,916,254 | -19,286 | -1,269,506 |

UXY | 2,442,818 | 2,415,971 | +26,847 | +2,334,339 |

US | 1,820,143 | 1,824,876 | -4,733 | -652,451 |

WN | 1,954,538 | 1,959,480 | -4,942 | -885,203 |

|

| Total | -17,698 | -1,069,981 |

SOFR: Net Long Setting In Whites Most Prominent On Thursday

OI data suggests that net long setting in SFRU5 & Z5 provided the most meaningful positioning swings on the strip on Thursday, with net short setting then seen in SFRH6 as the strip twist steepened.

- Net short setting provided the dominant positioning impetus in the reds, greens and blues, although instances of net long cover were noted in each of those packs.

| 10-Jul-25 | 09-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,298,517 | 1,299,336 | -819 | Whites | +75,202 |

SFRU5 | 1,226,012 | 1,192,240 | +33,772 | Reds | +7,809 |

SFRZ5 | 1,328,619 | 1,293,174 | +35,445 | Greens | +255 |

SFRH6 | 998,093 | 991,289 | +6,804 | Blues | +2,399 |

SFRM6 | 840,276 | 835,852 | +4,424 |

|

|

SFRU6 | 832,555 | 831,330 | +1,225 |

|

|

SFRZ6 | 892,739 | 886,344 | +6,395 |

|

|

SFRH7 | 715,565 | 719,800 | -4,235 |

|

|

SFRM7 | 671,858 | 671,348 | +510 |

|

|

SFRU7 | 474,051 | 471,017 | +3,034 |

|

|

SFRZ7 | 418,417 | 418,566 | -149 |

|

|

SFRH8 | 313,831 | 316,971 | -3,140 |

|

|

SFRM8 | 230,934 | 232,456 | -1,522 |

|

|

SFRU8 | 204,691 | 200,893 | +3,798 |

|

|

SFRZ8 | 201,476 | 201,583 | -107 |

|

|

SFRH9 | 141,148 | 140,918 | +230 |

|

|

EUROPE ISSUANCE UPDATE:

3/7/15-year BTP results

- E3.5bln of the 2.35% Jan-29 BTP. Avg yield 2.47% (bid-to-cover 1.52x).

- E3.5bln of the 3.25% Jul-32 BTP. Avg yield 3.17% (bid-to-cover 1.49x).

- E1.75bln of the 3.85% Oct-40 BTP. Avg yield 4.03% (bid-to-cover 1.67x).

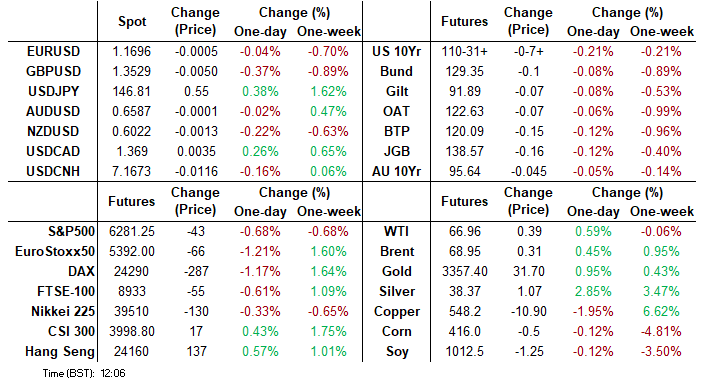

JPY: Some Analysts Remain Bearish USDJPY Despite Solid Recovery

- USDJPY is outperforming Friday as higher core yields provide a supportive backdrop and the market’s long yen position continues to be tested/unwound. A consistent 100 pip grind higher overnight was capped at Wednesday’s weekly high of 147.18, the immediate level of focus. A short-term bull cycle remains in play, bolstered by the latest recovery resulting in a clean break of the 50-day EMA, highlighting a stronger reversal which targets a move back towards 148.03, the Jun 23 high.

- Despite the more constructive price action, JP Morgan and Scotiabank maintain their expectations for a lower USDJPY ahead:

- JP Morgan believe that the gradual unwinding of JPY long positions, due to factors such as 1) rising stock prices and improved risk sentiment, 2) retreating expectations for BOJ rate hikes, 3) fiscal concern in Japan amid heightening uncertainties surrounding domestic politics, 4) waning expectations for a U.S.-Japan currency agreement, and 5) the lack of "de-dollarization" movement in Japan, has driven the JPY weakness since April this year.

- The weak trend of the yen, when viewed on an effective rate basis, is likely to persist. However, based on JP Morgan’s estimates, even if all IMM JPY long positions are unwound, the decline in JPY's nominal effective rate is expected to be relatively small, ranging from -1.6% to -1.4%. JPM maintain their end-2025 target at 140, but the expected decline is likely to be driven by USD weakness, rather than JPY strength.

- Scotiabank are also bearish USDJPY and maintain their forecast for meaningful weakness on the basis of fundamentals. The outlook for relative central bank policy is bullish for the JPY as they look to continued tightening from the BoJ and renewed easing from the Fed. The anticipated narrowing in US-Japan rates is a core component of their USDJPY view, and Scotia hold a year end 2025 target of 135 and a year end 2026 target of 125.

FOREX: CAD Volatility in Focus Ahead of Canadian Jobs Report

- European ranges for G10 FX have been relatively contained in comparison to the punchy moves during the APAC session. The USD index is rising once again, extending its cautious recovery from last week’s cycle lows to ~1.5%. The DXY is again testing above initial 20-day EMA resistance, of which a weekly close above would mark a bullish development.

- One of the key moves overnight was for the Canadian dollar following President Trump’s latest letter to Prime Minister Mark Carney. The announcement that Canada will face a 35% tariff on exports to the United States starting August 1 prompted a rapid spike for USDCAD, from levels around 1.3655 to an intra-day peak of 1.3731. Spot has since settled around the 1.37 mark, but the volatility provides an interesting dynamic ahead of today’s release of Canadian employment data for June, the highlight on the global calendar..

- Elsewhere, USDJPY is outperforming Friday following a consistent 100 pip grind higher overnight to match the weekly highs at 147.18 underpinning a short-term bull cycle that remains in play. The latest recovery has resulted in a breach of the 50-day EMA, highlighting a stronger reversal which will target a move back towards 148.03, the Jun 23 high. Higher US yields have been supportive of the move.

- In similar vein, GBP and NZD are notable underperformers on the session, both declining ~0.4%. For GBPUSD, spot is approaching the lowest levels of the week at 1.3526 following a soft May GDP print and weaker-than-expected industrial production figures. The market will concentrate on key 50-day EMA support which intersects today at 1.3481 and below here, a key trendline drawn from the January lows comes in just above the 1.34 mark.

- AUDNZD (+0.15%) continues its upswing above the May peak to trade at fresh 3-month highs. A sustained break would signal scope for a move back to the early April highs just above the 1.10 mark, being assisted by the Aussie outperformance in the aftermath of the hawkish RBA surprise this week.

CNH: USD/CNY Fixing Downtrend Persists, Error Term Widens

The USD/CNY fixing printed at 7.1475, versus a Bloomberg market consensus of 7.1781.

- This is a fresh low in the fixing back to Nov last year. We continue to see a downtrend in the fixing despite broader stability for USD indices.

- The fixing error also widened a touch to -306pips, from -284pips yesterday.

- USD/CNH is back under 7.1800, off earlier highs at 7.1834. USD sentiment is better elsewhere, aided by Trump's 35% tariff threat against Canada. This leaves CNH an outperformer.

OPTIONS: Expiries for Jul11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E2.1bln), $1.1550(E581mln), $1.1700(E1.4bln), $1.1770(E2.4bln), $1.1825-40(E1.8bln)

- USD/JPY: Y146.30($649mln), Y146.75-90($667mln)

- AUD/USD: $0.6550-60(A$580mln)

- USD/CAD: C$1.3625-45($ C$1.3700-15($1.1bln)

EQUITIES: US Futures Pressure Alltime Highs Despite Incoming Trade Letters

- The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract is trading at its recent highs. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7.

- Eurostoxx 50 futures have traded higher this week as the contract extends the recovery that started Jun 23. This exposed key resistance and the bull trigger at 5486.00, the May 20 high.

COMMODITIES: WTI Crude Futures Steady After Thursday Drift

- Recent weakness in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5.

- WTI futures maintain a bearish tone following the reversal from the Jun 23 high, and recent gains appear corrective. Support to watch is the 50-day EMA, at $65.27. The average has been pierced, a clear break of it would signal scope for a deeper retracement.

| Date | GMT/Local | Impact | Country | Event |

| 11/07/2025 | 1130/1330 | ECB Cipollone At Ukraine Recovery Conference | ||

| 11/07/2025 | 1230/0830 | *** | Labour Force Survey | |

| 11/07/2025 | 1230/0830 | * | Building Permits | |

| 11/07/2025 | 1230/0830 | *** | Labour Force Survey | |

| 11/07/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1800/1400 | ** | Treasury Budget |