MNI US MARKETS ANALYSIS - Trump Takes Dim View of Powell

Highlights:

- US assets volatile as Trump says Powell "termination cannot come fast enough!"

- ECB seen cutting a further 25bps, with neutral views eyed carefully

- USDJPY recovers off cycle lows as "good progress" seen in trade talks

US TSYS: Modestly Lower; Claims Headline Docket Before Early Cash Close

- Treasuries have pared losses with US President Trump contesting Fed independence with comments including "Powell's termination cannot come fast enough!".

- Earlier losses had been seen through Asia and Europe hours with net gains for equity futures in a reversal of a slide seen after Fed Chair Powell reiterated previous no need to hurry rhetoric and warning on inflation risks.

- Jobless claims data headlines today’s docket before cash trading sees an early close at 1300ET ahead of Good Friday tomorrow Futures see a full session today though.

- Cash yields are 2.7-3.6bp higher across the curve, holding within yesterday’s ranges throughout the session.

- TYM5 has lifted off earlier lows but hold a net decline to 111-07 (06+) on low cumulative volumes of 250k. Gains are considered corrective with resistance at 111-17+ (Apr 16 high) whilst support is seen at 110-15 (Apr 15 low) before a bear trigger at 109-08 (Apr 11).

- Data: Weekly jobless claims (0830ET), Housing starts/building permits Mar (0830ET), Philly Fed mfg Apr (0830ET)

- Fedspeak: Barr (1145ET, text + Q&A)

- Coupon issuance: US To Sell $25bn 5-Year TIPS - 91282CNB3 (1130ET)

- Bill issuance: US To Sell $85bn 4-Week, $75bn 8-Week (1000ET)

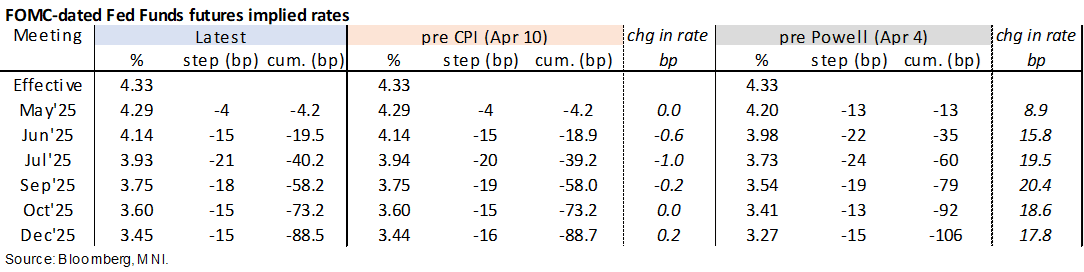

STIR: Fed Rates Back Near Unchanged Since Powell On Trump Termination Threat

- Fed Funds implied rates for 2025 meetings have been dragged 1-1.5bp lower by President Trump’s truth social post calling for the Fed to cut rates and that “Powell’s termination cannot come fast enough!”.

- Cumulative cuts from 4.33% effective: 4bp May, 19.5bp Jun, 40bp Jul, 58bp Sep and 88.5bp Dec.

- The path is now back near unchanged from just before Powell’s text was released, having closed lower before rising through Asia hours helped by net gains for equity and crude oil futures.

- Recall that by Powell repeating his assessment from less than two weeks ago that the tariffs and their likely effects are "significantly larger than anticipated" it may be construed as a slightly hawkish signal as he doesn't seem swayed by the subsequent April 9th 90-day tariff "pause" or market dislocations in the interim. He followed up in Q&A with "I do think we'll be moving away from" the dual mandate goals “probably for the balance of this year. Or at least not making any progress, and then we'll resume that progress as we can."

- Ahead, Fed Gov. Barr (permanent voter) in a fireside chat at a conference on cyber risk (1145ET, text + Q&A) is unlikely to be a market mover. In the event there is any monetary policy discussion, it will be his first remarks since “Liberation Day” tariffs having said that interest rates and lending standards are still high and tight.

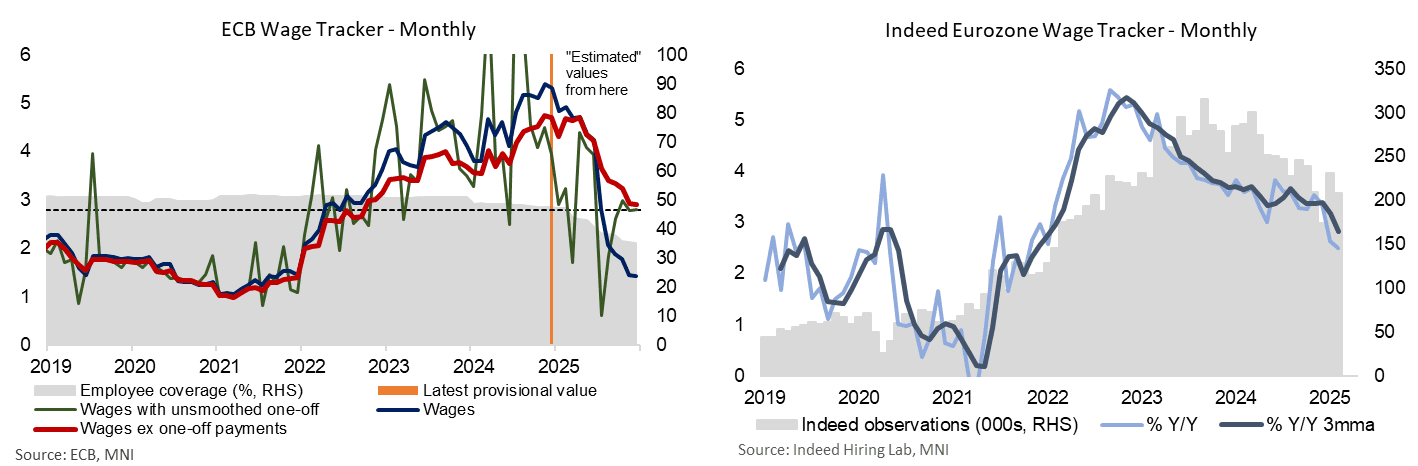

ECB: Macro Since Last ECB: Labour - Solid But Wage Growth Easing Still Eyed

- Labour data since the early March ECB meeting pointed to a solid picture prior to potential tariff impacts.

- The unemployment rate surprisingly pushed a tenth lower to a new series low of 6.1% in February.

- Whilst the rounded data can make it hard to get a sense of the scope of the latest improvement, it came with a solid 70k monthly decline in the seasonally adjusted level of unemployment after a modest 30k decline in January and a rare 49k increase in December at what was its largest increase since Jan 2024.

- That said, whilst the unemployment rate may have continued its trend decline, we see the ECB’s latest forward-looking wage tracker as consistent with President Lagarde's rhetoric at the March press conference: "Recent wage negotiations point to a continued moderation in labour cost pressures".

- Negotiated wage growth excluding one-off payments are tracking at 3.02% for 4Q25, a touch above the 2.97% reported in February, but still what would be notable moderation from the 4.66% estimated wage growth for 4Q24.

- The ECB projects compensation per employee growth to ease to 2.8% Y/Y by 4Q25, from 4.1% in 4Q24.

US TSY FUTURES: Net Long Setting Seen Across The Curve On Wednesday

OI data points to net long setting across all contracts during yesterday’s rally, with nearly $10mln DV01 equivalent of fresh net exposure added across the curve.

- The most meaningful net long setting seemed to come in FV futures.

| 16-Apr-25 | 15-Apr-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,038,667 | 3,990,944 | +47,723 | +1,794,078 |

FV | 6,474,022 | 6,402,110 | +71,912 | +3,106,069 |

TY | 4,777,800 | 4,755,493 | +22,307 | +1,444,636 |

UXY | 2,234,458 | 2,219,886 | +14,572 | +1,287,998 |

US | 1,805,476 | 1,801,369 | +4,107 | +523,316 |

WN | 1,843,495 | 1,835,728 | +7,767 | +1,439,134 |

|

| Total | +168,388 | +9,595,231 |

STIR: Mix Of Long Setting & Short Cover In SOFR Futures On Wednesday

OI data points to relatively contained rounds of net long setting and short cover across most of the SOFR futures strip on Wednesday.

| 16-Apr-25 | 15-Apr-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,121,829 | 1,120,038 | +1,791 | Whites | +17,532 |

SFRM5 | 1,242,825 | 1,224,859 | +17,966 | Reds | -21,429 |

SFRU5 | 966,482 | 972,961 | -6,479 | Greens | -2,634 |

SFRZ5 | 1,074,062 | 1,069,808 | +4,254 | Blues | +154 |

SFRH6 | 656,323 | 659,163 | -2,840 |

|

|

SFRM6 | 696,572 | 703,130 | -6,558 |

|

|

SFRU6 | 663,007 | 662,402 | +605 |

|

|

SFRZ6 | 865,604 | 878,240 | -12,636 |

|

|

SFRH7 | 600,867 | 596,613 | +4,254 |

|

|

SFRM7 | 551,294 | 553,903 | -2,609 |

|

|

SFRU7 | 361,265 | 364,189 | -2,924 |

|

|

SFRZ7 | 403,039 | 404,394 | -1,355 |

|

|

SFRH8 | 252,549 | 254,212 | -1,663 |

|

|

SFRM8 | 181,693 | 180,756 | +937 |

|

|

SFRU8 | 135,946 | 135,743 | +203 |

|

|

SFRZ8 | 149,179 | 148,502 | +677 |

|

|

ECB: MNI ECB Preview - July Hold, September Cut

- With no material developments on the data front since June and various GC members playing up the importance of quarterly projection meetings, the ECB will keep policy rates unchanged this week.

- Although the ECB has previously shown that its data dependence and meeting-by-meeting approach has a degree of inbuilt flexibility (as was the case when steering markets to expect the June cut), there is no need to pre-commit to a September cut at this juncture.

- Given the stickiness of domestic inflationary pressures – namely service prices – we continue to caution that a ‘one-and-done’ is a small, but still significant, risk for 2024.

Full preview, including summary of sell-side views and exclusive MNI policy analysis here: https://roar-assets-auto.rbl.ms/files/65234/ECB%20Preview%20July%202024.pdf

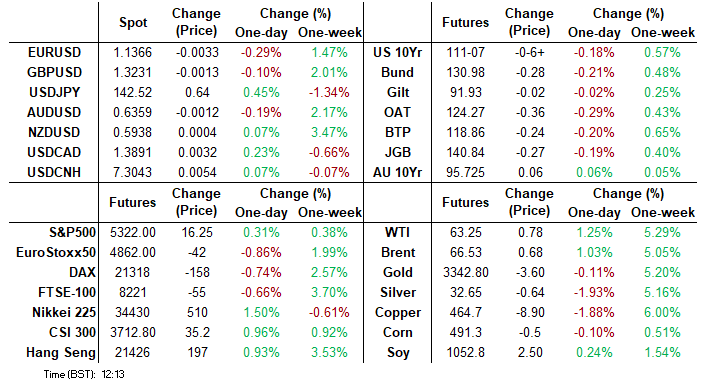

FOREX: USDJPY Recovers from Cycle Lows, DXY Consolidating ~99.50

- The majority of the focus for G10 currency markets on Thursday has been for the Japanese yen following the initial US-Japan trade talks taking place. The weaker greenback trend had prompted USDJPY to fall to a fresh cycle low overnight at 141.62, however positives emanating from these discussions then appeared to provide a boost to USDJPY.

- The pair now stands roughly 100 pips off the lows, having bounced as high as 143.08 in European trade. Furthermore, US equity futures are holding onto their session gains and combined with the higher US yields, appear to have provided a yen headwind on Thursday. Initial resistance for USDJPY is not seen until 144.64 the Apr 11 high.

- Amid the slightly firmer US dollar, the likes of AUD and NZD are struggling to extend their most recent recoveries. AUDUSD has failed on the approach to 0.6400 once more as a lower-than-expected employment change was countered by the unemployment rate coming in a tenth below expectations. Higher than forecast inflation data in New Zealand prompted a moderate bounce for NZDUSD, however so far, prior highs at 0.5944 have capped the upside.

- In similar vein, EURUSD made another attempt above 1.14 but has since subsided to the 1.1375 area. EURUSD vols are generally contained headed into today's ECB decision, where a 25bps rate cut is broadly expected. Key focus remains on 1.1495, the Feb 10 2022 high.

- Despite the moderate uptick on Thursday, the USD index has fallen sharply in recent weeks as a rotation out of US assets seems to be gathering momentum and normal correlations with yields have broken down. Positioning dynamics will be closely monitored as we approach the long holiday weekend.

OPTIONS: Expiries for Apr17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200(E605mln), $1.1215-25(E1.3bln), $1.1250(E849mln), $1.1350-60(E919mln)

- USD/JPY: Y142.80-00($1.1bln), Y145.00($1.4bln)

- USD/CAD: C$1.4000($1.4bln)

- AUD/USD: $0.6390-00(A$921mln)

- USD/CAD: C$1.3950($1.0bln), C$1.4000($2.0bln)

EQUITIES: Eurostoxx Futures Hold Above Recent Lows

- A reversal higher in S&P E-Minis on Apr 9 highlights the start of a corrective cycle. The trend condition has been oversold following recent weakness and the move higher is allowing this set-up to unwind. Initial resistance to watch is 5479.72, the 20-day EMA.

- Eurostoxx 50 futures continue to trade above their recent lows. The latest bounce highlights a corrective cycle and this is allowing an unwinding of the recent oversold trend condition. Resistance levels to watch are 4989.86, the 20-day EMA.

COMMODITIES: WTI Weakness Puts Prices Through Support

- Wednesday’s extension in Gold reinforces current bullish conditions. The yellow metal has traded to another fresh all-time high and confirmed a resumption of the primary uptrend. Note too that moving average studies are unchanged.

- A bearish theme in WTI futures remains intact and the rally on Apr 9 is - for now - considered corrective. The move higher is allowing an oversold trend condition to unwind. Recent weakness has resulted in the breach of a number of important support levels, reinforcing a bearish threat.

| Date | GMT/Local | Impact | Country | Event |

| 17/04/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 17/04/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 17/04/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 17/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/04/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/04/2025 | 1230/0830 | *** | Housing Starts | |

| 17/04/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/04/2025 | 1245/1445 | ECB Monetary Policy press conference | ||

| 17/04/2025 | 1400/1000 | * | US Bill 08 Week Treasury Auction Result | |

| 17/04/2025 | 1400/1000 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/04/2025 | 1530/1130 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 17/04/2025 | 1545/1145 | Fed Governor Michael Barr | ||

| 17/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 18/04/2025 | 2330/0830 | *** | CPI | |

| 18/04/2025 | 1500/1100 | San Francisco Fed's Mary Daly |