ECB: Macro Since Last ECB: Labour - Solid But Wage Growth Easing Still Eyed

Apr-17 11:07

- Labour data since the early March ECB meeting pointed to a solid picture prior to potential tariff impacts.

- The unemployment rate surprisingly pushed a tenth lower to a new series low of 6.1% in February.

- Whilst the rounded data can make it hard to get a sense of the scope of the latest improvement, it came with a solid 70k monthly decline in the seasonally adjusted level of unemployment after a modest 30k decline in January and a rare 49k increase in December at what was its largest increase since Jan 2024.

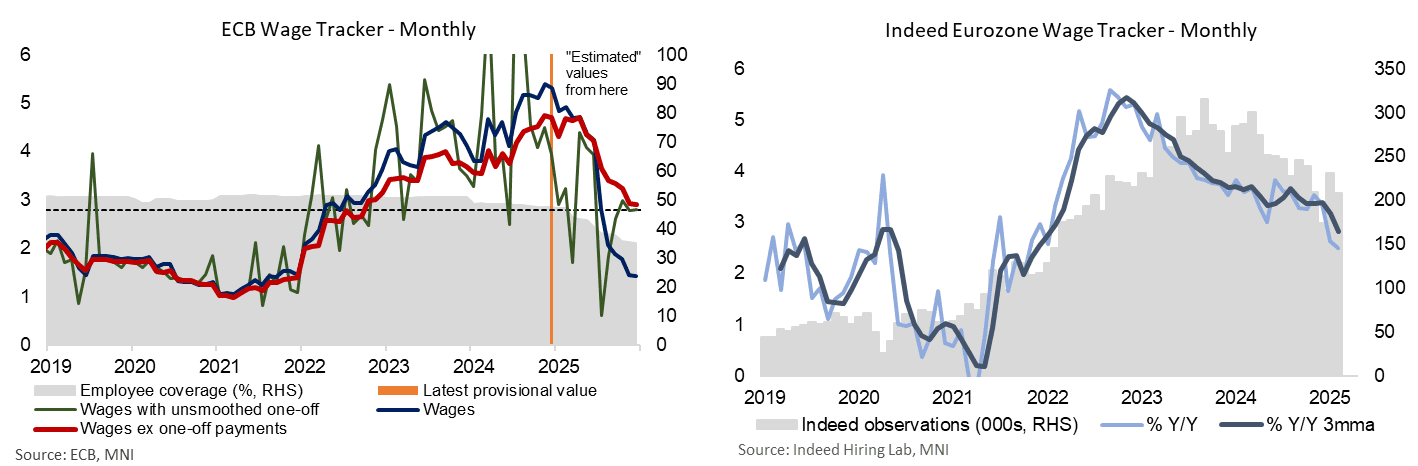

- That said, whilst the unemployment rate may have continued its trend decline, we see the ECB’s latest forward-looking wage tracker as consistent with President Lagarde's rhetoric at the March press conference: "Recent wage negotiations point to a continued moderation in labour cost pressures".

- Negotiated wage growth excluding one-off payments are tracking at 3.02% for 4Q25, a touch above the 2.97% reported in February, but still what would be notable moderation from the 4.66% estimated wage growth for 4Q24.

- The ECB projects compensation per employee growth to ease to 2.8% Y/Y by 4Q25, from 4.1% in 4Q24.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROZONE DATA: Mostly Firmer Vehicle Production But Trend Still Weak

Mar-18 11:06

The Eurozone auto sector generally saw production increase sequentially in January although it remains firmly below pre-pandemic levels as it struggles to keep up with Chinese competitors and emission targets.

- The seasonally adjusted January data from three of the four large Eurozone members showed M/M increases in vehicle production. France and Germany both increased 6.4% M/M and Italy increased 5.1% M/M, although Spain saw its biggest M/M fall since March 2022 (-11.6%).

- These increases do have to be caveated by the volatility in the data. For instance, Germany’s increase followed -10.4% M/M (sharpest since Mar 2022) and France's increase followed -11.1% M/M (sharpest since May 2021).

- The below chart more clearly shows these weak trends, with production levels comfortably below pre-Covid levels.

- This weakness continues to be reflected in car manufacturer decisions, with Audi announcing cutting 7,500 jobs in Germany by the end of 2029 due to "immense challenges" as the auto industry battles slowing demand for electric vehicles and rising competition from China.

- Note, the EU Auto Industrial Action Plan to drive innovation, sustainability, and competitiveness in the automotive sector was unveiled on 5th March. Whilst encouraging it is still very early to determine its effectiveness and on top of this it does not provide flexibility to car manufacturers in the Eurozone wide CO2 emissions 2035 targets (though the EU are considering a review to amend standards to consider performance average over a three-year period to offset shortfalls). Rather, the plan is aimed at supporting the automotive sector to keep pace with technological advancements whilst becoming a 'leader' in sustainable solutions. The plan also emphasised the success of the framework "will be up to Member States to ensure that this framework is efficiently implemented".

BONDS: Natixis Recommend Long U.S. 5y5y Inflation Swap vs. EUR

Mar-18 11:05

Natixis recommend longs in the U.S. 5y5y inflation swap vs. EUR equivalent at 24bp, targeting 39bp, with a stop set at 15bp.

- They highlight the recent “notable inflation repricing between U.S. and EUR inflation swaps, driven by two emerging themes. Germany's infrastructure and defence plan is poised to potentially increase long-term inflation expectations in Europe. Conversely, uncertainty surrounding a possible U.S. recession and tariff fluctuations has clouded the outlook for U.S. markets, leading to a tightening of the U.S.-EUR 5y5y inflation swap spread”.

- Looking ahead, they believe that “the market may be overestimating the impact of the German plan on inflation” (particularly near-term). Meanwhile, in the US, while recession fears have dampened sentiment, they expect a rise in inflation in the next few months that could “bolster U.S. inflation swaps”.

OPTIONS: Expiries for Mar18 NY cut 1000ET (Source DTCC)

Mar-18 11:02

- EUR/USD: $1.0745-55(E2.3bln), $1.0900-10(E678mln)

- USD/JPY: Y147.00($1.3bln), Y148.50($1.4bln), Y149.00($1.2bln), Y150.00($1.5bln)

- AUD/USD: $0.6320-30($1.5bln)

- USD/CNY: Cny7.2900($890mln)

Related bullets

Related by topic

EUR/USD

Bunds

Germany

Euribor

European Central Bank

Schatz

Bobl