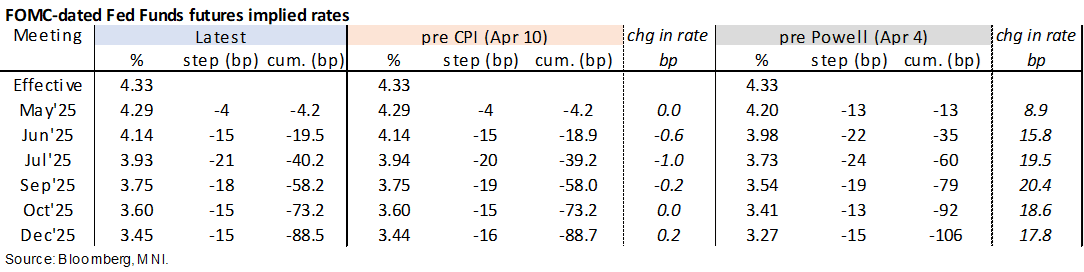

STIR: Fed Rates Back Near Unchanged Since Powell On Trump Termination Threat

Apr-17 10:44

- Fed Funds implied rates for 2025 meetings have been dragged 1-1.5bp lower by President Trump’s truth social post calling for the Fed to cut rates and that “Powell’s termination cannot come fast enough!”.

- Cumulative cuts from 4.33% effective: 4bp May, 19.5bp Jun, 40bp Jul, 58bp Sep and 88.5bp Dec.

- The path is now back near unchanged from just before Powell’s text was released, having closed lower before rising through Asia hours helped by net gains for equity and crude oil futures.

- Recall that by Powell repeating his assessment from less than two weeks ago that the tariffs and their likely effects are "significantly larger than anticipated" it may be construed as a slightly hawkish signal as he doesn't seem swayed by the subsequent April 9th 90-day tariff "pause" or market dislocations in the interim. He followed up in Q&A with "I do think we'll be moving away from" the dual mandate goals “probably for the balance of this year. Or at least not making any progress, and then we'll resume that progress as we can."

- Ahead, Fed Gov. Barr (permanent voter) in a fireside chat at a conference on cyber risk (1145ET, text + Q&A) is unlikely to be a market mover. In the event there is any monetary policy discussion, it will be his first remarks since “Liberation Day” tariffs having said that interest rates and lending standards are still high and tight.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Marginally Twist Steeper, Potential Spillover Factors Watched

Mar-18 10:44

- Treasuries are back to little changed on the day after a modest rolling over in equities, leaving benchmark tenors within +/-1bp of yesterday’s close.

- The Kremlin has said Putin and Trump are due to speak between 0900-1100ET today and we earlier saw Bloomberg report that Putin wants all arms to Ukraine to be halted as part of a ceasefire agreement.

- Today sees a string of second tier US data releases plus potential spillover from Canada CPI at 0830ET and the German Bundestag vote on fiscal reform also expected to start from ~0830ET (with Treasuries currently outperforming EGBs after yesterday's underperformance).

- TYM5 trades at 110-20+ (+ 01) on more limited cumulative volumes of 275k having remained within yesterday’s range throughout.

- Support at 110-12+ (Mar 6/13 low) remains intact whilst the trend condition remains bullish with resistance at 111-25 (Mar 11 high).

- Data: Import prices Feb (0830ET), Housing starts/building permits Feb (0830ET), NY Fed services Mar (0830ET), IP/Cap util Feb (0915ET)

- Coupon issuance: US Tsy $13B 20Y Bond reopen - 912810UJ5 (1300ET)

- Bill issuance: US Tsy $48B 52W & $70B 6W bill auctions (1130ET)

PIPELINE: Corporate Bound Roundup: ADP, ING on Tap

Mar-18 10:43

- Date $MM Issuer (Priced *, Launch #)

- 03/18 $Benchmark ADB 10Y SOFR+57

- 03/18 $Benchmark LG Energy 3Y, 5Y, 10Y

- 03/18 $Benchmark Bangkok Bank 15NC10 +215a

- 03/18 $Benchmark Korea National Oil 3Y +120a, 3Y SOFR, 5Y

- 03/18 $Benchmark ING 4NC3 +110a, 4NC3 SOFR, 6NC5 +125a, 11NC10 +150a

- $11B Priced Monday

US 10YR FUTURE TECHS: (M5) Support Remains Intact

Mar-18 10:38

- RES 4: 113-02 2.0% 10-dma envelope

- RES 3: 112-13 1.500 proj of the Jan 13 - Feb 7 - Feb 12 price swing

- RES 2: 112-01/02 High Mar 4 / 1.382 proj of Jan 13-Feb 7-12 swing

- RES 1: 111-25 High Mar 11

- PRICE: 110-20+ @ 10:27 GMT Mar 18

- SUP 1: 110-14+ 20-day EMA

- SUP 2: 110-12+/00 Low Mar 6 & 13 / High Feb 7 and 50-day EMA

- SUP 3: 109-13+ Low Feb 24

- SUP 4: 108-21 Low Feb 19

The trend condition in Treasury futures is unchanged, a bull cycle remains in play and the current consolidation marks a pause in the uptrend. A bull theme is reinforced by MA studies that are in a bull-mode condition, highlighting a dominant uptrend. Recent gains have resulted in a print above 111-22+, the Dec 3 ‘24 high. A clear breach of this level would open 112-02 and 112-13, Fibonacci projections. Firm support is 110-00, the Feb 7 high.