MNI US MARKETS ANALYSIS - Trump Focus Shifts Back to Shutdown

Highlights:

- Trump's focus shifts back to the domestic economy as shutdown lingers and POTUS considers options

- NZD weakness stands out; RBNZ member flags negative shocks to economy

- MNI Chicago PMI headlines the schedule, with no PCE data due

US TSYS: Modestly Bear Steeper, MNI Chicago PMI Headlines Docket

- Treasuries are a little lower overnight, mostly within yesterday’s range but with 30Y yields pushing to their highest since Oct 10 when US-China trade tensions first re-escalated (still not quite fully reversing the move despite this week’s Trump-Xi meeting).

- With no PCE or ECI releases due to the government shutdown, data focus is squarely on the MNI Chicago PMI. The Chicago CARTS retail sales indicator will also be updated.

- Cash yields are 0-1bp higher on the day, with increases led by the long end.

- The mild steepening bias goes against the underperformance at the very front end of the SOFR strip.

- TYZ5 trades at 112-20+ (-02) on subdued cumulative volumes of 235k, holding within yesterday’s range. Resistance is seen at 113-06 (20-day EMA) but a bear threat is present after a recent pullback, with support seen at 112-16 (yesterday’s low) before 112-14 (Oct 9 low) and 112-06 (Sep 25 low and reversal trigger).

- Data: Chicago CARTS (0830ET), MNI Chicago PMI (0945ET)

- Fedspeak: Logan opening remarks (0930ET), Hammack and Bostic fireside chat at bank funding conference (1200ET) – see STIR bullet

- Politics: Trump departs The White House for Florida (1000ET)

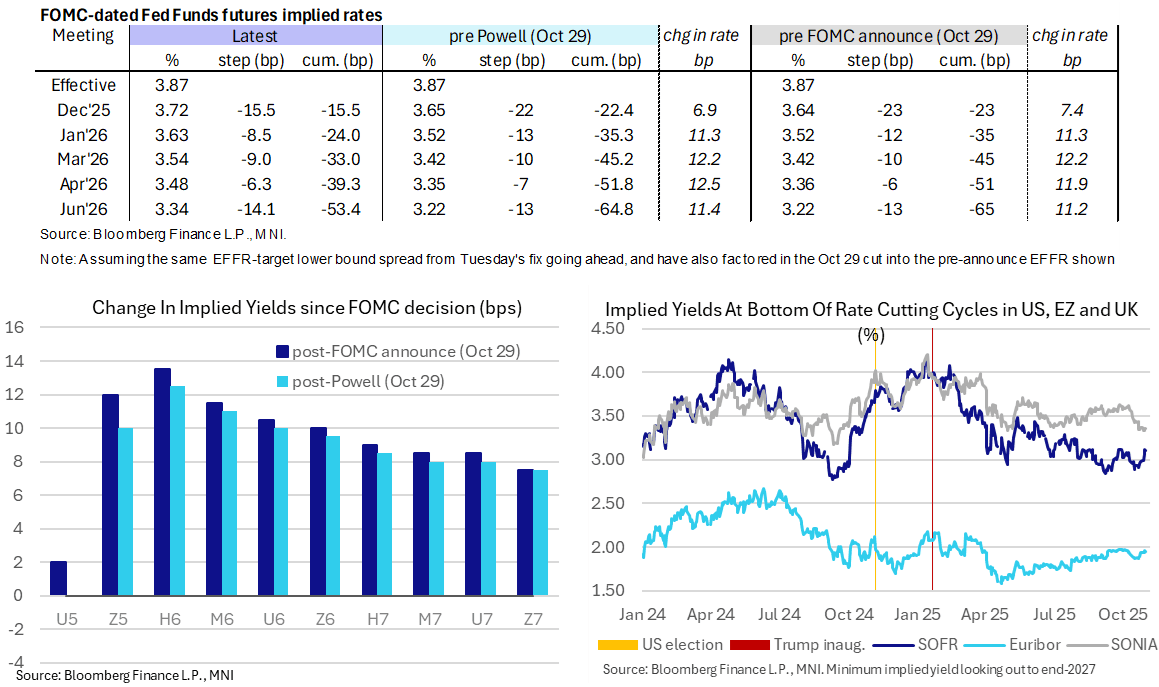

STIR: US Front Rates Underperform, Fedspeak To Resume After Divided FOMC Remarks

- US front rates have seen some modest downward pressure overnight, amongst other things extending uncertainty over a third consecutive cut at the next meeting in December after Powell’s press conference comments.

- Fed Funds implied rates have seen a 1-1.5bp increase for FOMC meetings out to April overnight, with the December implied rate back at Wednesday’s post-Powell high after yesterday’s mild paring.

- Cumulative cuts from an assumed 3.87% effective: 15.5bp Dec, 24bp Jan, 33bp Mar, 39.5bp Apr and 53.5bp Jun.

- SOFR futures have seen volumes concentrated in the SFRZ5, now up to 140k (next largest 83k in the H6) having already been above 100k heading into the European session. It underperforms at -0.02 with the strip more broadly little changed on the day.

- As such, the SOFR terminal implied yield of 3.105% (SFRH7) holds close to yesterday’s highest close since August.

- Fedspeak resumes today with the FOMC blackout now lifted, coming from a Dallas Fed Bank Funding Conference. We don’t expect many market moving headlines but will nevertheless monitor any comments regarding recent funding market pressures as well as those on the economic outlook or broader monetary policy after Powell indicated a strongly divided FOMC on December cut prospects.

- 0930ET – Logan (’26 voter) opening remarks (text only)

- 1200ET – Hammack (’26 voter) and Bostic (non-voter) in fireside chat (text tbd)

US: Trump: GOP Should Invoke Nuclear Option To Bypass Filibuster And Reopen Govt

In a statement on Truth Social, President Donald Trump has called on Senate Republicans to invoke the so-called 'nuclear option' to end the 60-vote filibuster to pass legislation to reopen the federal government.

- Such a move would require a simple majority vote in the Senate. A Democratic attempt to bypass the filibuster in 2022 to pass voting rights legislation failed due to opposition from centrist Democratic Senators Joe Manchin and Kyrsten Sinema. Senate Majority Leader John Thune (R-SD) may encounter the same problem from institutionalist Republicans who fear handing too much power to a future Democratic government.

- Axios reported earlier this week, “Sen. John Kennedy (R-LA) urged Vice President Vance during a closed-door lunch Tuesday to get President Trump to stop demanding that the Senate do away with the filibuster.”

- Indeed, three symbolic votes this week on Trump’s tariff agenda have revealed an anti-Trump majority which could reject a move to terminate the filibuster. Senators Rand Paul (R-KY), Susan Collins (R-ME), Lisa Murkowski (R-AK), and Mitch McConnell (R-KY) joined with Democrats to block tariffs. See TARIFFS: Senate Passes Symbolic Resolution Terminating Trump's Global Tariffs

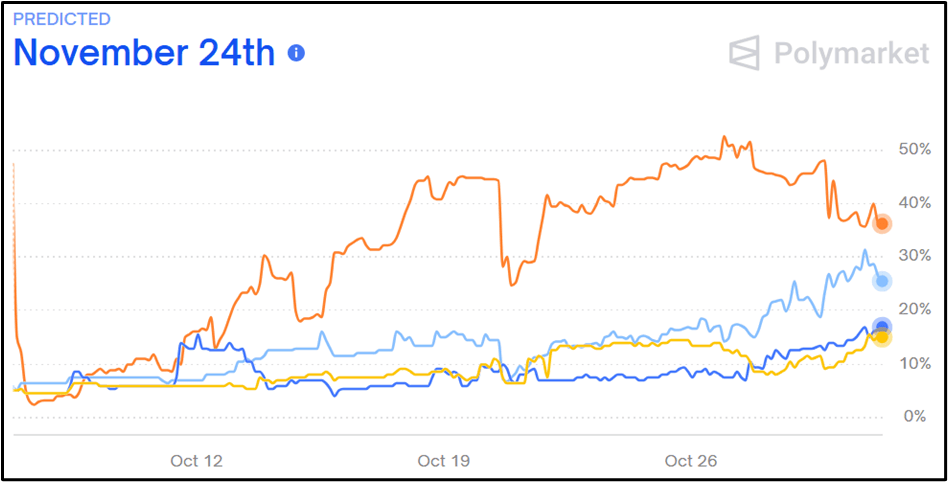

- Trump’s statement has done little to move the dial on prediction markets, but, with Trump back from Asia and 40 million Americans set to lose SNAP benefits from November 1, a resolution may come together quickly in the coming weeks, as noted by MNI's Political Risk team yesterday: US: Johnson Downplays Senate Talks On Shutdown, Trump's Move Next Week Critical

Figure 1: When will the Government Shutdown End?

Source: Polymarket

UK: Chancellor Survives Letting Revelations, Keeping Budget On Track

Chancellor of the Exchequer Rachel Reeves will remain in place after a chaotic day on 30 Oct, during which revelations surrounding the letting of her house in south London briefly threatened to force her from office just weeks ahead of a critical Budget statement on 26 Nov. On 29 Oct, the Daily Mail reported that Reeves had not obtained the correct licence to let her family home after she moved to the Chancellor's residence at 11 Downing St. following the 2024 general election.

- In an initial exchange of letters with PM Sir Keir Starmer, Reeves acknowledged her error, while Starmer said he accepted her version of events and that the independent Advisor on Ministerial Standards, Sir Laurie Magnus, had decided not to investigate further. Amid mounting political pressure during the day, emails came to light seemingly putting the blame on the letting agency, rather than Reeves or her husband.

- In a late-night exchange of letters, Reeves apologised for an "inadvertent mistake", while Starmer said it was "regrettable" that Reeves did not release the emails initially, but that he saw "no need for any further action".

- A greater challenge to Reeves' position may come post-budget, with growing expectations that Labour's manifesto promises on income tax/VAT/national insurance will be broken. This risks a major public backlash, and Reeves may end up as the senior minister forced out if pressure from the public or Labour backbenches becomes too much for Starmer.

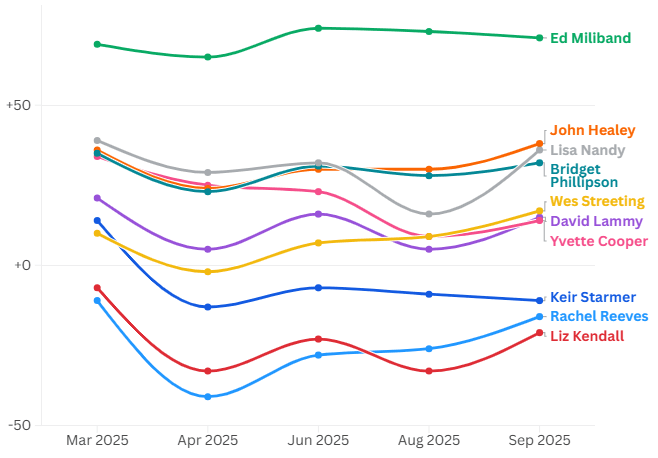

- Polling of grassroots Labour members shows Reeves as one of the least popular Cabinet ministers, alongside the PM himself (see chart below).

Chart 1. Net Approval Ratings for Senior Cabinet Ministers, %

Source: Survation, LabourList. Base: All respondents. Unweighted total: 1,254 Full question: Do you have a favourable or unfavourable opinion of the following?

FOREX: Kiwi Pressured by Overnight Comments, AUDNZD Approaches Cycle Highs

- Intraday weakness for NZD stands out on Friday, in a more subdued session overall for G10 FX. The Kiwi was pressured by comments from RBNZ committee member Prassanna Gai, who said that global shocks appear to have offset some of the monetary easing that has taken place since August 2024.

- Gai stated that “For a small open economy like New Zealand, the US tariffs have acted as a negative demand shock. Compounding this has been a much broader uncertainty shock as the weaponization of trade and finance have profoundly changed widely accepted norms and international rules of the game.”

- Combined with the renewed strength for the dollar following the Fed, the comments have allowed NZDUSD to extend lower, maintaining the bearish tone for the pair in recent months.

- NZDUSD trades within 40 pips of cycle lows, located at 0.5683. A move below here would turn the focus to 0.5636, the 76.4% retracement of the year’s range. 2025 lows are located at 0.5486.

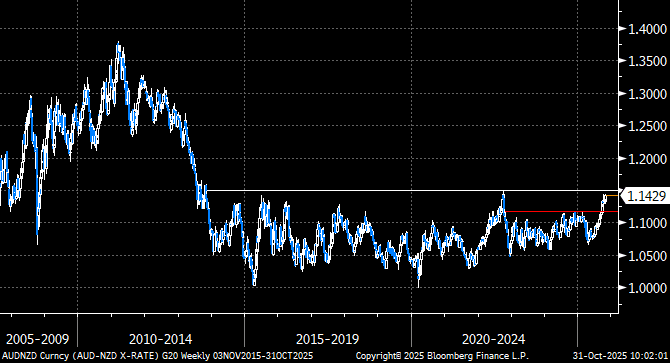

- It’s also worth noting that AUDNZD (weekly chart below), a cross that has garnered much attention, traded within 4 pips of cycle highs earlier today. It appears that solid demand was found beneath 1.13 and the rally could be set to extend towards the 2022 highs at 1.1491. A break of this level would place the cross at its highest point since 2013. Both the RBA and NZ employment are scheduled next week.

FOREX: NZD Under Pressure Friday, JPY and GBP Consolidating Moves Lower

- USDJPY stands just 20 pips below yesterday's 154.45 highs, recovering from an overnight pullback driven by firmer than expected Tokyo CPI and Japan Industrial Production data. Bullish conditions remain intact following the pair's impressive 4.7% gains since new PM Takaichi's LDP leadership win, a theme that extended sharply following the BOJ on Thursday. Commentary on recent exchange rate moves was in line with previous rhetoric, however, further upward pressure on USDJPY may raise concern amongst BoJ officials.

- Clearance of yesterday's highs in USDJPY would refocus attention on 154.80, the Feb 12 high. Pullbacks would be considered technically corrective at this juncture, with first important support much lower at 151.60, the 20-day EMA.

- GBPUSD remains in a position of weakness as Powell's relatively hawkish remarks during Wednesday's FOMC press conference and UK fiscal developments continue to significantly weigh on the pair. UK Chancellor Reeves' situation appears stable for now after her having to backpay some rental license fees, however, GBPUSD continues to test the key breakout level below 1.3142, multiple daily lows on the chart. A weekly close would strengthen the bearish bias, with attention turning to 1.3041, the Apr 14 low.

- Intraday weakness for NZD stands out on Friday, pressured by comments from RBNZ committee member Prassanna Gai, who said that global shocks appear to have offset some of the monetary easing that has taken place since August 2024. NZDUSD trades within 40 pips of cycle lows, located at 0.5683. AUDNZD has also made three-week highs, hovering just below 1.1450.

- Eurozone HICP is scheduled for release soon after national-level data implied slight upside risks for the print. Canadian GDP and the MNI Chicago PMI will follow later. Fed’s Logan and Hammack are on the speaker schedule.

FOREX: Adding to Month-End Models

- We noted earlier that Barclays FX rebalancing model indicates weak USD sales against all other majors.

- Credit Agricole's month-end models point to real-money sales of USD, and corporate selling of both EUR and GBP. Their strongest USD sell signal is against AUD.

- SEB's porfolio rebalancing model sees a need to buy SEK, most pronounced in SEK/JPY.

EQUITIES: Earnings Season Concludes; Reports Seen Supportive of Headline Indices

- The trend structure in Eurostoxx 50 futures remains bullish. This week’s fresh cycle highs reinforces a bull theme and the move higher maintains the rising price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on 5777.41, a Fibonacci projection. First support lies at 5646.82, the 20-day EMA.

- The trend condition in S&P E-Minis remains bullish and the latest pullback appears corrective. The fresh cycle high this week confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on 6974.04 next, a Fibonacci projection point. Initial firm support to watch lies at 6748.48, the 20-day EMA. Key pivot support lies at 6783.25, the 50-day EMA.

COMMODITIES: Gold Off Lows, But Downcycle Intact

- Recent gains in WTI futures appear corrective for now, however, note that price has recently traded through the 50-day EMA, currently at $61.05. The breach of this EMA signals scope for a stronger recovery. A resistance at $62.34, the Oct 8 high, has also been pierced. A clear break of it would expose key resistance at $65.77, the Sep 26 high. First key support and the bear trigger is unchanged at $55.96, the Oct 20 low.

- A fresh cycle low this week in Gold highlights an extension of the bear cycle that started Oct 20. The retracement this month has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3853.2. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

| Date | GMT/Local | Impact | Country | Event |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/10/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1330/0930 | Dallas Fed's Lorie Logan | ||

| 31/10/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/10/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 31/10/2025 | 1600/1200 | Fed's Beth Hammack, Raphael Bostic | ||

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |