MNI US MARKETS ANALYSIS - Treasuries Firmer on Muted Volumes

Highlights:

- Treasuries firmer into Thursday open, muted overall volumes

- ECB's Rehn raises prospect of larger ECB rate cuts, but little evidence he's changed his view

- Gold stabilising after weakness off highs

US TSYS: Firmer Amidst Low Volumes, Multiple Focal Points For Today's Session

- Treasuries appear to have been supported overnight by a softer risk environment with China refuting there have been US-China consultations or negotiations on tariffs, rather than the selling pressure seen on risk-off of recent weeks.

- Today sees wide-ranging focus, with data including jobless claims and durable goods, potential headlines from a Bessent-Kato meeting after the G20 FinMin meeting press conference scheduled for 1210-1240ET and a 7Y auction.

- Yesterday’s 5Y auction saw a decent 1bp stop through but foreign demand looked weaker with a sharp pull back for indirect take up (from 76% to 64%).

- Cleveland Fed’s Hammack (’26 voter) said yesterday that slowing the pace of balance sheet runoff will allow QT to continue for longer, approaching “the ‘just-above-ample’ point carefully”.

- Cash yields are 2-4.5bp lower on the day, with declines led by the belly.

- TYM5 sits at 110-28 (+07) on particularly low volumes of 235k, within yesterday’s wide range of 110-18+ to 111-18+.

- Yesterday’s 111-18+ sets latest initial resistance for another step towards a notable 111-25 (50% retrace of Apr 7-11 bear leg). The subsequent reversal however lends support to the technical view that gains are corrective, with support seen at 110-15 (Apr 15 low).

- Data: Durable goods Mar prelim (0830ET), Weekly jobless claims (0830ET), Chicago Fed national index Mar (0830ET), Existing home sales Mar (1000ET), Kansas Fed mfg Apr (1100ET)

- Fedspeak: Kashkari (’26) – see STIR bullet

- Coupon issuance: US Tsy $44B 7Y Note auction - 91282CNA5 (1300ET)

- Bill issuance: US Tsy $85B 4W & $75B 8W bill auctions (1130ET)

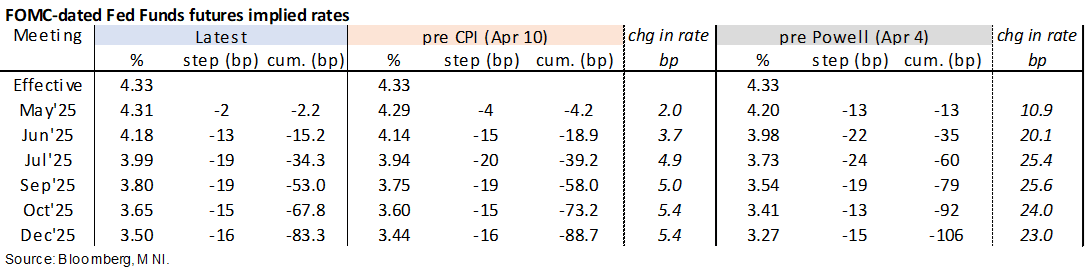

STIR: Fed Rates Softer But Still Only 15bp Of Cuts Priced With June FOMC

- Fed Funds implied rates are 0-4bp lower for 2025 meetings overnight, with early downward pressure from a softer risk environment as China denied there has been US consultations and negotiations on tariffs.

- Nearer-term meetings are still towards the more hawkish end of the past two months.

- Cumulative cuts from 4.33% effective: 2bp May, 15bp Jun, 34bp Jul and 83bp Dec.

- Today sees some data focus on durable goods orders for March and weekly jobless claims.

- Attention then turns to potential headlines following a Bessent-Kato meeting after the G20 Finance Ministers meeting. The post G20 meeting presser is scheduled to take place 1210-1240ET.

- Fedspeak is much more limited today, with just Kashkari (’26 voter) scheduled for a moderated discussion at 1700ET (no text). He said Apr 22 that independence has been “foundational” to the US economy’s success in recent decades amidst pressure to cut rates from President Trump, although also said that tariffs are at least somewhat inflationary in slightly less robust language than Apr 11 when he said tariffs suggest inflation will be going back up again and prefers focusing on the Fed’s inflation goal first. Still, those Apr 22 comments reiterated that the Fed must ensure tariff inflation isn’t persistent.

- Hammack (’26 voter) yesterday reiterated that “This is not a good time to be preemptive. This is a good time to sit and wait and watch” when it comes to adjusting rates.

- There are two days left before the FOMC media blackout kicks in.

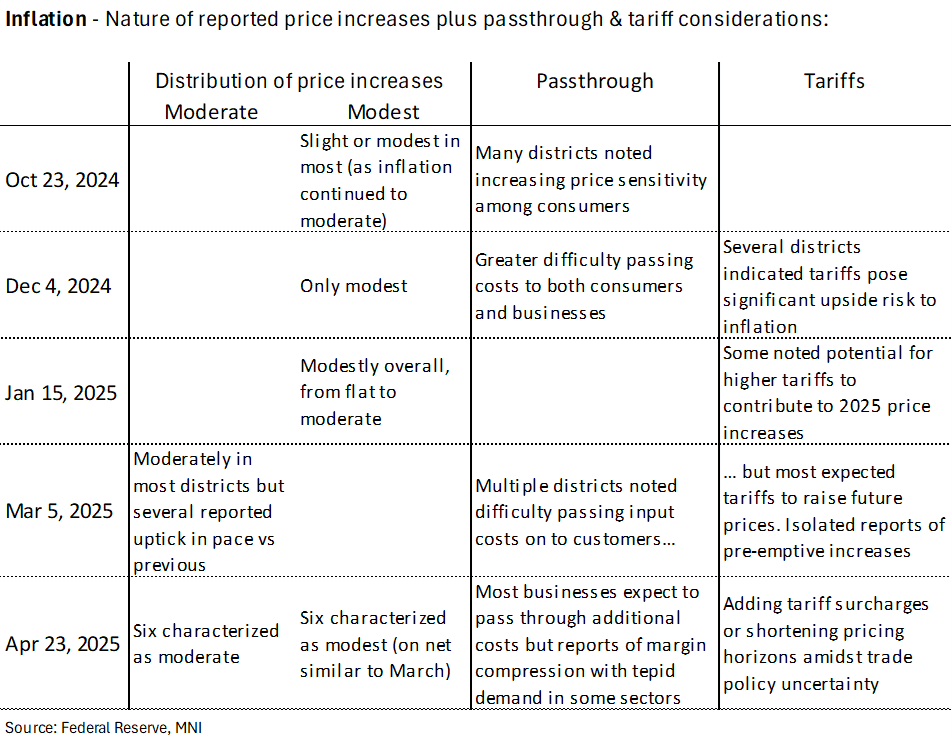

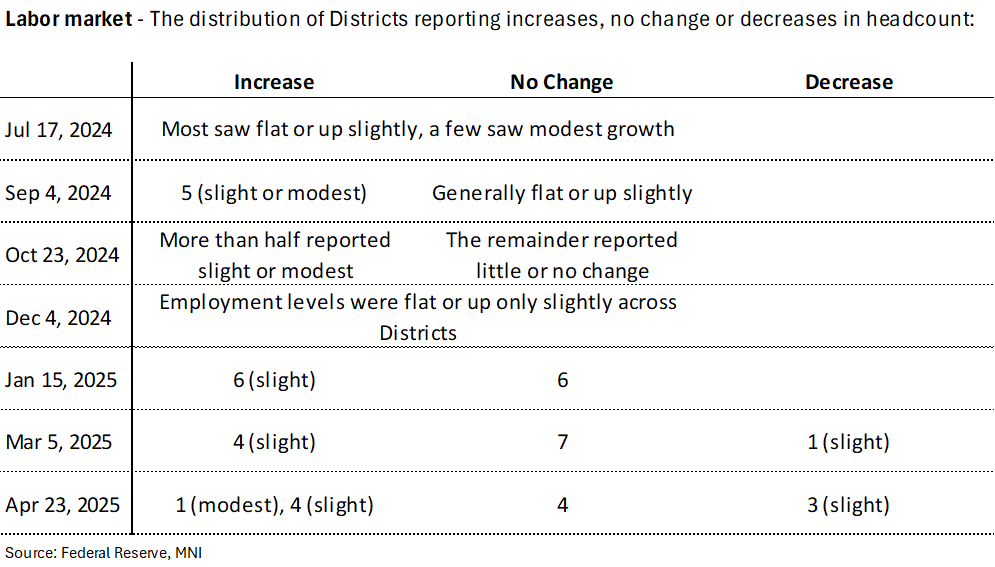

FED: Beige Book: Similar Price Increases To Six Weeks Ago, Weaker Employment

- We wrote on yesterday’s Beige Book in detail at the time but for those not around, the below tables offer a succinct summary of trend changes in inflation and labor conditions vs past reports.

- In short, price increases were explicitly acknowledged as similar to those with the March report six weeks ago, consolidating a firming compared to previous editions. On pricing behavior: "Most businesses expected to pass through additional costs to customers. However, there were reports about margin compression amid increased costs, as demand remained tepid in some sectors, especially for consumer-facing firms. "

- Employment saw a “slight deterioration” from March as it continues a trend of steady declines. More districts than not reported job growth but it’s starting to become more balanced. Unsurprisingly, “The most notable declines in headcount were in government roles or roles at organizations receiving government funding.”

ECB: Unclear How Much Rehn Has Actually Changed His View

While the headlines from Rehn around the scope for a "larger" ECB rate cut screen dovish, it’s unclear just how much of a change in tone it actually is.

- Firstly. there is still firm conditionality around a 50bp cut: “Whether a larger, 50-basis point cut may be considered, “depends on the inflation outlook in the medium term and how much worse or better the growth outlook will be,” Rehn said.”

- Furthermore, he already said that the ECB is to “maintain complete freedom of action” on Apr 2 (the morning ahead of Liberation Day tariff announcements) and Apr 9. On April 9, he added that “grounds for continuing rate cuts in the April meeting have grown clearly stronger based on a holistic assessment of inflation and economic growth”.

- Those comments of course came ahead of the ECB decision on Apr 17 with its unanimous support for a 25bp cut. Lagarde at the presser: “The decision to cut today was unanimous. Options were debated but there was no one to argue in favour of a 50bp cut, for instance. 25bp was definitely the rate cut on which all in the room agreed.”

- It’s hard to know what might have changed his view to an extent that would actually see a vote for a 50bp cut since then. On the data front, yesterday’s flash Eurozone service PMI admittedly missed expectations at 49.7 (cons 50.5) after 51.0 in March but stronger than expected manufacturing helped limit the decline in the composite from 50.9 to 50.1 (cons 50.2).

- Finally, acknowledgement that there are few good arguments to pause rate cuts already chimes with market pricing, which had been showing closer to 22bp priced for the June ECB decision prior to his comments (now nearer 24bp). That's followed by what had been a cumulative 36.5bp of cuts priced for July (now nearer 39bp).

US TSY FUTURES: Mix Of Short Setting & Short Cover Seen Wednesday

OI data points to a mix of net short setting (TU, FV & TY) and short cover (US & WN) during yesterday’s twist flattening of the curve.

- The net short setting in the front end/intermediates comfortably outweighed the net short cover further out the strip.

| 23-Apr-25 | 22-Apr-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,117,569 | 4,088,844 | +28,725 | +1,073,029 |

FV | 6,742,365 | 6,659,951 | +82,414 | +3,549,223 |

TY | 4,735,281 | 4,723,198 | +12,083 | +768,982 |

UXY | 2,249,506 | 2,246,047 | +3,459 | +304,479 |

US | 1,797,016 | 1,804,518 | -7,502 | -952,639 |

WN | 1,875,849 | 1,879,111 | -3,262 | -601,010 |

|

| Total | +115,917 | +4,142,064 |

STIR: Short Setting & Long Cover Dominated On SOFR Futures Strip On Wednesday

OI data points to a mix of net short setting and long cover across much of the SOFR futures strip on Wednesday, with the only exception coming via modest net short cover in SFRH5.

- The most meaningful net positioning swing seemed to come via net long cover in SFRZ6.

| 23-Apr-25 | 22-Apr-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,109,144 | 1,113,665 | -4,521 | Whites | -2,776 |

SFRM5 | 1,229,318 | 1,209,937 | +19,381 | Reds | -14,495 |

SFRU5 | 959,067 | 959,908 | -841 | Greens | -8,710 |

SFRZ5 | 1,062,654 | 1,079,449 | -16,795 | Blues | +9,260 |

SFRH6 | 688,970 | 682,850 | +6,120 |

|

|

SFRM6 | 693,340 | 686,896 | +6,444 |

|

|

SFRU6 | 674,355 | 664,602 | +9,753 |

|

|

SFRZ6 | 828,281 | 865,093 | -36,812 |

|

|

SFRH7 | 608,173 | 607,350 | +823 |

|

|

SFRM7 | 547,483 | 549,376 | -1,893 |

|

|

SFRU7 | 368,656 | 368,428 | +228 |

|

|

SFRZ7 | 386,533 | 394,401 | -7,868 |

|

|

SFRH8 | 259,381 | 254,362 | +5,019 |

|

|

SFRM8 | 181,504 | 180,939 | +565 |

|

|

SFRU8 | 136,713 | 135,061 | +1,652 |

|

|

SFRZ8 | 154,526 | 152,502 | +2,024 |

|

|

FOREX: Greenback Edges Lower as China Dismisses Talks Progress

- Risk sentiment is trading on a softer footing Thursday amid headlines from China dismissing any progress on trade talks with the US. The messaging goes against the most recent optimism surrounding potential de-escalation of the tariff war, and have placed the US dollar under pressure through the European morning. Greenback losses have been broad based in the G10 space, with the dollar only higher against CNH.

- These dynamics have boosted EURUSD by 0.55% with 1.13 providing solid support so far and the move down from Monday’s cycle high considered corrective. Moving average studies are in a bull-mode position which continues to signal a continued dominant uptrend. Most recent comments from ECB’s Rehn highlighting “there are few good arguments” to pause rate cuts lean dovish but have had little effect on the Euro. 1.1573/1.1181 remain the short-term technical parameters of note.

- Despite the upticks for both AUDUSD (+0.35%) and NZDUSD (+0.56%), the pairs remain notably below the 0.6400 and 0.6000 marks respectively. For AUDUSD specifically, the inability to consolidate gains above key resistance at 0.6409 is significant, and evident of the how fragile the pair remains to the broader risk backdrop.

- USDCHF highs of 0.8311 overnight fell around 20 pips shy of the prior breakdown point at 0.8333, the 2023 low. With bearish conditions prevailing, spot has reverted back towards 0.8260. We noted yesterday that Danske have updated their 12-month forecast for USDCHF to 0.7500. It is worth noting that EURCHF has edged back above 0.9400 as the cross edges further away from key medium-term support in the low 0.92s.

- US jobless claims, durable goods and existing home sales data highlight the economic calendar today. ECB’s Nagel will speak at 1300BST, and ECB’s Lane participates in a panel. Fed’s Kashkari is also scheduled.

USD: Analyst Expectations Appear Tilted Towards Further Greenback Weakness

While we have seen a resumption of dollar weakness today, the USD index remains ~1.5% off Monday lows. Short-term positioning dynamics will have likely assisted the bounce, however, analysts remain open to the idea that the greenback weakness could have room to extend:

- Deutsche Bank believe the pre-conditions are now in place for the beginning of a major dollar downtrend. Their forecasts foresee the end of a "higher for longer" dollar with EUR/USD appreciating closer to purchasing power parity of 1.30 over the remainder of the decade.

- They highlight three key aspects; a reduced desire by the rest of the world to fund growing twin deficits in the US; by extension, a peak and gradual unwind in elevated US asset holdings ; and a greater willingness to deploy domestic fiscal space to support growth and consumption outside of the US.

- Goldman Sachs' Chief Economist Hatzius has published an opinion piece in the FT this morning arguing that "reluctance by non-US investors to add to their US portfolios" will weigh on USD going forward amid GS seeing the US "unlikely" to outperform during the next couple of years - this led him to conclude that Dollar weakness "has considerably further to go."

- BBVA see that "market reactions suggest short USD positioning is crowded, which could amplify the profit-taking seen yesterday. Markets will continue to be driven by Trump headlines, but a prolongation of the short-term reversal in the USD index towards the 102/103 resistance area looks like an opportunity to short the index again."

- Danske take a similar view, seeing "In the near term, concerns about US asset confidence and a recession will support [EURUSD]. Longer term, structural challenges like US political shifts, the trade war, and capital rotation away from US assets suggest significant USD downside."

- ING think "Trump needs to keep feeding markets with positive news to fuel further dollar gains from here".

OPTIONS: Expiries for Apr24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1370(E505mln)

- USD/JPY: Y140.00($1.8bln), Y145.00($1.4bln)

EQUITIES: Wednesday's Gains for Eurostoxx Futures Highlight a Corrective Cycle

- Eurostoxx 50 futures have recovered from Tuesday’s low. Recent gains highlight a corrective cycle and the rally marks an unwinding of a recent oversold trend condition. The 20-day EMA has been cleared. The next key resistance to watch is 5102.45, the 50-day EMA. Key support and the bear trigger has been defined at 4444.00, the Apr 7 low. A break of this level would confirm a resumption of the downtrend.

- The bull cycle in S&P E-Minis that started on Apr 7 is considered corrective. The trend condition has been oversold following recent weakness and gains have allowed this to unwind. Price has traded above the 20-day EMA, at 5423.30. This exposes 5528.75, the Apr 10 high. Note that resistance at the 50-day EMA - a key level too - is at 5630.01. For bears, a resumption of weakness would refocus attention on 4832.00, the Apr 7 low and bear trigger.

COMMODITIES: Recent Move Lower for Gold Allowing Overbought Trend to Unwind

- A bearish theme in WTI futures remains intact and the recovery since Apr 9 is - for now - considered corrective. The move higher is allowing an oversold trend condition to unwind. Recent weakness has resulted in the breach of a number of important support levels, reinforcing a bearish threat. A resumption of the bear cycle would open $53.72, a Fibonacci projection. Resistance to watch is 65.96, the 50-day EMA.

- The trend needle in Gold continues to point north and this week’s fresh cycle high reinforces bullish conditions. The latest move down appears corrective and is allowing an overbought trend condition to unwind. Moving average studies are unchanged, they remain in a bull-mode position highlighting a dominant uptrend. The next objective is $3547.9, a Fibonacci projection. Initial firm support to watch lies at 3194.1, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 24/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/04/2025 | 1230/0830 | * | Payroll employment | |

| 24/04/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 24/04/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/04/2025 | 1300/1500 | ECB's Lane at Peterson Institute Webcast on Monetary Policy Strategy | ||

| 24/04/2025 | 1325/1425 | BOE's Lombardelli on Monetary Policy Strategy | ||

| 24/04/2025 | 1400/1000 | *** | NAR existing home sales | |

| 24/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 24/04/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 24/04/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 24/04/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 24/04/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 24/04/2025 | 2100/1700 | Minneapolis Fed's Neel Kashkari | ||

| 25/04/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 25/04/2025 | 2330/0830 | ** | Tokyo CPI | |

| 25/04/2025 | 0600/0700 | *** | Retail Sales | |

| 25/04/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 25/04/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 25/04/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/04/2025 | 1915/2015 | BOE's Greene on Inflation, growth and moentary policy | ||

| 25/04/2025 | 2000/1600 | Kevin Warsh |