FED: Beige Book: Similar Price Increases To Six Weeks Ago, Weaker Employment

Apr-24 09:28

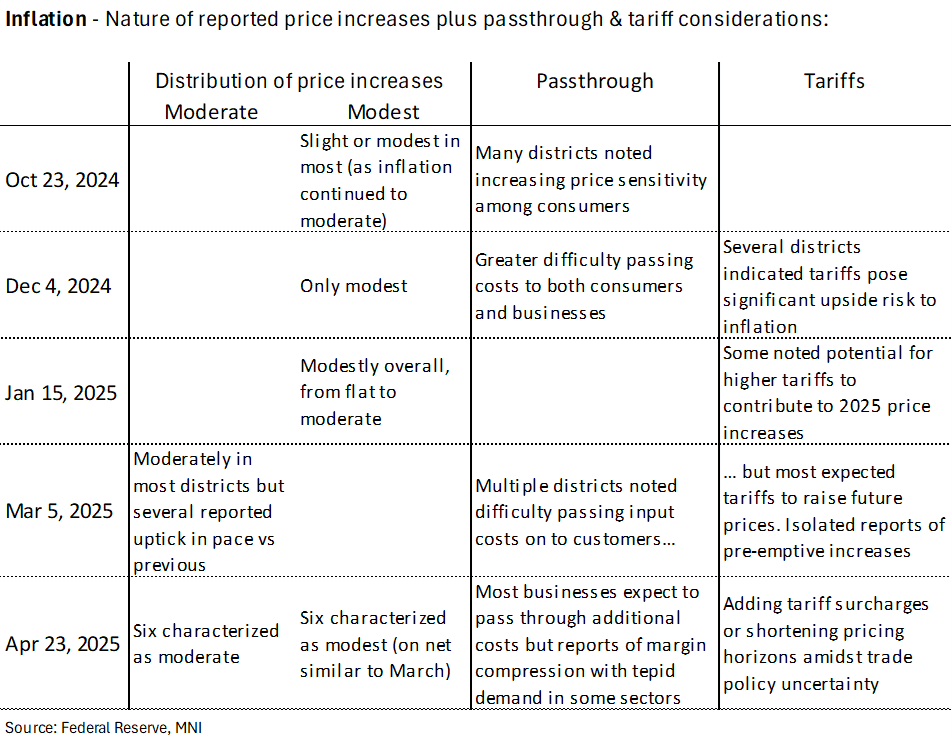

- We wrote on yesterday’s Beige Book in detail at the time but for those not around, the below tables offer a succinct summary of trend changes in inflation and labor conditions vs past reports.

- In short, price increases were explicitly acknowledged as similar to those with the March report six weeks ago, consolidating a firming compared to previous editions. On pricing behavior: "Most businesses expected to pass through additional costs to customers. However, there were reports about margin compression amid increased costs, as demand remained tepid in some sectors, especially for consumer-facing firms. "

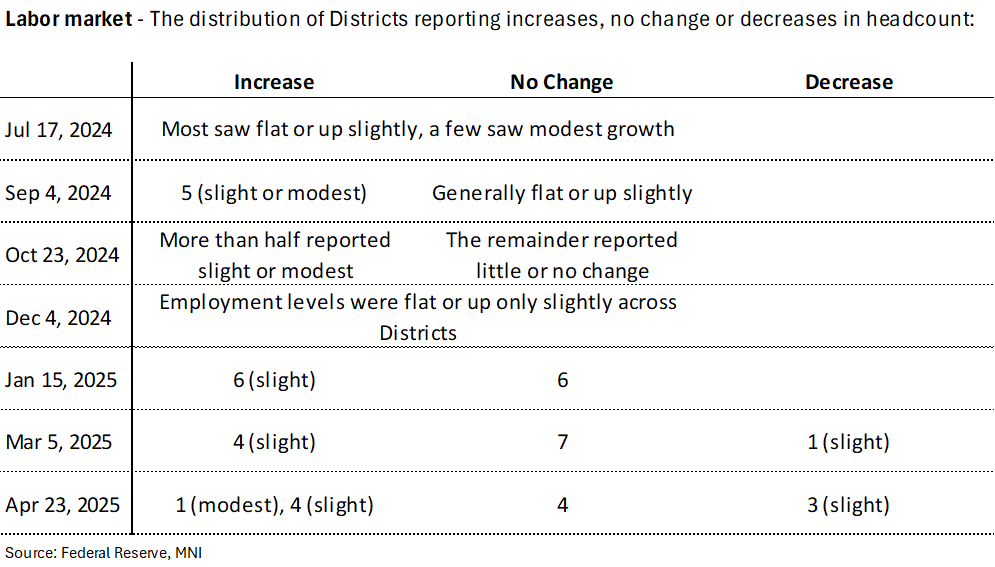

- Employment saw a “slight deterioration” from March as it continues a trend of steady declines. More districts than not reported job growth but it’s starting to become more balanced. Unsurprisingly, “The most notable declines in headcount were in government roles or roles at organizations receiving government funding.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SWEDEN: ESV Revises 2025 Deficit Projection Lower

Mar-25 09:26

The Swedish budget watchdog, ESV, now expect the Swedish 2025 budget deficit at 0.8% GDP. That’s down from a 1.7% deficit forecast in the November projection round. The deficit is expected to shrink further to 0.3% GDP in 2026, as the economy recovers.

- The press release notes that total spending is growing at a slower rate than incomes, and that “the municipal sector accounts for the largest strengthening as a result of lower pension costs”.

- Also from the release: “Both the recession and various tax cuts are contributing to a slow increase in tax revenues this year. At the same time, expenditures are increasing relatively rapidly in the state. This is due to large increases in spending in defense, the justice system and communications.”

- The ESV’s 2025 GDP forecast was revised up a tenth to 2.2%, while growth is seen accelerating to 2.8% in 2026. The Riksbank March MPR projections 2025 growth at 2.1% and 2026 growth at 2.2%.

BUNDS: Some momentum selling is going through

Mar-25 09:21

- Some momentum selling in Bund as it breaks through the figure, sold in 7k, likely some short term long bailing out.

- The contract has been selling off since the Cash Open, initially led by the US Treasuries, but the German supply (Bobl), EU Issuance as well as the German IFO beat have also weighted on the on the contract.

- Supports are unchanged, at 127.88, followed by 127.45, so far printed a 127.89 low.

GERMAN AUCTION PREVIEW: 2.40% Apr-30 Bobl

Mar-25 09:20

This morning, Germany will hold its fourth regular (non-green) Bobl auction of the year. On offer will be E4.5bln of the 2.40% Apr-30 Bobl.

- The size is in line with the E4.5bln seen at the last re-open of that Bobl on March 4.

- That last re-open was a rather weak auction, with the lowest bid-to-cover since June 2023 (1.69x) and the lowest bid-to-offer (1.32x) since April 2023 in the Bobl segment. At least the low price came in above the secondary markets mid-price at that auction. Note that March 4 was the day that later saw the major German fiscal announcement.

- Earlier auctions in the German Bobl segment have passed smoothly, with solid bid-to-covers (in a 1.73x to 2.75x range since January 2024), bid-to-offers (1.45x to 2.29x range since then) and the low prices above the secondary market mid-prices throughout 2024.

- Supply is in focus generally this morning, with a syndication from France and auctions from the Netherlands and the UK.

- Bobl positioning currently appears short - see our latest Europe Pi positioning indicator (published yesterday) here.

- The next German auction will be next tomorrow's E1.5bln of the 2.60% May-41 Bund (ISIN: DE000BU2F009) and E500mln of the 2.50% Aug-46 Bund (ISIN: DE0001102341), while the 2.40% Apr-30 Bobl will be reopened next on April 15.

- Timing: Results will be available shortly after the bidding window closes at 10:30GMT / 11:30CET.

Trending Top

Jan-30 21:43

Jan-30 21:11