MNI US MARKETS ANALYSIS - Takaichi in Tough Position

Highlights:

- Shutdown extends, but markets look to likely inflation print by month-end

- Japan's Takaichi in tough position as Komeito look to reassess coalition

- Musalem speech watched carefully for hawkish undertones

US TSYS: Bull Flatter With U.Mich And Musalem Headlining Docket

- Treasuries are firmer across the curve, mostly in line with EGBs and also aided by light spillover from JGB futures after the Komeito party withdrew from its coalition with the LDP. A further pullback in crude oil futures could also be factoring in.

- The Washington Post reports that behind the scenes, Trump and his aides have still not engaged with Democrats at all on the government shutdown.

- Today could see outsized focus on the preliminary U.Mich consumer survey for October amidst a dearth of data as the government shutdown continues. It should be viewed in light of the political split that appear to have been exaggerated this year.

- Cash yields are 1.5bp (2s) to 3.5bps (20s) lower on the day.

- The bull flattening sees 5s30s at 98bps for the flattest since Sep 30, with 30s unperturbed by yesterday's somewhat softer auction (tailed by 0.5bp with a steady bid-to-cover at 2.38x but indirect take up from 62.0% to 64.5%).

- TYZ5 at 112-22+ (+07) has slowly climbed back towards yesterday’s overnight highs, on another overnight session with modest volumes currently around 230k.

- It’s a little further above support at 112-14 (50-day EMA) after a short-lived clearance earlier this week but doesn’t yet trouble resistance at 113-00 (Sep 24 high).

- Data: U.Mich consumer survey Oct prelim (1000ET)

- Fedspeak: Goolsbee opening remarks (0945ET), Musalem on economy and mon pol (1300ET)

- Politics: Trump makes an announcement (1700ET)

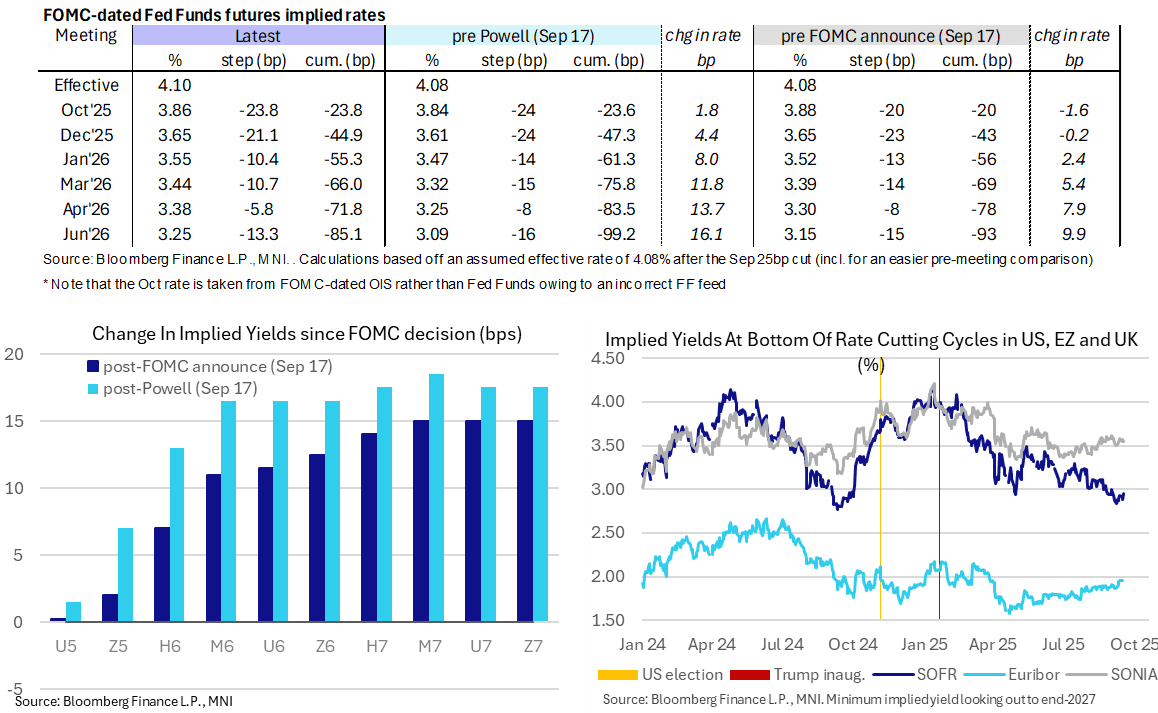

STIR: Fed Rate Path Mildly Lower, A Hawkish Musalem To Headline Fedspeak

- Fed Funds implied rates have ebbed lower overnight, with moves helped by a further decline in crude oil futures.

- Moves are limited for meetings out to mid-2026 (0.5bp lower) but a little larger thereafter.

- Cumulative cuts from 4.10% effective: 24bp Oct, 45bp Dec, 55.5bp Jan, 66bp Mar, 72bp Apr and 85bp Jun.

- SOFR futures trade between unchanged and 2.5 ticks firmer looking out to end-2027.

- The SOFR implied terminal yield of 3.07% (SFRZ6) is 1.5bp lower, implying a little over 100bp of cuts ahead when crudely based off the recent uptick in the effective fed funds rate to 4.10%.

- It’s a thinner docket for Fedspeak today, with our focus on St Louis Fed’s Musalem, one of the most hawkish members of the FOMC. We view him as one of the six dots from last month’s SEP looking for no further cuts this year after the 25bp cut in September.

- 0945ET – Goolsbee (’25 voter) opening remarks at Chicago community banker’s symposium (no Q&A)

- 1300ET – Musalem (’25 voter) in fireside chat on economy and mon pol (no text). He noted on Sep 29 that the labor market continues to soften but that it’s still near full employment. The Fed needs to tread cautiously whilst rates are between modestly restrictive and neutral.

- Fedspeak should take on much greater importance next week when Powell speaks on the economic outlook and monetary policy at a NABE event on Tuesday.

SOFR: Mix Of Positioning Swings In Futures On Thursday

OI data points to a mix of net long (SFRU5 & Z5) and short (SFRM6) setting in the whites, before short setting and long cover came to the fore further out as the SOFR futures strip twist steepened on Thursday.

| 09-Oct-25 | 08-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,429,471 | 1,415,421 | +14,050 | Whites | +66,735 |

SFRZ5 | 1,540,477 | 1,506,309 | +34,168 | Reds | -24,731 |

SFRH6 | 1,195,366 | 1,181,271 | +14,095 | Greens | +5,981 |

SFRM6 | 1,021,489 | 1,017,067 | +4,422 | Blues | +2,806 |

SFRU6 | 990,392 | 990,170 | +222 |

|

|

SFRZ6 | 1,005,118 | 1,023,285 | -18,167 |

|

|

SFRH7 | 791,541 | 796,283 | -4,742 |

|

|

SFRM7 | 786,712 | 788,756 | -2,044 |

|

|

SFRU7 | 678,380 | 674,063 | +4,317 |

|

|

SFRZ7 | 761,890 | 758,382 | +3,508 |

|

|

SFRH8 | 433,215 | 430,609 | +2,606 |

|

|

SFRM8 | 366,135 | 370,585 | -4,450 |

|

|

SFRU8 | 298,322 | 298,373 | -51 |

|

|

SFRZ8 | 330,184 | 327,879 | +2,305 |

|

|

SFRH9 | 191,741 | 191,816 | -75 |

|

|

SFRM9 | 169,548 | 168,921 | +627 |

|

|

US TSY FUTURES: Short Setting & Long Cover Offset On Thursday

OI data points to a mix of net long cover (TU, UXY & WN) and short setting (FV, TY & US) as Tsy futures ticked lower on Thursday.

- There wasn’t much in the way of movement in curve-wide DV01 terms as the two essentially offset.

- The largest DV01 positioning swings came via the net short setting in TY futures and net long cover in WN futures.

| 09-Oct-25 | 08-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,588,705 | 4,605,317 | -16,612 | -648,170 |

FV | 6,760,232 | 6,755,350 | +4,882 | +212,771 |

TY | 5,389,202 | 5,354,836 | +34,366 | +2,318,588 |

UXY | 2,457,926 | 2,461,831 | -3,905 | -352,723 |

US | 1,907,615 | 1,898,674 | +8,941 | +1,145,705 |

WN | 2,044,883 | 2,058,139 | -13,256 | -2,488,510 |

|

| Total | +14,416 | +187,661 |

JAPAN: Komeito Withdrawal From Gov't Puts LDP's Takaichi In Perilous Position

Leader of the centrist social conservative Komeito party, Tetsuo Saito, announced that his party wishes to 'reset' the governing coalition with the conservative Liberal Democratic Party (LDP) and that its lawmakers would not vote for the new LDP president, Sanae Takaichi, to become PM in a confirmatory vote expected in the National Diet on 20 October.

- The PM is confirmed in a two-round system. If no single nominee receives an overall majority, then the top two candidates hold a run-off . If the two chambers elect different candidates, a joint committee is formed to try to reach agreement. If there is no agreement, or the upper House of Councillors does not submit a nomination within 10 days, the lower House of Representatives' candidate is elected as PM.

- Takaichi has said to reporters that she would like to hold talks again next week, but whether Komeito accept remains to be seen. The two most likely scenarios would now appear to be:

- Takaichi reaches out to the opposition libertarian federalist Japan Innovation Party (Ishin) or conservative populist Democratic Party for the People (DPFP) to gain their backing. The DPFP have called for a blanket cut in sales tax to 5% that would be paid for via debt issuance, unspent gov't discretionary funds and any surplus from special accounts, as well as an increased tax threshold. Ishin have called for the elimination of sales tax on food for two years and the nomination of a 'second capital' in case Tokyo is damaged by natural disaster (likely Ishin's stronghold, Osaka).

- Ishin, DPFP and the main opposition liberal Constitutional Democratic Party (CDP) unite around a single candidate. There has been some speculation that Ishin and the CDP could unite behind DPFP leader Yuichiro Tamaki, but he said to reporters such a gov't could only work if there was ideological coherence.

FRANCE: Macron Calls Meeting Of Party Leaders @14:30CET Ahead Of PM Announcement

President Emmanuel Macron is convening a meeting of leaders of numerous political parties, excluding the far-left La France Insoumise and far-right Rassemblement National, at the Elysee Palace 14:30CET (08:30ET, 13:30BST). The Elysee says the meeting "must be a moment of collective responsibility". Macron is expected to announce his nominee to succeed Sebastien Lecornu as prime minister after the latter's resignation earlier in the week.

- Despite intense media speculation in recent days, it remains no clearer whether Macron will look to appoint a candidate from the existing centre/centre-right minority gov't, one from the centre-left, a technocratic head of gov't, or even reappoint Lecornu.

- Three of the four groups forming the leftist New Popular Front alliance, the centre-left Socialist Party (PS), environmentalist Ecologists (EELV), and left-wing Communists (PCF), have been meeting since 12:00CET. As with the Elysee meeting, the LFI has been excluded. The three parties have been pushing for Macron to appoint a PM from the left.

- Should Macron pursue this path, it would risk alienating the conservatives and centre-right parties that have backed the gov't previously. It would also limit the prospect of any fiscal consolidation in the 2026 budget, risking blowback from the EU given France's position within the Excessive Deficit Procedure.

- Earlier this morning Governor of the Banque de France, Francois Villeroy de Galhau, ruled out taking on the PM's position. Speaking to RTL, he claimed, "I was asked the question, but everyone has their mission to serve their country; mine is at the Bank of France."

ISRAEL: Netanyahu To Deliver Statement Shortly w/Ceasefire Holding

Reuters reports that PM Benjamin Netanyahu is set to deliver a statement to the media at 13:00 local time (06:00ET, 11:00BST). The PM's address comes a short time after a spox for the Israeli Defence Forces confirmed that "the ceasefire agreement went into effect as of 12:00 [local time]....As of 12:00, IDF forces have positioned themselves in the latest deployment lines, in accordance with the outline of the ceasefire agreement and the return of the kidnapped. IDF forces in the Southern Command are deployed in the area and will continue to operate to eliminate any immediate threat." The withdrawal to the 'yellow line' outlined in the ceasefire agreement still sees the IDF in control of around ~60% of the Gaza Strip.

- Following the signing off on the ceasefire deal at a cabinet meeting overnight, the clock has been ticking on a 72-hour period for Hamas to release all hostages, living and dead. This marks the first potential obstacle to the sustainability of the deal. If and when this process is concluded, alongside the release of nearly two thousand Palestinian prisoners held by Israel, it could bolster the lower geopolitical risk premium recognised within the Middle East since the ceasefire came into force.

- The actions of Houthi rebels in Yemen will also be closely watched. While the Iranian-backed proxy group welcomed the news of a ceasefire, Israel's Ynet noted on 9 Oct that the group has warned that any apparent backtracking on the agreement will result in a resumption of attacks on Israel and shipping in the Red Sea.

GBP: Spot Weakness Adds to Evidence of Fading GBP Resilience

GBP/USD returning lower in recent trade, with spot slipping through mild intraday support at 1.3280 with relatively little difficulty. GBP is now among the poorest performers in G10 - adding to the evidence that GBP resilience earlier this week has begun to fade.

- GBP/JPY is reversing hard: price is near 1.5% off the week's highs and through 202.67 support. Signs of a coalition breakdown in Japan (Komeito demanding concessions to reassess the long-lasting coalition) remain JPY positive - lessening the chances of Takaichi forming a dominant pro-easing force in parliament. Should Takaichi's negotiations with other opposition parties fail to succeed - she may face a difficult time in office proceeding with her preferred policy set.

- While JPY is the dominant leg in the cross, GBP/USD's close below the support zone of 1.3324-40 yesterday is a bearish sign - despite very few signs in BoE speeches this week that influential MPC members are considering more easing this year.

- We noted yesterday that moves in the GBP 1y1y chart are relatively contained, despite the hawkish shift, signalling a stickiness in terminal rates pricing that could signal GBP upside is limited despite the phase-out of rate cut pricing this year.

- This makes 1.3142 the broader downside GBP/USD target, however markets generally remain of the view that EURGBP upside is an easier expression of GBP weakness into year-end.

FOREX: Two-Way JPY Vol As Japan's Komeito Want to 'Reset' Coalition

- The USD is lower headed into the Friday crossover for the first time this week, aiding a shallow recovery off lows for both EUR/USD and GBP/USD. The greenback fade means the USD Index has retraced ~10% of the month-to-date rally, exposing 99.067 as first major intraday support - the 23.6% retracement of the bounce.

- Japanese politics remains a key focus for markets. JPY (briefly) rallied following headlines that Japan's Komeito Party wish to 'reset' the governing coalition following talks with Takaichi, stating that they cannot support her premiership without alignment.

- The initial JPY strength came on an unwind of expectations on the Takaichi trade (pro-fiscal, monetary easing), who may now face an uphill struggle to be confirmed as PM in a 20 Oct parliamentary session, let alone enact her expansionary policy agenda. The situation is evolving, with higher political risk premia having the potential to work against the JPY as other coalition options are investigated.

- From a technical perspective, bullish trend conditions in USDJPY remain intact, and sights are on 154.39, a Fibonacci retracement point. Initial support to watch lies at 150.92, the Aug 1 high.

- NOK underperforms following this morning’s lower than expected Norwegian inflation data. While the release was dovish on net, Norges Bank may need to see more evidence of declining underlying price pressures before deviating from its cautious stance, particularly with mainland demand still relatively resilient. SEK meanwhile is the strongest in G10 as August Swedish GDP rose much more than expected, supporting analyst, Riksbank and Government expectations for a cyclical recovery in activity going forward. The Riksbank is likely to remain at 1.75% for the foreseeable future, with the risk of a hike back to 2.00% outweighing the risk of another cut - an outlook which today's release supports.

- The combination of these data led NOKSEK 0.45% lower on the day at 0.9430. The cross remains on a sideways trend, with support located at 0.9399, the October 6 low, and key resistance seen around 0.9500.

- Canadian jobs data and the prelim October UMich sentiment release are the market focus Friday. Consensus looks for Canada to have added 5k jobs over September, while seeing consumer sentiment fade in the US.

OPTIONS: Expiries for Oct10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E1.1bln), $1.1500-20(E2.5bln), $1.1570-75(E780mln), $1.1600(E1.9bln), $1.1625-30(E1.1bln), $1.1650(E1.9bln), $1.1670-75(E695mln), $1.1700(E1.9bln), $1.1720-25(E907mln), $1.1740-50(E2.5bln), $1.1780-00(E2.8bln)

- USD/JPY: Y152.30-50($951mln)

- GBP/USD: $1.3400(Gbp942mln), $1.3470(Gbp638mln)

- AUD/USD: $0.6545(A$658mln)

- USD/CNY: Cny7.1034($600mln)

EQUITIES: Eurostoxx 50 Futures Consolidate Close to Recent Highs

- The trend condition in Eurostoxx 50 futures is unchanged, the direction remains up and the recent consolidation appears to be a flag formation - a bullish continuation pattern. The recent breach of key resistance at 5525.00, the Aug 22 high, confirmed a resumption of the uptrend. Sights are on the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Initial firm support lies at 5550.36, the 20-day EMA.

- The trend condition in S&P E-Minis is unchanged and the direction remains up. Fresh cycle highs this week confirm a continuation of the uptrend and maintain the positive price sequence of higher highs and higher lows. The contract is holding on to its latest gains and sights are on 6812.29 and 6819.25, Fibonacci projection points. Initial support to watch is at the 20-day EMA, at 6716.75. A clear break of it would signal scope for a pullback.

COMMODITIES: Next Target for Gold at $4074.54, a Fibonacci Projection

- A bearish theme in WTI futures remains intact and short-term gains are considered corrective. Recent weakness resulted in a move through key support and a bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens the bear threat and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance is at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal.

- A bull cycle in Gold remains in play and this week’s breach of the $4000 handle reinforces the uptrend. The move higher maintains the price sequence of higher highs and higher lows. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. For now, sights are on $4074.54, a Fibonacci projection. Support to watch is $3817.5, 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 10/10/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 10/10/2025 | 1230/0830 | *** | Labour Force Survey | |

| 10/10/2025 | 1230/0830 | *** | Labour Force Survey | |

| 10/10/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 10/10/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 10/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/10/2025 | 1700/1300 | St Louis Fed's Alberto Musalem | ||

| 10/10/2025 | 1800/1400 | ** | Treasury Budget |