US TSYS: Bull Flatter With U.Mich And Musalem Headlining Docket

Oct-10 10:59

- Treasuries are firmer across the curve, mostly in line with EGBs and also aided by light spillover from JGB futures after the Komeito party withdrew from its coalition with the LDP. A further pullback in crude oil futures could also be factoring in.

- The Washington Post reports that behind the scenes, Trump and his aides have still not engaged with Democrats at all on the government shutdown.

- Today could see outsized focus on the preliminary U.Mich consumer survey for October amidst a dearth of data as the government shutdown continues. It should be viewed in light of the political split that appear to have been exaggerated this year.

- Cash yields are 1.5bp (2s) to 3.5bps (20s) lower on the day.

- The bull flattening sees 5s30s at 98bps for the flattest since Sep 30, with 30s unperturbed by yesterday's somewhat softer auction (tailed by 0.5bp with a steady bid-to-cover at 2.38x but indirect take up from 62.0% to 64.5%).

- TYZ5 at 112-22+ (+07) has slowly climbed back towards yesterday’s overnight highs, on another overnight session with modest volumes currently around 230k.

- It’s a little further above support at 112-14 (50-day EMA) after a short-lived clearance earlier this week but doesn’t yet trouble resistance at 113-00 (Sep 24 high).

- Data: U.Mich consumer survey Oct prelim (1000ET)

- Fedspeak: Goolsbee opening remarks (0945ET), Musalem on economy and mon pol (1300ET)

- Politics: Trump makes an announcement (1700ET)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: Analysts' EUR STIR Views Ahead Of Thursday’s Decision (2/2)

Sep-10 10:56

Summarising some select EUR STIR views ahead of Thursday’s decision:

- Bank of America maintain their “received Oct ECB €str recommendation (Entry 1.765, target 1.565, current 1.905)". Even though they "see little chance of a rate cut by October given the lack of data between the two meetings, given only 2 bp are priced, we view the trade at this stage as a tail risk hedge”

- RBC believe that if the ECB will remain on hold going forward, it “makes sense to take short volatility positions on near-term Euribor options, for example being short straddles”. They note that “these positions are short gamma and short vega and hold positive carry since the term structure of Euribor option volatility is still upward sloping”.

- Morgan Stanley “find it unlikely that the ECB meeting will result in a hawkish enough outcome to further challenge the easing currently priced in”. They think that “short-dated rates have room to reprice lower” and “continue to favour Oct-Dec flattening given the low implied probability of a 25bp cut for December”.

- Santander instead believe “the risk bias across the EUR curve remains tilted to the upside, though it may take until later in the year for materially higher rates to materialise. Paying fixed in the front end still makes sense, but it will likely take several weeks before the trade pays off clearly.”

- MNI's full ECB preview is here.

US TSYS: Modestly Twist Steeper With PPI, Geopol and 10Y Supply In Focus

Sep-10 10:55

- Treasuries sit modestly twist steeper around the US crossover, with the front end paring yesterday’s decent-sized losses considering headline/data flow at the time.

- The long end sees little sign of haven flow following Poland triggering Article 4 after numerous drones violated its airspace. A press conference with E5 defense ministers is due at 0900ET today.

- Away from geopol, today’s scheduled focus will be on PPI inflation at 0830ET before the 10Y auction at 1300ET after last month’s poorly received offering.

- Cash yields range from 1.5bp lower (2s) to 1.2bp higher (30s).

- The moves do little to dent recent flattening away from multi-year steeps in 5s30s, at 113.5bp vs recent highs of 126.bps.

- TYZ5 trades at 113-08+ (-02+) in what have been relatively narrow ranges on thin cumulative volumes only just hitting 200k.

- A bullish theme remains in play with resistance seen at 113-21+ (Sep 5 high, post-NFPs) before 113-26+ (Fibo proj). An overnight low of 113-06 didn’t trouble support at 112-28+ (Sep 5 low).

- Data: MBA mortgage applications, PPI Aug (0830ET), Wholesale trade sales/inventories Jul/Jul F (1000ET)

- Coupon issuance: US Tsy $39B 10Y Note auction re-open - 91282CNT4 (1300ET). Last month’s 10Y auction tailed by 1bp along with a sizeable decline in the bid-to-cover from 2.61 to 2.35.

- Bill issuance: US Tsy $65B 17W bill auction (1130ET)

- Politics: No publicly scheduled events for Trump, with an intelligence briefing at 1130ET and a dinner at 1900ET.

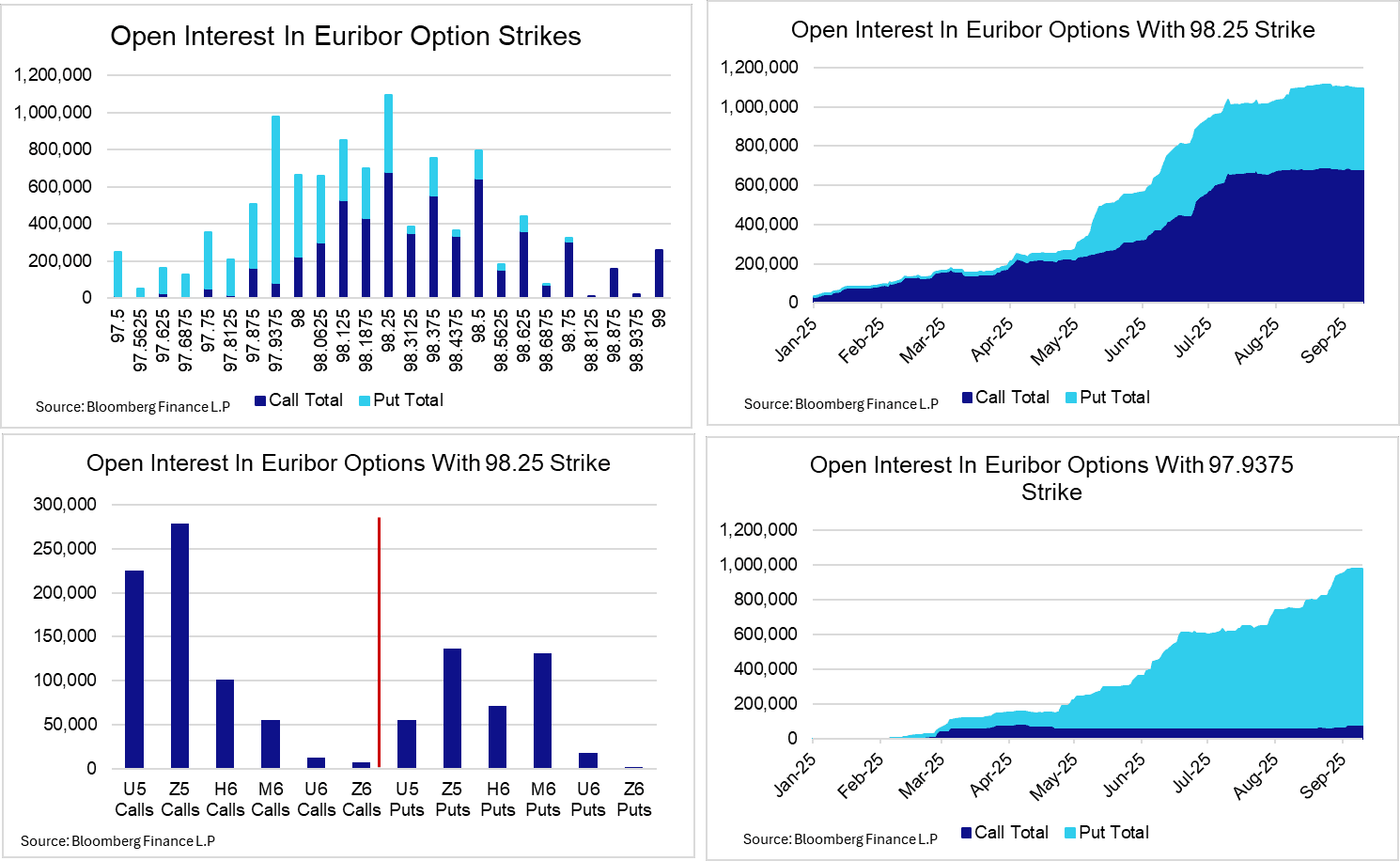

ECB: EUR STIR Options Flow More Balanced As Terminal Approaches (1/2)

Sep-10 10:55

With the ECB now at or close to its assumed terminal rate, recent EUR STIR options flow has been much more balanced than earlier this year (where it was dominated by demand for dovish call structures).

- A divergence in participants’ views likely reflect differing opinions on (i) the underlying strength of Eurozone domestic demand and the impact of past rate cuts, (ii) the eventual economic impact of a higher US effective tariff rate and (iii) the eventual impulse from higher German fiscal spending.

- Thursday’s communication and updated projections will provide an update on how the ECB currently assesses these drivers, and will be key in shaping any market reaction on the day.

- Popular dovish plays in recent weeks have included significant purchases of the ERM6 98.3125/98.4375 call spread, alongside other upside call structures in Z5 and H6. On a shorter-term basis, today’s flow has included a buyer of the ERU5 98.00/98.06 call spread. These options expire on Sep 15th, so essentially capture tomorrow’s ECB decision in isolation.

- However, there has also been demand for more hawkish put spreads and flies expiring through the course of next year during the past few weeks.

- Looking at options in ERU5, ERZ5, ERH6, ERM6, ERU6 and ERZ6, the 98.25 strike currently has the highest open interest, followed by the 97.9375 strike. While 98.25 strike OI is fairly evenly split between calls (60%) and puts (40%), 97.9375 is dominated by puts (90%). We note that put sales have been used to fund dovish call structures through this year, but recent increases in OI have also reflected increased demand for the hawkish put structures noted above.