MNI US MARKETS ANALYSIS - Stocks Up, USD Down on Shutdown News

Highlights:

- Pro-growth impulse follows shutdown progress news, favouring stocks and working against Treasuries & USD

- Senate progress over the weekend could smooth passage to full reopening by Friday

- Supply in focus, with 3y, 10y and 30y sales starting today

US TSYS: Lower On Shutdown Hopes, Front-Loaded Supply Headlines Docket

- Treasuries have pared losses but still sit comfortably lower on the day in response to improved odds of the government shutdown ending after eight centrist Democrats on Sunday voted with Republicans on a new CR to fund the US government through Jan 30.

- Today’s docket focus should be on front-loaded supply ahead of Veterans Day tomorrow, with a 3Y auction along with heavy bill issuance.

- Cash yields are 2.4-3.3bp higher on the day, with increases slightly led by the belly possibly ahead of that 3Y supply.

- TYZ5 trades at 112-20 (-07+) off an earlier low of 112-15 on reasonable overnight volumes nearing 340k.

- Resistance is seen at Friday’s joint high of 113-02 (Nov 5 & 7 highs, a key level), but a bear threat is still present at 112-06 (Sep 25 low) before which lies 112-09+ (Nov 5 high) and other various support levels.

- Data: No releases of note.

- Fedspeak: Daly on Bloomberg TV (0830ET), Musalem on Bloomberg TV (0945ET)

- Coupon issuance: US $58B 3Y Note Auction - 91282CPK1 (1300ET). Last month’s 3Y auction stopped through by 0.8bp although saw both the bid to cover and indirect take receded.

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET) and $95B 6W bill (1300ET)

- Politics: Trump in bilateral meeting with President of Syria (1100ET), Trump participates in swearing-in ceremony for Ambassador to Republic of India (1500ET)

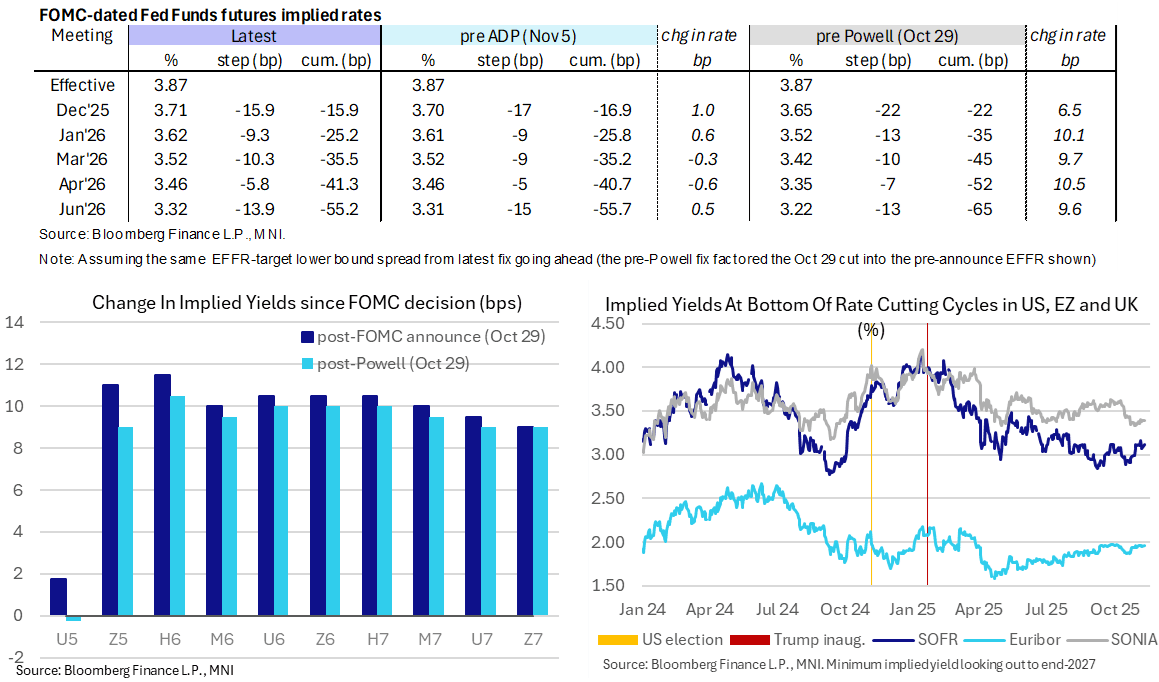

STIR: Fed Rate Path Buoyed By Improved Shutdown Ending Odds

- Fed Funds implied rates are a modest 0.5-1.5bp higher for meetings out to mid-2026, helped by a marked improvement in odds of the government shutdown ending.

- Cumulative cuts from 3.87% effective: 16bp Dec, 25bp Jan, 35.5bp Mar, 41.5bp Apr, 55bp Jun.

- SOFR futures see larger moves, up to 4.5 ticks lower through 2027 contracts.

- It sees the terminal yield higher at 3.12% (H7) but still off Wednesday’s 3.16% marked the highest close since late July, following beats for ADP and ISM services before weaker alternate labor data and consumer sentiment over Thu-Fri.

- We don’t expect today’s Fedspeak to move the needle having heard from both recently.

- 0830ET - SF Fed’s Daly (non-voter, leaning dove) on Bloomberg TV. She’s spoken a few times since the Oct 29 FOMC, including in a blog post this morning firming her dovish leaning stance.

- 0945ET - St Louis Fed’s Musalem (’25 voter, hawk) on Bloomberg TV. He said on Nov 6 that policy is getting close to neutral and that the Fed needs to lean against above-target inflation. The labor market is around full employment but there are some downside risks to it.

FED: Likely Experiencing A Negative Demand Shock - Daly

SF Fed’s Daly has published an essay (link) on the likely negative demand shock hitting the economy and the need for a balanced approach to policy setting. Her remarks support her dovish leaning stance, having last week said she completely supported the October 25bp cut and wants to keep an open mind about cutting again in December (although she doesn’t have a voting role in either 2025 or 2026).

- The bottom line of analyzing wage developments: “We are likely experiencing a negative demand shock. Demand for workers has fallen —it just happened to be met with a nearly coincident decline in the labor supply.”

- “[U]nlike what many projected, trade rebalancing has not led to more broad-based and persistent inflation dynamics.6 Indeed, so far, the effects of the tariffs have largely been confined to goods, with little spillover into services inflation or inflation expectations, which remain relatively well-anchored around our target.”

- Concerning a wide range of productivity growth “We don’t want to work so hard to not be the 1970s that we cut off the possibility of the 1990s, losing jobs and growth in the process. That would be trading one mistake for another.”

- “The FOMC had vigorous debates about whether to react strongly to low unemployment and signs of rising inflation or take signal from emerging hints of a secular shift in productivity growth and the labor market. In the end, they took a balanced approach to policy, and we ended up with the roaring 90s and contained inflation.”

- “Getting policy right will require an open mind and digging for evidence on both sides of the debate. Clarity is there. You just have to look for it, regardless of where it leads.”

- She repeats that monetary policy is “modestly” restrictive.

UK: Changes in UK market drivers post-Nov MPC (1/2)

As we wrote in our BOE Review (see full PDF here), we think that if labour and inflation data comes in line with the Bank’s updated near-term projections and the Budget is broadly in line with expectations (with some disinflationary measures and an income tax increase) we think it would be likely that Governor Bailey would support a December rate cut. We also think that the views of the other 8 MPC members are more entrenched than we had previously expected (despite the 5-4 vote in line with our base case). This has three main implications for UK market drivers in the coming weeks:

- 1) Speeches from Governor Bailey will have huge focus on them – particularly after the first round of labour and inflation data. He hasn’t made clear if he will only vote a cut if data comes in softer than the Bank’s projections or if it is in line with those projections. We look at this in more detail in the BOE review but the takeaway is that it will be harder for the data to undershoot expectations: private regular wage Q3 expectations are 0.4ppt below the Bank’s August projections; services CPI is expected to not see any bounceback in October and to continue to decelerate at a faster pace than the August MPR projections. The only category of CPI that appears to not have a high bar to see data coming in below the November projections is the “food and non-alcoholic beverages” category. The problem is that Governor Bailey currently has no speeches scheduled.

UK: Changes in UK market drivers post-Nov MPC (2/2)

- 2) Governor Bailey (and the other dovish MPC members in general) are not as concerned about the upside inflationary risks as they were. There was a box in the MPR that pointed to food prices impacting inflation expectations but not having a corresponding impact on future inflation outcomes. So it seems as though consumer inflation expectation data will not be as important for the market as it was previously. Conversely labour and inflation data will have even more importance than previously.

- 3) With the other 8 MPC members having entrenched views and what they are watching fairly clearly set out in the individual view paragraphs in the Minutes, market volatility around non-Bailey speeches is likely to be much reduced. This week we have appearances from Lombardelli (today), Greene (Tuesday / Thursday) and Pill (Wednesday) – but we know that none of these members are likely to vote for a December cut. And further, we know that cuts can be delivered in the near-term via 5-4 votes without needing any of them to change their views.

SOFR: Net Short setting Dominated In Futures On Friday

OI data points to net short setting dominating as the SOFR futures strip twist steepened on Friday.

- SFRU5 seemed to see the only instance of net long setting, while net short setting outweighed any instances of net long cover further out the strip (in net pack terms).

| 07-Nov-25 | 06-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,368,954 | 1,363,750 | +5,204 | Whites | +34,537 |

SFRZ5 | 1,463,465 | 1,429,462 | +34,003 | Reds | +20,745 |

SFRH6 | 1,200,012 | 1,204,612 | -4,600 | Greens | +31,944 |

SFRM6 | 1,090,951 | 1,091,021 | -70 | Blues | +7,049 |

SFRU6 | 1,101,732 | 1,100,311 | +1,421 |

|

|

SFRZ6 | 1,202,057 | 1,202,939 | -882 |

|

|

SFRH7 | 841,411 | 834,972 | +6,439 |

|

|

SFRM7 | 813,661 | 799,894 | +13,767 |

|

|

SFRU7 | 765,582 | 748,577 | +17,005 |

|

|

SFRZ7 | 804,505 | 804,277 | +228 |

|

|

SFRH8 | 438,003 | 426,474 | +11,529 |

|

|

SFRM8 | 406,936 | 403,754 | +3,182 |

|

|

SFRU8 | 352,757 | 343,579 | +9,178 |

|

|

SFRZ8 | 331,139 | 332,094 | -955 |

|

|

SFRH9 | 203,432 | 203,438 | -6 |

|

|

SFRM9 | 186,997 | 188,165 | -1,168 |

|

|

US TSY FUTURES: Exposure Rose On Friday

OI data points to a mix of net long setting (TU & FV), short cover (TY), long cover (US) and short setting (WN) as the curve twist steepened on Friday. Additions to curve-wide net exposure comfortably outweighed more limited instances of cover.

| 07-Nov-25 | 06-Nov-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,670,919 | 4,663,989 | +6,930 | +259,724 |

FV | 6,880,202 | 6,852,719 | +27,483 | +1,177,056 |

TY | 5,436,482 | 5,447,959 | -11,477 | -765,922 |

UXY | 2,494,108 | 2,479,221 | +14,887 | +1,333,333 |

US | 1,853,409 | 1,854,908 | -1,499 | -189,983 |

WN | 2,161,227 | 2,154,048 | +7,179 | +1,332,946 |

|

| Total | +43,503 | +3,147,153 |

BOE: MNI BOE Review: November 2025 - Where is the bar for December?

For the full MNI BOE Review, including summaries of sellside views click here.

- The title of our BOE Preview was “It’s All About Bailey” and we expected a 5-4 vote (without much confidence over which way the 5-4 vote would swing). The outcome was a 5-4 vote to leave Bank Rate on hold and the new individual member paragraphs in the Minutes indicated that Governor Bailey was the only MPC member who did have see their vote as a clear cut decision at this meeting.

- We think that overall if data comes in line with the BOE's updated short-term projections and we get a disinflationary Budget that Bailey will support a near-term cut.

- We look into detail at the near-term projections with some material downgrades to the August MPR projections making it harder to undershoot the forecasts.

- We think it unlikely barring very large surprises that we would see any of the other 8 MPC members not repeating their votes at the December meeting.

- 9/21 sellside reviews that we have read see a change in view with 16/21 analysts now looking for a December cut. We look at these views in more detail.

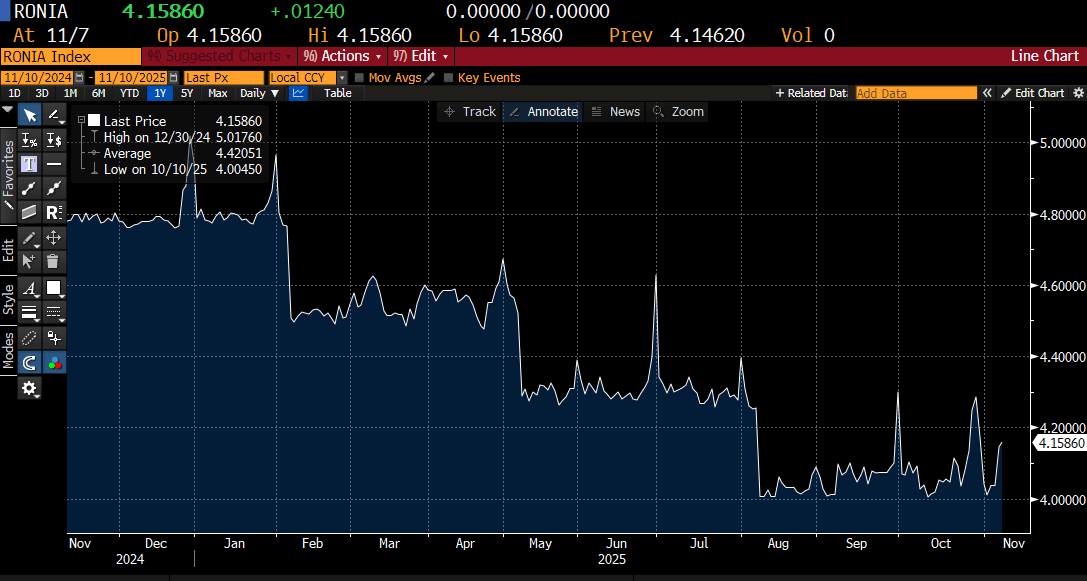

STIR: RONIA likely to remain elevated until Thursday's STR operation

- There is continued focus on UK funding markets. STR takeup dropped back somewhat last week and we saw RONIA spike once again on Thursday as a result, a move that was continued and slightly extended on Friday. We expect RONIA may remain at elevated levels until STR usage picks up again this week (which is very likely in our view).

- Note that tomorrow sees the last ILTR operation before the spread is increased with the operation being priced at Bank Rate plus 3bp from next week when used with Level A collateral (rather than the Bank Rate flat as it has been priced at so far). The change in the spread will only apply to new drawings from next week and so will be the last opportunity to lock in a slightly cheaper rate for 6-months. The date the spread change would be applicable from was announced on Friday but it had been announced months ago that this would take place in November.

- We are unsure how much of the previous ILTR takeup was in response to ILTR repayments and how much was frontrunning ahead of the spread changing. ILTR usage stands at GBP55.4bln (as of last week’s operation) up from around GBP31bln two months ago (around GBP24bln more). In the same two month period TFSME usage fell from around GBP79bln to around GBP42bln (around GBP37bln less).

- We still think that the increase in RONIA is largely a temporary market dislocation but as we continue to edge closer to PMRR and to a more demand-led BOE balance sheet with ample rather than excess reserves volatility in RONIA is likely to be increased relatively to prior periods.

Chart source: Bloomberg Finance LLP

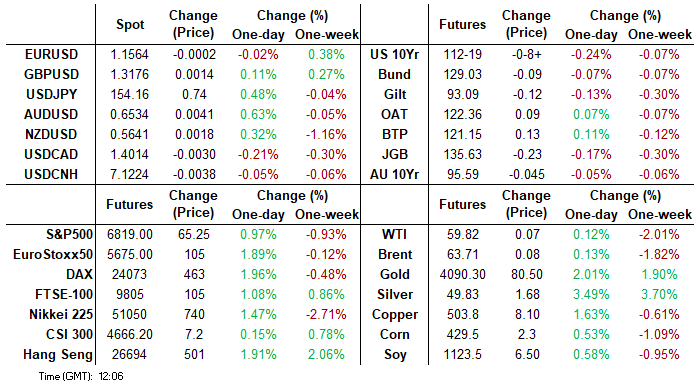

FOREX: Pro-Growth Expectations on Shutdown Optimism Favour AUD, Hamper JPY

- A pro-growth impulse from expectations for the US government reopen potentially this week has led the USD to consolidate last week's losses. Reactions across G10 do not surprise, with positive risk sentiment apparent through strong equity performance weighing on the low-yielding JPY and CHF while supporting the likes of AUD, NZD and NOK.

- USDJPY subsequently sees renewed upside today, clearing Friday's highs and approaching the Nov 4 high at 154.48, the bull trigger. A break of this level would confirm a resumption of the uptrend and open 154.80, the Feb 12 high. First important support lies much further out at 152.46, the 20-day EMA.

- AUD received further tailwinds from RBA Hauser comments being on the hawkish side. For AUDUSD (+0.68%), a break above key resistance at 0.6618 (Oct 29 high) would be required to reinstate a bullish theme.

- NOK meanwhile also benefits from an upside surprise to domestic October CPI. A December cut was already unlikely following last week's Norges Bank meeting and the prospects of that are likely to fall back even further. EURNOK has extended the pullback from 11.80, potentially forming a double top pattern multi-week.

- ZAR outperforms in emerging market FX, very much a product of the precious metals rally (gold +2%), which adds further support to the positive risk backdrop and consolidating dollar weakness.

- Key to watch in the days ahead will be further developments on the shutdown, with a handful of legislative hurdles still to be met: Senate is yet to formally schedule a vote final passage, and a House vote will have to follow. Comments from Fed’s Daly & Musalem, as well as BoE’s Lombardelli, headline a limited G10 calendar today.

OPTIONS: Expiries for Nov10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1475(E1.9bln), $1.1500(E1.1bln), $1.1550(E723mln), $1.1600(E784mln), $1.1750(E1.1bln), $1.1770(E1.2bln)

- GBP/USD: $1.3100(Gbp712mln)

- EUR/GBP: Gbp0.8825(E609mln)

- AUD/USD: $0.6610-20(A$1.3bln)

- USD/CNY: Cny7.1000($651mln)

EQUITIES: Medium-Term Bull Trend in Eurostoxx Futures Intact

- A medium-term bull trend in Eurostoxx 50 futures remains intact and recent weakness is considered corrective. Price has managed to find support below two important price points; the 50-day EMA, at 5576.77, and 5571.50, the base of a bull channel drawn from the Aug 1 low. A clear break of both levels would strengthen a bear theme and highlight a stronger reversal. The bull trigger is 5742.00, the Oct 29 high.

- The trend condition in S&P E-Minis remains bullish and the pullback since the Oct 30 high appears corrective. The contract has managed to find support below the 50-day EMA, currently at 6710.28 and a key support. Friday’s activity also highlights a potential reversal signal - a bullish doji candle. This defines key support at 6655.50, the Oct 7 low. A continuation higher would signal the end of a correction and open 6953.75, Oct 30 high and bull trigger.

COMMODITIES: Downleg in Gold That Started Oct 20 Appears to Have Been Correction

- Recent weakness in WTI futures appears to be a flag formation - a bullish continuation pattern. This suggests that a bullish corrective cycle remains intact for now. Price has recently traded through the 50-day EMA, at $60.87, signalling scope for a stronger recovery. Note too that resistance at $62.34, the Oct 8 high, has been pierced. A clear move through it would expose key resistance at $65.77, Sep 26 high. The bear trigger is $55.96, the Oct 20 low.

- The downleg in Gold that started Oct 20 appears to have been a correction and has allowed an overbought condition to unwind. Price remains above a key support area at the 50-day EMA, at $3880.7. Clearance of this EMA would strengthen a short-term bear theme and signal scope for a deeper retracement. Initial resistance is at $4161.4, the Oct 22 high. A stronger recovery would refocus attention on $4381.5, the Oct 20 high and bull trigger.

| Date | GMT/Local | Impact | Country | Event |

| 10/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 10/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 10/11/2025 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 10/11/2025 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 11/11/2025 | 2350/0850 | Balance of Payments | ||

| 11/11/2025 | 0001/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 11/11/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 11/11/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 11/11/2025 | 0820/0920 | ECB Lagarde Video Message at Bank of Albania | ||

| 11/11/2025 | 0830/0930 | Riksbank Minutes | ||

| 11/11/2025 | 0830/0830 | BOE Greene in Panel at UBS European Conference | ||

| 11/11/2025 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 11/11/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 11/11/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 11/11/2025 | 1200/1200 | BOE APF Quarterly Report | ||

| 11/11/2025 | - | *** | Money Supply | |

| 11/11/2025 | - | *** | New Loans | |

| 11/11/2025 | - | *** | Social Financing | |

| 11/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index |