FOREX: Pro-Growth Expectations on Shutdown Optimism Favour AUD, Hamper JPY

- A pro-growth impulse from expectations for the US government reopen potentially this week has led the USD to consolidate last week's losses. Reactions across G10 do not surprise, with positive risk sentiment apparent through strong equity performance weighing on the low-yielding JPY and CHF while supporting the likes of AUD, NZD and NOK.

- USDJPY subsequently sees renewed upside today, clearing Friday's highs and approaching the Nov 4 high at 154.48, the bull trigger. A break of this level would confirm a resumption of the uptrend and open 154.80, the Feb 12 high. First important support lies much further out at 152.46, the 20-day EMA.

- AUD received further tailwinds from RBA Hauser comments being on the hawkish side. For AUDUSD (+0.68%), a break above key resistance at 0.6618 (Oct 29 high) would be required to reinstate a bullish theme.

- NOK meanwhile also benefits from an upside surprise to domestic October CPI. A December cut was already unlikely following last week's Norges Bank meeting and the prospects of that are likely to fall back even further. EURNOK has extended the pullback from 11.80, potentially forming a double top pattern multi-week.

- ZAR outperforms in emerging market FX, very much a product of the precious metals rally (gold +2%), which adds further support to the positive risk backdrop and consolidating dollar weakness.

- Key to watch in the days ahead will be further developments on the shutdown, with a handful of legislative hurdles still to be met: Senate is yet to formally schedule a vote final passage, and a House vote will have to follow. Comments from Fed’s Daly & Musalem, as well as BoE’s Lombardelli, headline a limited G10 calendar today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Trump Oval Office Announcement Underway Shortly

US President Donald Trump is shortly due to deliver an announcement in the White House Oval Office. LIVESTREAM The announcement is expected to relate to drug pricing and could follow a similar template to a recent pledge from Pfizer.

- The announcement will be Trump's first press remarks since a market-moving Truth Social statement earlier today in which Trump suggested calling off a meeting with Chinese President Xi Jinping and raising tariffs on China in response to new export controls from Beijing on rare earths. See earlier bullets here and here.

RATINGS: Moody's Completes Periodic Review Of Belgium, No Rating Action

No ratings actions for Belgium from Moody's, which is quoted in a press release on Bloomberg: "Moody's Ratings (Moody's) has completed a periodic review of the ratings of Belgium and other ratings that are associated with this issuer. The review was conducted through a rating committee held on 2 October 2025 in which we reassessed the appropriateness of the ratings in the context of the relevant principal methodology(ies), and recent developments. This publication does not announce a credit rating action and is not an indication of whether or not a credit rating action is likely in the near future."

- There had been some speculation there could be a ratings action - MNI wrote Thursday: "* Moody's on Belgium (Current rating Aa3, Outlook Negative): We expect Moody's to maintain their current stance in the absence of 2026 budget details."

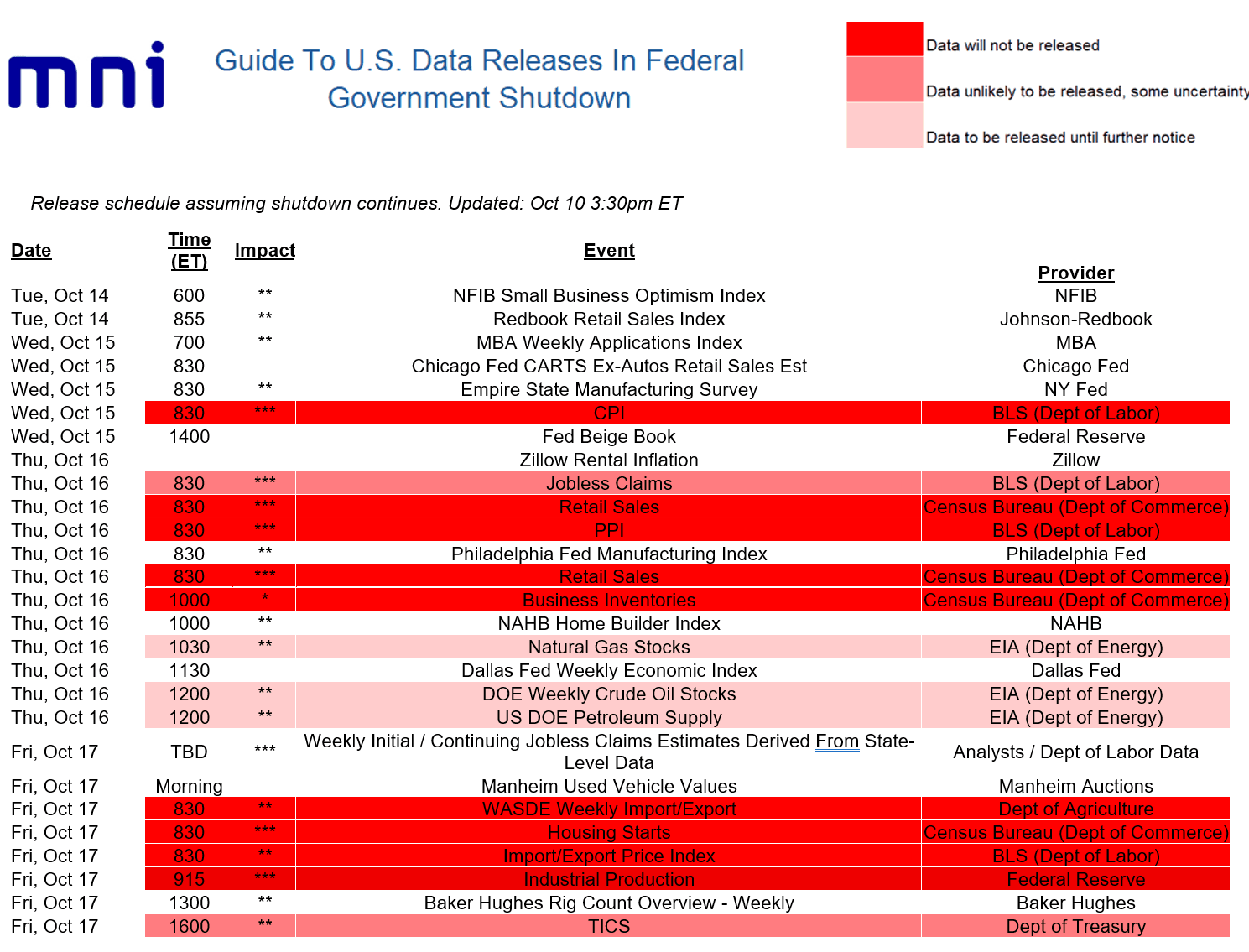

MACRO ANALYSIS: US Macro Week Ahead: No CPI, But Plenty Of Pre-Blackout FedSpeak

Below is the week’s data schedule, with MNI’s annotation of whether or not data will be postponed.

- As we went to press, the Fed announced that next week's Industrial Production data will be postponed (was due to be published next Friday Oct 17) as the data “incorporate a range of data from other government agencies, the publication of which has been delayed as a result of the federal government shutdown.”

- We won’t be getting September CPI as scheduled on Oct 15, but at least the BLS announced it will publish the data on Oct 24.

- As such next week we’ll be looking at some under-covered data points, including the Redbook weekly and Chicago Fed’s CARTS retail sales data (in lieu of the Census Bureau retail sales report), with a little more focus than usual on regional Fed manufacturing indices (NY, Philadelphia).

- Once again, the dearth of tier-one data leaves Fed commentary in focus ahead of the pre-FOMC blackout period: highlights for us are Philadelphia Fed President Paulson making her first comments on monetary policy on Monday since being appointed in the summer, while as always Chair Powell bears watching on Tuesday (we also hear from Bowman, Waller, Collins, Miran, Schmid, and Musalem).

- Additionally we get the latest Beige Book which was already key given the FOMC was already increasingly focused on anecdotal information as it attempts to navigate murky economic waters.