MNI US MARKETS ANALYSIS - Stocks Set for Higher Open

Highlights:

- Equities set for a higher open as Trump rows back Powell criticism, is optimistic on China

- GBP hammer candle could set base for further S/T strength

- Bessent appearance to be watched carefully; speaks at IIF at 1000ET/1500BST

US TSYS: TYA Probes Resistance In Extension Of Trump Softening Powell Stance

- Treasuries are firmly twist flatter, with the majority of moves coming at the open after President Trump said he had no intention of firing Fed Chair Powell.

- It helps build on the broader improvement in risk seen with a softened stance around China trade.

- Long-end gains have extended over the past hour as US desks filter in, with Treasuries continuing their recent relationship of firming amidst risk-on as deleveraging pressures dissipate.

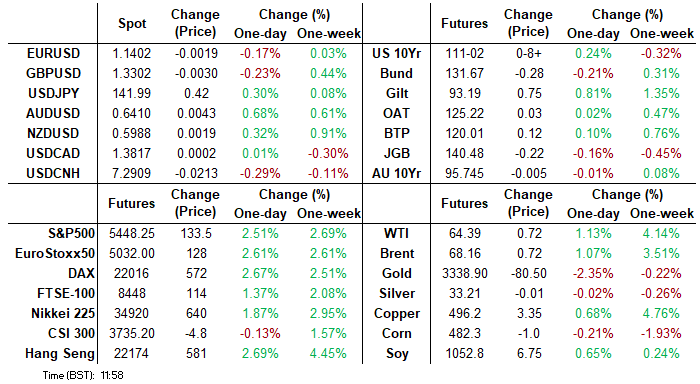

- Cash yields are 2.5bp higher (2s) to 11bp lower (30s).

- 2s10s at 50bp (-8.5bp) for lows since Apr 17 vs a high of over 66bp on Monday.

- 5s30s at 80.6bp (-8.2bp) for lows since Apr 16 vs a high of 97bp on Monday.

- TYM5 has recently touched session highs of 111-04 (+10+) on decent cumulative volumes of 415k.

- It has cleared resistance at 111-00+ (20-day EMA) after which lies 111-17+ (Apr 16 high). Gains are still deemed corrective from a technical angle, with a firmer resistance level at 111-25 (50% retrace of Apr 7-11 bear leg) watched.

- Data: MBA mortgages (0700ET), S&P Global US mfg & serv PMI Apr flash (0945ET), New home sales Mar (1000ET)

- Fedspeak: Goolsbee (0900ET), Musalem (0930ET), Waller (0935ET), Musalem (1435ET), Hammack (1830ET) – see STIR bullet

- Coupon issuance: US Tsy $30B 2Y FRN (1130ET), $70B 5Y Note auction - 91282CMZ1 (1300ET)

- Bill issuance: US Tsy $60B 17W bill auctions (1130ET)

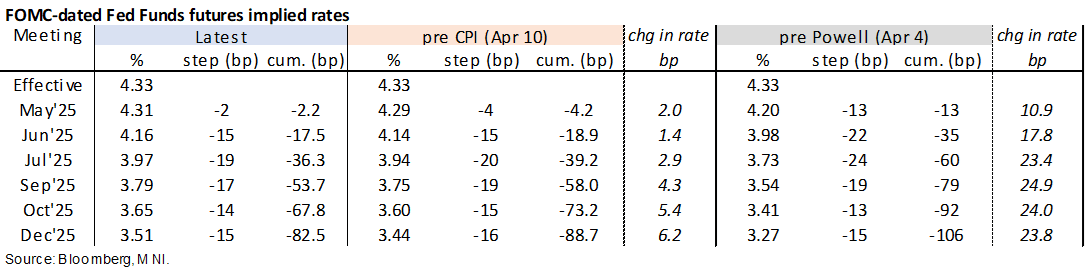

STIR: Fed June Cut Odds Drift Further On Improved Risk Environment

- Fed Funds implied rates are 0.5-4bp higher for 2025 meetings with a firmer risk environment following US President Trump saying he has no intention of firing Powell (but still urges lower rates) and a softer stance on China trade.

- Cumulative cuts from 4.33% effective: 2bp May, 17.5bp Jun, 36.5bp Jul and 82.5bp Dec.

- The Dec 2025 implied rate is 3-4bps lower than overnight highs but otherwise at its highest since early last week.

- The SOFR implied terminal yield of 3.225% (SFRU6) sits +7bp on the day.

- Today’s data focus is on flash PMIs and the Fed’s Beige Book. There is another heavy line-up for Fedspeak although the ‘opening remarks’-heavy nature of today’s speaking schedule could limit content and all speakers have spoken recently.

- Yesterday’s Fedspeak ended up being surprisingly light on headlines amidst Trump’s pressure on the Fed (prior to him somewhat rolling back) although Kugler was marginally less hawkish having previously more explicitly pushed the inflation side of the dual mandate.

- Kugler (permanent voter): "I will support maintaining the current policy rate for as long as these upside risks to inflation continue, while economic activity and employment remain stable. I remain committed to achieving both of our dual-mandate goals of maximum employment and stable prices”. She had said Apr 7 that inflation was now the more pressing issue with regards to tariffs and that the Fed needs to make sure it doesn't rise.

- 0900ET – Goolsbee (’25, dove) opening remarks at economic mobility summit (text tbd)

- 0930ET – Musalem (’25, hawk) opening remarks at Fed Listens event (text tbd)

- 0935ET – Waller (permanent voter, dove) opening remarks at Fed Listens event (text only)

- 1435ET – Musalem (’25, hawk) informal closing remarks

- 1830ET – Hammack (’26, hawk) on balance sheet (text + Q&A)

EUROZONE DATA: Weak France and Germany Weigh On EZ April Flash Services PMI

The Eurozone-wide services PMI was 49.7 (vs 50.5 cons, 51.0 prior). While the miss was expected given the weaker-than-expected French and German data earlier this morning, the smaller deviation from consensus (compared to FR/GE) suggests the EZ ex-France and Germany was a little better than expected.

- We estimate the German/France composite services PMI at 48.0 (vs 49.6 prior), with the ex-German/France composite at 52.7 (vs 53.3 prior).

- The manufacturing reading was 48.7 (vs 47.4 cons, 48.6 prior). We estimate the German/France composite manufacturing PMI at 48.1 (vs 48.4 prior) and the ex-German/France composite at 49.5 (vs 48.9 prior).

- The composite EZ reading was 50.1 (vs 50.2 cons 50.9 prior), the lowest since December.

Key notes from the EZ-wide release (focusing on ex-German/France comments):

- “The rest of the Eurozone continued to record solid growth of output, albeit with the pace of expansion easing slightly from that seen in March”.

- “Companies were generally reluctant to expand output given a further reduction in new orders during April”…” New export orders (which include intra-Eurozone exports) also decreased, and at a broadly similar pace to that seen for total new business”

- “April saw a sharp drop in business confidence in the euro area”…” . The drop in confidence was widespread, both in terms of sector and geographical coverage”

- “A solid reduction in manufacturing staffing levels outweighed a modest and slower increase in workforce numbers in the service sector. Continued falls in employment in the largest two Eurozone economies cancelled out job creation elsewhere”.

- “Cost inflationary pressures waned at the start of the second quarter”…” Inflation was centred on the services sector”.

- “Selling prices were raised across both monitored sectors”.

US TSY FUTURES: Mix Of Positioning Swings Seen On Tuesday, Little DV01 Change

OI data points to a mix of net short setting (TU & FV), long cover (TY), long setting (UXY) and short cover (US & WN) as the curve twist flattened on Tuesday. The curve-wide net DV01 equivalent change on the day was very limited.

| 22-Apr-25 | 21-Apr-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,089,333 | 4,082,707 | +6,626 | +247,855 |

FV | 6,666,775 | 6,610,989 | +55,786 | +2,402,962 |

TY | 4,723,656 | 4,750,113 | -26,457 | -1,708,211 |

UXY | 2,247,491 | 2,243,868 | +3,623 | +318,991 |

US | 1,804,213 | 1,817,369 | -13,156 | -1,671,466 |

WN | 1,880,800 | 1,883,017 | -2,217 | -409,330 |

|

| Total | +24,205 | -819,198 |

STIR: Mix Of Long Cover & Short Setting Seen in SOFR Futures On Tuesday

OI data points to a mix of net long cover and short setting through the SOFR blues on Tuesday, with the former slightly more prominent.

| 22-Apr-25 | 21-Apr-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,113,665 | 1,116,586 | -2,921 | Whites | -41,399 |

SFRM5 | 1,209,954 | 1,226,802 | -16,848 | Reds | +32,007 |

SFRU5 | 959,684 | 968,954 | -9,270 | Greens | -8,655 |

SFRZ5 | 1,078,733 | 1,091,093 | -12,360 | Blues | +2,760 |

SFRH6 | 682,724 | 673,679 | +9,045 |

|

|

SFRM6 | 686,265 | 678,423 | +7,842 |

|

|

SFRU6 | 664,863 | 663,406 | +1,457 |

|

|

SFRZ6 | 865,341 | 851,678 | +13,663 |

|

|

SFRH7 | 607,014 | 610,085 | -3,071 |

|

|

SFRM7 | 548,928 | 556,859 | -7,931 |

|

|

SFRU7 | 368,061 | 365,046 | +3,015 |

|

|

SFRZ7 | 394,801 | 395,469 | -668 |

|

|

SFRH8 | 254,575 | 252,278 | +2,297 |

|

|

SFRM8 | 180,609 | 179,827 | +782 |

|

|

SFRU8 | 135,185 | 134,516 | +669 |

|

|

SFRZ8 | 152,456 | 153,444 | -988 |

|

|

EUROPE ISSUANCE UPDATE

Austria triple tranche syndication: Spreads set

- Benchmark tap of the 2.50% Oct-29 RAGB. Spread set at MS + 19bp (guidance was MS+20 Area), Books in excess of E12bln.

- Benchmark tap of the 3.20% Jul-39 RAGB. Spread set at MS + 66bp (guidance was MS+67 Area), Books in excess of E16bln.

- Benchmark tap of the 3.15% Oct-53 RAGB. Spread set at MS + 97bp (guidance was MS+98 Area), Books in excess of E18bln.

German auction results

- Very soft 10-year Bund auction; still no futures impact

- Another German auction with soft demand - this time for a 10-year Bund.

- That was the smallest volume of bids for a 10-year Bund auction since October 2022.

- Some of this is expected as it is a smaller auction size (E4.0bln rather than the recent E4.5bln) but the bid-to-offer of 1.06x compares to 1.64x earlier this month and the bid-to-cover of 1.38x compares to 2.16x - so those metrics are weak too.

- Still not a big impact on Bund futures.

- E4bln (E3.049bln allotted) of the 2.50% Feb-35 Bund. Avg yield 2.47% (bid-to-offer 1.06x; bid-to-cover 1.38x).

FOREX: USD Off Lows, But Rally Shallow Ahead of Bessent Appearance

- A key focus for markets Wednesday will be an appearance from US Treasury Secretary Scott Bessent, who appears at an Institute of International Finance event to share his thoughts on the state of the global financial system. The appearance will take on greater focus given the reports yesterday that Bessent foresees a de-escalation in trade tensions between the US and China, who have effectively installed a bilateral trade embargo. He is set to appear from 1000ET/1500BST.

- The USD Index maintains a large part of the Tuesday rally - triggered by Trump's assurance that he has no intention of firing the Fed chair - however further gains for the USD clearly need fresh impetus given the close proximity to the pullback low. The USD Index remains under the pressure of a death cross in DMA space (50-dma < 200-dma), signaling the building of negative short-term momentum.

- Equity futures markets are firmer across the board, with Wall Street set for a solid open later today. Tesla shares are sharply higher pre-market after earnings yesterday disclosed that Elon Musk would step back from his role in government and focus more wholly on the company. As a result, shares are higher by 6.5% pre-market and set to add $50bln in market cap at the open.

- This risk-on backdrop is supporting AUD most notably, keeping AUD/USD within range of the 0.6439 bull trigger and 0.6467 200-dma. Separately, the tariff and Fed-independence induced volatility has prompted the potential formation of a hammer in the GBP/USD daily chart which, if confirmed, could see the pair establish a base and resume the short-term uptrend. Strength through 1.3400-24 would be key here - opening the 1.3434 bull trigger (the Sep'24 high).

GBP: Potential Hammer Formation Headed into Trade Talks

- Tariff and Fed-independence induced volatility has prompted the potential formation of a hammer in the GBP/USD daily chart which, if confirmed, could see the pair establish a base and resume the short-term uptrend. Strength through 1.3400-24 would be key here - opening the 1.3434 bull trigger (the Sep'24 high).

- The prospects of a UK-US trade deal remain front page news. Today's Times runs that the government is "hopeful" that a deal will allow the UK to avoid the worst of the tariffs - specifically the 25% tariff on steel, aluminium and car imports - however the 10% blanket tariff could be here to stay. Chancellor Reeves is set to meet the US Treasury Secretary on Friday. The Times concludes that ministers hope that they will be able to get a deal over the line by the end of the month.

- JP Morgan write that GBP strength on any US-UK trade deal would present good entry levels to fade over the medium term - with any deal unlikely to undo the key impacts of the last months events on the currency. The UK could also get caught between opposing demands from the US and EU on trade. As a result, they use favourable levels to enter a short GBP position vs NOK, SEK cash basket. They see Sterling’s stagflationary reaction function as remaining on the table as a threat over the rest of the year.

OPTIONS: Expiries for Apr23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E1.9bln), $1.1500-10(E1.3bln)

- USD/JPY: Y138.50($560mln), Y141.00-20($808mln)

- AUD/USD: $0.6290-00(A$2.7bln), $0.6350-55(A$1.2bln)

- NZD/USD: $0.5855(N$704mln)

- USD/CAD: C$1.3975($562mln)

- USD/CNY: Cny7.3000($679mln)

EQUITIES: E-Mini S&P Builds on Tuesday's Gains, Targets Resistance at 20-Day EMA

- Eurostoxx 50 futures have recovered from Tuesday’s low. Recent gains highlight a corrective cycle and the rally marks an unwinding of a recent oversold trend condition. Resistance at the 20-day EMA, at 4971.53, has been breached. The next level to watch is 5105.00, the 50-day EMA. Key support and the bear trigger has been defined at 4444.00, the Apr 7 low. A break of this level would confirm a resumption of the downtrend.

- A reversal higher in S&P E-Minis on Apr 9 highlighted the start of a correction. The trend condition has been oversold following recent weakness and gains have allowed this to unwind. The contract remains below important resistance points and the trend condition is bearish. A resumption of weakness would refocus attention on 4832.00, the Apr 7 low and bear trigger. Initial resistance to watch is 5425.57, the 20-day EMA.

COMMODITIES: Recovery in WTI Futures Still Considered Corrective, For Now

- A bearish theme in WTI futures remains intact and the recovery since Apr 9 is - for now - considered corrective. The move higher is allowing an oversold trend condition to unwind. Recent weakness has resulted in the breach of a number of important support levels, reinforcing a bearish threat. A resumption of the bear cycle would open $53.72, a Fibonacci projection. Resistance is seen at $64.49, the Mar 5 low. The 50-day EMA is at $66.12.

- The trend needle in Gold continues to point north and this week’s fresh cycle high reinforces bullish conditions. The latest move down is allowing an overbought trend condition to unwind. Moving average studies are unchanged, they remain in a bull-mode position highlighting a dominant uptrend. The next objective is $2547.9, a Fibonacci projection. Initial firm support to watch lies at 3184.2, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 23/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 23/04/2025 | 1300/0900 | Chicago Fed's Austan Goolsbee | ||

| 23/04/2025 | 1330/0930 | St. Louis Fed's Alberto Musalem | ||

| 23/04/2025 | 1330/0930 | Fed Governor Christopher Waller | ||

| 23/04/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/04/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/04/2025 | 1400/1000 | *** | New Home Sales | |

| 23/04/2025 | 1400/1000 | Treasury Secretary Scott Bessent | ||

| 23/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 23/04/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 23/04/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 23/04/2025 | 1715/1815 | BOE's Bailey at Institute of International Finance | ||

| 23/04/2025 | 1800/1400 | Fed Beige Book | ||

| 23/04/2025 | 1800/1900 | BOE's Breeden on Monetary Policy and Financial Stability | ||

| 23/04/2025 | 1915/2115 | ECB's Lane in panel on Central Bankers' Dilemmas Amid Changing Liquidity | ||

| 23/04/2025 | 1945/2145 | ECB's Cipollone in panel on Tokenization and the Financial System | ||

| 23/04/2025 | 2230/1830 | Cleveland Fed's Beth Hammack | ||

| 24/04/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 24/04/2025 | 0700/0900 | ** | PPI | |

| 24/04/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 24/04/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/04/2025 | 1230/0830 | * | Payroll employment | |

| 24/04/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 24/04/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/04/2025 | 1300/1500 | ECB's Lane at Peterson Institute Webcast on Monetary Policy Strategy | ||

| 24/04/2025 | 1325/1425 | BOE's Lombardelli on Monetary Policy Strategy | ||

| 24/04/2025 | 1400/1000 | *** | NAR existing home sales | |

| 24/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 24/04/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 24/04/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 24/04/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 24/04/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 24/04/2025 | 2100/1700 | Minneapolis Fed's Neel Kashkari |