MNI US MARKETS ANALYSIS - Still Sensitive to Iran Headlines

Highlights:

- Markets again display sensitivity to any signals of Iran de-escalation - true or otherwise

- Front-end US Treasury yields still rising toward weekly highs

- Labor market data still in focus; Challenger, weekly claims and Revelio Labs all today ahead of payrolls tomorrow

US TSYS: TYM6 Off Lows After Iran Headline Questioned Having Probed Support

Treasuries have extended yesterday’s sell-off, with the front-end pushing back towards Tuesday’s recent lows and the longer end through those lows. Markets are particularly attentive to signs of off-ramps in the Middle East whilst today also sees various labor updates including the easy to miss from calendars Revelio Labs release plus import prices.

- Treasuries and equities rallied off lows on an earlier Sky News Arabia headline that Iran “is ready to abandon its nuclear program on condition that the United States presents a satisfactory alternative offer”, before paring the move somewhat with a lack of corroboration elsewhere.

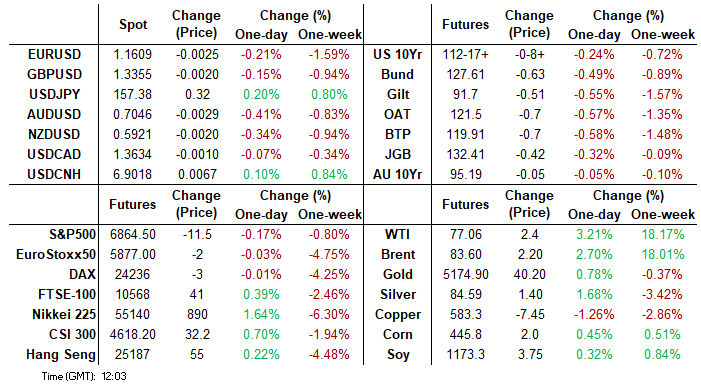

- Cash yields are 1.5-2.5bp higher on the day, led by the front end.

- TYM6 trades at 112-18 (-08) on another solid overnight for volumes at a cumulative 575k.

- It’s off an earlier low of 112-15+ in a move that probed support at 112-16+ (50-day EMA) after which lies 112-11 (61.8% retrace of Jan 20 – Mar 2 bull leg).

- Yield-based levels to note are a 10Y yield of 4.15% equating to 112-11+ and 4.20% to 112-01, with the 10Y yield currently at 4.119% off an earlier high of 4.129%.

- Data: Challenger job cuts Feb (0730ET), Weekly jobless claims (0830ET), ULCs/Productivity Q4 prelim (0830ET), Revelio Labs labor statistics Feb (0830ET), Chicago Fed u/e rate nowcast Feb final (0830ET), Import/Export prices Jan (0830ET)

- Fedspeak: Bowman moderated discussion (1315ET), Goolsbee (1900ET)

- Bill issuance: US Tsy $105B 4W & $95B 8W bill auctions (1130ET)

- Politics: Trump receives intelligence briefing (1100ET), Trump participates in visit of 2025 MLS Champions (1600ET), Trump in policy meeting (1730ET)

STIR: A Renewed Hawkish Shift On Geopol Grounds Before A Labor Data Heavy Docket

- US 2026 rates are back towards Tuesday’s most hawkish levels since June, with crude futures climbing further on net albeit off earlier highs as markets remain particularly attentive to signs of escalation/off-ramps in the Middle East.

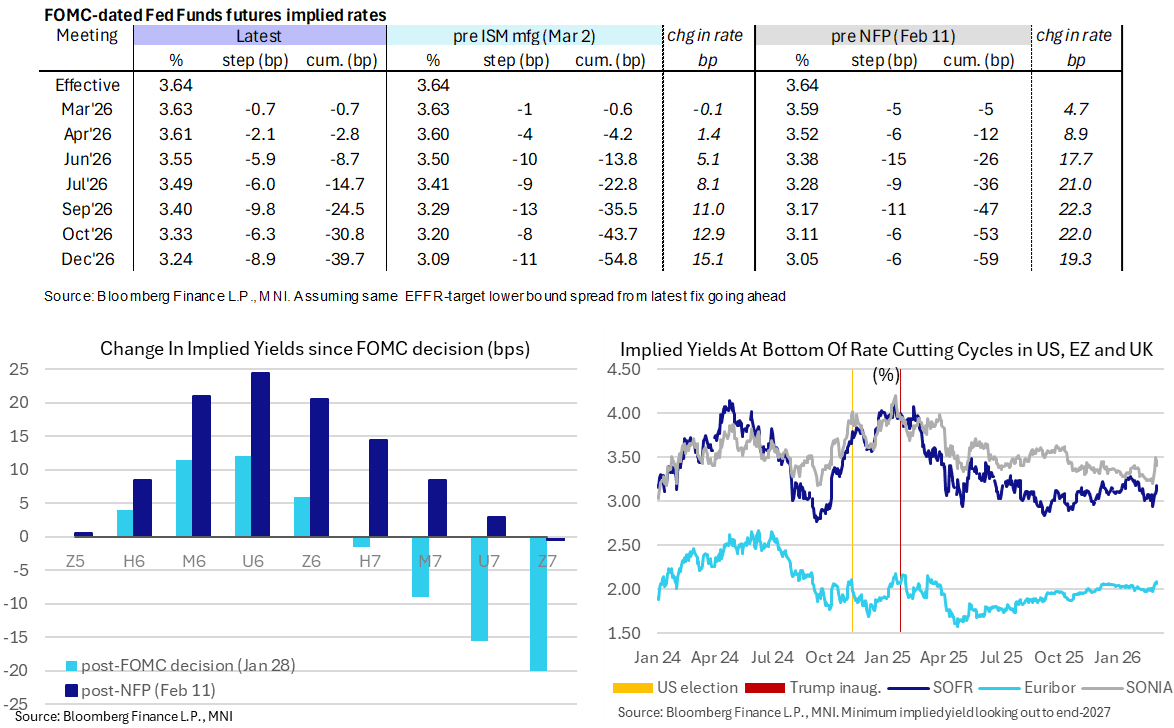

- Cumulative cuts from 3.64% effective: 0.5bp Mar, 3bp Apr, 10bp Jun, 17.5bp Jul, 28.5bp Sep, 31bp Oct and 39.5bp Dec.

- SOFR futures are 4.5 ticks lower through most 2027 contracts, with the terminal implied yield of 3.18% (U7) in the upper half of the ytd range of 2.94-3.285%.

- There’s a heavy collection of labor data today, with Challenger job cuts in Feb (0730ET), preliminary Q4 estimates for ULCs/productivity (0830ET), Revelio Labs labor statistics for Feb (0830ET), the final Feb update for the Chicago Fed’s u/e rate nowcast (0830ET) and the usual weekly jobless claims update (0830ET).

- Today’s Fedspeak is limited to VC Supervision Bowman (voter, dove) at an event on banking supervision and the economy at 1315ET (no text) before Chicago Fed’s Goolsbee (’27 voter, typically dovish but a hawkish dissent in Dec25) at a Foreign Policy Association dinner at 1900ET.

SOFR: Mix Of Long Cover & Short Setting In Futures On Wednesday

OI data points to long cover dominating in the whites, greens and blues, while short setting was most prominent in the reds as most SOFR futures settled lower on Wednesday. The escalation of the conflict in the Middle East and resultant swings in oil prices continue to dominate when it comes to fundamental inputs.

| 04-Mar-26 | 03-Mar-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,309,075 | 1,305,899 | +3,176 | Whites | -49,877 |

SFRH6 | 1,329,975 | 1,342,151 | -12,176 | Reds | +63,024 |

SFRM6 | 1,301,300 | 1,311,312 | -10,012 | Greens | -14,831 |

SFRU6 | 1,205,302 | 1,236,167 | -30,865 | Blues | -5,909 |

SFRZ6 | 1,345,326 | 1,305,806 | +39,520 |

|

|

SFRH7 | 929,038 | 915,492 | +13,546 |

|

|

SFRM7 | 877,541 | 865,641 | +11,900 |

|

|

SFRU7 | 724,542 | 726,484 | -1,942 |

|

|

SFRZ7 | 1,072,763 | 1,068,007 | +4,756 |

|

|

SFRH8 | 526,358 | 547,256 | -20,898 |

|

|

SFRM8 | 432,051 | 432,663 | -612 |

|

|

SFRU8 | 382,152 | 380,229 | +1,923 |

|

|

SFRZ8 | 380,881 | 379,910 | +971 |

|

|

SFRH9 | 222,404 | 227,412 | -5,008 |

|

|

SFRM9 | 189,231 | 188,743 | +488 |

|

|

SFRU9 | 180,648 | 183,008 | -2,360 |

|

|

NATO: Rutte Speaks On Iran Situation & France's Nuclear Doctrine

Reuters is reporting wide-ranging comments from NATO Secretary General Mark Rutte. Regarding the NATO interception of a ballistic missile fired from Iran towards Turkey, Rutte calls it a 'serious' incident, but Article 5 (NATO's collective defence response) is not in order here. He says the NATO air and missile defence systems that were able to down the missile over the eastern Mediterranean showed that the alliance is vigilant.

- Iran has denied it fired the missile. Middle East Eye reports it could have been fired by 'isolated' Iranian forces, noting the "system known as the “Mosaic” doctrine to respond to challenges in cases of a breakdown in command and control."

- On the conflict in general, Rutte says Iran "was close to becoming a threat to Europe as well", and that "We support [US President Donald] Trump for taking out Iran's nuclear and missile capabilities." He acknowledges that it is "difficult to assess how the situation in Iran will end", but that it must be ensured that Tehran no longer poses a threat. Adds that "My sense is the US knows what it is doing."

- He welcomes French President Emmanuel Macron's speech on nuclear deterrence. Earlier in the week, Macron outlined a new doctrine of 'forward deterrence' that would see France increase its stockpile of nuclear warheads, and facilitate the deployment of its airborne nuclear fleet to bases across Europe. Rutte said this shift was not related to any worry about the US' commitment as an ally, claiming there is 'total commitment' to NATO in Washington, D.C.

AUD: Hormuz Positive Needed For AUDUSD To Clear Resistance Cluster

- AUDUSD has continued to exhibit notable volatility on Thursday, already trading in a 1.11% range on the session. Spot trades 0.44% in the red as an overnight headline of a strike on a Kuwait tanker may still be weighing, despite the latest Iran headlines providing an offsetting boost to risk sentiment.

- Bullish conditions remain intact for AUDUSD after support at the 50-day EMA held Tuesday, intersecting at 0.6931. Short-term parameters for the pair are well defined, with a cluster of significant resistance building between 0.7125-50.

- Potential positive news around the Strait of Hormuz may be required for a convincing move above that cluster as AUD's risk sensitivity would add to Australia's significant exposure to flows through the strait in such a case.

- The RBA is likely to wait until May before lifting its cash rate from 3.85%, but could consider a larger 50bp increase if the Iran conflict pushes oil prices higher and feeds into first-quarter CPI, especially with inflation already above the target band, former officials told MNI. They warned that repeated forecast misses combined with an energy shock risk de-anchoring inflation expectations.

CHF: EURCHF Narrows Gap To 0.9025, Sight Deposits Monday

- EURCHF continues to trade with a bearish tilt on Thursday, slipping to a session low of 0.9050 in recent trade, and eroding the week’s prior rally that was assisted by SNB commentary on a higher readiness to intervene.

- As a reminder, SNB Vice Chairman Martin yesterday reiterated an earlier statement which read "We are prepared to intervene in the foreign exchange market to curb a rapid and excessive appreciation of the Swiss franc, which would jeopardize price stability in Switzerland".

- The phrasing of ‘would jeopardize’ perhaps places a greater emphasis on the importance of this week's cycle lows at 0.9025, with moves below this level likely to be met with additional central bank rhetoric, or active intervention. This potentially limits the attractiveness for fresh CHF longs at this juncture from a risk/reward perspective. Notably, domestic sights deposit data on Monday will show if the Bank has already started to curb franc strength.

- Should EURCHF downside persist, the Fibonacci projection of 0.8913 looks a noteworthy target, while resistance moves down to 0.9121, the 20-day EMA.

- Following yesterday's inflation data, it remains to be seen to what extent early-26 CHF appreciation will filter through to imported Swiss inflation in the coming months, with the feedthrough so far limited - likely a key topic ahead of the March 19 SNB meeting.

OPTIONS: Expiries for Mar05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1565(E894mln), $1.1600(E2.0bln), $1.1650-55(E2.3bln), $1.1685(E1.8bln), $1.1700(E1.0bln), $1.1700-20(E1.1bln)

- USD/JPY: Y157.00-05($1.4bln), Y158.00($818mln)

- EUR/GBP: Gbp0.8725(E698mln)

- AUD/USD: $0.7000(A$1.5bln), $0.7150(A$1.4bln)

- NZD/USD: $0.5950(N$895mln)

- USD/CAD: C$1.3600($1.9bln)

EQUITIES: E-Mini S&P Continues to Trade Within a Relatively Tight Range

- A strong short-term reversal in EuroStoxx 50 futures has resulted in a breach of both the 20- and 50-day EMAs. This highlights potential for a deeper near-term pullback and Tuesday’s sell-off confirmed this threat. Sights are on 5689.00 next, the Dec 18 ‘25 low. On the upside, initial firm resistance is 5964.14, the 50-day EMA ahead of 6023.56, the 20-day EMA. For now, gains would likely be corrective.

- S&P E-Minis have recovered from their most recent lows. For now, the contract continues to trade inside a range. Attention is on the base of this range at 6751.50, the Feb 6 low. This support has been pierced, a clear break of it would highlight a stronger bear threat. On the upside, a resumption of gains and a breach of 6983.75, the Feb 25 high, would instead refocus attention on key resistance and the range top at 7043.00, the Jan 28 high.

COMMODITIES: WTI Futures Bull Cycle Intact, $80 the Next Target

- A volatile bull cycle in WTI futures remains intact. Despite being in overbought territory, the contract traded higher Tuesday to confirm a resumption of the current uptrend. The move higher paves the way for a climb towards the $80.00 handle next. The first key support to monitor is $66.75, the 20-day EMA. A pullback would allow the overbought condition to unwind.

- Gold continues to trade below Monday’s intraday high. For now, a short-term bullish theme remains intact following recent gains. The metal has cleared all key retracement points of the sharp sell-off between Jan 29 - Feb 2. This strengthens the short-term bullish theme and signals scope for an extension towards key resistance and the bull trigger at $5595.5, the Jan 29 high. Initial firm support to watch lies at $5083.1, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 05/03/2026 | - | National People's Congress | ||

| 05/03/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/03/2026 | 1330/0830 | *** | Jobless Claims | |

| 05/03/2026 | 1330/0830 | ** | Import/Export Price Index | |

| 05/03/2026 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 05/03/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 05/03/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/03/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/03/2026 | 1700/1800 | ECB Lagarde Lecture on Global Risk | ||

| 05/03/2026 | 1815/1315 | Fed's Michelle Bowman | ||

| 06/03/2026 | 0700/0800 | ** | Manufacturing Orders | |

| 06/03/2026 | 1000/1100 | *** | EZ GDP 3rd (Regular) | |

| 06/03/2026 | 1000/1100 | ECB Lagarde Lecture at Politecnico di Milano | ||

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/1430 | ECB Cipollone Presentation at European Banking Federation Meeting | ||

| 06/03/2026 | 1330/0830 | *** | Retail Sales | |

| 06/03/2026 | 1330/0830 | *** | Retail Sales | |

| 06/03/2026 | 1500/1000 | * | Ivey PMI | |

| 06/03/2026 | 1500/1000 | * | Business Inventories | |

| 06/03/2026 | 1515/1015 | San Francisco FEd's Mary Daly | ||

| 06/03/2026 | 1515/1015 | Philadelphia Fed's Anna Paulson | ||

| 06/03/2026 | 1700/1800 | ECB Schnabel Keynote at Booth School of Business Policy Forum | ||

| 06/03/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/03/2026 | 1820/1320 | Boston Fed's Susan Collins | ||

| 06/03/2026 | 1830/1330 | Cleveland Fed's Beth Hammack | ||

| 06/03/2026 | 2000/1500 | * | Consumer Credit |