MNI US MARKETS ANALYSIS - Scant Chance of Fed Policy Changes

Highlights:

- Fed decision in view, but scant chance of policy changes

- USD Index stable above lows as US-China trade talks seen commencing by Friday

- Local markets look through escalating India-Pakistan tensions

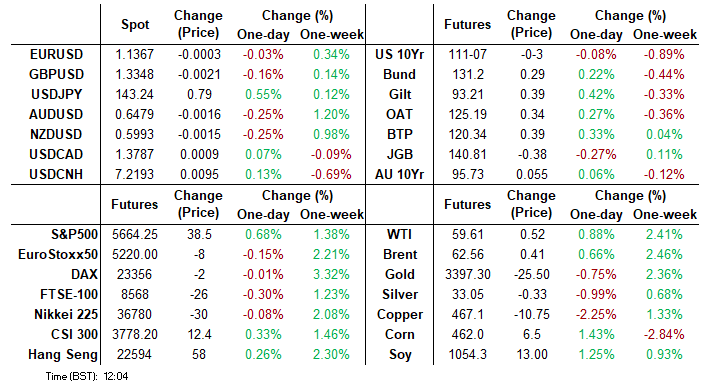

US TSYS: Bear Flatter With A Light Docket Ahead Of The Fed

- Treasuries trade bear flatter, with the front end paring some of yesterday’s gains as investors favor pricing a next 25bp cut in July and for now don't want to price in that much more than 75bp of cuts for 2025 as a whole.

- Risk sentiment was supported on early headlines of US-China trade talks scheduled in Switzerland for later this week. This was followed by PBoC easing but US equity futures and Tsy yields are subsequently off session highs.

- Cash yields are 0-3bp higher on the day, with increases led by 3s whilst 20s and 30s lag.

- 5s30s at 88bps is firmly off cycle highs of 100bps from May 1.

- TYM5 trades at 111-08+ (-01+) for close to yesterday’s highs of 111-12+, on another subdued overnight session with volumes at 230k despite no Japan holiday today.

- It hasn’t troubled resistance at 112-01+ (May 2 high) and the contract still trades close to recent lows, undermining the recent bull cycle. Support is seen at 110-27+ (May 6 low).

- Fed: FOMC announcement (1400ET), Chair Powell press conference (1430ET)

- Data: Weekly MBA mortgage data (0700ET), Consumer credit Mar (1500ET)

- Tsy Sec Bessent also sees day two of his Congressional testimony at 1000ET.

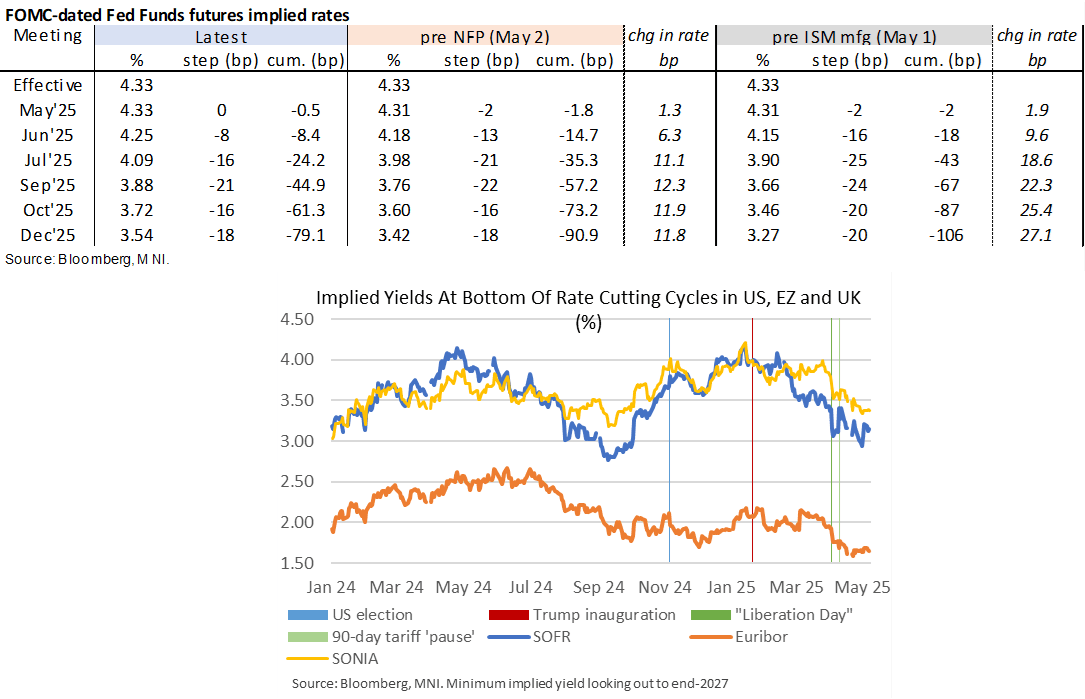

STIR: Fed Rates Tread Water With FOMC Eyed, Terminal Drifts To Dec’26

- Fed Funds implied rates are 0-2bp higher for 2025 meetings with some mild impetus from PBOC easing, although remain comfortably within yesterday’s range.

- Recent beats for ISM mfg (Thu) and services (Mon) plus a resilient payrolls report (Fri) has seen what was already low probability of a cut at today’s FOMC decision dwindle even further to 0.5bp.

- There’s also low probability of a June cut (8.5bp vs 18bp pre ISM mfg) with a next move hovering around Jul (24bp).

- Cumulative cuts from 4.33% effective: 0.5bp May, 8.5bp Jun, 24bp Jul, 45bp Sep and 79bp Dec.

Further out the curve, SOFR futures point to an implied terminal yield of 3.15%, nudging out to SFRZ6 after months in the U6 (although a few days with both U6 and Z6 yields equal). It’s technically the furthest out since fleetingly on Feb 26 and before that mid-Dec prior to the Fed’s hawkish pivot.

CENTRAL BANK PREVIEWS

MNI FED PREVIEW - MAY 2025: When in Doubt, Wait It Out

The FOMC will extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement. It has been an eventful six weeks since the prior decision which included escalation and subsequent partial backtracking in US tariff policy, and the impact of uncertainty on economic sentiment (if not yet the “hard” data). As the FOMC awaits clarity in both government policy and the data on the degree to which one if not both dual mandate targets will be missed, most participants will continue to support a holding pattern until there is a clearer signal to act. See a summary of analyst views here.

MNI BOE PREVIEW - MAY 2025: Could “Gradual” Be Dropped?

Going into this week’s meeting an outcome other than a 25bp cut would be surprising but there will be a number of things to watch: any changes to the guidance and the inflation / growth forecast changes, the vote split and the introduction of new scenarios. For the guidance we expect "restrictive" and "careful" to remain but we question whether "gradual" will be removed and talk through the rationale for this potential change.

MNI RIKSBANK PREVIEW - MAY 2025: Scope for Dovish Tilt

The Riksbank is expected to keep rates on hold at 2.25% on May 8. Although the May decision does not include an updated set of macroeconomic forecasts and rate path projection, we still think there is scope to open the door to another rate cut later this year, conditional on downside growth risks materialising.

MNI NORGES BANK PREVIEW - MAY 2025: Still Holding Steady

Norges Bank is widely expected to keep policy rates on hold at 4.50% on May 8. Rates have been at this level since December 2023, after the Board opted to go against prior guidance for a cut in March due to an acceleration in inflationary pressures at the start of this year. Analysts are unanimous in projecting rates to be held at 4.50% in May, with limited expectations for any guidance changes in the policy statement. Most analysts expect 2x25bp cuts in 2025, with September the most likely start date.

MNI NBP PREVIEW - MAY 2025: Locked & Loaded

The National Bank of Poland will reduce interest rates this week for the first time since October 2023. The recent streak of expectation-missing inflation, labour market and economic activity data have created a conducive environment for looser monetary policy. An abating risk of a rebound in energy prices in 4Q25 further supports the case for the long-awaited launch of an easing cycle. We align with consensus and market pricing in seeing a 50bp rate cut as the most likely outcome of this week’s MPC meeting but see two-sided risks to this baseline scenario.

MNI CNB PREVIEW - MAY 2025: Close Call

The Czech National Bank may be nearing the end of its rate-cutting cycle, but fine-tuning the repo rate by another 25bp to 3.50% is on the table, even though it would likely be framed as a “hawkish cut”. Below-target inflation reported on the eve of the meeting supports the case for an imminent cut, but the underlying structure of inflationary pressures may strengthen the Bank Board’s determination to turn more cautious going forward.

MNI BCB PREVIEW - MAY 2025: Tightening Cycle Nearing End

The Copom is expected to deliver a smaller 50bp Selic rate hike on Wednesday to 14.75%, consistent with the guidance for a slowdown in the tightening pace from prior 100bp increments. Governor Galipolo recently said the board is responding to an inflation dynamic that is challenging, and that the current tightening bias in place remains valid. However, given an uncertain external outlook that demands caution and a well-behaved BRL, a below-consensus 25bp hike should not be ruled out.

MNI BNM PREVIEW - MAY 2025: On Hold for Now

The implications of tariffs from the US remains unclear. Inflation has softened further, yet upside risks are present given the trade war. Domestic consumption remains robust and the recent delay in the GST hike is supportive of the consumer.

US OUTLOOK/OPINION: MNI Fed Preview and Summary Of Analyst Fed Views

In addition to the MNI Fed Preview published on Friday (found here: https://media.marketnews.com/Fed_Prev_May20251_3b6325bf75.pdf), we’re re-upping a summary of analyst views ahead of today’s decision.

- Of the 23 analysts below, the median looks for 75bp of cuts in 2025 before 25bp in 2026.

- After the hawkish readjustment since late last week, the market is similar for this year with Fed Funds futures pricing 78bp of cuts for 2025 although is a little more dovish still in 2026 with close to another 50bp priced.

- Analyst views for 2025 range from zero cuts (Berenberg and Morgan Stanley) to 125bp of cuts (Citi, JPMorgan, TD Securities and Wells Fargo).

- Next cut timing: 9 expect June, 3 in July, 8 in Sept (with SEP meetings still carrying weight), 1 in Dec, 1 in 2026 and 1 seeing no cuts at all.

- A few views stand out, including Morgan Stanley who switch from one of the most hawkish to dovish from end-2025 to end-2026.

US TSY FUTURES: Mix Of Long Setting & Short Cover Seen Tuesday

OI data points to a mix of net long setting (FV, UXY, US & WN) and short cover (TU & TY) during Tuesday’s uptick in Tsy futures, with curve-wide positioning effectively neutral in DV01 equivalent terms.

| 06-May-25 | 05-May-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,037,146 | 4,072,824 | -35,678 | -1,309,381 |

FV | 6,912,263 | 6,909,348 | +2,915 | +124,907 |

TY | 4,956,466 | 4,960,841 | -4,375 | -281,996 |

UXY | 2,291,366 | 2,290,501 | +865 | +76,188 |

US | 1,794,426 | 1,784,087 | +10,339 | +1,313,740 |

WN | 1,888,341 | 1,887,370 | +971 | +178,666 |

|

| Total | -24,963 | +102,124 |

STIR: Short Cover Further Out The SOFR Strip On Tuesday

OI data points to a mix of net long setting and short cover in SOFR futures on Tuesday.

- The single largest positioning swing came via net long setting in SFRU6, while the most meaningful probably came via net short cover in the late greens and entirety of the blues.

| 06-May-25 | 05-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,081,657 | 1,080,637 | +1,020 | Whites | -9 |

SFRM5 | 1,249,521 | 1,253,066 | -3,545 | Reds | +10,397 |

SFRU5 | 1,008,902 | 1,004,235 | +4,667 | Greens | +2,193 |

SFRZ5 | 1,074,181 | 1,076,332 | -2,151 | Blues | -22,907 |

SFRH6 | 741,988 | 748,954 | -6,966 |

|

|

SFRM6 | 724,208 | 721,691 | +2,517 |

|

|

SFRU6 | 718,726 | 701,188 | +17,538 |

|

|

SFRZ6 | 855,264 | 857,956 | -2,692 |

|

|

SFRH7 | 668,341 | 664,651 | +3,690 |

|

|

SFRM7 | 552,913 | 551,371 | +1,542 |

|

|

SFRU7 | 360,952 | 361,800 | -848 |

|

|

SFRZ7 | 393,608 | 395,799 | -2,191 |

|

|

SFRH8 | 269,942 | 277,418 | -7,476 |

|

|

SFRM8 | 189,190 | 194,183 | -4,993 |

|

|

SFRU8 | 149,352 | 153,413 | -4,061 |

|

|

SFRZ8 | 158,551 | 164,928 | -6,377 |

|

|

FOREX: Greenback Stable Above Lows on US-China Trade Talks

- The greenback is more stable above yesterday's low, seeing support from yesterday's late reports that US-China trade talks will commence by the end of the week. This has tipped USD/JPY well off yesterday's lows and back above the Y143.00 handle. Nonetheless, the primary trend direction in USDJPY remains bearish and gains since Apr 22 appear corrective. Resistance at the 50-day EMA, at 146.33, remains intact.

- Meanwhile, GBP/USD has faded further off the Tuesday high, putting prices through the overnight low as well as 1.3329 - the 38.2% retracement of the downleg posted off the Apr28 high. The BoE decision due tomorrow should prove influential here, with the MPC seen opting for another 25bps rate cut.

- The Fed decision due later today is expected to be one of the least consequential of the year, with no change in policy expected as the FOMC look through recent market volatility and await hard economic data in the coming few months to make a decision on rates. Markets price scant chance of any move today, with the next 25bps step lower seen at the July meeting, once we get the first insight into economic behaviour post-tariffs via the NFP and CPI reports.

- Trump's schedule Wednesday is relatively light, however much focus may be paid to his participation in the swearing in ceremony for David Purdue as the US ambassador to China - often seen as a critic of China.

OPTIONS: Expiries for May07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E763mln)

- USD/JPY: Y142.50($804mln), Y143.00($595mln), Y143.20($746mln), Y145.50-55($1.1bln), Y145.85-00($1.6bln)

- EUR/GBP: Gbp0.8555-68(E501mln)

- AUD/USD: $0.6400(A$676mln), $0.6600(A$717mln)

- USD/CAD: C$1.3750-65825mln), C$1.3775-80($961mln)

- USD/CNY: Cny7.2000($500mln)

INR: Rupee Weakness Broadly Contained, Local Traders Warn of Complacency

While the rupee has weakened following the exchange of strikes between India and Pakistan, the move lower for the currency has been fairly contained, with ongoing inflows into local equities and the announcement of new measures from Chinese authorities to support markets helping to limit rupee weakness. USDINR 1-month NDFs spiked moderately higher as initial headlines of the strikes crossed the wires, though price action remains contained within its recent range. Meanwhile, the 1-month 25d risk reversal has spiked from a 7-month low to a 3-month high in the space of a day, indicating that it has become more expensive to hedge against rupee weakness.

- Spot USDINR has generally looked through rising India-Pakistan tensions with the RBI expected to intervene should there be any signs of disorderly moves. Today’s 0.5% move higher – albeit notable – has merely helped to pare last week’s decline, with the pair still over 2% lower compared to the April highs.

- The general lack of follow through into Indian assets (benchmark equity indices are little changed overall) suggests a degree of calmness as markets digest the news flow. Traders who spoke to Reuters say complacency might become a factor if the situation worsens.

- On the other hand, a protracted move higher in implied vols – 1-month USDINR vols showed at their highest since 2022 – points to worries over the potential for a further escalation, with Pakistan having termed India’s assault as a "blatant act of war."

- U.S. Secretary of State Marco Rubio said Washington would continue to engage the Asian neighbours to reach a "peaceful resolution," while a Chinese foreign ministry spokesperson said it finds India's military operation “regrettable.” Note that India procures the majority of its arms from Western nations while Pakistan relies more heavily on China (as per data from the Stockholm International Peace Research Institute).

EQUITIES: Bullish Conditions in E-Mini S&P Remain Intact

- Eurostoxx 50 futures maintain a positive tone and the contract is trading at its recent highs. Price has recently cleared both the 20- and 50-day EMAs, and attention is on 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. This hurdle has been pierced, a clear break of it would pave the way for a climb towards 5341.00, the Mar 27 high. Initial support to watch lies at 5082.47, the 20-day EMA. Clearance of this level would signal a possible reversal.

- Bullish conditions in S&P E-Minis remain intact. The contract has breached the 50-day EMA, at 5622.98. A continuation of the bull phase would expose 5837.25 next, the Mar 25 high and a bull trigger. It is still possible that the entire rally since Apr 7 is a correction. A reversal lower would signal the end of this corrective phase and expose initially, support at 5127.25, the Apr 21 low. First support to watch is 5536.59, the 20-day EMA.

COMMODITIES: Recent Recovery for Gold Could Signal End of Correction Lower

- A medium-term bearish trend in WTI futures remains intact and short-term gains are considered corrective. The move down that started Apr 23 signals the end of the correction between Apr 9 - 23. That cycle higher allowed an oversold condition to unwind. Attention is on $54.67, the Apr 9 low and a bear trigger. Clearance of this level would resume the downtrend and open $53.72, a Fibonacci projection. Key resistance to watch is $64.12, the 50-day EMA.

- Gold has recovered from its recent lows and this suggests the correction between Apr 22 - May 1, is over. A continuation higher would refocus attention on key resistance and the bull trigger at $3500.1, the Apr 22 high. Clearance of this level would confirm a resumption of the primary uptrend. Key short-term support has been defined at $3202.0, the May 1 low. A break of this level is required to signal scope for a deeper retracement.

| Date | GMT/Local | Impact | Country | Event |

| 07/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 07/05/2025 | 1400/1000 | Treasury Secretary Scott Bessent | ||

| 07/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 07/05/2025 | 1800/1400 | *** | FOMC Statement | |

| 07/05/2025 | 1900/1500 | * | Consumer Credit | |

| 08/05/2025 | - | NorgesBank Meeting | ||

| 08/05/2025 | 0600/0800 | ** | Trade Balance | |

| 08/05/2025 | 0600/0800 | ** | Industrial Production | |

| 08/05/2025 | 0700/0900 | ** | Industrial Production | |

| 08/05/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 08/05/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1130/1230 | BOE Press Conference | ||

| 08/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 08/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 08/05/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/05/2025 | 1300/1400 | Decision Maker Panel data | ||

| 08/05/2025 | 1400/1000 | BOC Financial Stability Report and Financial System Survey | ||

| 08/05/2025 | 1400/1000 | ** | Wholesale Trade | |

| 08/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 08/05/2025 | 1500/1100 | BOC Governor Macklem press conference on Financial System Review | ||

| 08/05/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 08/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 08/05/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 08/05/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill |