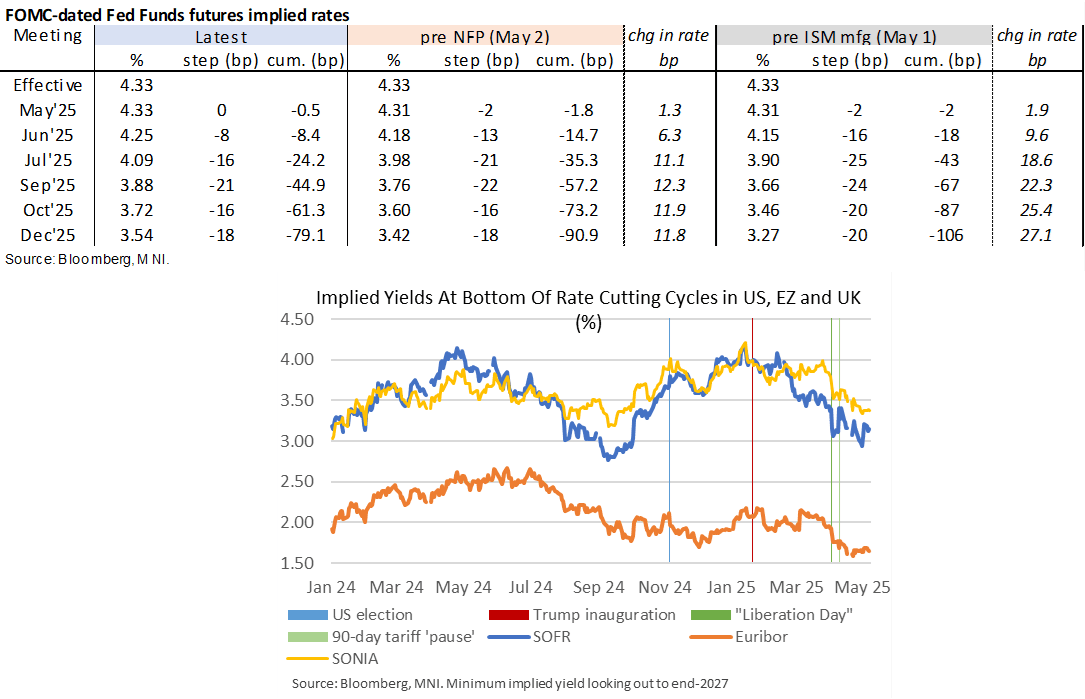

STIR: Fed Rates Tread Water With FOMC Eyed, Terminal Drifts To Dec’26

- Fed Funds implied rates are 0-2bp higher for 2025 meetings with some mild impetus from PBOC easing, although remain comfortably within yesterday’s range.

- Recent beats for ISM mfg (Thu) and services (Mon) plus a resilient payrolls report (Fri) has seen what was already low probability of a cut at today’s FOMC decision dwindle even further to 0.5bp.

- There’s also low probability of a June cut (8.5bp vs 18bp pre ISM mfg) with a next move hovering around Jul (24bp).

- Cumulative cuts from 4.33% effective: 0.5bp May, 8.5bp Jun, 24bp Jul, 45bp Sep and 79bp Dec.

Further out the curve, SOFR futures point to an implied terminal yield of 3.15%, nudging out to SFRZ6 after months in the U6 (although a few days with both U6 and Z6 yields equal). It’s technically the furthest out since fleetingly on Feb 26 and before that mid-Dec prior to the Fed’s hawkish pivot.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Monday Data Calendar: Fed Speak, Bill Auctions

- US Data/Speaker Calendar (prior, estimate)

- 07-Apr 1030 Fed Gov Kugler on inflation dynamics & Phillips curve (ne text, Q&A)

- 07-Apr 1130 US Tsy $76B 13W, $68B 26W bill auctions

- 07-Apr 1300 US Tsy $0B 14D CMB

- 07-Apr 1500 Consumer Credit ($18.084B, $15.0B)

SCANDIS: Underperform G10 Basket On Sour Risk Sentiment and Global Growth Fears

Scandi currencies notably underperform the G10 this morning, with risk sentiment souring amid fresh global growth concerns. Weak Brent crude and natural gas price action has provided an additional headwind to the NOK, leaving NOKSEK down 0.3% today at ~0.9270. A clear break of the November 2020 low at 0.9274 would expose the 76.4% retracement of the March 2020 - March 2022 bull leg at 0.9147 as next support.

- EURNOK is up 1.4% on the session, after breaching trendline resistance drawn from the August 2024 high at 11.7185 on Friday. The psychological 12.0000 handle was pierced earlier before the rally faded. This level remains the initial resistance.

- USDNOK has rallied ~5.5% from last Thursday’s close, with the pair now trading above the 50-day EMA for the first time since March 4.

- For SEK, there will be heightened interest around tomorrow’s Riksbank speeches from Bunge (0645BST) and Thedeen (1230BST). Although the March decision and minutes suggested the current policy rate of 2.25% was an appropriate reflection of the upside and downside risks to the inflation outlook, the Board emphasised a clear readiness to act if the outlook changes.

- The sharp reversal in spot rates over the past two sessions has been reflected in options markets, with the vol premium for 3-month calls over puts spiking higher in Scandi crosses against both USD and EUR.

- This week’s Scandinavian data calendar is headlined by Norwegian March inflation on Thursday. Swedish February activity data (Thursday) and final March CPI (Friday) are also due.

BONDS: TY Futures Close Opening Gap As Equities Edge Away From Lows

TY futures close their opening gap higher as equities tick higher (the latter move has been covered in recent bullets). 10+-Year Tsy yields now 1-4bp higher on the day, with the curve twist steepening. Bund and gilt futures remain above late Friday levels.