MNI US MARKETS ANALYSIS - Oil Surge Sticks, Hindering Equities

Highlights:

- Oil surges on tighter US restrictions for Russian producers

- NOK primary beneficiary, but JPY is weaker against all others

- No weekly jobless claims today, markets anticipate tomorrow's inflation print instead

US TSYS: Firmly Bear Steeper On Sanctions-Driven Crude Oil Surge

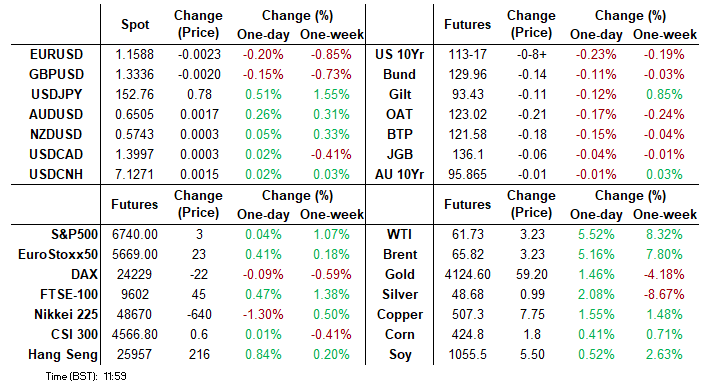

- Treasuries have seen a sizeable bear steepening through European trade in response to crude oil futures surging on US Treasury sanctions on large Russian oil producers (WTI +5.5%).

- Today’s data is headlined by existing home sales and state-level jobless claims later on. Tomorrow’s delayed US CPI report looms large though (MNI Preview here).

- Unusually, there’s no official schedule set for President Trump. One area of headline watch could be developments after yesterday’s risk-off from Reuters reporting the US is considering curbs on software-powered exports to China.

- Cash yields are 2.1-4.7bp higher on the day, led by the long end.

- TYZ5 trades at 113-17 (-08+) on still relatively modest cumulative volumes of 275k.

- It doesn’t trouble support at 113-06 (20-day EMA) whilst a bullish trend structure remains with resistance at 114-02 (Oct 17 high).

- Data: Existing home sales Sep (1000ET), KC Fed mfg survey Oct (1100ET), State-level jobless claims from the afternoon

- Coupon issuance: US Tsy $26B 5Y TIPS - 91282CPH8 (1300ET)

- Bill issuance: US Tsy $110B 4W & $95B 8W bill auctions (1130ET)

- Politics: No Trump schedule posted, leaving scope for ad-hoc comments instead.

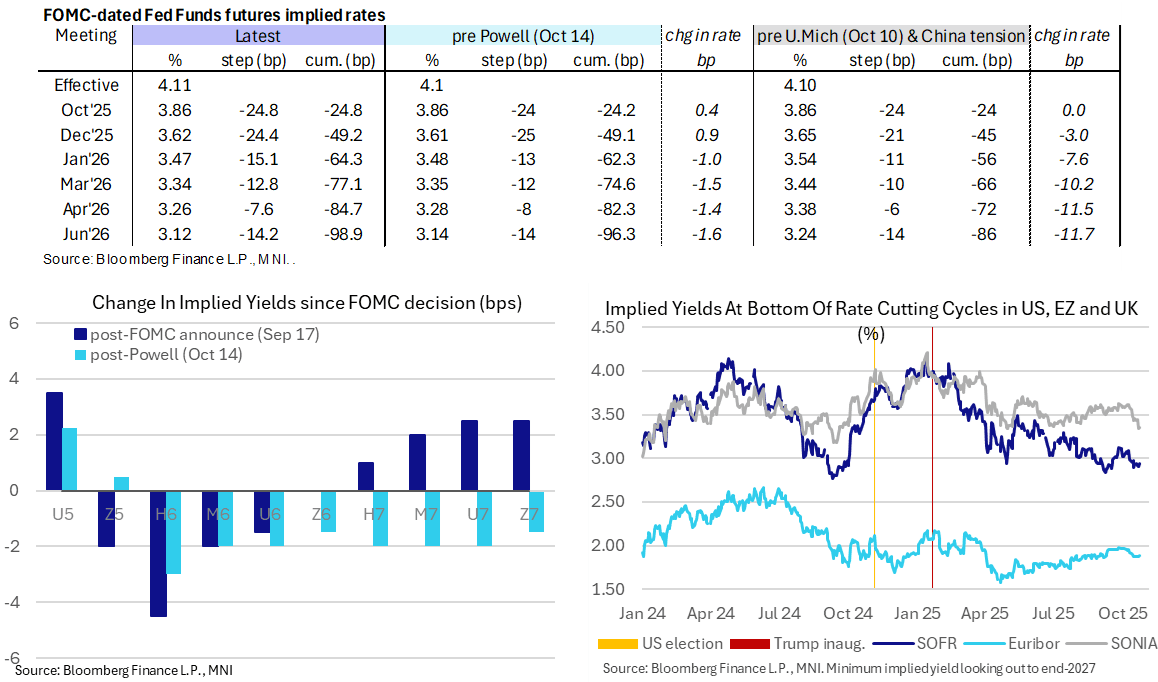

STIR: Modest Impact On Fed Rate Path From Oil Surge

- Fed Funds implied rates are up to 1.5bp higher overnight looking out to mid-2026 meetings, lifted by crude oil futures surging on US Treasury sanctions on large Russian oil producers (WTI +5.5%).

- That said, there’s unwillingness to move away from cumulative cuts next week and in December before a quarterly pace thereafter to mid-2026.

- Cumulative cuts from 4.11% effective: 25bp Oct, 49bp Dec, 64.5bp Jan, 77bp Mar, 84.5bp Apr and 99bp Jun.

- SOFR futures see larger moves on the day, up to 4.5 ticks lower looking out to end-2027.

- It's seen the SOFR terminal implied yield increase to 2.94% (SFRH7, +3.5bp) for the higher end of the past few days but still firmly on the dovish side of longer ranges.

- Today’s data focus sees existing home sales at 1000ET before the now familiar state-level jobless claims release during the afternoon.

US INFLATION: MNI US CPI Preview Update: The Year’s Last ‘Reliable’ CPI Read?

- See the below link for a small update to the original MNI US CPI preview published on Oct 22, now also including unrounded and detailed estimates from Morgan Stanley and NatWest.

- The median unrounded headline CPI estimate ticks up from 0.40 to 0.41% M/M and core ticks up from 0.30 to 0.32% but the broad story is unsurprisingly still the same.

- https://media.marketnews.com/USCPI_Prev_Oct2025_update_24969dda49.pdf

MNI UK Inflation Insight: September 2025

For the full report click here.

- Headline CPI was 0.21ppt below the BOE’s forecast at 3.78%Y/Y with food the biggest surprise (the MNI median expectation was 4.0%Y/Y). Softness is also evident in services which came in at 4.69%Y/Y (0.36ppt below the BOE’s forecast). There was a smaller, but still notable 0.2ppt downside surprise for consensus within services.

- We estimate that only around a quarter to a third of this month's softness has strong potential to be reversed in October data.

- Combine this with last week’s softer-than-expected wage data which saw private regular earnings data come in on course to see a 0.3ppt downside surprise for Q3 and we think the prospects of a November cut have increased to around 50/50.

- Market pricing has shifted decisively with 8.1bp of cuts priced in for the November meeting implying around a 1/3 probability of a 25bp cut. Ahead of the data only 2.1bp was priced for November (and intraday we reached 10.5bp at the peak). A cumulative 16.9bp is now priced by December (implying around a 2/3 probability of a 25bp cut this year – this was pricing around a ¼ probability ahead of last week’s labour market release).

- We look in details at the drivers of the release.

TARIFFS: Fresh Trade Policy Uncertainty Amid Section 301 Pharma Probe

The FT reported yesterday that the US administration is preparing a new probe on trading partner’s pharmaceutical product pricing, under Section 301 of the 1974 Trade Act. If trading partners are found responsible for unfair foreign trade practices, it could set the stage for a fresh round of tariffs on the sector. Link to the story here

- The EU’s existing trade agreement with the US places a 15% cap on pharma tariffs (comprised of the MFN tariff rate plus those imposed under Section 232 of the 1962 Trade Expansion Act). As such, the base case would be that this ceiling holds under a scenario where Section 301 levies are also imposed.

- Countries such as the UK and Switzerland face more uncertainty. Talks between the US and UK on pharma are still ongoing, while Switzerland’s economy is heavily dependent on pharmaceutical sector exports (of which 23% go to the US).

- A reminder that Trump threatened 100% tariffs on imports of branded drugs via Truth Social at the end of last month, but the administration has not yet followed through on those remarks. Officials have said that companies will be given time to show their intentions in moving production into the US and lowering domestic prices.

SCHATZ: Front-end EUR Ranges Contained Ahead Of Tomorrow's PMIs

The EUR front-end has traded in a relatively contained range through this week, with focus still on tomorrow’s October flash PMIs. Last Friday’s lows have limited downside in ERU6 and Z6 futures on several occasions over the last four sessions.

- Accordingly, Monday’s 107.175 low has provided a floor in Schatz futures for now (currently -2 ticks at 107.180).

- Our technical analyst notes that the trend in Schatz futures remains bullish, with initial support at 107.150 (Oct 15 low). A deeper pullback would expose the 20-day EMA at 107.117.

FOREX: Crude Surge Boosts NOK, But Broader G10 Awaiting US CPI

- The targeting of Lukoil and Rosneft by the US administration has led to a surge in crude oil futures, which has filtered well through to FX markets. Resultantly, NOK trades markedly higher, and energy importers are under pressure. As such, JPY is among the poorest performers so far Thursday. The initial move on sanctions by the Treasury was later underpinned by India noting they are likely to make massive cuts in Russian crude imports due to sanctions from the US and Europe.

- As such, NOK outperforms. EURNOK is set for its fifth consecutive negative session and just broke below initial support at 11.58, putting sights on 11.5387 (Sep 15 low). Global developments are set to continue dictating NOK price action in the near-term, with little in the way of market moving domestic data due ahead of Norges Bank's November decision.

- JPY meanwhile is the clear underperformer in G10. USDJPY hovers at its October 14 high of 152.61, with the bull trigger defined as 153.27, the October 10 high. The 50-day EMA is key support for the pair. A clear break of it would signal scope for a deeper pullback.

- SNB meeting minutes from the September meeting mostly reaffirmed the narrative that the Governing Board was quite far away from further easing in their last decision, infitting with the initial policy statement and Q&A. EURCHF is consolidating its bounce from key clustered support between 0.9206/21, again underpinning the relevance of that area as a mid-term pivot point.

- Apart from further potential geopolitical developments, US CPI will highlight the remainder of the week, possibly being the last report that won’t be adversely impacted by the shutdown until the new year. The labor market is driving the Fed rate cut profile currently but broad-based upside surprises in this September report can see this path come into question in the near-term.

- Some ECB speakers are scheduled to speak in the next couple of days, but, as previously, are mostly expected to reiterate previous "rates are in a good place" rhetoric.

OPTIONS: Expiries for Oct23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1515-25(E1.1bln), $1.1555-65(E1.3bln), $1.1575(E1.4bln), $1.1595-00(E741mln), $1.1620-25(E552mln), $1.1650(E1.1bln), $1.1670-80(E1.0bln), $1.1750-70(E2.8bln)

- USD/JPY: Y151.00($434mln), Y152.00($605mln)

- AUD/USD: $0.6585-00(A$1.1bln)

- USD/CAD: C$1.4000-15($657mln)

EQUITIES: Trend Structure in EStoxx50 Remains Bullish

The trend condition in S&P E-Minis remains bullish and the contract is trading above the 50-day EMA. The average, currently at 6632.20, has been pierced but remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. The trend structure in Eurostoxx 50 futures remains bullish. The breach of 5689.00, the Oct 2 high and bull trigger, confirms a resumption of the uptrend. This maintains the price sequence of higher highs and higher lows.

COMMODITIES: WTI Rallies on Latest Russian Sanctions Pressure

A sharp pullback in Gold this week appears corrective - for now. Note that the trend is overbought and a deeper retracement would allow this condition to unwind. Support at the 20-day EMA, at $4037.8, has been pierced. A bearish theme in WTI futures remains intact despite the latest recovery - a correction. Moving average studies are in a bear-mode position, highlighting a dominant downtrend.

| Date | GMT/Local | Impact | Country | Event |

| 23/10/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 23/10/2025 | - | ECB Lagarde at Euro Summit in Brussels | ||

| 23/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 23/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1330/1530 | ECB Lane Award Acceptance Speech | ||

| 23/10/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/10/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 23/10/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 23/10/2025 | 1425/1025 | Fed Governor Michael Barr | ||

| 23/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 23/10/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 23/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 23/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 23/10/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 24/10/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 24/10/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 24/10/2025 | 2330/0830 | *** | CPI | |

| 24/10/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 24/10/2025 | 0600/0800 | ** | PPI | |

| 24/10/2025 | 0600/0700 | *** | Retail Sales | |

| 24/10/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 24/10/2025 | 0700/0900 | ** | PPI | |

| 24/10/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 24/10/2025 | 0800/1000 | ECB Cipollone Fireside Chat on International Finance | ||

| 24/10/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 24/10/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 24/10/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 24/10/2025 | 1200/0800 | ** | Brazil Preliminary CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/10/2025 | 1400/1000 | *** | New Home Sales | |

| 24/10/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 24/10/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 24/10/2025 | 1400/1000 | *** | New Home Sales | |

| 24/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 24/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |