MNI US MARKETS ANALYSIS - Oil Spike Sold; Backdrop Benign

Highlights:

- Market backdrop much more benign than feared after US strikes on Iran

- Iran vows retaliation, but no signs of major escalation yet

- Oil prices gapped higher at the open, but Brent retreats as much as 6% off highs

US TSYS: Modestly Lower, Flash PMIs Headline Docket

- Treasuries have seen a particularly contained reaction to US weekend strikes on Iran nuclear facilities, comfortably within Friday’s ranges across benchmark tenors.

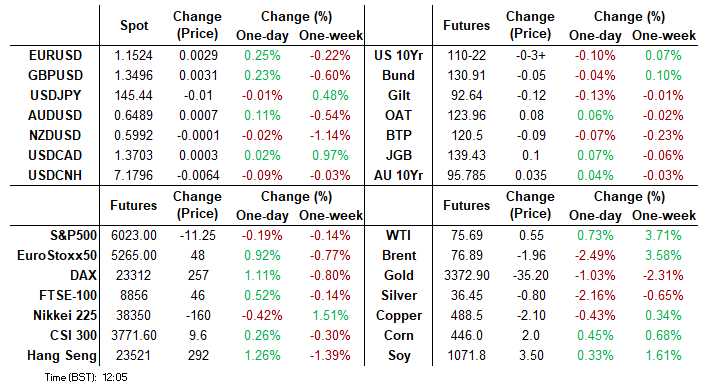

- WTI August futures have given back most of what was almost a 6% increase in Asia trading (currently +0.7% on the day) as markets question the feasibility of Iran’s threat of shutting the Strait of Hormuz.

- Cash yields are 0.8-1.7bp higher across the curve.

- TYU5 trades at 110-28+ (-03) on typical volumes of 305k, off a high of 111-04 with the Asia open.

- Resistance continues to be monitored, seen at 111-13 (Jun 13 high) before 111-14+ (Jun 5 high & 61.8% retrace of May 1-22 downleg). Support is seen at 110-10+ (Jun 16 low).

- Today sees data focus likely on the flash PMIs although existing home sales could see greater sensitivity than usual after various weak housing releases recently.

- Data: S&P Global US flash PMIs Jun (0945ET), Existing home sales May (1000ET)

- Fedspeak: VC Supervision Bowman on mon pol and banking (1000ET), Goolsbee moderated discussion (1310ET), Kugler welcoming remarks (1430ET) – see STIR bullet

- Bill issuance: US Tsy $76B 13W, $68B 26W bill auctions

- Trump meets with the National Security Team at 1300ET – closed press (per Roll Call)

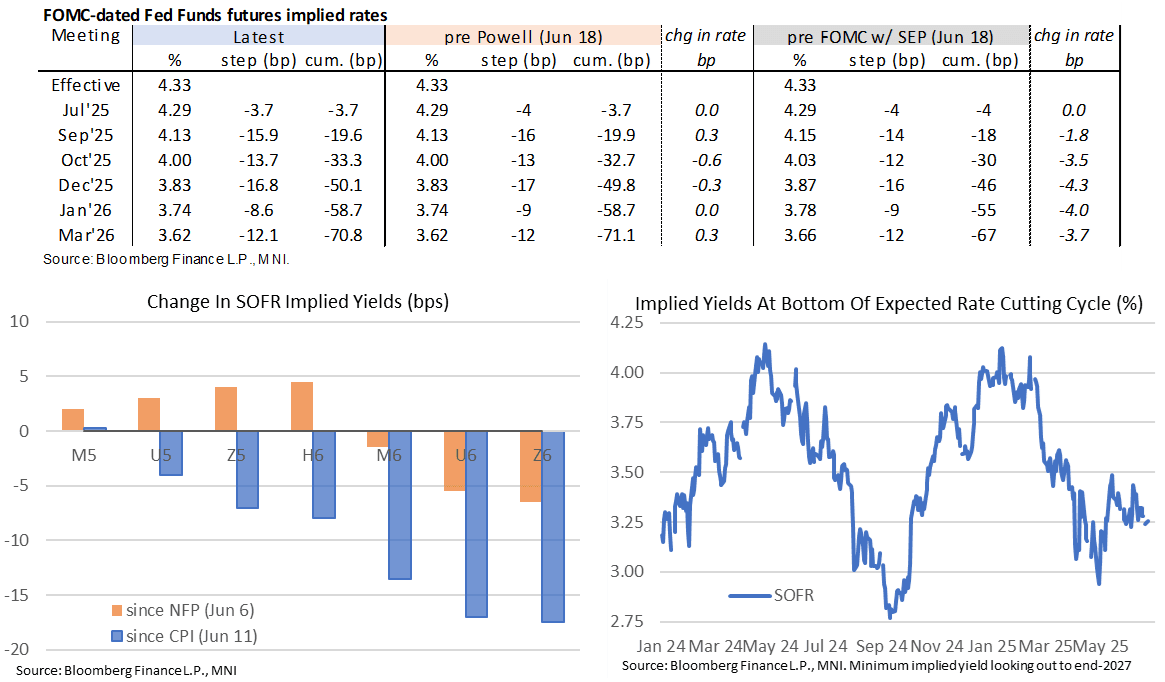

STIR: Fed Rates Shrug Off US Iran Strikes, Post-FOMC Fedspeak Continues

- Fed Funds implied rates are up to 1bp higher for 2025 meetings having seen little sign of net inflationary pressures from the US weekend strikes on Iran nuclear facilities.

- Cumulative cuts from 4.33% effective: 3.5bp Jul, 20bp Sep, 33.5bp Oct, 50.5bp Dec and 59.5bp Jan.

- The SOFR implied terminal yield of 3.255% (SFRZ6, +1.5bp) comes after Friday’s close of 3.24% was the lowest since Jun 4.

- Today sees some more Fedspeak - with focus on Bowman - as we continue to hear views from an increasingly divided FOMC after Friday’s first day with the blackout lifted. 7 of the FOMC see no rate cuts this year through to 2 eyeing three cuts.

- We’ve so far heard from a dovish Waller (voter) re potentially cutting in July whilst Barkin (non-voter) sees no rush to cut rates. Daly (non-voter) appeared somewhere between the two: policy is in a good place now but can’t wait so long before fundamentals necessitate cuts, more to the fall (further labor market slowing could turn into a weakening).

- 1000ET – Fed VC for Supervision Bowman (permanent voter, hawk) speaks on monetary policy and banking (text only)

- 1310ET – Goolsbee (’25 voter, dove) in moderated discussion (text tbd)

- 1430ET – Williams & Kugler (permanent voters) hot Fed Listens event with opening remarks from Kugler (text only). The nature of the event and structure of the remarks should limit market relevance.

SOFR: Long Setting Dominated In Futures Ahead Of Weekend

OI data points to net long setting dominating in most SOFR futures contracts across Thursday & Friday (no settlement Thursday owing to the Juneteenth holiday), with tensions in the Middle East and dovish comments from Fed Governor Waller getting most of the attention.

- There were only isolated, limited pockets of net short cover.

| 20-Jun-25 | 19-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,312,736 | 1,314,473 | -1,737 | Whites | +53,575 |

SFRU5 | 1,151,413 | 1,135,604 | +15,809 | Reds | +22,313 |

SFRZ5 | 1,273,663 | 1,263,262 | +10,401 | Greens | +6,102 |

SFRH6 | 1,008,094 | 978,992 | +29,102 | Blues | +15,756 |

SFRM6 | 851,647 | 848,532 | +3,115 |

|

|

SFRU6 | 799,176 | 783,035 | +16,141 |

|

|

SFRZ6 | 905,688 | 902,245 | +3,443 |

|

|

SFRH7 | 681,872 | 682,258 | -386 |

|

|

SFRM7 | 632,729 | 631,121 | +1,608 |

|

|

SFRU7 | 437,726 | 437,164 | +562 |

|

|

SFRZ7 | 405,989 | 402,584 | +3,405 |

|

|

SFRH8 | 298,037 | 297,510 | +527 |

|

|

SFRM8 | 224,521 | 215,039 | +9,482 |

|

|

SFRU8 | 186,259 | 182,642 | +3,617 |

|

|

SFRZ8 | 172,007 | 170,439 | +1,568 |

|

|

SFRH9 | 142,432 | 141,343 | +1,089 |

|

|

US TSY FUTURES: Long Setting Most Prominent At End Of Last Week

OI data points to net long setting in most contracts between Wednesday and Friday settlement (there was no settlement on Thursday owing to the observation of the Juneteenth holiday).

- Exceptions to the wider theme came via limited net short cover in the long end (US & WN).

- TY futures experienced the only meaningful DV01 positioning swing of note.

| 20-Jun-25 | 18-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,119,715 | 4,102,063 | +17,652 | +686,386 |

FV | 6,976,469 | 6,954,354 | +22,115 | +961,436 |

TY | 4,822,978 | 4,788,474 | +34,504 | +2,285,417 |

UXY | 2,369,694 | 2,367,532 | +2,162 | +188,826 |

US | 1,746,724 | 1,747,909 | -1,185 | -163,378 |

WN | 1,876,909 | 1,880,098 | -3,189 | -571,035 |

|

| Total | +72,059 | +3,387,651 |

SNB: MNI SNB Review - June 2025: Raising the Bar

FULL REPORT HERE (incl. a rough transcript of the post-announcement press conference Q&A)

Executive Summary:

- SNB cut its policy rate by 25bp, meeting market and analyst consensus

- The updated conditional inflation forecast, opening remarks and press conference all had a hawkish tilt to them in our view

- Market pricing through the next, September, meeting was initially aggressive but has since then paired back to OIS-implied odds of around 20% for a further cut into negative territory

EUROPE ISSUANCE UPDATE:

Slovenia syndication: Mandate

- Slovenia has announced a mandate to hold an investor call today ahead of a transaction to launch an inaugural 10-year EUR sustainability-linked bond.

EU auction results

- E1.798bln of the 2.875% Oct-29 EU-bond. Avg yield 2.383% (bid-to-cover 1.56x).

- E2.182bln of the 3.375% Dec-35 EU-bond. Avg yield 3.096% (bid-to-cover 1.28x).

- E1.372bln of the 0.70% Jul-51 EU-bond. Avg yield 3.631% (bid-to-cover 1.07x).

Belgium auction results

- E902mln of the 0.10% Jun-30 OLO. Avg yield 2.444% (bid-to-cover 2.13x).

- E1.075bln of the 3.10% Jun-35 OLO. Avg yield 3.085% (bid-to-cover 2.00x).

- E1.325bln of the 0.40% Jun-40 OLO. Avg yield 3.515% (bid-to-cover 2.08x).

MIDEAST: IDF Spox Says IRGC HQ Hit; Russia's Putin Meets w/Iran For Min

Amid continuing Iranian missile strikes on Israel, and vice versa, Reuters reports comments from Israeli Defence Forces (IDF) spox Effie Defrin. Says that the Iranian attacks "are not behind us" and that the "Iranian threat has not been eliminated". Claims that the Israeli air force has hit every Iranian base from where missiles have been launched at Israel. Adds that Israel's military chief has been in regular contact with his US counterpart. Amichai Stein at Israel's i24 posts on X: "In the current attack, hundreds of [IRGC] members were eliminated inside the targeted buildings..."

- Israeli Defence Minister Israel Katz's office confirms the strike on the IRGC HQ, as well as Evin Prison. His office says "for every attack on Israel's home front, the Iranian dictator will be severely punished and strikes will continue with full force." Adds "We will continue to act to defend the home front and defeat the enemy until all war objectives are achieved."

- Separately, a high-profile meeting between Russian President Vladimir Putin and Iranian Foreign Minister Abbas Araghchi it taking place in Moscow. State TV reports Putin telling Araghchi that "Our position on current events has been relayed by the foreign ministry: that the aggression against Iran is groundless." Says Russia will "try to help the Iranian people," adding their meeting "will give us the best opportunity to find ways out of the current situation."

- Aragchi tells Putin that the US and Israeli actions are "illegitimate" and that Russia "is on the right side of history."

FOREX: USD Behaviour Suggests S/T Base Could Be In

- Greenback rally is holding here despite the more benign market backdrop in response to the US strikes on Iran. The move higher in the USD doesn't look directly headline driven, but participation is decent on the EUR/USD sell-off as the pair tests overnight lows. Headlines on repeated Israeli targeting of the Fordow nuclear site will be pressing for this direction of travel, however.

- It's USD/JPY and GBP/USD that stand out here, however. GBP/USD is through last week's 1.3383 and a close at current or lower levels today would mark the first close below the 50-dma since October last year.

- This price actions plays into the signals of a short-term base of the USD here - and a possible buy-on-dips pattern forming. We noted last week the importance of the USD Index showing above the downtrendline that's defined dollar weakness across Trump's term so far - and noted that even de-escalation headlines were proving insufficient to trigger any material weakness in the USD. This leaves 100.481 - 100.569 area as the next upside target and plausible resistance for a short-term bounce.

FOREX: USD Rallies Despite More Benign Market Backdrop

- Despite a more benign-than-expected market reaction to the US strikes on Iran - particularly in the oil market - the USD is firmer against all others in G10 headed through to the crossover, staying favoured against all others amid higher geopolitical tensions. There remain several questions over the efficacy of strikes on Iran's nuclear sites over the weekend, but there are few signs of material retaliation from Tehran, despite full-throated threats and even warnings of the closure of the Strait of Hormuz in the hours after the attacks.

- For now, Trump's goals remain a return of Tehran to the negotiating table, or regime change away from the hardline approach of the current government.

- This price actions plays into the signals of a short-term base of the USD here - and a possible buy-on-dips pattern forming. We noted last week the importance of the USD Index showing above the downtrendline that's defined dollar weakness across Trump's term so far - and noted that even de-escalation headlines were proving insufficient to trigger any material weakness in the USD. This leaves 100.481 - 100.569 area as the next upside target and plausible resistance for a short-term bounce.

- With oil prices fully reversing their initial surge to start the week, and equity benchmarks remaining resilient to geopolitical developments, Japanese Yen weakness is continuing to standout. The break of a confluence of technical parameters has been assisting the move higher, namely the breach of the downtrend (drawn from the January highs) and the clean break of the May 29 high, cancelling the recent bearish theme.

- Preliminary June PMI data from the US is expected to confirm a slowing manufacturing sector but resilience from services, with existing home sales set to follow. Central bank speak Monday is headlined by ECB's Lagarde, who addresses EU parliament at 1400BST/0900ET, while Fed's Bowman speaks on monetary policy shortly afterward. ECB's Nagel, Fed's Goolsbee, Williams and Kugler also make appearances.

OPTIONS: Expiries for Jun23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1460-70(E917mln), $1.1490(E863mln), $1.1500(E524mln), $1.1550(E891mln)

- AUD/USD: $0.6500-10(A$597mln)

COMMODITIES: WTI Futures Hit Fresh Cycle High, Bull Cycle Remains Intact

- A bull cycle in WTI futures remains intact and the contract has delivered a fresh cycle high today. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend remains in an extreme overbought position. A continuation higher would expose the $80.00 handle. A firm support is noted at $67.11, the Jun 13 low. A breach of this level would signal scope for a deeper retracement.

- A bullish theme in Gold remains intact and last week’s pullback is considered corrective. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has recently been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3282.7, the 50-day EMA.

EQUITIES: Short-Term Bear Cycle in Eurostoxx 50 Futures Still in Play

- A short-term bear cycle in Eurostoxx 50 futures remains intact and the contract has traded to a fresh cycle low today. Recent weakness has resulted in a breach of the 50-day EMA. Price has also traded through 5279.00, May 23 low. The clear break of both support points signals a S/T top and scope for a deeper retracement. Sights are on 5182.00, the May 2 low and 5100.94, a Fibonacci retracement. Initial resistance is 5343.47, the 20-day EMA.

- The trend condition in S&P E-Minis is unchanged, it remains bullish. For now, the most recent shallow pullback is considered corrective. The contract has pierced support at 6007.80, the 20-day EMA. A clear breach of this average would suggest potential for a deeper retracement and expose the 50-day EMA, at 5906.79. Key short-term resistance and the bull trigger has been defined at 6128.75, the Jun 11 high.

| Date | GMT/Local | Impact | Country | Event |

| 23/06/2025 | - | BOE Bailey At Insurance Chairs Dinner | ||

| 23/06/2025 | 1300/1500 | ECB Lagarde At ECON Hearing | ||

| 23/06/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/06/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/06/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/06/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 23/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 23/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 23/06/2025 | 1720/1320 | Chicago Fed's Austan Goolsbee | ||

| 23/06/2025 | 1830/1430 | Fed Governor Adriana Kugler | ||

| 24/06/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/06/2025 | 0800/0900 | BOE Bailey At Gold Standard Conference | ||

| 24/06/2025 | 0845/1045 | 2025 Budget Press Conference | ||

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0930/1030 | BOE Green On CB Balance Sheet Mgmt | ||

| 24/06/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/06/2025 | 1115/1315 | ECB de Guindos At XLII APIE seminar | ||

| 24/06/2025 | 1230/0830 | *** | CPI | |

| 24/06/2025 | 1230/0830 | * | Current Account Balance | |

| 24/06/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 24/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 24/06/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/06/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/1500 | ECB Lagarde Accepts De Sanctis Award "Europa" | ||

| 24/06/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 24/06/2025 | 1335/1435 | BOE Ramsden At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1355/1555 | ECB Lane Keynote At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 24/06/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 24/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 24/06/2025 | 1400/1500 | BOE Bailey At Lords Econ Affairs Committee | ||

| 24/06/2025 | 1540/1640 | BOE Pill At Gold Standard Conference | ||

| 24/06/2025 | 1550/1650 | BOE Breeden At UK Finance Digital Innovation Summit | ||

| 24/06/2025 | 1630/1230 | New York Fed's John Williams | ||

| 24/06/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 24/06/2025 | 1805/1405 | Boston Fed's Susan Collins | ||

| 24/06/2025 | 2000/1600 | Fed Governor Michael Barr |