MNI US MARKETS ANALYSIS - Light Data Slate Keeps Focus on Fed

Highlights:

- Trump still in Middle-East to talk up investment, while key Russia-Ukraine talks in Istanbul loom

- US - South Korea talks on currency triggers brief phase of USD sales

- Light data schedule keeps focus on market sentiment, central bank speakers

US TSYS: Modestly Firmer In A Thin Docket Before A Busy Thursday

- Treasuries are slightly firmer overnight, more comfortably back in the middle of yesterday’s range awaiting fresh drivers.

- It’s a thin data docket today (just weekly mortgage data) which sees Fed Vice Chair Jefferson in a little more focus at 0910ET, and with an eye on tomorrow’s April reports for US PPI and retail sales amongst others.

- US President Trump flies from Saudi Arabia to Qatar today.

- Cash yields are 0.5-1.5bp lower on the day, with declines led by the belly.

- TYM5 sits at 110-06+ (+ 07+) as it lifts a little more off yesterday’s latest lows of 109-30, on modest cumulative volumes of 280k.

- Technicals point to a bear mode condition, having most recently cleared support at 110-01+ (76.4% retrace of Apr 11 – May 1 bull leg) in a step closer to key support at 109-08 (Apr 11 low).

- Data: MBA mortgage applications (0700ET)

- Fedspeak: Jefferson (0910ET), Daly (1740ET) – see STIR bullet

- Bill issuance: US Tsy to sell $60bn 17-w bills (1130ET)

STIR: Fed Vice Chair Jefferson Headlines Docket

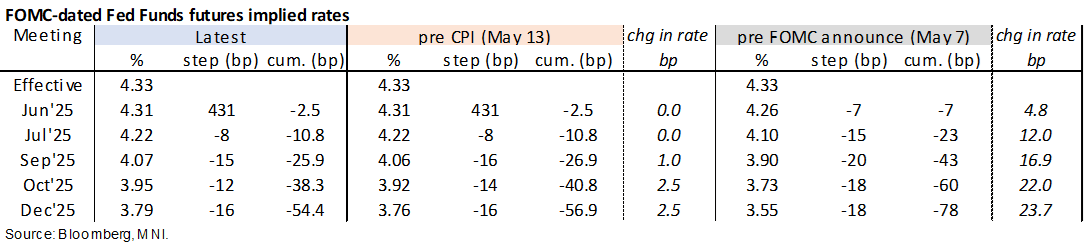

- Fed Funds implied rates are 0-1bp lower for 2025 meetings, close to hawkish extremes.

- The 54bp of cuts priced for 2025 is off yesterday’s 52bps but those were levels last seen in February.

- Cumulative cuts from 4.33% effective: 2.5bp Jun, 11bp Jul, 26bp Sep, 38.5bp Oct and 54.5bp Dec.

- Today’s lighter docket should have tomorrow in mind with PPI/retail sales reports for April and Fed Chair Powell speaking 10 minutes after, albeit on the framework review.

- We touched on Chicago Fed’s Goolsbee (’25 voter) just below, on him solid underlying strength but with him watching for more timely signs of consumers and businesses pulling back.

- Still to come, Fed Vice Chair Jefferson (voter) speaks on the economic outlook at 0910ET (text only) before SF Fed’s Daly (non-voter) in a fireside chat late on at 1740ET (Q&A only).

- A senior figure on the FOMC who doesn’t speak particularly often, Jefferson will be watched closely for any reaction to the US-China trade de-escalation seen since the weekend. He said Apr 3: "In my view, there is no need to be in a hurry to make further policy rate adjustments. The current policy stance is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate… If the economy remains strong and inflation does not continue to move sustainably toward 2%, the current policy restraint could be retained for longer. If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, policy could be eased accordingly."

US TSY FUTURES: Long Cover Most Prominent During Tuesday's Downtick

OI data points to a mix of net long cover (TU, FV, TY & US) and short setting (UXY & WN) as Tsy futures settled lower on Tuesday.

- The curve-wide bias was tilted towards net long cover.

| 13-May-25 | 12-May-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,069,019 | 4,069,747 | -728 | -26,349 |

FV | 6,829,064 | 6,833,604 | -4,540 | -192,231 |

TY | 4,946,063 | 4,961,839 | -15,776 | -1,004,324 |

UXY | 2,311,357 | 2,302,456 | +8,901 | +773,216 |

US | 1,789,209 | 1,809,046 | -19,837 | -2,473,904 |

WN | 1,893,199 | 1,892,210 | +989 | +177,659 |

|

| Total | -30,991 | -2,745,934 |

STIR: Net Short Setting Dominated In SOFR Futures On Tuesday

OI data points to a mix of net short setting and long cover as SOFR futures ticked lower on Tuesday, with the former providing the dominant impulse in all packs through the blues.

| 13-May-25 | 12-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,085,144 | 1,090,242 | -5,098 | Whites | +9,879 |

SFRM5 | 1,213,692 | 1,218,043 | -4,351 | Reds | +27,211 |

SFRU5 | 1,028,381 | 1,013,528 | +14,853 | Greens | +16,719 |

SFRZ5 | 1,142,875 | 1,138,400 | +4,475 | Blues | +3,800 |

SFRH6 | 758,731 | 763,656 | -4,925 |

|

|

SFRM6 | 750,310 | 740,219 | +10,091 |

|

|

SFRU6 | 727,179 | 717,459 | +9,720 |

|

|

SFRZ6 | 875,369 | 863,044 | +12,325 |

|

|

SFRH7 | 655,483 | 658,708 | -3,225 |

|

|

SFRM7 | 578,536 | 569,910 | +8,626 |

|

|

SFRU7 | 362,124 | 357,959 | +4,165 |

|

|

SFRZ7 | 402,425 | 395,272 | +7,153 |

|

|

SFRH8 | 270,127 | 274,575 | -4,448 |

|

|

SFRM8 | 191,706 | 185,255 | +6,451 |

|

|

SFRU8 | 157,639 | 156,480 | +1,159 |

|

|

SFRZ8 | 165,825 | 165,187 | +638 |

|

|

RUSSIA: Kremlin Again Refuses To Say If Putin Will Attend Ukraine Peace Talks

Wires carrying comments from Kremlin spox Dmitry Peskov. Says that the Kremlin will disclose the make-up of the Russian delegation to Istanbul for Ukraine peace talks on Thursday (15 May) when President Vladimir Putin gives the order. This stands in contrast to comments from an unnamed senior Russian lawmaker on Telegram, claiming that the identity of the delegation will be known this evening, and that an 'all-for-all' prisoner exchange could be discussed.

- Peskov claims that Putin's offer of direct talks on Thursday stands. Says "the Russian delegation will be in Istanbul on Thursday and wait for the Ukrainian delegation.

- There remains absolute uncertainty as to whether Putin will attend the talks in person. Not attending risks a backlash from the US, with senior figures including President Donald Trump becoming increasingly tetchy at what they have said is foot-dragging by Moscow.

- Earlier, Brazilian President Luiz Inacio Lula da Silva said that on his way back from a state visit to China, he will stop over in Russia to try and push for negotiations. Lula: “I’ll try to talk to Putin. It costs me nothing to say, ‘hey, comrade Putin, go to Istanbul and negotiate, dammit’”

- On other issues, Peskov says that Putin has an invitation to visit Iran, but that there is no date for the trip agreed yet. On reports that French President Emmanuel Macron is open to deploying nuclear-armed planes across Europe, Peskov says 'proliferation of nuclear arms would not enhance Europe's security.'

IRAN: Foreign Min Confirms E3 Talks Friday As US Denies 'Joint Venture' Proposal

Iranian Foreign Minister Abbas Araghchi has confirmed that officials from Tehran will hold talks with counterparts from France, Germany, and the UK (the 'E3' countries) in Istanbul on Friday, 16 May, as part of the now-collapsed Joint Comprehensive Plan of Action (JCPoA, the 2015 nuclear deal). Araghchi has said that the E3 nations are currently 'isolated' by the indirect talks between Iran and the US that have taken place in recent weeks, adding that he wants this to change.

- On 13 May, NYT reported that "Iran has proposed the creation of a joint nuclear-enrichment venture involving regional Arab countries and American investments as an alternative to Washington’s demand that it dismantle its nuclear program," The article claims that Araghchi presented the proposal to US Middle East envoy Steve Witkoff during the fourth round of talks last weekend in Oman, a claim denied by a spox for Witkoff.

- NYT: "Iran’s proposal entails the establishment of a three-country nuclear consortium in which Iran would enrich uranium to a low grade, beneath that needed for nuclear weapons, and then ship it to other Arab countries for civilian use, [...] a major difference [to the JCPoA] would be the on-the-ground presence of representatives from other countries — perhaps even the United States — to provide an extra layer of oversight and involvement."

- It remains to be seen whether the US' approach of talking up a deal while threatening military consequences if no agreement is reached pushes Tehran towards notable concessions.

EUROPE ISSUANCE UPDATE:

Belgium syndication: Final terms

- EUR7bln (MNI had expected a E7bln size) of the of the new Oct-30 OLO. Books above EU72b, spread set at MS+28 (guidance was MS+30 Area).

Latvia syndication: Revised guidance

- New EUR Benchmark May-30 LatvGB (MNI thinks there is a good chance of a large E1.0-1.5bln transaction size). Revised guidance MS+70a (+/-5) will price in range (guidance was MS+80 area), Books above EU2.8b.

EFSF RfP

- "Today, EFSF, the European Financial Stability Facility, rated Aaa (Moody's) /

AA- (Fitch) / AA (S&P), has sent a Request for Proposal to a selection of banks from the EFSF/ESM Market Group with regards to an upcoming transaction, subject to market conditions." - MNI expects the transaction to take place Monday or Tuesday.

UK auction results

- Looks like decent demand metrics on the 4.50% Mar-35 Gilt auction, though the lowest accepted price of 98.618 was notably below the 98.645 pre-auction mid. However, there has been limited reaction in the secondary market price and in Gilt futures following the publication of the results.

- The 0.3bp tail was tighter than the 0.5bps seen in March and 0.4bps seen in April.

- Meanwhile, the cover ratio of 3.13x was above March’s 2.92x and April’s 2.85x.

- GBP4.25bln of the 4.50% Mar-35 Gilt. Avg yield 4.673% (bid-to-cover 3.13x, tail 0.3bp).

German auction results

- E1.5bln (E1.313bln allotted) of the 1.25% Aug-48 Bund. Avg yield 3.09% (bid-to-offer 3.68x; bid-to-cover 4.20x).

- E1bln (E818mln allotted) of the 2.50% Aug-54 Bund. Avg yield 3.12% (bid-to-offer 1.85x; bid-to-cover 2.27x).

Portugal auction results

- E548mln of the 1.65% Jul-32 OT. Avg yield 2.716% (bid-to-cover 1.97x).

- E702mln of the 4.10% Feb-45 OT. Avg yield 3.753% (bid-to-cover 1.92x).

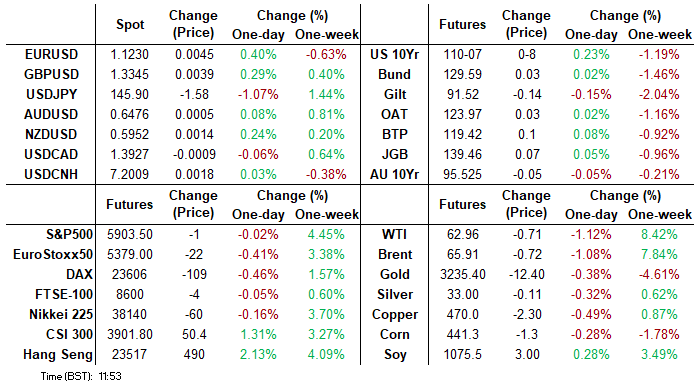

FOREX: USD Slips, FX Strategy in Focus in Light Data Day

- An early phase of USD weakness came alongside reports that the US and South Korea had discussed FX policy as part of trade talks - a standout report considering negotiations with both Japan and China has explicitly not covered currency issues. The move in the greenback was isolated to currency markets given the relative stability in equities and the front-end of the US curve. EUR/USD showed to a new weekly high in response, but USD/JPY is more notable - the price is close to fully erasing the entirety of the China-triggered rally from early Monday morning on healthy volumes.

- USD/JPY slippage Wednesday confirms the bearish technical bias for the pair. A further reversal lower would refocus attention on 142.36, the May 6 low, below which April's pullback low comes into contention.

- EUR/AUD is firmer off lows into the NY crossover, however price printed a fresh monthly low at 1.7248 overnight, keeping focus on 1.7198, the 61.8% retracement of the upleg posted off the February low. A further stabilisation for equities here could see this level come under pressure.

- The data slate is clear Wednesday, leaving more focus on Trump's extended visit to the Middle-East and the central bank speaker schedule - Fed's Waller, Jefferson, Daly and Goolsbee are all set to make appearances, as well as ECB's Villeroy and Holzmann.

- Trump is continuing to talk up relations with Gulf allies, while adding further pressure to Tehran to conclude their commitment to nuclear weapons development in return for closer and freer ties with Western markets. Further negotiations between Tehran and Washington are set for the coming days - progress within which would represent any de-escalation of geopolitical tensions.

JPY: USD/JPY Downside Sticks into NY Crossover, Underlying Long Plays Through

The step lower for USD/JPY triggered by a phase of dollar weakness is picking up into the NY crossover, with rate now having fully erased the Monday rally tripped by the interim US-China trade agreement.

- JPY's progress off the week's lows despite a healthier equity picture may reflect market that remains happy to stay long JPY, despite USD/JPY's bounce off the pullback low: Our CFTC positioning tracker shows a net long of ~50% of open interest, pushing the 52w Z-score to 1.68, the highest among all currencies surveyed.

- This keeps focus on 145.30 support initially - the 38.2% retracement for the upleg posted off 139.89 - with momentum pointed lower - the 50-dma/200-dma differential is now it's largest since October last year.

- Nonetheless, JPY strength is also playing a part here - we know from a WSJ report that neither currency management nor FX rate target levels were mentioned in US-Japan trade talks - meaning there are few implications or conditions on the BoJ's slow tightening cycle ahead.

OPTIONS: Expiries for May14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1150-65(E1.3bln), $1.1175($969mln), $1.1200(E835mln), $1.1390-10(E1.9bln)

- AUD/USD: $0.6475(A$574mln), $0.6500(A$591mln)

- NZD/USD: $0.5855-75(N$757mln)

- USD/CAD: C$1.4000($543mln)

- USD/CNY: Cny7.2000($658mln)

EQUITIES: E-Mini S&P Maintains Positive Tone Following Break of Bull Trigger

- A bullish theme in the Eurostoxx 50 futures contract remains intact. Gains on Monday reinforce current bullish conditions. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. The continuation higher signals scope for a climb towards 5516.00, the Mar 3 high and the key bull trigger. Initial firm support to watch lies at 5152.85, the 50-day EMA. Clearance of this level would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact and this week’s appreciation reinforces bullish conditions. The contract has cleared an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5648.28, the 50-day EMA.

COMMODITIES: Recent Pullback in Gold Considered Technically Corrective

- A downtrend in WTI futures remains intact and S/T gains are considered corrective. For now, the corrective cycle remains in play and price has traded through the 20-day EMA. Key resistance to watch is $63.55, the 50-day EMA. It has been pierced, a clear break of it would highlight a stronger reversal. This would open $66.41, the Apr 4 high. For bears a reversal lower would refocus attention on $54.67, the Apr 9 low and bear trigger.

- The latest pullback in Gold still appears corrective. Key short-term support to watch is $3202.0, the May 1 low. A clear break of this level would undermine the short-term bullish theme and signal scope for a deeper retracement. This would open $3164.3, 61.8% of the Apr 7 - Apr 22 upleg. Note that the 50-day EMA is at $3164.5 - a key support too. The M/T trend remains bullish, a reversal would refocus attention on $3500.1, the Apr 22 high and bull trigger.

| Date | GMT/Local | Impact | Country | Event |

| 14/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 14/05/2025 | 1230/0830 | * | Building Permits | |

| 14/05/2025 | 1240/1440 | ECB's Cipollone On Liquidity Issues Panel | ||

| 14/05/2025 | 1310/0910 | Fed Vice Chair Philip Jefferson | ||

| 14/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 14/05/2025 | 2140/1740 | San Francisco Fed's Mary Daly | ||

| 15/05/2025 | 0130/1130 | *** | Labor Force Survey | |

| 15/05/2025 | 0600/0700 | ** | UK Monthly GDP | |

| 15/05/2025 | 0600/0700 | ** | Index of Services | |

| 15/05/2025 | 0600/0700 | *** | Index of Production | |

| 15/05/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 15/05/2025 | 0600/0700 | *** | GDP First Estimate | |

| 15/05/2025 | 0600/0800 | ** | Norway GDP | |

| 15/05/2025 | 0600/0700 | ** | Trade Balance | |

| 15/05/2025 | 0645/0845 | *** | HICP (f) | |

| 15/05/2025 | 0700/0900 | Flash GDP | ||

| 15/05/2025 | 0700/0900 | ECB's Cipollone at Payments Forum | ||

| 15/05/2025 | 0750/0950 | ECB's Elderson At Green Finance Conference | ||

| 15/05/2025 | 0900/1100 | ** | Industrial Production | |

| 15/05/2025 | 0900/1100 | *** | GDP (p) | |

| 15/05/2025 | 1015/1215 | ECB's De Guindos At ISDA Meeting | ||

| 15/05/2025 | 1130/1330 | ECB's Cipollone In Digital Currency Fireside Chat | ||

| 15/05/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 15/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 15/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 15/05/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/05/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/05/2025 | 1230/0830 | *** | Retail Sales | |

| 15/05/2025 | 1230/0830 | *** | PPI | |

| 15/05/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/05/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 15/05/2025 | 1240/0840 | Fed Chair Jerome Powell | ||

| 15/05/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/05/2025 | 1315/0915 | *** | Industrial Production | |

| 15/05/2025 | 1400/1000 | * | Business Inventories | |

| 15/05/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 15/05/2025 | 1400/1500 | BOE Dhingra At New Economics Foundation conference | ||

| 15/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 15/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 15/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 15/05/2025 | 1800/1400 | *** | Mexico Interest Rate | |

| 15/05/2025 | 1805/1405 | Fed Governor Michael Barr |