MNI US MARKETS ANALYSIS - ISM Services, 3y Supply in Focus

Highlights:

- ISM services and 3y Treasury supply the focus

- USD Index awaiting input as Trump considers Fed, BLS options

- HKMA intervene again, draining more liquidity from local market

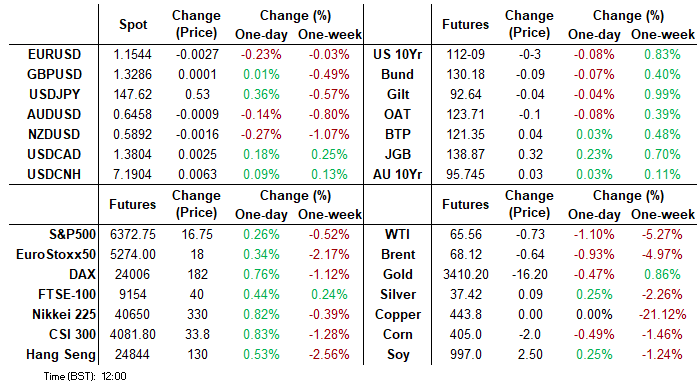

US TSYS: Modestly Lower But Rangebound, ISM Services And 3Y Supply In Focus

- Treasuries are modestly lower across the curve but continue to hold a relatively narrow range seen since Friday’s nonfarm payrolls and less so ISM manufacturing reports were digested.

- Moves have been aided by equity futures consolidating yesterday's strong gains.

- Today’s focus should be on ISM services with sensitivity to further downside surprises whilst 3Y supply will be watched closely. There’s little scheduled for President Trump today, signing an executive order at 1600ET, but markets will be on watch for any potential contenders for Fed Governor Kugler’s position and the new BLS commissioner.

- Cash yields are 1.5-2.5bp higher on the day, with increases led by the front end.

- 2Y yields, currently at 3.6996%, appear to have found some support at 3.65% in the post-payrolls period, with a low of 3.655% with Monday’s Asia open. They last traded below this level in late April/very early May.

- TYU5 trades at 112-09 (-03), easing back from an overnight high for a second day running albeit at a slower pace today. Cumulative volumes are low at 230k.

- The latest high of 112-15+ more comfortably cleared resistance at a bull trigger of 112-12+ (Jul 1 high) and briefly 112-15 (61.8% retrace of Apr 7-11 sell-off). A firmer break could open 112-23 (May 1 high).

- Data: Trade balance Jun (0830ET), S&P Global US serv/comp PMI Jul final (0945ET), ISM services Jul (1000ET)

- Fedspeak: None scheduled

- Coupon issuance: US Tsy $58B 3Y Note auction - 91282CNU1 (1300ET)

- Bill issuance: US Tsy $85B 6W & $50B 52W bill auctions (1130ET)

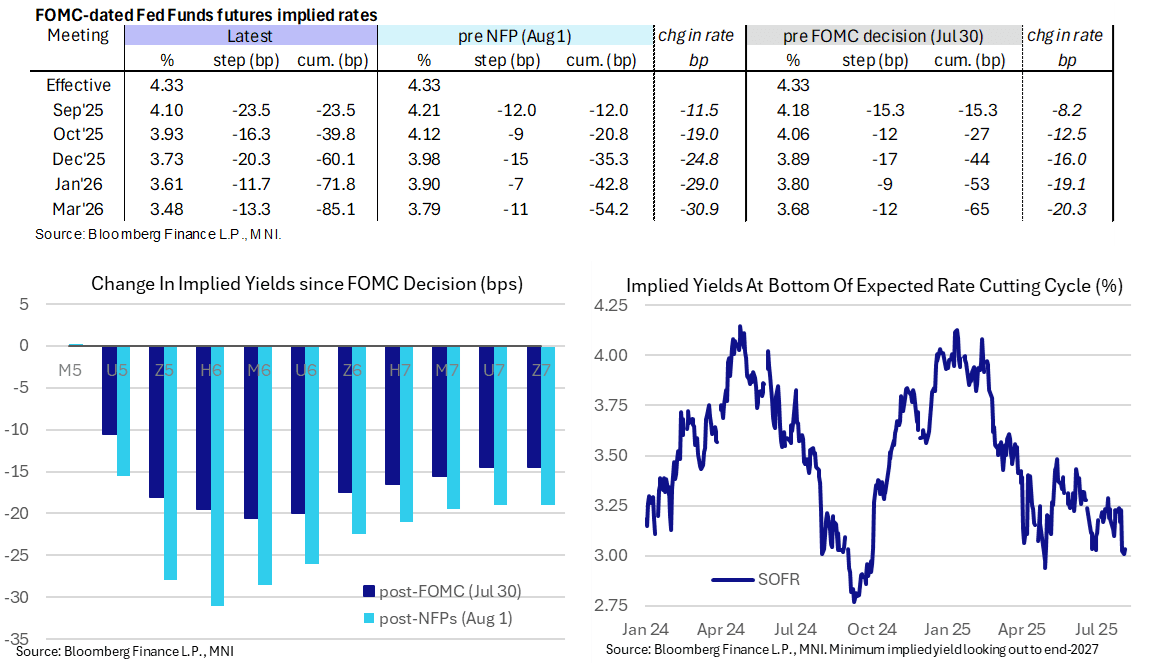

STIR: September Fed Cut Close To Fully Priced, ISM Services Headlines

- Fed Funds implied rates are 1.5-3bp higher on the day for nearer-term meetings having lifted off lows seen after a more dovish take from SF Fed’s Daly (non-voter) late yesterday to Reuters vs Friday’s more patient tone of Bostic and Hammack.

- They still hold all of Friday’s large dovish shift on the weak payrolls report and the helping hand from soft ISM mfg, with a cut close to being fully priced for the next meeting in September.

- Cumulative cuts from 4.33% effective: 23.5bp Sep (vs 12bp pre-NFP), 40bp Oct, 60bp Dec (vs 35bp), 72bp Jan and 85bp Mar.

- The SOFR implied terminal yield of 3.035% (SFRH7) is 2.5bp higher from yesterday’s lowest close since late April, still eyeing more than five cuts from current levels.

- Today sees main macro focus on ISM services plus any indication of potential contenders in for Fed Governor Kugler’s position and the new BLS commissioner.

- Daly said “I was willing to wait another cycle, but I can’t wait forever” [on rate cut prospects]. She still sees the two rate cuts pencilled in for this year as “an appropriate amount of recalibration”. “We of course could do fewer than two (rate cuts) if inflation picks up and spills over or if the labor market springs back”. However, “I think the more likely thing is that we might have to do more than two...we also should be prepared in my judgment to do more if the labor market looks to be entering that period of weakness and we still haven’t seen spillovers to inflation”

FOREX: Tech Focus: USD Index at Key Inflection Point

The USD Index remains in a bear cycle and in July pierced a key long-term support at 96.55 - a trendline drawn from the May 2011 low. Trend signals highlight a number of important technical conditions.

- On a monthly, weekly and daily scale, an oversold condition has been highlighted .

- This does not mean that a trendline break (if confirmed) isn’t important and that the downtrend cannot extend.

- However, the oversold position does raise the possibility that either; a correction unfolds soon, or that the pace of the trend slows down.

- As is always the case in such situations, the momentum/oversold position is merely a warning sign for chartists. A reversal signal in price is required to highlight a base.

- July could prove to be a key month. Based on the close, a bullish engulfing candle pattern has developed.

- This is regarded as a strong reversal signal and the fact that it has occurred at the trendline, strengthens the importance of the pattern.

- Furthermore, it also suggests that the daily, weekly and monthly time scales are in sync - a bullish signal.

- Key support is at the July low of 96.38 and this price point represents an important pivot point.

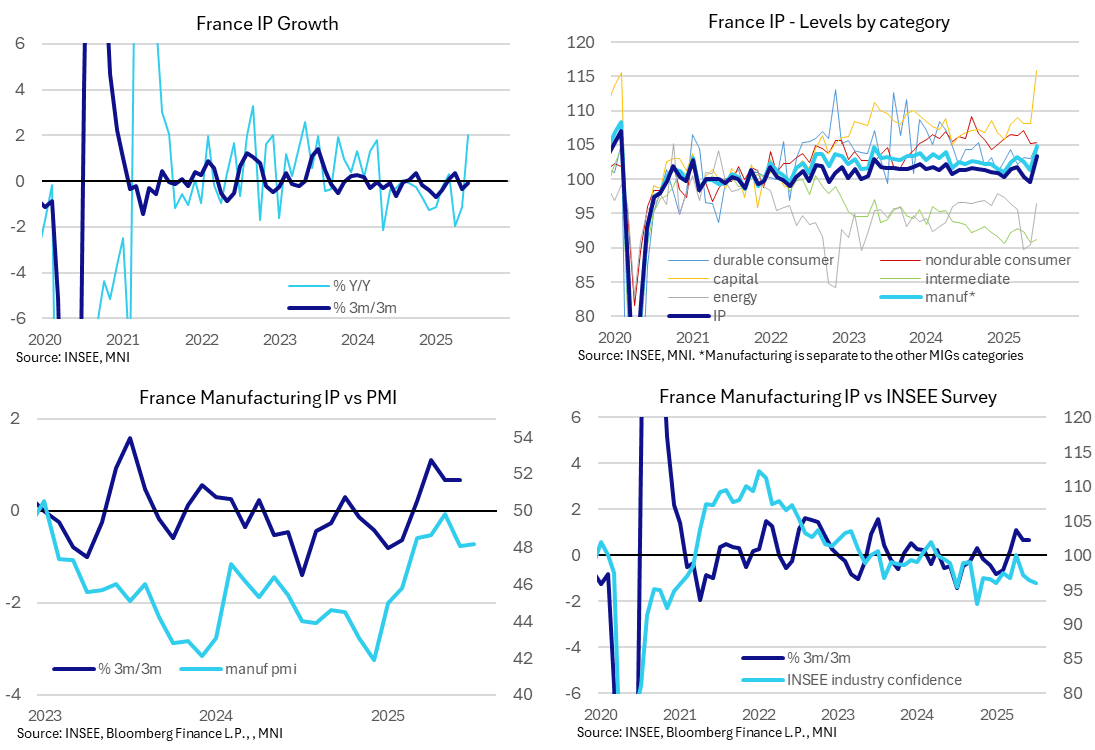

FRANCE DATA: June IP Surge At Least Partially Due To One-Offs; Weak Outlook

French industrial production was far stronger than expected in June as it surged 3.8% M/M driven in large part but not entirely by catch-up in aeronautical and space construction. Despite that jump, IP fell -0.1% Q/Q in Q2 after 0.1% in Q1 (admittedly with manufacturing at a stronger 0.7% Q/Q) and industrial indicators look soft ahead.

- IP surprisingly surged 3.8% M/M in June (cons 0.6) after -0.7% M/M in May (revised from -0.5%) and a heavy -1.4% M/M in April.

- It came as manufacturing production jumped 3.5% M/M in June (cons 1.2) after -1.2% in May along with a helping hand from the remaining category of "mining & quarrying, energy, water supply and waste management" (about 18% of total IP) rising 5.0% M/M after 1.7% in May.

- Explaining the former the press release added "The exceptional increase in [the transport] sector was mainly driven by the manufacture of "other transport equipment" (aircraft, shipbuilding, rail, etc.) " (+26.7% after +1.8%), and more specifically by aeronautical and space construction. This is explained by a catch-up over the month of delays accumulated over the quarter and the lifting of constraints on supply chains for certain companies in this sector".

- As such, manufacturing of transport surged 16.6% M/M after 0.3% but the separate category of manufacturing of machinery & equipment goods also increased a strong 4.2% M/M after -1.0% so it wasn't in isolation.

- For a slightly broader take, the alternate classification of capital goods production increased 7.2% M/M for its largest monthly increase since July 2020.

- Highlighting the weak backdrop seen in previous months, despite this (presumably largely one-off) strength in June, IP still fell -0.1% Q/Q non-annualised in Q2 after 0.1% in Q1. Manufacturing was at least stronger at 0.7% in Q2 after 0.2% in Q1.

- It clearly sees production heading into Q3 on better momentum, depending on the extent of the payback seen in July, although broader manufacturing prospects don't appear optimistic. The INSEE manufacturing confidence indicator fell for a third consecutive month to 96.0 in July and the manufacturing PMI was roughly unchanged at 48.2. The press release for the latter noted: "the lack of movement in the headline index masked a host of adverse signals seen in the survey's sub-indices. Most notable was a sharp and accelerated drop in new orders".

- A reminder when it comes to French IP however that France has the lowest industry share of GVA amongst the big five Eurozone countries. The 14% in 2024 compared with 23% in Germany (highest) and 19% in Italy (second highest).

HONG KONG: Interbank Liquidity More Than Halved, But No Relief for HKD

- USD/HKD underwent a now-usual phase of sales at the local open in price action reminiscent of HKMA HKD buying (unlike other phases of USD/HKD downside e.g. On Jul28, which did not match the pattern of intervention).

- As such, a further step lower of ~HKD 6.5bln in the HKMA Aggregate Balance is expected this week, pressing interbank liquidity down to HKD72.5bln and closer to the pre-HKD rout levels of early May (circa HKD 45bln). This leaves interbank liquidity at less than half the prevailing level in May - however there has been minimal relief in USD/HKD spot which, again, is pressuring 7.85.

- Persistent HKD pressure comes as the carry trade dynamics remain highly favourable: overnight and one-week HKD swap rates remain heavily supressed (0.35% and 0.31$ respectively) which is limiting the advance in HIBOR (1m has failed to rise materially above 1%) and, in turn, keeping long USD/HKD a favourable carry trade.

- This leaves a material lag between falling interbank liquidity, the side effect of higher local rates, and a stronger spot HKD. Low demand for HK securities and still-low levels of corporate activity are largely responsible here - meaning narrowing US-HK rate spreads via Fed easing will likely be required to pull USD/HKD lower barring a material improvement in the HK IPO pipeline.

SWITZERLAND: Keller-Sutter To Visit US In Effort To Avoid 39% Tariffs

The Swiss gov't has confirmed president of the Swiss Confederation, Karin Keller-Sutter, will travel to Washington, D.C., today (5 August) to discuss the 39% tariff rate imposed as part of US President Donald Trump's 'reciprocal' tariffs. Says the "aim is to present the US with [a] more attractive offer to reduce the level of additional tariffs on Swiss exports".

- Keller-Sutter has come in for significant domestic criticism for her percieved failures in negotiating a trade deal with the US. The FT reports that the President of the Swiss Confederation, "is accused of grossly miscalculating the trade deal she thought she was able to secure with the Trump administration. [...] “It’s knives out,” a former Swiss diplomat said. Late on Thursday, Keller-Sutter held a “disastrous” phone call with Donald Trump, according to multiple people familiar with the situation."

- Keller-Sutter is one of seven on the Federal Council, which sits as the cabinet and a collective head of government and state. The president does not hold any more powers than the other councillors, only chairing meetings and is a 'first among equals'. This means that she will not travel to the US as the head of the Swiss gov't or state, but as the Federal Councillor responsible for the Federal Department of Finance.

- Inter-industry spats have developed, with exporters hit by tariffs criticising the sizeable pharmaceutical industry (not currently subject to tariffs). FT reports "watchmaker Breitling’s chief executive Georges Kern said his country was being “held hostage” by the pharmaceutical industry".

US-RUSSIA: Kremlin Raises Stakes As Nuclear-Capable Missiles Sent To NATO Border

Military tensions between Russia and the US continue to escalate ahead of the 8 August deadline for Russia to agree a ceasefire in Ukraine. Over the weekend, President Donald Trump redeployed nuclear submarines in the context of perceived verbal threats from National Security Council Deputy Chair Dmitry Medvedev. Following this, Kremlin spox Peskov says that Russia "considers itself entitled to take any appropriate measures to deploy intermediate- and shorter-range missiles (INF); it is now not limited in any way."

- The Russian Foreign Ministry announced on 4 July that it would no longer abide by the provisions of the defunct Intermediate-Range Nuclear Forces (INF) Treaty. Trump pulled out of the INF Treaty in 2019, claiming persistent breaches by Russia, mirroring those first made by the Obama administration in 2014 following the annexation of Crimea.

- On 1 August, President Vladimir Putin confirmed the nuclear-capable Oreshnik intermediate-range ballistic missile had entered service (it is widely assumed to have already been used in a strike on the Ukrainian city of Dnipro in November 2024) and would be deployed in Belarus, which borders three NATO member states.

- As NYT reports, "The announced collapse of the I.N.F. Treaty and tensions with Russia over Ukraine have raised worries in the West of a return to a dangerous Cold War-style arms race, in which extremely fast Russian missiles armed with nuclear weapons could reach European capitals in a matter of minutes, with little warning or ability to mount a defense."

FOREX: USD Index Awaiting Directional Input from Trump's Appointments

- Markets are in consolidation mode Tuesday, with the USD Index holding well above the weekly low. Focus for markets near-term is on the trajectory of the USD from here: whether the USD shift lower on NFP is the start of a resumption of the YTD downtrend, or a corrective pullback as part of the recovery off the oversold condition. This leaves Trump's appointments at both the BLS and Fed this week in sharper focus - as he's expected to appoint a governor to replace Kugler that favours his preference for lower policy rates, as well as a BLS head willing to look into Trump's concerns over government data.

- As a result, the key parameters for the USD Index remain unchanged: the 50-dma undercuts as support at 98.293, while 99.241 marks the 50% retracement for the NFP downleg.

- CHF remains a currency of concern as the Swiss-US governments are yet to reach a broader trade agreement after the installation of 39% tariffs on Swiss exports to the US. The Swiss Franc is among the poorest performers in G10 for a second consecutive day despite yesterday's firmer-than-expected Swiss July CPI print. While USDCHF continues to hover around its 0.8092 50-dma, Franc weakness arguably stands out the most against the Japanese Yen, with CHFJPY losses over the last three sessions exceeding 2.1%.

- A swift tariff resolution here is expected to prove CHF positive - but for now, notable tariff premia holds over the currency.

- The session ahead sees ISM Services Index data - currently expected to rise to 51.5 from 50.8 prior, although prices paid is seen moderating slightly. US and Canadian trade balance stats also cross.

OPTIONS: Expiries for Aug05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1425(E1.6bln), $1.1450-56(E574mln), $1.1500(E1.4bln), $1.1550(E2.3bln), $1.1585-00(E3.2bln), $1.1650-60(E784mln)

- USD/JPY: Y146.00($611mln), Y147.45-53($630mln), Y148.00($558mln)

- GBP/USD: $1.3330-60(Gbp1.0bln), $1.3390(Gbp643mln)

- EUR/GBP: Gbp0.8650-70(E1.3bln)

- AUD/USD: $0.6465-80(A$1.2bln)

- USD/CAD: C$1.3850($601mln)

EQUITIES: EStoxx 50 More Stable After Breaking Bear Trigger

- E-mini S&P sold off sharply Friday on the back of the soft NFP print - pushing prices through mid-July lows in the process. This puts price well clear of support at the 20-day EMA, at 6329.81, signaling scope for a deeper retracement.

- The trend condition in Eurostoxx 50 futures faltered Friday, with short-term weakness resulting in a break of the bear trigger. Having shown below 5194.00, the Jun 23 low, the April 30 hi/lo range at 5078-5138 becomes the area of downside interest.

COMMODITIES: WTI Futures Sold for Third Consecutive Session into Monday Close

- WTI futures fell for a third session into the Monday close, keeping S/T momentum pointed lower. Support to watch remains the 50-day EMA, at $65.48. The average has been pierced, a clear break of it would expose $58.17, the May 30 low.

- Gold benefited from the soft NFP print on Friday, returning prices toward the top-end of the recent range. This supports the view that short-term weakness is corrective - for now - and a bull cycle that started Jun 30 remains intact.

| Date | GMT/Local | Impact | Country | Event |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 05/08/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 05/08/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 05/08/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 05/08/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 05/08/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 06/08/2025 | 2330/0830 | ** | average wages (p) | |

| 06/08/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 06/08/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/08/2025 | 0800/1000 | * | Industrial Production | |

| 06/08/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/08/2025 | 0900/1100 | ** | Retail Sales | |

| 06/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 06/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 06/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 06/08/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 06/08/2025 | 1800/1400 | Boston Fed's Susan Collins | ||

| 06/08/2025 | 1800/1400 | Fed Governor Lisa Cook | ||

| 06/08/2025 | 1910/1510 | San Francisco Fed's Mary Daly |