MNI US MARKETS ANALYSIS - Hawk Fed Cut Exp, Rates Vol Extends

Highlights:

- Hawkish cut expected from Fed, Powell presser watched carefully

- Bear cycle in Treasuries extends amid ongoing vol in European rates

- USDJPY rally moderates on approach into resistance

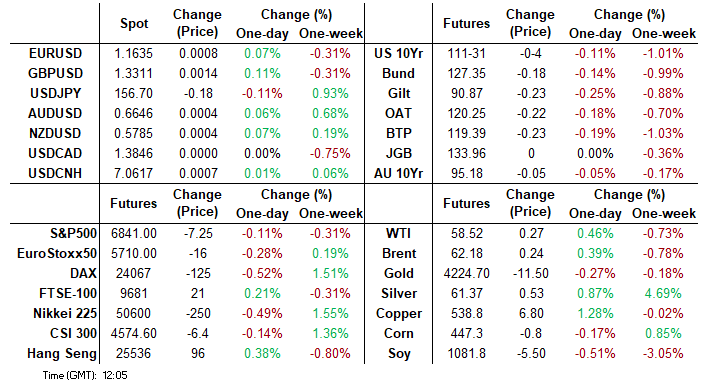

US TSYS: Bear Cycle Extends With Fed In Spotlight

Treasuries are off lows that were inspired by earlier EGB pressure but have still broadly extended a bear cycle that has seen a number of steps lower. Today’s focus is squarely on the FOMC decision, SEP and Powell’s press conference whilst data is headlined by the delayed ECI for Q3.

- Cash yields are 0.3-1.1bp higher on the day, with increases led by 5s and 7s.

- 2Y yields sit at 3.621% (+0.7bp) having earlier seen 3.625% for the highest since Nov 5, Oct 30 and before that late September.

- 5s30s have slowly extended a sizeable flattening since mid-last week, at 101.3bp vs a fresh two and a half month high of 111bp on Dec 3.

- TYH6 trades at 111-31 (-04) off an earlier latest low 111-29, on reasonable cumulative volumes of 290k for an overnight session ahead of a FOMC decision.

- It has previously cleared an important short-term support at 112-07 (Nov 5 low) and opened 111-19/111-11 (Fibo projections of Oct 17-Nov5-25 price swing) after which lies the round 111-00. In the event the SEP and Powell fail to meet hawkish expectations, resistance meanwhile is seen at 112-10+ (Nov 20 low) before 112-25+ (20-day EMA).

- FOMC decision + SEP (1400ET), Powell press conference (1430ET)

- Data: Weekly MBA mortgage data (0700ET), Employment Cost Index Q3 (0830ET – shutdown catch-up), Monthly Treasury Statement (1400ET)

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump participates in roundtable (1400ET), Trump greets pastors (1700ET)

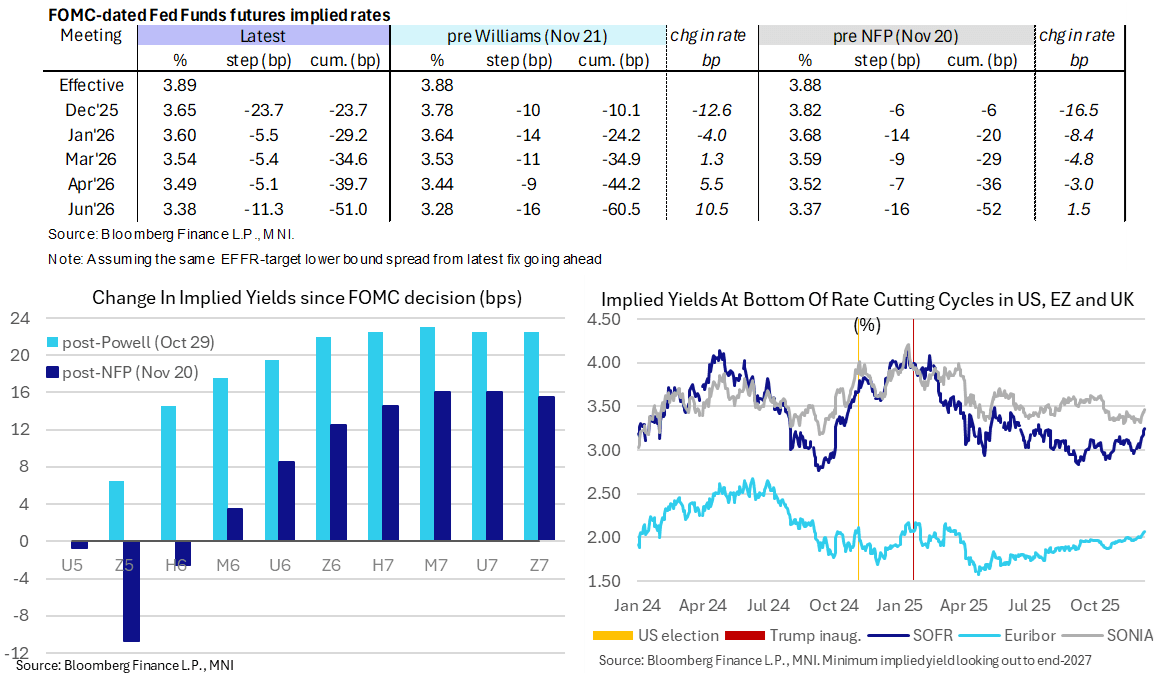

STIR: Hawkish Fed Cut Priced, Highest Terminal Since June

- Fed Funds implied rates for meetings out to mid-2026 hold their hawkish tilt seen yesterday with surprisingly strong JOLTS job openings despite some softer details such as the quits rate in particular.

- Whilst a 25bp cut today is seen as extremely likely, the next fully priced cut doesn’t come until June under a new Fed Chair.

- The FT reported Trump will soon launch a final round of interviews for Fed Chair, pitting NEC’s Hassett against a trio of other candidates. He’s still a firm favorite in betting markets although the 70% on Polymarket currently shows as the lowest since Nov 30.

- Cumulative cuts from 3.89% effective: 23.5bp Dec, 29bp Jan, 34.5bp Mar, 39.5bp Apr and 51bp Jun.

- SOFR futures have modestly extended recent declines however, following European rates on the day, with losses of up to -0.025 in late 2027 contracts.

- It sees a terminal implied yield of 3.245% (Z6/H7) for ~25bp higher than lows after NY Fed Williams’ unusual guidance on a near-term cut. This last sustainably closed higher in June, leaving an already hawkish backdrop ahead of Powell’s press conference.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Dec2025_With_Analysts_4d5a318a2b.pdf

CENTRAL BANK PREVIEWS

MNI FED PREVIEW: Winter of Discontent

The FOMC is expected to look through the data fog and deliver a “hawkish cut” on December 10, with a third consecutive 25bp reduction in the Fed funds rate range to 3.50-3.75%. While a December cut is over 90% priced, a follow-up cut in January is seen as having under 30% probability, and the next easing is only fully priced by next June. There will be the usual attention on the Summary of Economic Projections including the Dot Plot, but more attention than usual on the Statement to see how resolutely the easing bias remains.

MNI BOC PREVIEW: Firm Hold, But Hike Talk Picking Up

The Bank of Canada’s easing cycle looks to be at an end, with markets overwhelmingly expecting a rate hold in December through the subsequent 4 meetings to mid-2026. Firmer-than-expected macroeconomic data since the October meeting has fuelled speculation that the BOC’s next move will be a hike and not a cut, with a 25bp increase fully priced by Q4 2026. With incoming data catching all observers off guard, it leaves open the possibility that the BOC could sound a little more cautious about its current rate stance than it did at the previous meeting, though MNI Markets (and consensus) expects the overall message to remain the same.

MNI SNB PREVIEW: Likely to Remain Neutral

The SNB are expected to keep policy rates unchanged at 0.00%, with a cut back into negative territory highly improbable given inflation has remained within the SNB’s defined range of price stability since June. The rate outlook is likely to continue to be characterized by a high bar to further cuts, with focus on any messaging on how far the Bank are from such a move given inflation undershot the latest Q4 forecasts by almost 0.3pp

MNI BCB PREVIEW: Guidance Focus as Policy Shift Nears

The Copom is widely expected to leave the Selic rate unchanged at 15.00% for a fourth successive meeting on Wednesday, as it remains cautious amid unanchored inflation expectations. However, the very restrictive stance appears to be having the desired effect, with inflation and inflation expectations now declining and economic activity softening. As such, focus will be on the forward guidance and any signals that the Copom is opening the door to a rate cut early next year.

MNI CBRT PREVIEW: Size of Cut in Question

Analysts are split on whether the CBRT will cut the one-week repo rate by another 100bps at its final meeting of the year or accelerate the easing pace to 150bps. Despite a significant downside surprise to headline CPI in November, underlying indicators and consumer inflation expectations remain at uncomfortable levels, which may justify keeping the rate cut pace unchanged at 100bp/meeting, particularly as repricing effects and minimum wage negotiations add uncertainty to the outlook for inflation for 2026.

SOFR: Short Setting & Long Cover Seen In Futures On Tuesday

OI data suggests that net short setting dominated through the reds as SOFR futures sold off on Tuesday, before a better mix of short setting and long cover was seen in the greens and long cover dominated in the whites.

- Firmer-than-expected JOLTS job openings data drove much of the hawkish move, although the finer details of the release were softer than the headline reading.

| 09-Dec-25 | 08-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,304,279 | 1,298,677 | +5,602 | Whites | +35,190 |

SFRZ5 | 1,609,323 | 1,584,259 | +25,064 | Reds | +36,511 |

SFRH6 | 1,462,042 | 1,439,357 | +22,685 | Greens | +3,190 |

SFRM6 | 1,113,193 | 1,131,354 | -18,161 | Blues | -19,522 |

SFRU6 | 1,094,579 | 1,082,871 | +11,708 |

|

|

SFRZ6 | 1,131,495 | 1,122,066 | +9,429 |

|

|

SFRH7 | 853,243 | 842,651 | +10,592 |

|

|

SFRM7 | 781,292 | 776,510 | +4,782 |

|

|

SFRU7 | 813,697 | 800,035 | +13,662 |

|

|

SFRZ7 | 833,822 | 837,578 | -3,756 |

|

|

SFRH8 | 437,073 | 441,870 | -4,797 |

|

|

SFRM8 | 397,615 | 399,534 | -1,919 |

|

|

SFRU8 | 371,275 | 380,247 | -8,972 |

|

|

SFRZ8 | 327,808 | 331,093 | -3,285 |

|

|

SFRH9 | 191,324 | 196,071 | -4,747 |

|

|

SFRM9 | 208,323 | 210,841 | -2,518 |

|

|

UK FISCAL: Reeves: "I reserve the right to be able to take action at any point"

Reeves asked if headroom was lower by e.g. GBP5bln or GBP10bln in the Spring, would that be enough to mean more fiscal measures need to be taken in the Spring?

She avoids the question and then when pushed to ask says "I reserve the right to be able to take action at any point. But I believe the headroom that we have and the changes that we've made means that I won't need to do that in the spring. But of course, I reserve the right at any time to take action."

ECB: Lagarde Suggests Growth Projections Will Be Upgraded In Dec

ECB President Lagarde is speaking to Martin Wolf of the FT. The topic of the discussion is "What are the futures of the euro and the dollar as global currencies, and what are the opportunities for the digital euro?"

Initial headlines give an early insight into the December macroeconomic projections, set to be released next Thursday:

- "*LAGARDE: GROWTH PROJECTIONS ARE LIKELY TO BE REVISED HIGHER" Bloomberg

- "ECB'S LAGARDE: WE REMAIN IN A GOOD PLACE" - Reuters

Asked about French President Macron's suggestion for the ECB to add growth and employment considerations into its mandate (alongside suggestions that policy can be "significantly adjusted today"), she suggests focus should remain on enhancing the single market.

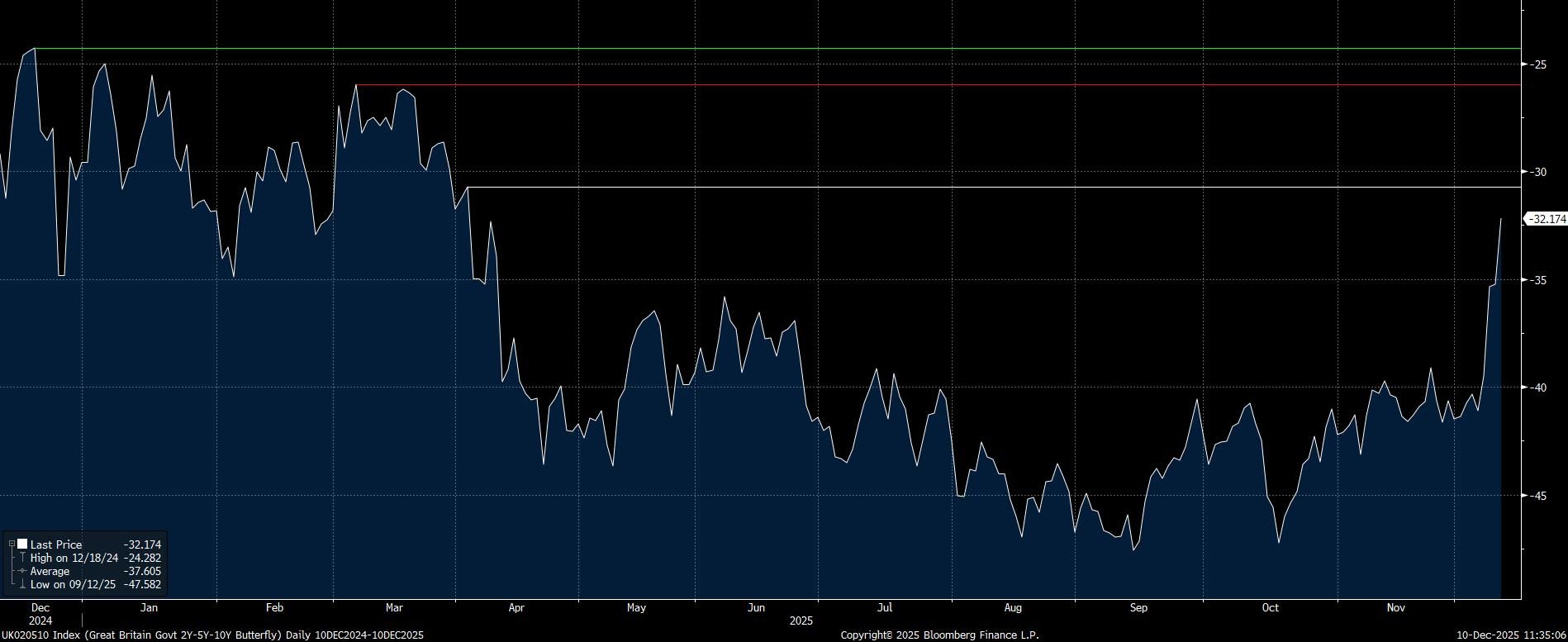

GILTS: 2s5s10s Fly Nears Early April Highs

The hawkish repricing derived from moves on the EUR strip has led to the belly selling off on the 2-/5-/10-Year gilt butterfly.

- Markets give greater consideration to the timing of the end of the BoE’s easing cycle, as well as any spillover from a potential hiking cycle at the ECB.

- Underperformance of the belly of the fly is further underpinned by the market continuing to price another ~50bp of BoE rate cuts and ongoing skew away from long end issuance by the DMO.

- 5s have cheapened by nearly 10bp on the structure month-to-date, with the next upside level of note located less than 2bp away at April’s closing high (-30.73bp).

- BMO note that “yields are still much more expensive on the fly than at the end of past rate cut cycles”, suggesting that 5s could cheapen by at least another 30bp on the structure as “the rate cycle reaches its trough”.

Fig. 1: UK 2-/5-/10-Year Butterfly (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

FOREX: USDJPY Momentum Stalls Short Of 157.00 Handle Ahead Of FOMC

- USDJPY momentum stalled on the run-up to 156.95 yesterday, as a EUR-led phase of USD selling across early Europe contained any broader dollar rally. Downward pressure on the JPY continues to be a focus this week, amid the hawkish repricing for core fixed income markets and regional geopolitical uncertainty taking its toll. Key resistance for USDJPY remains at 157.89, the Nov 20 high and bull trigger. Despite a slightly weaker risk backdrop today, cross/JPY remains a notable beneficiary of the overall dynamics.

- The next key driver for the greenback will be today's FOMC, with more attention than usual on the Statement to see how resolute any remaining easing bias is. Forward guidance is likely to be amended to reflect a more patient stance on cuts. As such, the market reaction to the meeting could hinge on how Chair Powell portrays the burden of proof for further easing ahead.

- EURUSD meanwhile has seen an 1.1658 overnight high before this morning’s ECBspeak reaffirmed the idea that the Governing Council deems rates to be “in a good place”, despite Executive Board member Schnabel expressing her comfort with markets pricing the next rate move as a hike earlier in the week.

- Initial resistance comes in at the 50% retracement of the Sep17-Nov 5 bear leg (1.1694), while support is located at the 20-day EMA intersecting at 1.1607. A French Gov't spokesperson acknowledged this morning the 2026 budget may not pass by year-end in the country - further pessimism here despite yesterday's narrow passage of the Social Security Financing Bill would pressure EUR from here.

- Weekly MBA mortgage applications and the Q3 employment cost index are on the calendar ahead of the FOMC. Australian labour market data is scheduled overnight.

OPTIONS: Expiries for Dec10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1580-81(E1.7bln), $1.1610(E779mln), $1.1650-60(E1.5bln), $1.1800(E1.7bln)

- USD/JPY: Y156.00($901mln)

- GBP/USD: $1.3300(Gbp540mln)

- AUD/USD: $0.6600(A$822mln)

- NZD/USD: $0.5700(N$558mln)

- USD/CAD: C$1.3800($520mln)

- USD/CNY: Cny7.1088($1.2bln)

EQUITIES: Bull Cycle in E-Mini S&P Intact, Contract Still Above 20-, 50-Day EMAs

- A bull cycle in Eurostoxx 50 futures remains intact and the contract is trading closer to its recent highs. Price has cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. Sights are on 5742.40 next (pierced), 76.4% of the Nov 13 - 21 bear leg. A clear breach of this price point would pave the way for an extension towards 5825.00, the Nov 13 high and a key resistance. First key support to watch lies at 5629.92, the 50-day EMA.

- A bull cycle in S&P E-Minis remains intact and price continues to trade above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6807.02, the 20-day EMA.

COMMODITIES: Gold in Consolidation Mode, Trend Remains Bullish Overall

- Short-term gains in WTI futures appear corrective - for now - and a bear threat remains present. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A stronger resumption of the bear leg would open key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high.

- Gold is in consolidation mode. The trend condition is unchanged, the set-up remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4044.0. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 10/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 10/12/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 10/12/2025 | 1330/0830 | *** | Employment Cost Index | |

| 10/12/2025 | 1445/0945 | *** | Bank of Canada Policy Decision | |

| 10/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/12/2025 | 1530/1030 | BOC press conference | ||

| 10/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 10/12/2025 | 1900/1400 | ** | Treasury Budget | |

| 10/12/2025 | 1900/1400 | *** | FOMC Statement | |

| 10/12/2025 | 1930/1430 | Fed Chair Powell Press Conference | ||

| 11/12/2025 | - | Swiss National Bank Meeting | ||

| 11/12/2025 | 0001/0001 | * | RICS House Prices | |

| 11/12/2025 | 0030/1130 | *** | Labor Force Survey | |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0830/0930 | *** | SNB Interest Rate Decision | |

| 11/12/2025 | 0950/0950 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 11/12/2025 | 1000/1000 | BOE Bailey Gives Evidence At Covid-19 Inquiry | ||

| 11/12/2025 | 1100/0600 | *** | Turkey Benchmark Rate | |

| 11/12/2025 | - | *** | Money Supply | |

| 11/12/2025 | - | *** | Social Financing | |

| 11/12/2025 | - | *** | New Loans | |

| 11/12/2025 | - | ECB Lagarde and Cipollone at Eurogroup Meeting | ||

| 11/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 11/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 11/12/2025 | 1330/0830 | * | Household debt-to-income | |

| 11/12/2025 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1500/1000 | * | Services Revenues | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 11/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/12/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond |