US TSYS: Bear Cycle Extends With Fed In Spotlight

Dec-10 11:53

Treasuries are off lows that were inspired by earlier EGB pressure but have still broadly extended a bear cycle that has seen a number of steps lower. Today’s focus is squarely on the FOMC decision, SEP and Powell’s press conference whilst data is headlined by the delayed ECI for Q3.

- Cash yields are 0.3-1.1bp higher on the day, with increases led by 5s and 7s.

- 2Y yields sit at 3.621% (+0.7bp) having earlier seen 3.625% for the highest since Nov 5, Oct 30 and before that late September.

- 5s30s have slowly extended a sizeable flattening since mid-last week, at 101.3bp vs a fresh two and a half month high of 111bp on Dec 3.

- TYH6 trades at 111-31 (-04) off an earlier latest low 111-29, on reasonable cumulative volumes of 290k for an overnight session ahead of a FOMC decision.

- It has previously cleared an important short-term support at 112-07 (Nov 5 low) and opened 111-19/111-11 (Fibo projections of Oct 17-Nov5-25 price swing) after which lies the round 111-00. In the event the SEP and Powell fail to meet hawkish expectations, resistance meanwhile is seen at 112-10+ (Nov 20 low) before 112-25+ (20-day EMA).

- FOMC decision + SEP (1400ET), Powell press conference (1430ET)

- Data: Weekly MBA mortgage data (0700ET), Employment Cost Index Q3 (0830ET – shutdown catch-up), Monthly Treasury Statement (1400ET)

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump participates in roundtable (1400ET), Trump greets pastors (1700ET)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Lower On Shutdown Hopes, Front-Loaded Supply Headlines Docket

Nov-10 11:53

- Treasuries have pared losses but still sit comfortably lower on the day in response to improved odds of the government shutdown ending after eight centrist Democrats on Sunday voted with Republicans on a new CR to fund the US government through Jan 30.

- Today’s docket focus should be on front-loaded supply ahead of Veterans Day tomorrow, with a 3Y auction along with heavy bill issuance.

- Cash yields are 2.4-3.3bp higher on the day, with increases slightly led by the belly possibly ahead of that 3Y supply.

- TYZ5 trades at 112-20 (-07+) off an earlier low of 112-15 on reasonable overnight volumes nearing 340k.

- Resistance is seen at Friday’s joint high of 113-02 (Nov 5 & 7 highs, a key level), but a bear threat is still present at 112-06 (Sep 25 low) before which lies 112-09+ (Nov 5 high) and other various support levels.

- Data: No releases of note.

- Fedspeak: Daly on Bloomberg TV (0830ET), Musalem on Bloomberg TV (0945ET)

- Coupon issuance: US $58B 3Y Note Auction - 91282CPK1 (1300ET). Last month’s 3Y auction stopped through by 0.8bp although saw both the bid to cover and indirect take receded.

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET) and $95B 6W bill (1300ET)

- Politics: Trump in bilateral meeting with President of Syria (1100ET), Trump participates in swearing-in ceremony for Ambassador to Republic of India (1500ET)

OUTLOOK: Price Signal Summary - USDJPY Trend Needle Points North

Nov-10 11:38

- In FX, EURUSD has recovered from its recent lows. The move higher, for now, appears corrective. A short-term recovery is allowing a recent oversold condition to unwind. Resistance to watch is the 20-day EMA, at 1.1587. It has been pierced, a clear break of it would signal scope for an extension towards the 50-day EMA, at 1.1627. The trend remains bearish. A reversal would refocus attention on the bear trigger at 1.1469, the Nov 5 low.

- A bear trend in GBPUSD remains intact and the latest recovery appears corrective. The move higher is allowing an oversold trend condition to unwind. Firm short-term resistance to watch is at the 20-day EMA, at 1.3237. A break of this hurdle would signal scope for an extension towards the 50-day EMA, at 1.3340. A resumption of the downtrend would pave the way for an extension towards 1.2971. The bear trigger is 1.3010, the Nov 4 and 5 low.

- The trend structure in USDJPY is unchanged, it remains bullish and the latest shallow pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 154.48, the Nov 4 high. A break of this level would confirm a resumption of the uptrend and open 154.80, the Feb 12 high. First important support to watch lies at 152.46, the 20-day EMA.

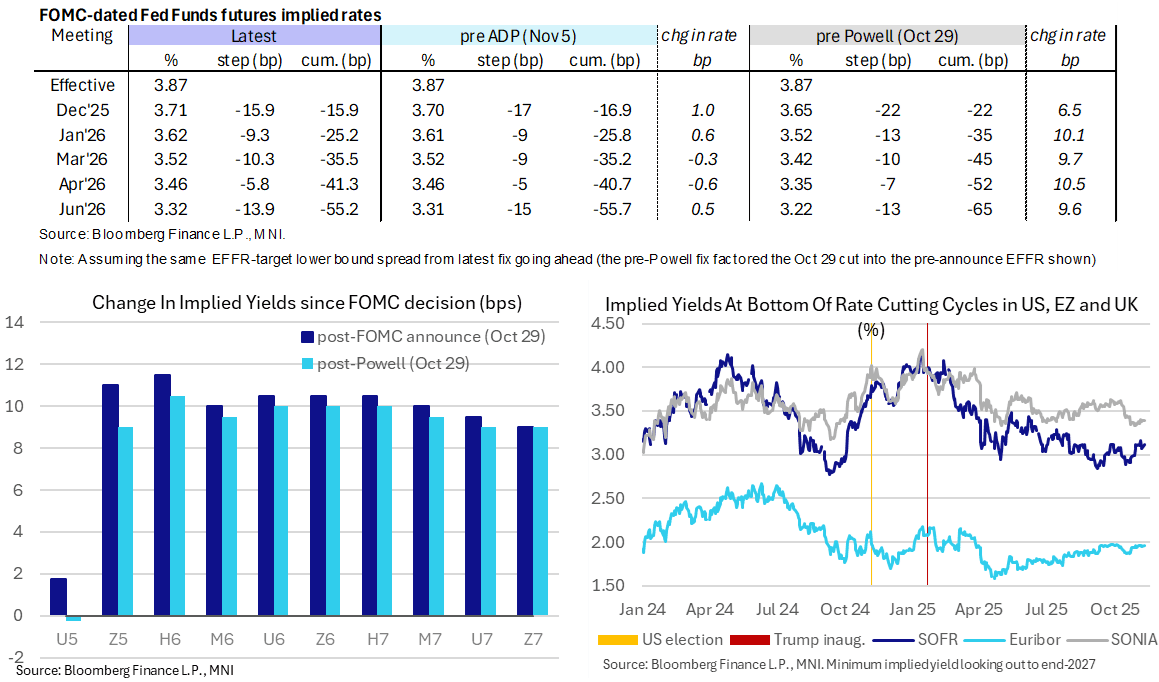

STIR: Fed Rate Path Buoyed By Improved Shutdown Ending Odds

Nov-10 11:37

- Fed Funds implied rates are a modest 0.5-1.5bp higher for meetings out to mid-2026, helped by a marked improvement in odds of the government shutdown ending.

- Cumulative cuts from 3.87% effective: 16bp Dec, 25bp Jan, 35.5bp Mar, 41.5bp Apr, 55bp Jun.

- SOFR futures see larger moves, up to 4.5 ticks lower through 2027 contracts.

- It sees the terminal yield higher at 3.12% (H7) but still off Wednesday’s 3.16% marked the highest close since late July, following beats for ADP and ISM services before weaker alternate labor data and consumer sentiment over Thu-Fri.

- We don’t expect today’s Fedspeak to move the needle having heard from both recently.

- 0830ET - SF Fed’s Daly (non-voter, leaning dove) on Bloomberg TV. She’s spoken a few times since the Oct 29 FOMC, including in a blog post this morning firming her dovish leaning stance.

- 0945ET - St Louis Fed’s Musalem (’25 voter, hawk) on Bloomberg TV. He said on Nov 6 that policy is getting close to neutral and that the Fed needs to lean against above-target inflation. The labor market is around full employment but there are some downside risks to it.