MNI US MARKETS ANALYSIS - GBP Rallies on Early Budget Details

Highlights:

- Early touted release of OBR estimates see UK with larger headroom than expected

- GBP, Gilts briefly rally into Reeves' presentation

- Jobless claims, MNI Chicago PMI the data focus

US TSYS: TYH6 Key Resistance Eyed, Jobless Claims & Earlier Auctions Headline

Treasuries continue to see impact from yesterday’s bull flattening on Bloomberg sources seeing Hassett as a frontrunner for the next Fed Chair role. There have recently been short-lived intraday gains in spillover from Gilts ahead of the UK budget, back to small losses on the day supported by stronger risk sentiment.

- Thanksgiving schedule. Cash and futures full session today, cash closed & future early close on Thursday, cash & futures early close on Friday.

- Note the earlier auction timings ahead of the Thanksgiving holiday - see below.

- Cash yields are 0.1-0.7bp higher, led by the belly with today's 7Y supply possibly in mind.

- TYH6 trades at 113-18+ (-00+) off yesterday’s latest highs of 113-22+ on solid cumulative volumes of 320k, still boosted by the roll but with it nearing completion.

- Yesterday’s climb saw it step closer to latest resistance at 113-23 (Oct 23 high), increasingly eyeing a key resistance at 113-29+ (Oct 17 high).

- Data: MBA mortgages (0700ET), Weekly jobless claims (0830ET), Durable goods Sep prelim (0830ET), MNI Chicago PMI Nov (0945ET), Dallas Fed weekly economic index (1130ET)

- Fedspeak: Fed Beige Book (1400ET)

- Coupon issuance: US Tsy $44B 7Y Note - 91282CPM7 (1130ET). Yesterday's 5Y tailed slightly by 0.2bp although bid-to-cover increased from 2.38 to 2.41 whilst last month's 7Y auction saw its largest tail in over a year.

- Bill issuance: US Tsy $100B 4W & $85B 8W bill auctions (1000ET), $69B 17W bill auctions (1130ET)

- Politics: No public events scheduled for Trump

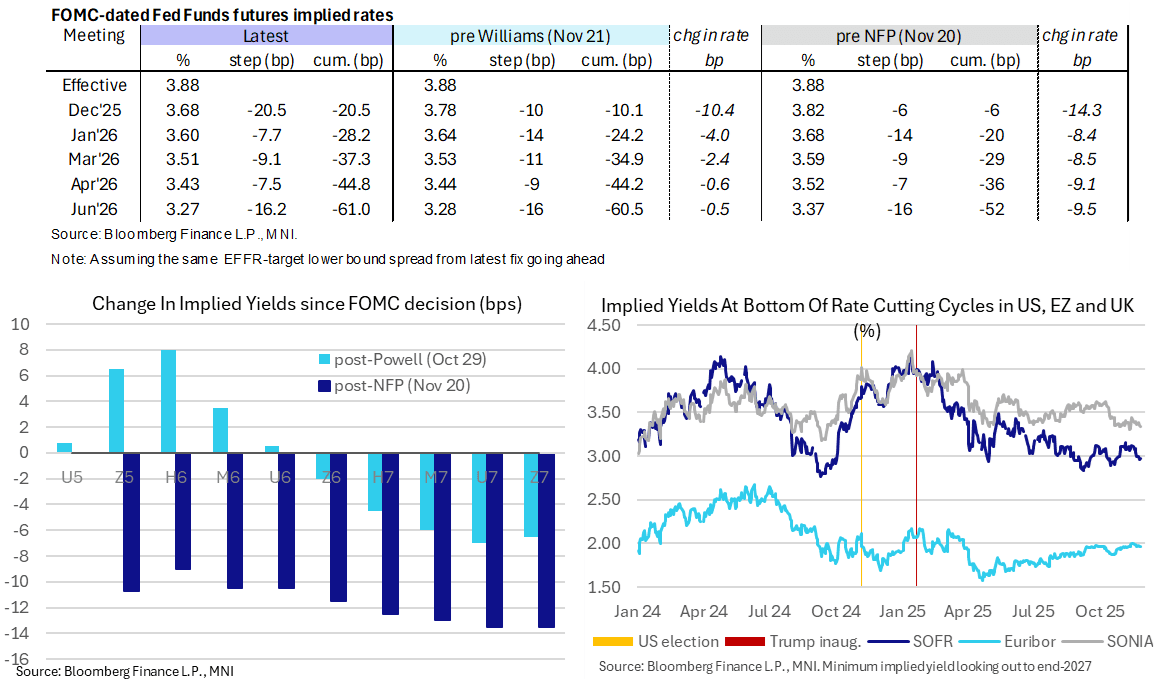

STIR: Hassett Rally Partly Pared, Pre-Thanksgiving Claims Data In First Focus

- US rates have given back some of yesterday’s rally for 2026/27 contracts although the impact still holds from NEC’s Hassett being reiterated as frontrunner for Fed Chair considerations (per Bloomberg sources) as we draw nearer to an expected announcement before Christmas.

- Fed Funds implied rates are near unchanged on the day ahead of a data-focused docket, including weekly jobless claims brought forward for Thanksgiving.

- Cumulative cuts from 3.88% effective: 20.5bp Dec, 28bp Jan, 36.5bp Mar, 45bp Apr and 61bp Jun.

- SOFR futures are flat to -0.02, with the terminal implied yield at 2.975% (H7) +1.5bp from yesterday’s fresh lowest close since the days ahead of the hawkish Oct 29 FOMC press conference.

- There’s no Fedspeak scheduled today but the Fed’s Beige Book should be watched for latest liaison survey findings. The October Beige Book noted weaker economic activity and a still subdued labor market although price descriptions were arguably the most inflationary Beige Book of 2025, certainly joint with June which saw 8 (of 12) districts characterize inflation pressures as "moderate".

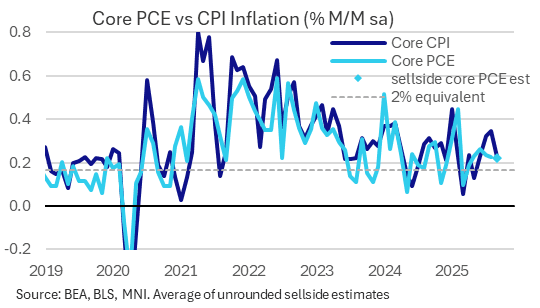

US OUTLOOK/OPINION: Core PCE Tracking Raises Likelihood Of Lower FOMC Forecast

- Updating latest core PCE estimates for September after yesterday’s PPI report, we now track a median of 0.22% M/M vs 0.25% pre-PPI and closer to 0.30% pre-CPI.

- This September release won’t come until Friday, Dec 5. There seems to be some confusion over the October PCE report, originally scheduled for today, but it’s currently without a release date and we’re not sure how it can be calculated if BLS isn’t publishing an October CPI report.

- A range of core PCE estimates: 0.20 (JPM), 0.21% (Nomura and TD Securities), 0.22% (GS), 0.23% (Barclays and MS).

- These estimates point to a similar pace to the 0.23% M/M in August as well as the 0.24% averaged through May-July. Morgan Stanley see scope for a +1bp revision to Aug and +1.5bp for Jul.

- Assuming no revisions for simplicity here, a 0.22% M/M increase would continue to imply an above target run rate at 2.8% annualized in latest three months or 2.85% Y/Y, although it would help stop any further increases in the Y/Y after 2.9% in Aug. It starts to make it more likely we’ll see downward revisions to the FOMC median core PCE forecast of 3.1% Y/Y in 4Q25 with next month’s revised SEP.

- As for more detailed estimates, core services ex-housing (supercore) inflation is seen at 0.26% M/M by Nomura and 0.28% by MS for a still robust pace after the 0.33% averaged in Jul-Aug.

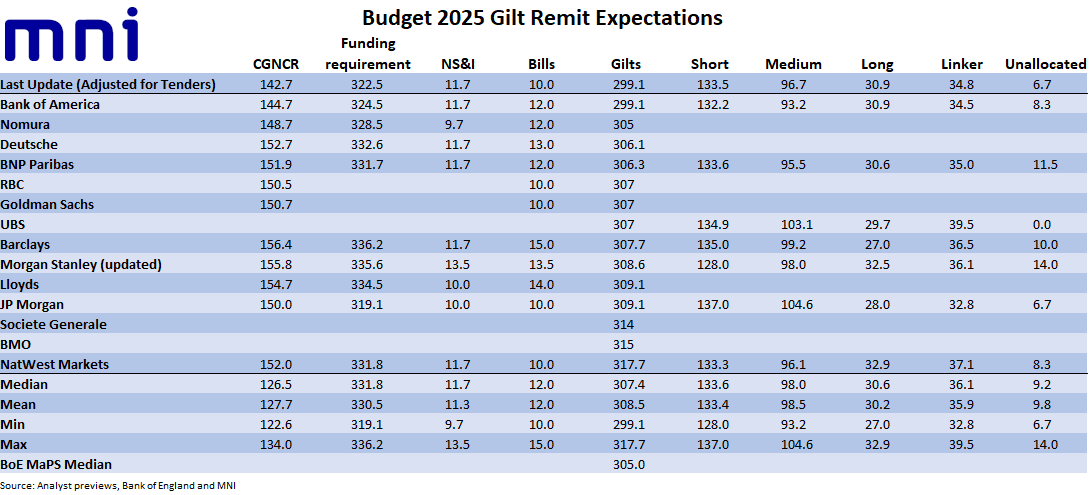

UK FISCAL: Market reactions to the remit and consultation agenda (1/2)

A reminder that our full Budget Preview is here (from Friday) and that on Monday we set out 5 things to watch for the Budget market reaction here.

- We think that there will likely be market moves on a remit larger than GBP320bln or smaller than GBP295bln - but moves on remit announcements smaller than that will be more dependant upon what Reeves has said before and whether the market has already reacted, as well as the amount of headroom and CGNCR revisions through to 2030.

- The median expectation for the remit is an increase of around GBP8bln to GBP307bln with a GBP2bln extra in the UKTB net target to an increase of GBP12bln. These will both be announced with the main remit that will be announced as Chancellor Rachel Reeves ends her speech. See the table below for an updated sell-side expectations table.

- Also announced with the main remit will be the updated bucket breakdown, including planned number of syndications in each budget and planned number of auctions in each bucket.

- As things stand there is one remaining syndication in each of the medium, long and linker buckets. There are 25 planned short auctions (8 remaining, 6 in FQ4), 19 medium (6 remaining, 5 in FQ4), 10 longs (3 remaining, all in FQ4) and 15 linker auctions (5 remaining, 4 in FQ4).

UK FISCAL: Market reactions to the remit and consultation agenda (2/2)

- We think there is a good chance that the long-dated syndication is cancelled, which would result in the size of the long-dated bucket being reduced, particularly as some auctions may also be cancelled. The initial reaction to this may be a flattening of the curve.

- However, this may be somewhat nuanced. The DMO consultation agenda (published later at 15:30GMT) normally includes some guidance on any new gilts under consideration for the upcoming quarter (FQ4, Jan-Mar) as well as some thoughts on the syndications. Regarding the syndications, the DMO can either leave options open or lead with a relatively strong view on what the most likely gilt is.

- The Jan-41 gilt could be sold via syndication in either the long-dated bucket (if sold in January) or the medium-dated bucket (if sold in Feb/Mar).

- If this we have had a long syndication cancelled but it is hinted as that the Jan-41 gilt is the likely choice in the consultation agenda for a medium syndication, some of the flattening of the curve in the 10-15 area may be reversed.

- Equally, if the long syndication isn't cancelled and then a new green is proposed in the long bucket with the Jan-41 gilt in the medium bucket, this may lead to some steepening of the curve (particularly 10s20s assuming the new green gilt has a maturity around the 18-20 year area).

- If we don't get a new 10-year gilt launch via syndication in March, we think that there is a good chance we still see a syndication, but in April instead (hence slipping into the next fiscal year). And hence, we don't think 10-year supply over the next 6 months will be hugely impacted by today's announcement.

- In terms of how FX reacts to these announcements, we think FX as a whole will probably be led by gilt futures. Smaller compositional changes and curve moves might not be so relevant here, but a bit steepening of the curve and material moves in gilt futures could drive the currency. Moves in the front-end (more likely driven by the policies outlined, particularly how disinflationary they are) are likely to be a bigger driver of FX overall, however.

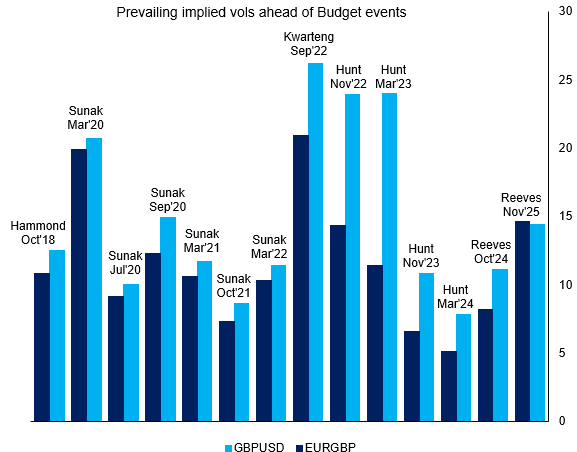

GBP: Notable Two-Way GBP Risk Today; Vols Well Elevated

- GBPUSD still sees notable two-way risk headed into today's Budget - despite trickling details of policy measures across the UK press this morning. This week's spot recovery works against the bearish trend theme, which would resume on a break below 1.3010, the Nov 4 / 5 low, but we also see positioning dynamics possibly creating room for a GBP squeeze, raising the risk of a short squeeze given the amount of Budget scrutiny the currency has been under this month.

- The front-end of the vol curve remains well elevated in anticipation of the Budget. An overnight GBPUSD straddle breaks-even on a ~90 pip swing, close to double the running YTD average, indicating greater expectations of intraday vol across the Budget today.

- Compared to previous Budgets, markets are clearly cautious of not being caught offguard with market vol as was the case in 2024 - however vol gauges are still more moderate when compared to Budget events in 2022, 2023 - and in particular the Truss-Kwarteng mini-Budget 3 years ago (see below).

We still see scope for market surprises, with key uncertainties remaining over headline changes in tax, disinflationary measures, fiscal headroom and scope for Gilt sales (see more here: https://www.mnimarkets.com/articles/five-factors-that-will-drive-the-budget-market-reaction-12-1763984878006 ).

- Chancellor Reeves is due to start to deliver her speech today starting around 12:30GMT (normally a couple of minutes late). During the speech she will announce the policy changes and the headline OBR forecasts.

- When she has finished speaking, the full OBR forecasts (EFO: Economic and Fiscal Outlook) will be published as well as the DMO’s updated gilt remit.

- At 15:30GMT the DMO will then publish its consultation agenda for the FQ4 (Jan-Mar) investor / GEMM meetings.

- The meetings will then be held on Monday 1 December before the full calendar for the remainder of the fiscal year is published on Friday 5 December.

FOREX: NZD Outperforms Post RBNZ, Two-Sided Risks For GBP Into Budget

- NZD is the outperformer today after RBNZ guidance amid their 25bp cut signals a likely hold through H1 next year. This led NZDUSD to see session highs of 0.5697, breaking above its 20-day EMA. This signals scope for a stronger recovery to 0.5725, which represents both the 50-day and prior trendline support turned resistance. 0.5800 remains a key medium-term pivot.

- AUDNZD meanwhile saw downside following the RBNZ meeting, despite the new monthly Australian CPI coming in firmer than expected. The cross overnight saw its lowest levels this month at 1.1407, with the 50-day EMA providing initial support at 1.1391.

- Dollar weakness and further hawkish BOJ reports promoted USDJPY to print a 155.65 pullback low overnight. With dips remaining very well supported, the pair has firmed since, recovering to 156.40 at typing. A break above the 157.89 November 20 high would signal scope for an extension of the current uptrend.

- GBPUSD still sees notable two-way risk headed into today's Budget - despite trickling details of policy measures across the UK press this morning. This week's spot recovery works against the bearish trend theme, which would resume on a break below 1.3010, the Nov 4 / 5 low, but we also see positioning dynamics possibly creating room for a GBP squeeze, raising the risk of a stronger recovery given the amount of Budget scrutiny the currency has been under this month.

- We still see scope for market surprises, with key uncertainties remaining over headline changes in tax, disinflationary measures, fiscal headroom and scope for Gilt sales. Key resistance meanwhile stands at 1.3261, the 50-day EMA. A clear break of this hurdle would highlight a potential reversal.

- Aside from the UK budget, US MBA mortgage applications, weekly claims, September durable goods orders, MNI Chicago PMI, and the Fed Beige Book are on the calendar.

OPTIONS: Expiries for Nov26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1480-00(E2.4bln), $1.1525(E1.0bln), $1.1565(E685mln), $1.1595-00(E1.7bln), $1.1650(E721mln)

- USD/JPY: Y153.00($1.2bln), Y154.00($2.1bln), Y155.00($1.9bln), Y156.00($977mln), Y157.00($941mln)

- AUD/USD: $0.6450(A$1.1bln), $0.6535(A$1.7bln)

- NZD/USD: $0.5670-75(N$1.2bln)

- USD/CAD: C$1.3990-00($1.1bln), C$1.4085-00($1.5bln), C$1.4170($525mln)

- USD/CNY: Cny7.00($1.3bln)

EQUITIES: E-Mini S&P Extends Recovery From Nov 21 Low

- A bearish theme in Eurostoxx 50 futures remains present following recent weakness. However, the contract has traded above the 50-day EMA, at 5595.08, and pierced the 20-day EMA, at 5620.85. A clear break of both averages would highlight a possible reversal and signal scope for a stronger recovery. This would open 5691.30, a Fibonacci retracement point. Key short-term support and the bear trigger is at 5475.00, the Nov 21 low.

- S&P E-Minis are trading higher as the contract extends the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a climb towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support has been defined at 6525.00, the Nov 21 low.

COMMODITIES: WTI Futures Bear Trigger in Focus Following Recent Weakness

- Recent weakness in WTI futures highlights a bearish theme. A stronger resumption of the bear leg would pave the way for a move towards key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- The trend condition in Gold remains bullish and the bear phase between Oct 20 and 28 appears to have been a correction. This allowed a recent overbought condition to unwind. Key support to watch lies at the 50-day EMA, at $3966.8. Clearance of this EMA would signal scope for a deeper retracement. The first short-term bull trigger has been defined at $4245.23, the Nov 13 high.

| Date | GMT/Local | Impact | Country | Event |

| 26/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 26/11/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 26/11/2025 | 1230/1230 | Chancellor Reeves to deliver UK Budget | ||

| 26/11/2025 | 1330/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 26/11/2025 | 1442/0942 | *** | MNI Chicago PMI | |

| 26/11/2025 | 1500/1000 | * | US Bill 08 Week Treasury Auction Result | |

| 26/11/2025 | 1500/1000 | ** | US Bill 04 Week Treasury Auction Result | |

| 26/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 26/11/2025 | 1530/1530 | DMO to publish consultation agenda | ||

| 26/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 26/11/2025 | 1605/1705 | ECB Lane Fireside Chat on Macro Outlook | ||

| 26/11/2025 | 1630/1130 | ** | US Treasury Auction Result for 7 Year Note | |

| 26/11/2025 | 1700/1200 | ** | Natural Gas Stocks | |

| 26/11/2025 | 1700/1800 | ECB Lagarde Acceptance Speech | ||

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1900/1400 | Fed Beige Book | ||

| 27/11/2025 | 0030/1130 | * | Private New Capex and Expected Expenditure | |

| 27/11/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 27/11/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 27/11/2025 | 0830/0930 | ECB Cipollone Remarks at Euro Cyber Resilience Board | ||

| 27/11/2025 | 0900/1000 | ** | M3 | |

| 27/11/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 27/11/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 27/11/2025 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 27/11/2025 | 1100/1200 | ECB de Guindos Remarks at CEDE Congress of Executives | ||

| 27/11/2025 | 1330/0830 | * | Current account | |

| 27/11/2025 | 1330/0830 | * | Payroll employment | |

| 27/11/2025 | 1630/1630 | BOE Greene Speech at Goodbody Conference | ||

| 28/11/2025 | 2330/0830 | ** | Tokyo CPI | |

| 28/11/2025 | 2330/0830 | * | Labor Force Survey | |

| 28/11/2025 | 2350/0850 | * | Retail Sales (p) | |

| 28/11/2025 | 2350/0850 | ** | Industrial Production |