UK FISCAL: Market reactions to the remit and consultation agenda (1/2)

A reminder that our full Budget Preview is here (from Friday) and that on Monday we set out 5 things to watch for the Budget market reaction here.

- We think that there will likely be market moves on a remit larger than GBP320bln or smaller than GBP295bln - but moves on remit announcements smaller than that will be more dependant upon what Reeves has said before and whether the market has already reacted, as well as the amount of headroom and CGNCR revisions through to 2030.

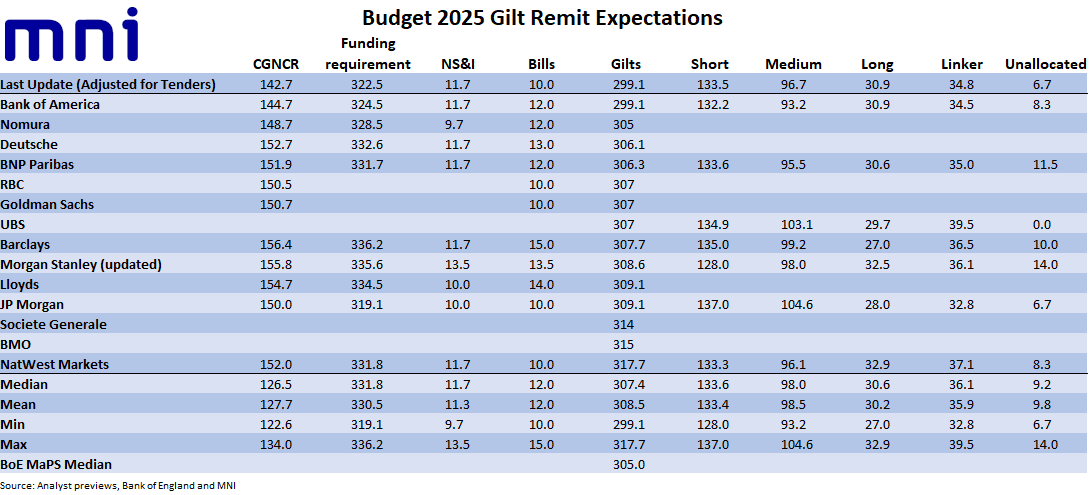

- The median expectation for the remit is an increase of around GBP8bln to GBP307bln with a GBP2bln extra in the UKTB net target to an increase of GBP12bln. These will both be announced with the main remit that will be announced as Chancellor Rachel Reeves ends her speech. See the table below for an updated sell-side expectations table.

- Also announced with the main remit will be the updated bucket breakdown, including planned number of syndications in each budget and planned number of auctions in each bucket.

- As things stand there is one remaining syndication in each of the medium, long and linker buckets. There are 25 planned short auctions (8 remaining, 6 in FQ4), 19 medium (6 remaining, 5 in FQ4), 10 longs (3 remaining, all in FQ4) and 15 linker auctions (5 remaining, 4 in FQ4).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUR: FX Exchange traded Option

EURUSD (7th Nov) 1.1600p, sold at 0.0020 in ~1.2k.

SONIA OPTIONS: Call Spread seller

SFIZ5 96.35/96.60cs,sold at 1.5 in 3k.

FRANCE: No Impact From Moody's Outlook Downgrade, But Budget Negotiations A Risk

Moody’s downgraded France’s outlook to Negative from Stable on Friday, but it’s not had any market impact. At least an outlook downgrade was likely, and there may instead be some relief that an outright downgrade to A1 was avoided. Ongoing budget negotiations remain the focus for OATs this week, with PM Lecornu having to tread a fine line to maintain tacit support from the Socialist and LR parties. Should his government fall to censure, it would promote a fresh widening impulse in OAT/EGB spreads.

- The 10-year OAT/Bund spread is currently 0.5bps narrower at ~80bps. The spread may struggle to meaningfully unwind political risk premium while budget negotiations are ongoing.

- Moody’s noted that “the decision to change the outlook to negative reflects rising risks of a weakening of France's institutions and governance as well as of a partial reversal of structural reforms”.

- Although avoided at the latest review, Moody’s wrote that “A downgrade of France's ratings would likely result from further evidence that the ability of the legislative institutions to effectively tackle the country's key credit challenges has durably weakened. This would likely be evidenced by continued difficulties to materially reduce the fiscal deficit and contain the expected weakening of the government's debt burden and debt affordability metrics. A lasting pause or reversal of key provisions of previous structural reforms, most notably on pensions, would also add to downward pressure on the rating.”

- After voting on other budget proposals took too long over the weekend, a vote on the Socialist’s wealth tax proposal has been delayed till later in the week. The Socialists have emphasised that taxes on rich individuals are a necessary condition for non-censorship of Lecornu’s government