MNI US MARKETS ANALYSIS: GBP & Long Gilts Lower On PSNB

Highlights:

- Broader USD adds to post-Fed recovery.

- GBP sells off & UK long end gilts struggle as PSNB data underscores fiscal challenges.

- Canadian retail sales due later, Trump-Xi call also eyed as well as post-FOMC Fedspeak & U.S. government funding matters.

US TSYS: Post-Claims Lows Mostly Hold, Fedspeak and House CR Vote Eyed

Treasuries hold close to yesterday’s jobless claims driven lows and in the case of 30s actually pushed a little through those lows but have since pared that move.

- Gilts provide some additional selling impetus after larger than expected monthly government borrowing, although have also pared losses.

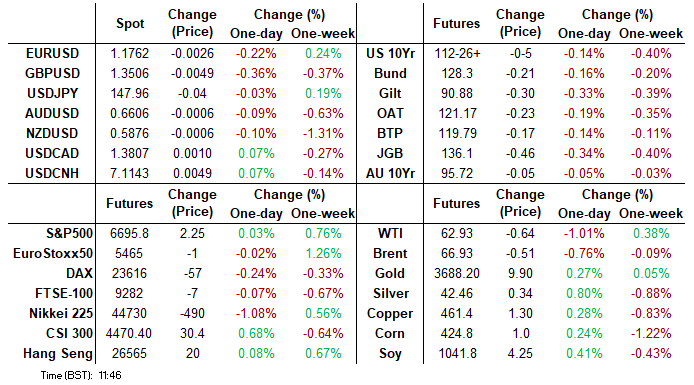

- Cash yields are 1-2bp higher across the curve. 10Y yields at 4.1255% (+2.1bp) earlier hit 4.1351% to essentially yesterday’s 4.1352%.

- TYZ5 trades at 112-26+ (-05) on thin cumulative volumes of 215k.

- Yesterday saw a low of 112-23+ (marking initial support) after initial jobless claims surprised lower despite some continued signs of Texas fraud and continuing claims fell for a fourth consecutive week for further away from cycle highs.

- With a corrective pullback in play, subsequent support could be seen at 112-15+ (Aug 5/14 high), whilst resistance remains the bull trigger at 113-29 (Sep 11 high).

- Data: No notable releases scheduled

- Fedspeak: Miran on CNBC (1100ET), Daly on fireside chat on AI (1430ET), Miran on Fox Business (1600ET) – see STIR bullet

- Politics: At 1020 ET, the House is expected to vote on a 'clean' GOP CR to extend government funding through Nov 21. Despite regular conservative criticism of CRs, the bill is expected to pass. After which, Speaker Johnson (R-LA) is likely to recess the House until after the October 1 shutdown deadline.

- Later on, Trump signs executive orders (1500ET)

US TSY FUTURES: Mix Of Net Short Setting & Long Cover Seen Thursday

OI data points to a mix of net short setting (TU & UXY) and long cover (FV, TY, US & WN) as Tsy futures settled lower on Thursday, with the curve-wide bias tilted towards the latter.

| 18-Sep-25 | 17-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,499,634 | 4,491,786 | +7,848 | +315,494 |

FV | 6,746,113 | 6,751,031 | -4,918 | -217,407 |

TY | 5,395,370 | 5,400,033 | -4,663 | -317,347 |

UXY | 2,377,569 | 2,373,523 | +4,046 | +366,994 |

US | 1,826,037 | 1,830,969 | -4,932 | -697,920 |

WN | 2,018,449 | 2,026,897 | -8,448 | -1,567,628 |

|

| Total | -11,067 | -2,117,814 |

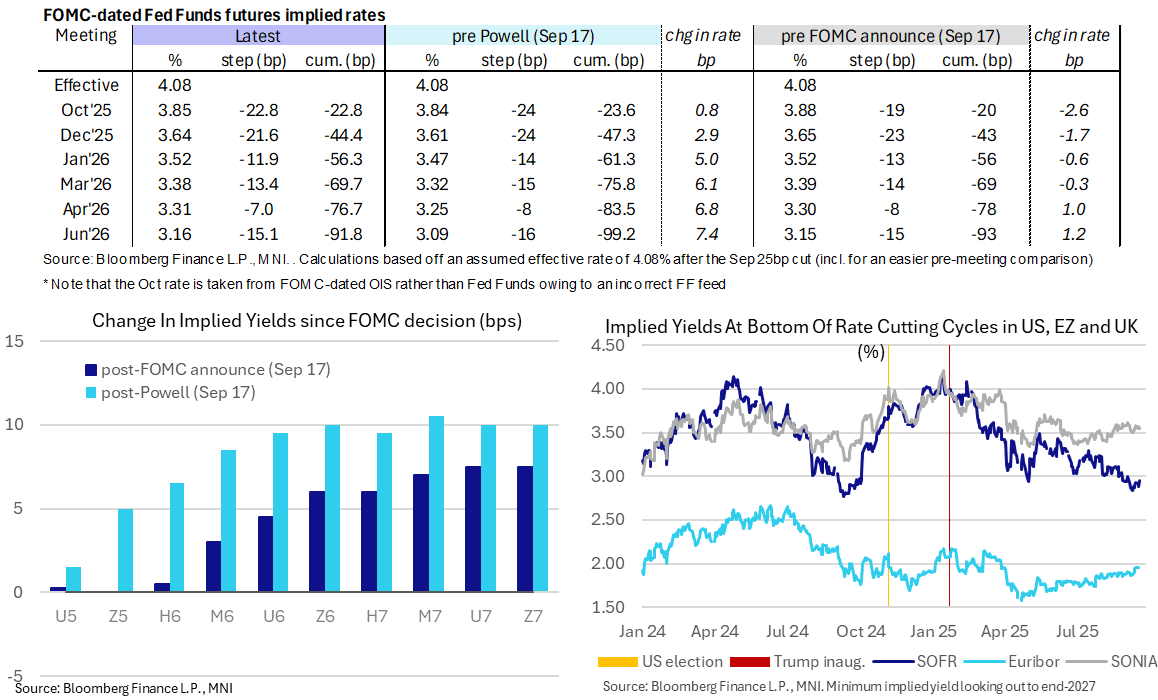

STIR: Fed Rate Path Marginally Higher Ahead Of Post-FOMC Fedspeak

Fed Funds implied rates are little changed overnight, up to 1bp higher ahead of a session where the calendar is headlined by the first post-FOMC Fedspeak.

- Cumulative cuts from 4.08% effective: 23bp Oct, 44.5bp Dec, 56.5bp Jan, 69.5bp Mar, 76.5bp Apr and 92bp Jun.

- SOFR futures are 0.5-1 ticks lower.

- The implied terminal yield of 2.99% (SFRH7) is 0.5bp higher overnight yesterday’s close was its highest since Sep 2 (weak NFP report on Sep 5), although still reasonably close to dovish extremes. It implies ~110bp of cuts ahead.

- Tradition would suggest we get CEA’s/Fed Gov Miran’s statement explaining his dissent from this week’s meeting. There’s no set time but that would usually come at some point earlier in the US morning, but if not he’s still set to appear on CNBC (1100ET) and Fox Business (1600ET).

- Miran would have preferred to cut 50bp this week (analysts expected at least a 50bp dissent) and was almost certainly the 2.9% dot for 2025 (i.e. an implied 50bp cuts at each of the Sep, Oct and Dec meetings).

- SF Fed’s Daly (non-voter) also speaks on a fireside chat about AI at 1430ET. We imagine she was one of the nine dots that made up the median 3.6% (i.e. looking for two more 25bp cuts in the two meetings left this year).

SOFR: Net Long Cover In The White Pack Dominated In Futures On Thursday

OI data points to a mix of net short setting and long cover as SOFR futures finished lower on Thursday.

- The combination of the post-FOMC decision rhetoric from Chair Powell and yesterday’s U.S. data (with most of the focus on the fall in the jobless claims data recently impacted by fraudulent dealings in Texas) was enough to drive meaningful net long cover in most of the white contracts after a build up of longs in recent weeks.

- Net pack positioning swings were a little more balanced across the remainder of the strip.

| 18-Sep-25 | 17-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,468,209 | 1,473,356 | -5,147 | Whites | -92,682 |

SFRZ5 | 1,601,199 | 1,664,992 | -63,793 | Reds | -2,263 |

SFRH6 | 1,160,097 | 1,193,117 | -33,020 | Greens | -5,518 |

SFRM6 | 1,041,763 | 1,032,485 | +9,278 | Blues | +6,956 |

SFRU6 | 940,132 | 960,409 | -20,277 |

|

|

SFRZ6 | 1,043,332 | 1,025,206 | +18,126 |

|

|

SFRH7 | 756,723 | 753,399 | +3,324 |

|

|

SFRM7 | 812,696 | 816,132 | -3,436 |

|

|

SFRU7 | 657,669 | 670,627 | -12,958 |

|

|

SFRZ7 | 709,127 | 698,830 | +10,297 |

|

|

SFRH8 | 435,277 | 439,258 | -3,981 |

|

|

SFRM8 | 357,091 | 355,967 | +1,124 |

|

|

SFRU8 | 273,047 | 271,976 | +1,071 |

|

|

SFRZ8 | 294,487 | 289,121 | +5,366 |

|

|

SFRH9 | 189,131 | 186,762 | +2,369 |

|

|

SFRM9 | 176,491 | 178,341 | -1,850 |

|

|

UK FISCAL: Timetable and economic/fiscal data included in the OBR's forecasts

Just to reiterate that we are in the 10 week countdown to the Budget (kicked off by the Chancellor announcing the date and asking the OBR to provide a forecast). There has been focus recently on the productivity targets (flagged in particular by the IFS).

- The OBR's timetable for the forecast round is set out below.

- There are three pre-measures rounds which incorporate updated economic and fiscal data and do not take into account new policies unless they have already been announced e.g. the winter fuel payments. Other policies are separately costed at first.

- The first of these forecasts will be sent to the Chancellor on Friday 3 October (in the past this has led to increased speculation around the forecasts at this time and the increased possibility of media leaks).

- The second forecast on 20 October will take into account the updated labour market data and August GDP.

- The final pre-measures round we expect to include next month's public finance data as well as September CPI and that will be presented to the Chancellor on Halloween.

- After that, the first round to incorporate proposed new measures will be on 10 November (but the November MPC decision will be past the cut off) and then the final major round will be sent to the Chancellor on Friday 21 November ahead of the Budget the following week - most proposed measures are in place by then but there is always room for last minute tweaks.

- Q2 GDP revisions: Tuesday 30 September

- Round 1 (Pre-measures): Friday 3 October

- Labour market data (including updated July AWE numbers used for pension triple lock): Tuesday 14 October

- August monthly GDP: Thursday 16 October

- Round 2 (Pre-measures): Monday 20 October

- September public finance data: Tuesday 21 October

- September CPI (which is expected by the BOE and most analysts to mark the peak and is also used for uprating most benefits): Wednesday 22 October

- Round 3 (Pre-measures): Friday 31 October

- Round 4: Monday 10 November: Round 4

- Round 5: Friday 21 November: Round 5

- Wednesday 26 November: UK Budget and OBR's EFO (Economic and Fiscal Outlook) published.

EUROPEAN ISSUANCE UPDATE

Coupon set for next week's 30-year DSL:

The DSTA has set the coupon for next week's DDA launch of the 30-year Jan-56 DSL at 3.50% (short first).

- The initial spread guidance will be released on Monday with the transaction taking place on Tuesday with books opening at 9:00BST / 10:00CET (we also usually get a preliminary initial spread guidance come out Friday afternoon).

- The ISIN will be NL0015002P70.

- The DSL will be launched for E4-5bln (we expect the top of the range) with a maturity of 15 January 2056 with the reference bond the 2.90% Aug-56 Bund.

MEF to issue new retail 7-year BTP Valore from 20-24 October:

The guaranteed minimum coupon rates for all three periods will be announced on Friday 17 October, together with the ISIN.

- "Coupons will be paid quarterly and increasing over time according to a step-up mechanism of 3+2+2 years. The extra final bonus will be 0.8% of the invested capital for investors who purchase the bond during the placement period and hold it until maturity."

- This will be the fifth BTP Valore issued (but the first of 2025) and have the longest maturity to date.

- Since launching in 2023, BTP Valore volumes have ranged from E11.2-18.3bln with maturities ranging from 4-6 years.

- So far in 2025 there have been two Italian retail offerings: the 9-year BTP Piu in February for E14.9bln and the 7-year BTP Italian in May with the retail takeup E8.8bln.

Tender details for Thursday 25 September:

The DMO has announced that it will go ahead with two lines to be sold at its tender next week and will be looking to sell:

- At 10:00BST: GBP1.25bln of the 4.50% Sep-34 Gilt (ISIN: GB00B52WS153)

- At 11:30BST: GBP750mln of the 4.75% Dec-38 Gilt (ISIN: GB00B00NY175)

FOREX: USDJPY Selloff Well Supported Post BOJ, GBP Underperforms

The dollar index trades in positive territory Friday, rising around 0.2% on the session. Broadly, the index is consolidating the solid post-Fed recovery, holding 1.4% above this week’s cycle lows. Japanese yen volatility has been notable on the session following the Bank of Japan, however, it’s GBP that is under particular pressure, after the latest round of UK PSNB data underscored the fiscal challenge that the UK faces at present.

- USDJPY traded around 80 pips lower following the BOJ’s relatively hawkish hold, as board members Naoki Tamura and Hajime Takata dissented and wanted to raise the policy rate to 0.75%. USDJPY fell to a session low of 147.20. However, with the BOJ overall keeping its cautious economic view, leaving largely unchanged its assessment of private consumption, capital investment and exports, those initial USDJPY declines were pared steadily throughout the late APAC session and into the press conference.

- The pair has since consolidated just below the 148 mark. Optimistic sentiment for the pair has been assisted by a bullish candle pattern on Wednesday - a hammer formation - providing an early reversal signal. Immediate resistance is at yesterday’s high of 148.27, and a continuation higher would open 149.14, the Sep 3 high.

- GBPUSD sits 0.38% in the red on Friday after briefly piercing back below the 1.35 mark. Recent developments show no shift in the UK’s mix of sticky inflation and fiscal worry, resulting in the potential for higher for longer interest rates, but providing a negative impact on the pound.

- Initial firm support to watch at 1.3495, the 50-day EMA, has been pierced. A sustained break would threaten the recent bullish theme. In similar vein, EURGBP is back above 0.8700, keeping bullish conditions intact for the cross. A stronger resumption of gains would open 0.8744, the Aug 7 high. Key resistance and the bull trigger is at 0.8769, the Jul 28 high.

- Canadian retail sales data for July provides the final data release for the week.

FOREX OPTIONS: Expiries for Sep19 NY cut 1000ET (Source: DTCC)

- EURUSD: 1.1700 (1.23bn), 1.1750 (1.64bn), 1.1800 (2.08bn)

- GBPUSD: 1.3525 (374mln)

- USDJPY: 147.50 (527mln), 147.55 (587mln)

- USDCAD: 1.3800 (414mln), 1.3820 (340mln), 1.3830 (269mln), 1.3850 (515mln)

- AUDUSD: 0.6600 (807mln)

- USDCNY: 7.0900 (700mln), 7.1000 (380mln)

- USDZAR: 17.4800 (349mln)

EQUITIES: S&P E-Minis Trend Needle Points North

A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high yesterday. Price has breached the 6700.00 handle and this signals scope for an extension towards 6748.50, a 1.236 projection of the Aug 1 - 15 - 20 price swing. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Initial support to watch lies at 6589.32, the 20-day EMA.

- EUROSTOXX 50 futures recently traded through resistance around the 20-day EMA - a bullish development for now - and yesterday’s rally reinforces this theme. The move signals potential for a climb towards 5525.00, the Aug 22 high and a bull trigger. On the downside, key support has been defined at 5302.00, the Sep 2 low.

COMMODITIES: Price Signal Summary - Gold Bulls Remain In The Driver's Seat

Gold remains in a clear bull cycle and short-term weakness is for now, considered corrective. A fresh all-time high, once again this week, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3705.2, a 1.382 projection of the May 15 - Jun 16 - 30 price swing. Initial firm support lies at $3566.6, the 20-day EMA.

- The trend condition in WTI futures is unchanged - a bear cycle remains intact and the latest recovery is considered corrective. The pullback from the Sep 2 high highlights a possible reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. A stronger resumption of weakness would open $57.71, the May 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 19/09/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/09/2025 | 2330/0830 | *** | CPI | |

| 19/09/2025 | 0347/1247 | *** | BOJ Policy Rate Announcement | |

| 19/09/2025 | 0600/0700 | *** | Public Sector Finances | |

| 19/09/2025 | 0600/0700 | *** | Retail Sales | |

| 19/09/2025 | 0600/0800 | ** | PPI | |

| 19/09/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 19/09/2025 | 1005/1205 | ECB Lagarde and Cipollone at Eurogroup ECOFIN Meeting | ||

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1830/1430 | San Francisco Fed's Mary Daly | ||

| 22/09/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/09/2025 | 1230/1330 | BOE Pill At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/1545 | ECB Lane At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/0945 | New York Fed's John Williams | ||

| 22/09/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 22/09/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 22/09/2025 | 1600/1200 | Cleveland Fed's Beth Hammack | ||

| 22/09/2025 | 1600/1200 | Richmond Fed's Tom Barkin | ||

| 22/09/2025 | 1715/1315 | BOC Sr Deputy speaks at LSE panel on supervision | ||

| 22/09/2025 | 1800/1900 | BOE Bailey Fireside Chat On Supervision | ||

| 22/09/2025 | 1945/1545 | BOC Deputy Kozicki speaks at BIS panel on central bank frameworks |