STIR: Fed Rate Path Marginally Higher Ahead Of Post-FOMC Fedspeak

Sep-19 10:24

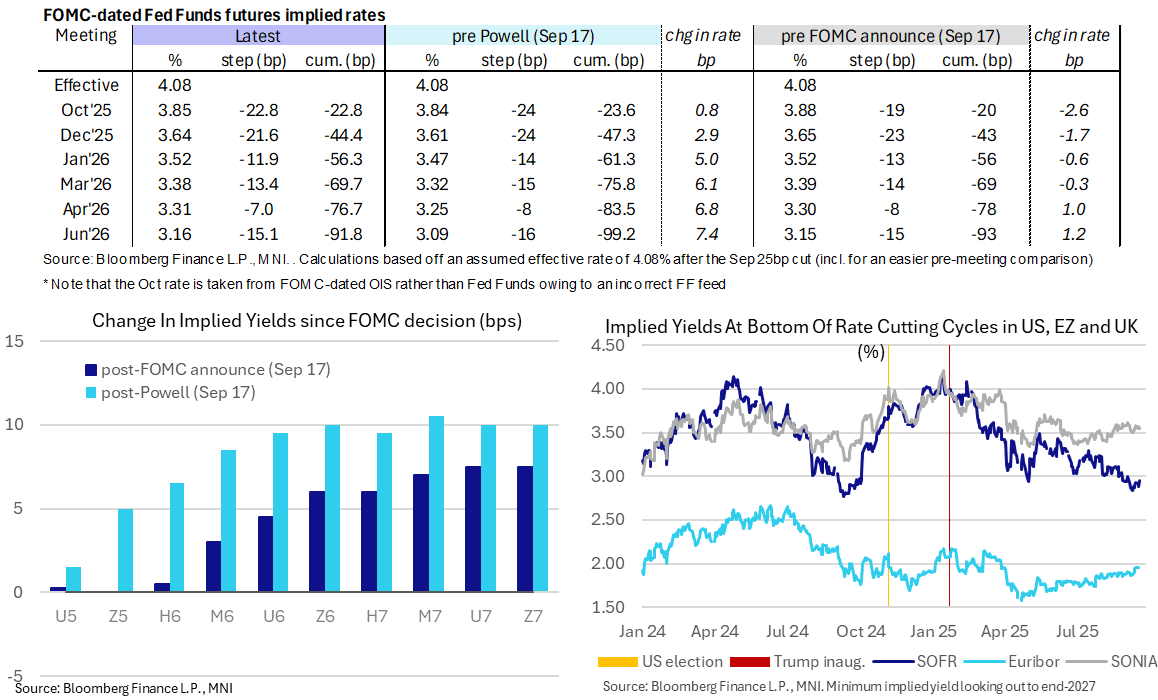

- Fed Funds implied rates are little changed overnight, up to 1bp higher ahead of a session where the calendar is headlined by the first post-FOMC Fedspeak.

- Cumulative cuts from 4.08% effective: 23bp Oct, 44.5bp Dec, 56.5bp Jan, 69.5bp Mar, 76.5bp Apr and 92bp Jun.

- SOFR futures are 0.5-1 ticks lower.

- The implied terminal yield of 2.99% (SFRH7) is 0.5bp higher overnight yesterday’s close was its highest since Sep 2 (weak NFP report on Sep 5), although still reasonably close to dovish extremes. It implies ~110bp of cuts ahead.

- Tradition would suggest we get CEA’s/Fed Gov Miran’s statement explaining his dissent from this week’s meeting. There’s no set time but that would usually come at some point earlier in the US morning, but if not he’s still set to appear on CNBC (1100ET) and Fox Business (1600ET).

- Miran would have preferred to cut 50bp this week (analysts expected at least a 50bp dissent) and was almost certainly the 2.9% dot for 2025 (i.e. an implied 50bp cuts at each of the Sep, Oct and Dec meetings).

- SF Fed’s Daly (non-voter) also speaks on a fireside chat about AI at 1430ET. We imagine she was one of the nine dots that made up the median 3.6% (i.e. looking for two more 25bp cuts in the two meetings left this year).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (U5) Outlook Remains Bullish

Aug-20 10:23

- RES 4: 113-23 76.4% retracement of the Sep’24 - Jan’25 sell-off

- RES 3: 113-07 76.4% retracement of the Apr 7 - 11 sell-off

- RES 2: 112-23 High May 1

- RES 1: 112-15+ High Aug 5 and the bull trigger

- PRICE: 111-25 @ 11:12 BST Aug 20

- SUP 1: 111-11 50-day EMA

- SUP 2: 110-23+/08+ Low Aug 1 / Low Jul 15 & 16

- SUP 3: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 4: 109-28 Low Jun 6 and 11

A bullish theme in Treasury futures remains intact. The contract continues to trade above support at the 50-day EMA, at 111-.11. A clear break of this average would expose support at 110-23+, the Aug 1 low. For bulls, a resumption of gains would refocus attention on 112-15+, the Aug 5 high and bull trigger. A break of this hurdle would resume the uptrend and pave the way for a climb towards 112-23 initially, the May 1 high.

FOREX: NZDUSD Prints Four-Month Lows Following Dovish RBNZ Cut

Aug-20 10:22

- The New Zealand dollar has been under significant pressure Wednesday, after the RBNZ committee voted to reduce the OCR by 25bps to 3.00%. There were two votes for a larger 50bp interest rate cut, representing the most fractious vote split in the MPC’s history. The dovish tilt saw NZGBs close 10-16bp richer, with OIS pricing down 14-23bp across future meetings, and 35bp of further easing priced by November.

- Kiwi weakness had been notable ahead of the decision, largely reflective of the weakness for the major equity benchmarks. NZDUSD recorded its first print below 0.5900 in two weeks, and the subsequent extension south has seen the pair trade down to a four-month low at 0.5815.

- Exponential moving average studies have moved into a bear-mode position and today’s move through the May lows bolsters the short-term bearish momentum. The 50% and 61.8% retracements of the April-July price swing are the next notable support levels, located at 0.5803 and 0.5728 respectively.

- In the crosses, AUDNZD has broken a number of daily highs just below the psychological 1.10 mark, rising to an intra-day high of 1.1069 and the highest level since early March. Further strength would place the focus back on key medium-term resistance between 1.1175/80.

- Following the upside surprise for UK inflation data, GBPNZD has surged 1.2%, briefly extending the bounce from the July lows to 4.25%. Price action for the cross has significantly narrowed the gap to the blowout highs from April this year, located around 2.3350. Downtrend resistance from the 2015 highs comes in just below this level.

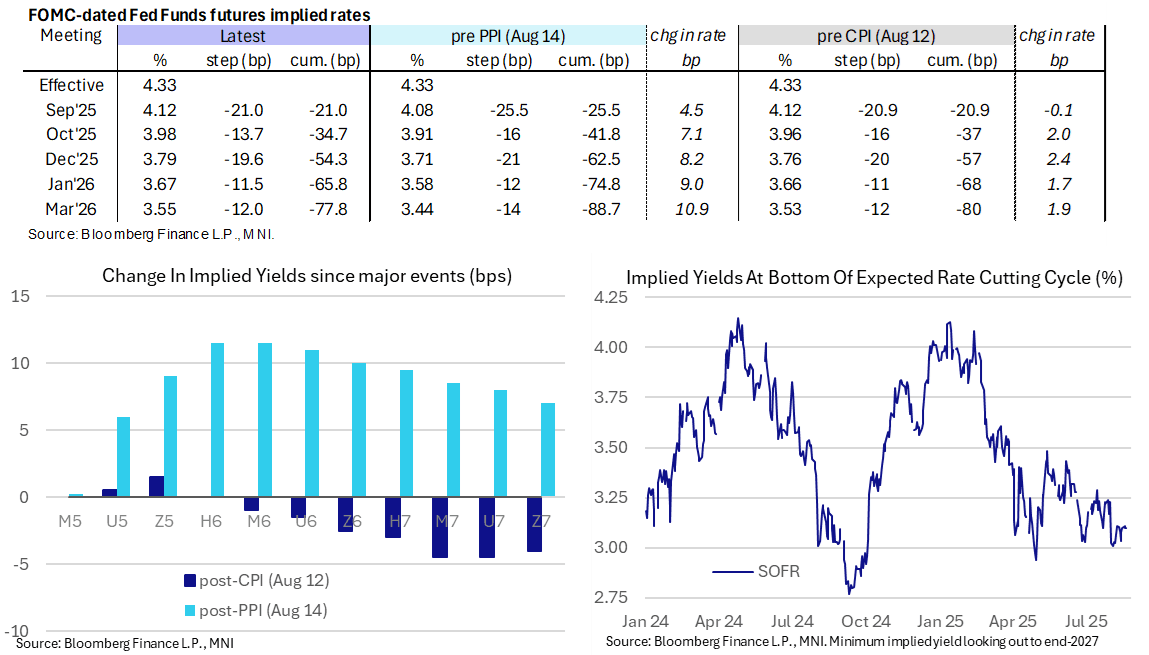

STIR: Fed Rates Treading Water, FOMC Minutes Later Today

Aug-20 10:12

- Fed Funds implied rates are little changed overnight as they keep to relatively narrow ranges seen so far this week.

- Whilst the FOMC minutes are released later today, the main data of the week comes tomorrow with jobless claims and flash PMIs before Powell’s Jackson Hole appearance on Friday.

- Cumulative cuts from 4.33% effective: 21bp Sep, 34.5bp Oct, 54.5bp Dec, 66bp Jan and 78bp Mar.

- The SOFR implied terminal yield of 3.10% (SFRH7, unch) also keeps to particularly narrow ranges, having closed the past three sessions between 3.10-3.11%. More broadly, it holds the +/-5bp of 125bp of cuts from current levels range seen since the Aug 1 payrolls report.

- Today’s Fedspeak:

- 1100ET – Fed Gov Waller (permanent voter, dove) speaks on payments at Blockchain Symposium (text + Q&A). If anything like Bowman’s appearance yesterday, expect a simple acknowledgement that his view remains the same (“the wait and see approach is overly cautious and, in my opinion, does not properly balance the risks to the outlook and could lead to policy falling behind the curve”) before moving onto areas that are less directly monetary policy relevant.

- 1400ET – FOMC minutes for the Jul 29-30 meeting, offering further color on the meeting that saw two dissenters with Bowman and Waller preferring to cut rates. This is firmly seen as secondary to Fed Chair Powell’s Jackson Hole speech at 1000ET on Friday.

- 1500ET – Bostic (non-voter) in conversation on economy (Q&A only). He said Aug 13 ““For the rest of this year, I still have one cut on my outlook… that also is predicated on the notion that labor markets stay solid. If they weaken considerably, that balance of risks starts to look differently and the appropriate path will look different as well.”