MNI US MARKETS ANALYSIS - French PM Could be Toppled in Vote

Highlights:

- Inflation in focus, with PPI and CPI all due this week

- Bayrou may face vote that could topple his cabinet later today

- JPY weaker as market considers alternatives after Ishiba's resignation

US TSYS: Modestly Twist Steeper Within Payrolls Driven Ranges

- Treasuries sit twist steeper but within Friday’s payrolls-driven range.

- The JGB curve twist steepened following Sunday’s resignation of LDP leader Ishiba although spillover to Treasuries was limited with the Asia cash open.

- It’s a quieter start to the week with Trump remarks to the White House Religious Liberty Commission at 1010ET possibly the main scheduled event along with the NY Fed's consumer survey including its inflation expectations.

- Greater focus is on preliminary payrolls benchmark revisions, PPI and CPI over Tue-Thu, with previews for those out later today and tomorrow.

- Cash yields are between 0.8bp lower (2s) to 1.8bp higher (30s).

- Curves are off recent steeps, including 2s10s at 58.3bp off Wednesday’s 63.9bp and 5s30s at 119.3bp off 126.9bp post-NFPs (multi-year steeps).

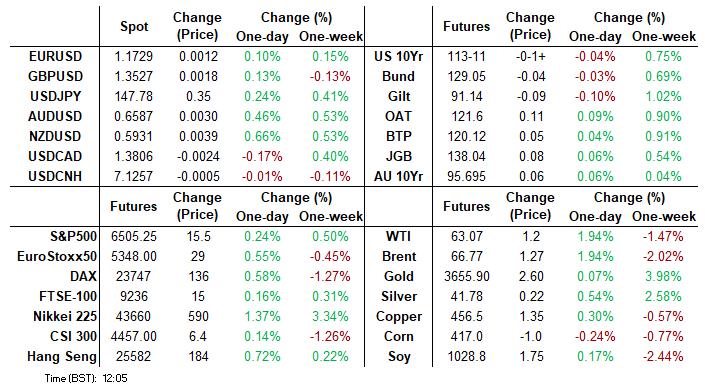

- TYZ5 trades near unchanged at 113-11 (-01+) on modest cumulative volumes of 265k.

- The post-payrolls high of 113-21+ marked another fresh short-term cycle high and points to a bullish structure. It marks resistance after which lies 113-26+ (2.764 proj of Jul 15-22-28 price swing) whilst support is seen at 112-28+ (Sep 5 low).

- Data: NY Fed consumer survey Aug (1100ET), Consumer credit Jul (1500ET)

- Bill issuance: US Tsy $82B 13W & $73B 26W bill auctions (1130ET)

- Politics: Trump delivers remarks (1010ET)

STIR: Payrolls Rally Broadly Consolidated With Tue-Thu Data Eyed

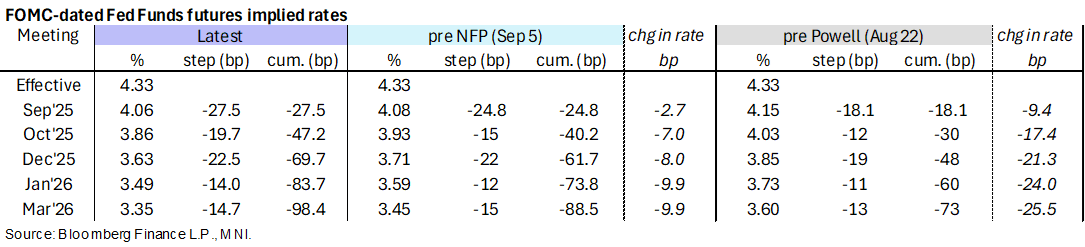

- Fed Funds implied rates are little changed since Friday’s close, holding what was only a modest paring of the rally on a soft payrolls report at the time.

- It sees close to three consecutive cuts priced to year-end, with only limited odds of a 50bp cut next week (~10%).

- Cumulative cuts from 4.33% effective: 27.5bp Sep, 47bp Oct, 69.5bp Dec, 83.5bp Jan and 98.5bp Mar.

- The SOFR implied terminal yield of 2.86% (SFRH7) is 1bp lower from Friday as it sits a little off 150bp of cuts ahead from current levels. The yield is only 2.5bp lower than levels just prior to the NFP release after rates rallied into the release.

- It’s a quieter start to the week before preliminary payrolls benchmark revisions, PPI and CPI over Tue-Thu. The Fed is now in media blackout ahead of the FOMC meeting on Sep 16-17.

IRAN: Grossi Touts Progress w/Iran, Analysts Sceptical 'Snapback' Can Be Averted

IAEA Director Rafael Grossi said he hopes for a successful conclusion to nuclear discussions with Iran in the next 'few days'. The talks are aimed at a last-minute deal between Iran and the UN's nuclear watchdog to avert the imminent re-imposition of 'snapback' UN sanctions.

- In an opening statement to the IAEA Board of Governors' meeting this morning, Grossi said, “progress has been made in talks with Iran on full resumption of inspections, I hope that within the next few days it will be possible to come to a successful conclusion of discussions.”

- Grossi added: "There is still time. But not much... I can assure you that we are exercising our utmost efforts to come to a good outcome within the next few days, perhaps hours."

- Iran Nuances reports that Iran’s Foreign Ministry spokesperson said: “The results of the discussions with the [IAEA] are currently under review by the relevant authorities in Tehran. We are waiting for a final conclusion to be reached, and based on that, we will announce what the next step will be.” The spokesperson added no decision has been taken yet on withdrawing from the nucelar non-proliferation treaty (NPT).

- While, the comments suggest a deal could be reached to avert ‘snapback’, Ali Vaez at the International Crisis Group notes that he, “can’t see a meaningful Iran-IAEA technical deal in the absence a political deal between Iran and the West.”

- Foreign Minister Abbas Araghchi said yesterday the impact of 'snapback' will be “mainly political,” suggesting its economic impact is being exaggerated.

FRANCE: Result of No-confidence Vote Not Expected Till 1900CET At The Earliest

Local and political media outlets report that the result of the French no-confidence vote is not expected to be known until 1900CET (1800BST) at the earliest.

- PM Bayrou in theory has an unlimited amount of time to deliver his general policy address at 1400BST/1500CET.

- Following this address, speakers from each parliamentary group (eleven in total) will provide remarks. Speaking times depend on the number of seats each group holds in the National Assembly. From Le Figaro:

- Ensenble Group: 35 mins

- RN, DR and MODEM (Bayrou's party): 15 mins

- Other groups (fewer than 35 deputies): 10 mins:

- Speaker for non-registered deputies: 5 mins

- Following these speeches, Bayrou will then be able to speak again before votes begin.

- Le Parisien highlights that "The debates surrounding his previous general policy statement, on January 14, lasted approximately five hours, without a vote"

NATURAL GAS: “US demands EU stops buying Russian gas" - FT

“US demands EU stops buying Russian gas if it wants new sanctions on Putin” - FT

- "European countries should stop buying Russian oil and gas if they want Washington to tighten sanctions on Moscow, according to Donald Trump’s energy chief, who said the trade was funding Vladimir Putin’s “war machine”."

- "Chris Wright, US energy secretary, told the Financial Times that European countries should instead buy American liquefied natural gas, gasoline and other fossil fuel products to meet the terms of the US-EU trade deal, which calls on EU countries to buy $750bn of US energy by the end of 2028."

- Link here

FOREX: JPY Weaker as Ishiba Resignation Opens Up Uncertainty

- JPY remains weaker against all others early Monday. For much of last week, markets were speculating over the chances of Ishiba in a potential LDP vote to

bring forward a party leadership election, but the PM has gotten ahead of any further uncertainty by announcing his resignation. So why is JPY weaker? Thatcherite MP Sanae Takaichi is a front-runner among many opinion polls - and also ran against Ishiba in the last leadership race, triggering JPY vol. While politically conservative, she's made clear her preference for easy monetary policy and a bigger role for fiscal spending - reminiscent of the Abenomics policy set from 2012 - 2020. - EUR/JPY rallied to 173.91 overnight, but has stalled since. 173.97 remains the bull trigger here, clearance of which puts the rate at the best levels since last year. AUD, NZD extend their recent spell of strength, with NZD/USD just below Friday's highs of 0.5918. A rally through here and 0.5927 would break downtrendline resistance drawn off the early July highs.

- Firmer equity sentiment since the open has allowed the likes of AUD and NZD to outperform in G10 currency markets on Monday, capitalising on the bearish dollar sentiment following the softer-than-expected US employment report. As a result, AUDUSD (+0.41%) has traded within one pip of the Friday highs and the latest price action has helped the pair consolidate above short-term resistance of 0.6569, which was cleared last week. This places the market’s interest back on the 0.66 handle, of which we have only had one daily close above since the US election related volatility back in November 2024.

- Focus this week remains on the US inflation picture, with PPI and CPI prints due on Wednesday and Thursday respectively. With a September Fed rate cut now all but assured - a weaker price turnout this week could trigger further speculation over an easing step of over 25bps at next week's committee meeting.

INDONESIA: Offshore IDR Weaker as Finance Minister Reshuffled Out of Office

While the local close sees USDIDR lower by ~0.7% on the day, offshore markets see a spell of weakness on the finance ministry reshuffle: 1m outrights erase the day's downside to trade just above Friday's close of 16,407.

- State minister Hadi confirmed that Sri Mylyani Indrawati has been removed from the post of finance minister as part of the reshuffle - but there is no confirmation on who will be replacing her.

- The reshuffle follows the broad protests and scenes of violence across the country - and may signal a spell of near-term political uncertainty in Indonesia - particularly as Indrawati held the role of finance minister for the vast majority of the past 20 years - having first been appointed in 2005.

FX OPTIONS: EUR pinned between sizeable strikes

EUR spot remains pinned between a series of sizeable strikes - over E3.7bln notional is set to roll-off between 1.1700 - 1.1750 today, which could help dictate the range. With US PPI, CPI data set for this week, the larger option pipeline is thinner than usual, but decent sized options expiring at 1.1740-50(E1.4bln) and $1.1825(E1.7bln) in EURUSD on Thursday could be of post-data interest.

Full expiry schedule for today's cut here:

- EUR/USD: $1.1600(E1.2bln), $1.1620-30(E1.0bln), $1.1690-00(E1.3bln), $1.1750(E1.2bln), $1.1835(E873mln)

- USD/JPY: Y146.00($1.1bln), Y146.45-55($945mln)

- USD/CAD: C$1.4000($517mln)

- USD/CNY: Cny6.9500($1.4bln)

EQUITIES: Corrective Bear Cycle in Eurostoxx 50 Futures Remains in Play

- A corrective bear cycle in Eurostoxx 50 futures remains in play. Recent weakness resulted in a breach of 5368.74, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5378.06, the 20-day EMA. A clear break of it would be a bullish development.

- A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high last week, breaching the Aug 28 high of 6523.00. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6447.06, the 20-day EMA.

COMMODITIES: Last Week's Gains Reinforce Bullish Conditions for Gold

- A bear cycle in WTI futures remains intact and the latest bull phase appears to have been a correction. The pullback from last Tuesday’s high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.56, the Aug 4 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

- Gold remains in a clear bull cycle and last week’s gains reinforce current conditions. The yellow metal has breached a key resistance at $3500.1, the Apr 22 high, delivering a fresh all-time high. The break also confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3623.1, a Fibonacci projection. Initial firm support lies at $3440.0, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 08/09/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 08/09/2025 | 1900/1500 | * | Consumer Credit | |

| 09/09/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 09/09/2025 | 0645/0845 | * | Industrial Production | |

| 09/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/09/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 09/09/2025 | 1150/1350 | SNB's Schlegel at BIS fireside chat | ||

| 09/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 09/09/2025 | 1515/1615 | BOE Breeden Moderates BIS Fireside Chat | ||

| 09/09/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result |