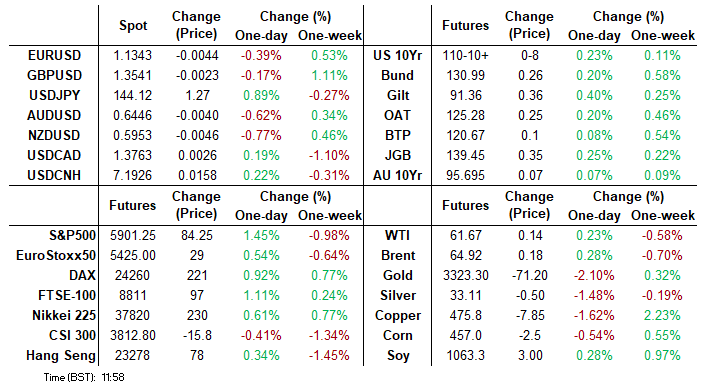

MNI US MARKETS ANALYSIS - Flatter JGB Curve Boosts USD/JPY

Highlights:

- JGB curve bull flattens, providing relief for USD/JPY

- Softer-than-expected French CPI drives EUR lower, EGBs higher

- GBP shows relative resilience as backtrack in BoE pricing holds

US TSYS: Bull Flatter With Japan Looking At Bond Issuance Composition

- Treasuries sit bull flatter from Friday’s close after yesterday’s cash closure and thin futures trading for US Memorial Day.

- The flattening impetus is aided by Reuters reporting the Japan MoF may shift the composition of its bond issuance plan for the current fiscal year.

- Cash yields are 1.5-7bp lower from Friday after yesterday’s cash closure, with declines led by 30s (at 4.968% for a further shift away from last week’s 5.15%).

- It sees a pullback from last week’s multi-year steeps for 5s30s, currently at 91.8bp after fleetingly clearing 100bps on both Thu and Fri with a high of 101bp (highest since Oct 2021).

- TYM5 trades at 110-09+, +07 from Friday’s settle after an early close yesterday, off an earlier high of 110-13. The lift off the May 22 low of 109-13 is deemed corrective and could next see resistance at 110-21+ (May 16 high), a key near-term level.

- The June expiry is still the front month but the quarterly roll should now dominate, with first notice on May 30th.

- Data: Durable goods Apr prelim (0830ET) – FHFA and S&P CoreLogic house prices Mar (0900ET), Conference Board consumer survey May (1000ET), Dallas Fed mfg May (1030ET)

- Fedspeak: Barkin on BBG TV (0930ET), Williams in moderated discussion (2000ET) – see STIR bullet.

- Coupon issuance: US Tsy to sell 2Y $69B 2Y Note 91282CNE7 (1300ET)

- Bill issuance: $76B 13W and $68B 26W (1130ET) before $70B 6W (1300ET)

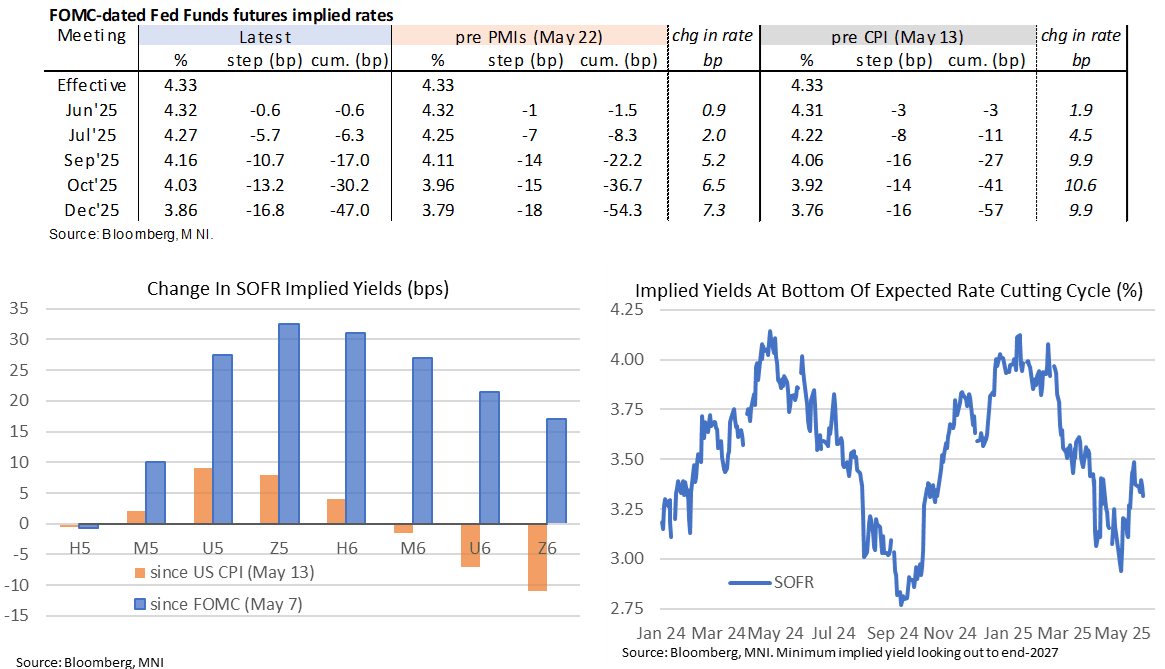

STIR: Next Fed Cut Seen In October, Kashkari Warns On Tariff Look Through

- Fed Funds implied rates are little changed from Friday’s close for meetings out to 2025 after yesterday’s thin trading with the US Memorial Day and a UK bank holiday.

- The rate path remains close to the most hawkish it has been since February, with a next Fed cut fully priced for the Oct FOMC.

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 6.5bp Jul, 17.5bp Sep, 30bp Oct and 47bp Dec.

- A SOFR implied terminal yield of 3.295% (SFRZ6, -2bp) meanwhile is at a two-and-a-half week low.

- Minneapolis Fed’s Kashkari (’26 voter) earlier today noted a preference not to look through tariff-induced inflation, adding to his comments yesterday that he thinks it’s unlikely to have a clear enough picture to move rates in September.

- Today sees data highlights from preliminary durable goods orders for April and the Conference Board consumer survey for May. It’s a thin docket for Fedspeak, with just Barkin in the session before Williams late on from Japan.

- 0930ET – Richmond Fed’s Barkin (non-voter) on BBG TV. He last noted on May 9 that consumer spending and business investment is still very solid although it’s not a given that firms can raise prices on tariffs.

- 2000ET – NY Fed’s Williams (voter) moderated discussion in Tokyo (no text). He was more explicit than usual on May 19 in offering a rough timetable behind rate cut patience, with broader FOMC communications continuing to suggest that a cut before the end of summer is not in the frame.

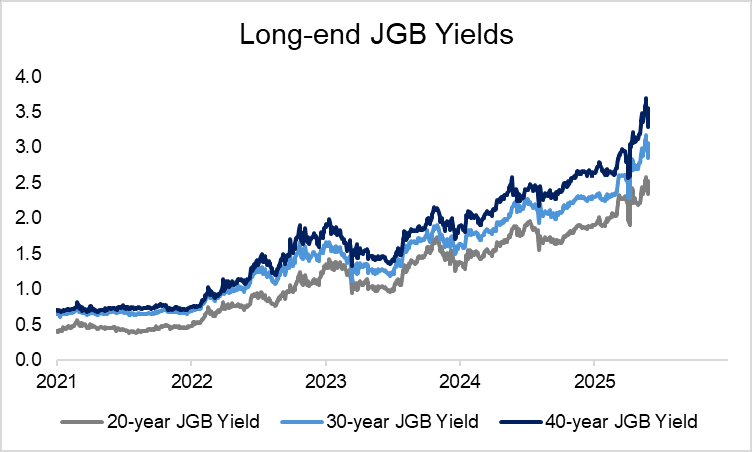

JGBS: Sharp Reprieve For Long-end JGBs On MOF Sources; Focus On Auction Demand

40-year JGB yields are down 24.5bps to 3.312% today, with the curve sharply bull flatter, after Reuters sources suggested the MOF will consider skewing the composition of its current issuance programme away from super-long-end instruments. That’s the largest one-day decline in 40-year yields since Bloomberg began tracking the data in February 2008 (and the 2nd largest absolute change in yields). 40-year yields are now almost 40bps below last Friday’s 3.697% high, with short-positioning likely exacerbating the last few days’ relief rally. However, focus remains intently on tomorrow’s 40-year auction.

- There have been several factors contributing to the sharp sell-off in (particularly long-end) JGBs over the last two months.

- (i) Signs of waning structural demand from domestic counterparties, such as the life insurance sector. Weak auction results (e.g last week’s 20-year auction) may reflect such dynamics.

- (ii) Concerns around less BOJ-led support for government bonds in the coming quarters.

- (iii) Fiscal concerns, particularly with the upper house election due in July. This morning (per BBG), a government advisory panel called for enhanced domestic fiscal prudence: “We must manage finances with a heightened sense of urgency to prevent rising debt costs from crowding out essential policy spending”.

- (iv) Global curve steepening on a wider global assessment of long-dated issuance in a structurally higher inflation environment with heightened policy uncertainty. Moves in US Treasuries have embodied this dynamic, with erratic tariff policy changes and still-expansionary fiscal policy forcing investors to demand a higher term premium for long-end US debt. The UK DMO has already skewed its issuance plans away from long-end debt due to “declining strength” of demand for these instruments.

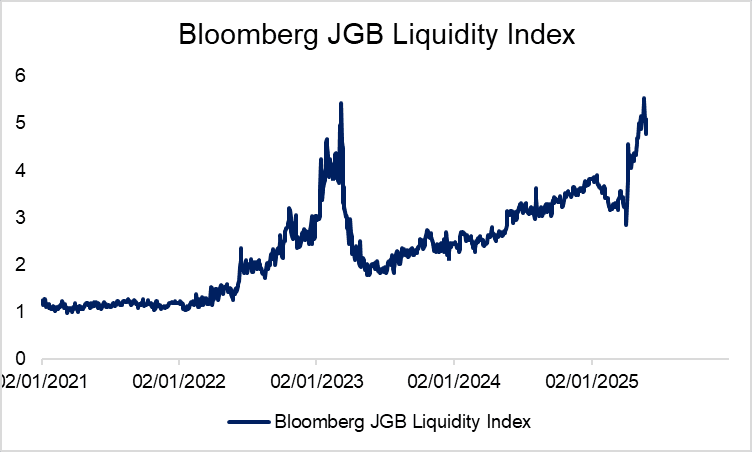

JGBS: Mid-June In Focus For MOF Selling and BOJ Buying Tweaks

- These factors have come against a backdrop of reduced liquidity in the Japanese bond market, especially at the long-end. Bloomberg’s JGB liquidity index (which isn’t a perfect measure of this given it includes all bonds with a maturity greater than one year) has fallen from last week’s highs but remains elevated, indicating worse liquidity conditions.

- Reuters notes that the MOF will make a decision on its issuance plan around mid- to-late June, after holding discussions with market participants.

- This will align closely with the BOJ’s June 17 meeting, where the bank will review its bond purchase reduction plan. The BOJ is currently reducing bond purchases by JPY400 billion per quarter through March 2026. A former BOJ official recently told MNI that the BOJ should clearly communicate the pace at which it plans to reduce its JGB holdings, including both purchases and expected redemptions, to help maintain bond market stability.

SOUTH AFRICA: MNI SARB Preview - May 2025: Will SARB Resume Cuts?

Download Full Report Here

Executive Summary:

- Consensus is leaning towards a 25bp cut but some analysts are calling for a hold.

- Favourable short-term inflation developments give the MPC some comfort to ease policy.

- Longer-term uncertainty remains elevated, demanding cautious approach.

Consensus is leaning towards a 25bp cut at South African Reserve Bank’s (SARB’s) monetary policy meeting this week, as recent price dynamics have proven relatively benign, with headline inflation tracking below the +3.0-6.0% Y/Y target range. However, the wider perception is that it is a close call, with upside inflation risks further ahead and broader uncertainty around the outlook encouraging the Monetary Policy Committee (MPC) to remain cautious. In the meantime, SARB watchers will be on the lookout for any announcements surrounding ongoing talks with the National Treasury on the inflation target revision.

FOREX: Global Curve Dynamics Roil Currencies, USD/JPY Rallies 1.3%

- Global bond markets and the shape of yield curves remain the key driver for currencies, as renewed volatility in the JGB market triggers a slump in the JPY and a broad USD rally. According to sources, the Japanese Ministry of Finance solicited market opinions on the curve and the government's issuance approach via a questionnaire - triggering broad speculation that the government would re-orient away from longer-end issuance.

- The ensuing bull-flattening of the Japanese curve worked against the JPY, boosting USD/JPY by over 1.3% off the overnight low, and well within range of the Y144.00 handle. A close at current or higher levels for the pair would snap the short-term downtrend that had reversed the pair off the Y148.65 mid-May high. The initial resistance zone at 144.40, last Thursday’s high and the 20-day EMA. Above here, the 50-day EMA currently intersects at 145.73.

- EUR losses posted off the back of a lower-than-expected French CPI miss are holding, with a new pullback low at 1.1341, dipping the price below the Friday close - and reversing the entirety of the gains posted off the Trump EU tariff threat delay from yesterday. USD strength is also playing a part here - dollar's rallying alongside equities as the inverse relationship between yields and the currency continues - with strong USD/JPY demand adding an extra tailwind.

- Technically, EUR/USD sees scant support until 1.1271, the 20-day EMA, meaning today's dip lower is counter-trend. But a clear break below here would highlight a stronger reversal and signal scope for a deeper retracement. EUR/GBP meanwhile is testing major support at the 200-dma of 0.8383. This level was briefly pierced intraday last week, but hasn't sustained a break below since March earlier this year. Weakness through 0.8380 would result in the lowest print since April 3rd.

- Focus for markets Tuesday rests on prelim durable goods orders and May consumer confidence from the US. Fed's Barkin and ECB's Nagel make up the Fedspeak.

FOREX: GBP Shows Relative Resilience, Cable Consolidates Near 3-Year Highs

- Dollar strength remains evident on Tuesday amid the bull flattening for global yield curves, led by the impressive moves for JGBs. The greenback rally has been broad, with the likes of AUD and NZD shrugging off the optimistic tone for equity markets and falling around 0.6% on the session. However, GBPs only modest dip lower stands out in G10, and underpins the prevailing bullish theme for GBPUSD.

- The break of 1.3444 (Apr 28 / 29 high) remains significant here, confirming a resumption of the technical uptrend. This allowed the pair to print fresh cycle highs of 1.3593 on Monday, narrowing the gap substantially to 1.3605, a Fibonacci retracement. Moving average studies continue to highlight a dominant uptrend. First support lies at 1.3351, the 20-day EMA.

- EURGBP meanwhile is testing major support at the 200-dma of 0.8383. This level was briefly pierced intraday last week, but hasn't sustained a break below since March earlier this year. Weakness through 0.8380 sees the cross trade at its lowest level since April 3rd. 0.8359 is an immediate chart point of note, however, a more significant support resides at 0.8316, the March 28 low and a key support.

- While sticky BOE pricing remains another likely driver behind sterling’s resilience, the UK calendar is void of tier-one releases this week. Short-term focus will therefore be on BOE Pill today and Governor Bailey on Thursday. Further out, the June 10 spending review will garner much attention, while labour market & activity data is scheduled on June 10/12 respectively.

TURKEY: USDTRY Spikes After Probe Launched Into Interim Istanbul Mayor

- USDTRY spiked on headlines stating that Turkey has opened a probe into Istanbul interim mayor Nuri Aslan for “resisting a security official.” The pair rallied to as high as 39.06, up 0.1% at typing. Meanwhile, the Borsa Istanbul Stock index reversed earlier gains to trade around 0.8% lower.

- Nuri Aslan was elected as the interim mayor of Istanbul following the suspension of Mayor Ekrem Imamoglu over corruption charges.

- Videos have been circulating on social media which appear to show Nuri Aslan in confrontation with security guards in a courthouse. That follows the Court of Istanbul arresting 25 people as part of corruption allegations yesterday. Those arrested included the municipality’s deputy secretary-general, housing company chairman and chief of staff, Anadolu Agency reported.

EQUITIES: Latest Gains Reinforce Bullish E-Mini S&P Trend Condition

- A bullish theme in Eurostoxx 50 futures remains intact and the recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear uptrend and recent gains maintain the sequence of higher highs and higher lows. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Key support to watch lies at 5230.62, the 50-day EMA. Clearance of this average would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact and the latest pullback is considered corrective. Last Friday’s sell-off resulted in a print below the 20-day EMA, at 5779.53. A key support lies at 5719.58, the 50-day EMA. A clear break of this average is required to highlight a stronger reversal and signal scope for a deeper retracement. Sights are on the bull trigger at 5993.50, the May 20 high.

COMMODITIES: Gold Medium-Term Trend Signal Unchanged and Bullish

- WTI futures traded to a fresh S/T cycle high last Wednesday before finding resistance. The recovery since Apr 9, appears corrective. Key resistance to watch is $62.71, the 50-day EMA. It has been pierced, a clear break of it would highlight a stronger reversal and open $65.82, Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. The price pattern on May 21 is a shooting star - a reversal signal.

- Gold has recovered from its recent lows. The climb signals the end of the corrective phase between Apr 22 - May 15. Medium-term trend signals are unchanged and remain bullish. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. A continuation higher would open $3435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3121.0, the May 15 low.

| Date | GMT/Local | Impact | Country | Event |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 27/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 27/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 27/05/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 28/05/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 28/05/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 28/05/2025 | 0130/1130 | *** | Quarterly construction work done | |

| 28/05/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 28/05/2025 | 0600/0800 | ** | Retail Sales | |

| 28/05/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 28/05/2025 | 0645/0845 | ** | PPI | |

| 28/05/2025 | 0645/0845 | *** | GDP (f) | |

| 28/05/2025 | 0645/0845 | ** | Consumer Spending | |

| 28/05/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/05/2025 | 0755/0955 | ** | Unemployment | |

| 28/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kahkari | ||

| 28/05/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 28/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 28/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/05/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/05/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/05/2025 | 1500/1600 | BOE's Pill on monetary policy panel at Austria National Bank / SUERF | ||

| 28/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 28/05/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/05/2025 | 1800/1400 | FOMC Minutes |