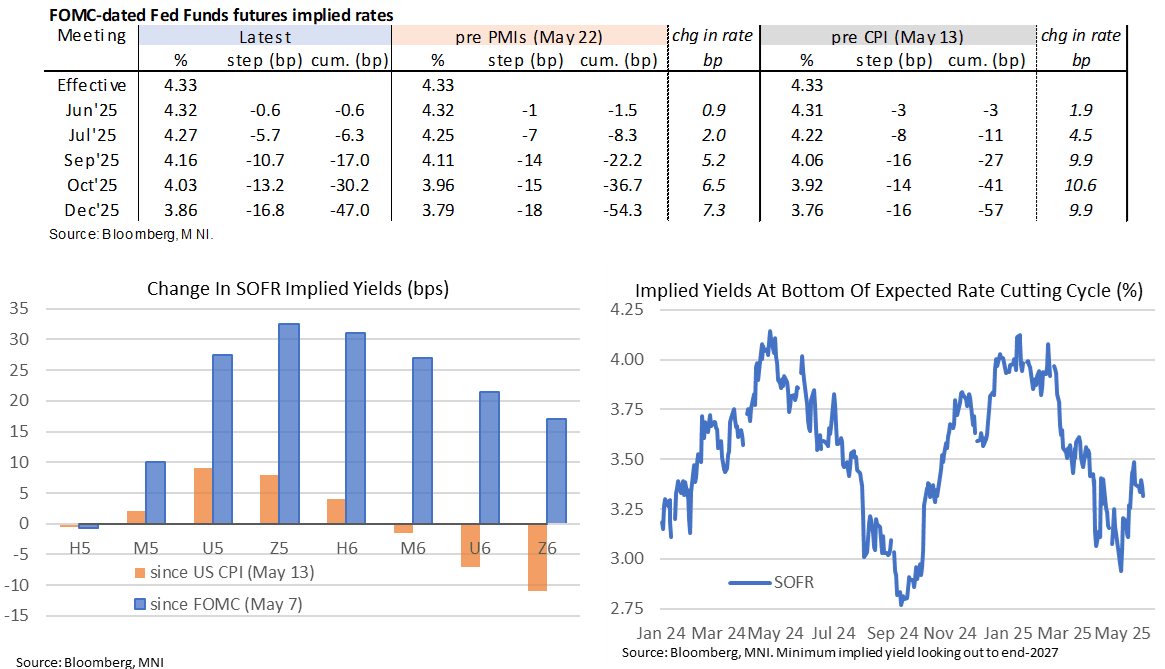

STIR: Next Fed Cut Seen In October, Kashkari Warns On Tariff Look Through

- Fed Funds implied rates are little changed from Friday’s close for meetings out to 2025 after yesterday’s thin trading with the US Memorial Day and a UK bank holiday.

- The rate path remains close to the most hawkish it has been since February, with a next Fed cut fully priced for the Oct FOMC.

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 6.5bp Jul, 17.5bp Sep, 30bp Oct and 47bp Dec.

- A SOFR implied terminal yield of 3.295% (SFRZ6, -2bp) meanwhile is at a two-and-a-half week low.

- Minneapolis Fed’s Kashkari (’26 voter) earlier today noted a preference not to look through tariff-induced inflation, adding to his comments yesterday that he thinks it’s unlikely to have a clear enough picture to move rates in September.

- Today sees data highlights from preliminary durable goods orders for April and the Conference Board consumer survey for May. It’s a thin docket for Fedspeak, with just Barkin in the session before Williams late on from Japan.

- 0930ET – Richmond Fed’s Barkin (non-voter) on BBG TV. He last noted on May 9 that consumer spending and business investment is still very solid although it’s not a given that firms can raise prices on tariffs.

- 2000ET – NY Fed’s Williams (voter) moderated discussion in Tokyo (no text). He was more explicit than usual on May 19 in offering a rough timetable behind rate cut patience, with broader FOMC communications continuing to suggest that a cut before the end of summer is not in the frame.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Extraordinary Measures And Cash Look Sufficient To Head Off X-Date

Treasury has about $164B in "extraordinary measures" available as of April 23 to avoid hitting the debt limit, per its regular report out Friday. That's out of a maximum total of $375B (they have used $211B).

- With Treasury cash looking healthy (around $600B), that's a fair amount of dry powder to get through the summer months to wait out the debt limit impasse. Tax receipts have looked strong with tariff revenues also starting to boost cash flows, further reducing the near-term urgency to adjust bond issuance.

- This has also helped push back analyst “x-date” expectations to later in the summer/September. We expect to hear from Treasury about its own x-date assumptions next week.

US TSYS: Treasury Market Trading Stayed Orderly In April: Fed Report

Liquidity across financial markets including the Treasury market deteriorated after President Trump's April 2 reciprocal tariffs announcement but market functioning was generally orderly, according to the Federal Reserve's semiannual report on financial stability, released Friday. (PDF link is here)

- Treasury market liquidity has been poor for years and yields were particularly volatile in early April, contributing to a deterioration in market liquidity, the Fed said.

- Nevertheless "trading remained orderly, and markets continued to function without serious disruption," according to the report, which looked at information available as of April 11.

FED: Ex-Gov Warsh: Fed Has Failed To Satisfy Price Stability Remit

From our Washington Policy Team - Some fairly sharp words today from ex-Fed Governor Warsh on the central bank (who for what it's worth is seen by betting markets as by far the frontrunner for the next Fed Chair):

- The best way for the Federal Reserve to safeguard its independence is for policymakers to avoid expanding the institution's role over time, including wading into policy areas that are outside its core mission, former Fed Governor Kevin Warsh, a leading contender to replace Jerome Powell as chair next year, said Friday.

- "I strongly believe in the operational independence of monetary policy as a wise political economy decision. And I believe that Fed independence is chiefly up to the Fed," Warsh said in a speech at a Group of Thirty event on the sidelines of the IMF meetings. "Institutional drift has coincided with the Fed’s failure to satisfy an essential part of its statutory remit, price stability. It has also contributed to an explosion of federal spending." His speech made no mention of Trump's tariffs or the appropriate monetary policy to deal with them.

- He said the ideas of data dependence and forward guidance widely adopted by Fed officials are not especially useful and might even be counterproductive.

"We should care little about two numbers to the right of the decimal point in the latest government release. Breathlessly awaiting trailing data from stale national accounts -- subject to significant, subsequent revision -- is evidence of false precision and analytic complacency," he said.

"Near-term forecasting is another distracting Fed preoccupation. Economists are not immune to the frailties of human nature. Once policymakers reveal their economic forecast, they can become prisoners of their own words. Fed leaders would be well-served to skip opportunities to share their latest musings."