MNI US MARKETS ANALYSIS - Fed Pricing Up for Grabs Into NFP

Highlights:

- Treasuries firm ahead of NFP, with July Fed pricing in jeopardy

- Consensus sees payrolls at +106k, but market poised more pessimistic

- GBP, Gilts hold bounce as PM defends Chancellor and affirms fiscal rules

US TSYS: Slightly Firmer Before NFPs, ISM Services, OBBB Vote and Early Close

Treasuries are modestly firmer as we await a packed session headlined by nonfarm payrolls. Trump’s OBBB also now looks likely to be passed by the House in a final vote at 0800ET ahead of a self-imposed Jul 4 deadline. This all comes ahead of a truncated session for cash trading ahead of Independence Day tomorrow.

- The June payrolls report headlines today’s session (MNI Preview here) but there are plenty of other market moving releases including ISM services.

- The House rule vote on Trump’s OBBB has passed after Conservative holdouts among House Republicans flipped their support, seen as a test run for the final vote expected at 0800ET. The Bill's passage now seems all-but-assured.

- Independence Day trading: Cash sees early close today (1400ET) before full closure tomorrow. Futures sees full session today before early close tomorrow (1300ET).

- Cash yields are 1.5-3bp lower on the day, with declines led by 2s.

- TYU5 trades at 111-26+ (+ 06+) on lower cumulative volumes of 270k, having remained within yesterday’s range throughout.

- A bull cycle in Treasury futures is intact but prices remain below Tuesday’s session high of 112-12+. Attention is on the next important resistance at 112-15 (61.8% retrace of the Apr 7 - 11 steep sell-off) after which lies 112-13 (May 1 high). First key support is 111-08+ (20-day EMA).

- Data: Nonfarm payrolls Jun (0830ET), Weekly jobless claims (0830ET), International trade May final (0830ET), S&P Global US services/composite PMI Jun final (0945ET), ISM services (1000ET), Durable goods May (1000ET)

- Fedspeak: Bostic on speech on mon pol (1100ET)

- Bill issuance: US Tsy $55B 4W & $45B 8W bill auctions (1000ET - earlier than usual owing to the upcoming holiday), US Tsys $60B 77-Day CMB (1130ET)

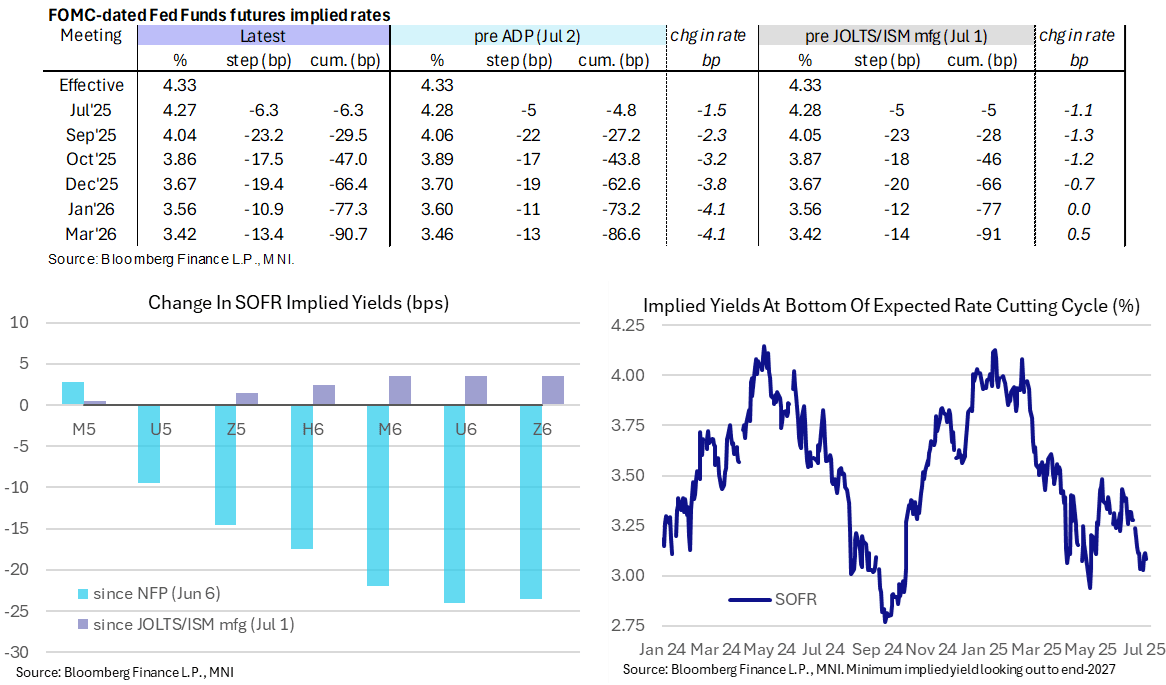

STIR: July FOMC Near Most Dovish Levels In A Month Ahead Of Stacked Docket

- Fed Funds implied rates are up to 1.5bp lower on the day for 2025 meetings ahead of a potentially instrumental day for data.

- Yesterday’s weak ADP report for June has helped reverse the lift seen after Tuesday’s strong JOLTS report for May.

- Sensitivity to labor market weakness – aided by recent dovish steers from Waller and then Bowman – has seen July FOMC pricing at its most dovish since late Jun 12/early Jun 13 (initial reaction to US strikes on Iran) and before that prior to a solid payrolls report on Jun 6.

- Cumulative cuts from 4.33% effective: 6.5bp Jul, 29.5bp Sep, 47bp Oct, 66.5bp Dec, 77bp Jan and 91bp Mar.

- The SOFR implied terminal yield of 3.085% (SFRZ6, +3bp) remains towards the low end of recent ranges with circa five cuts priced.

- Today sees a stacked data calendar ahead of Independence Day tomorrow. It’s headlined by the nonfarm payrolls report for June but with other notable releases including ISM services and weekly jobless claims.

- Bostic (non-voter) is the only scheduled FOMC speaker today, giving a speech on monetary policy at 1100ET (text + Q&A). He spoke in-depth on the economic outlook at a MNI Connect event on Monday, indicating he pencilled in one cut in 2025 and three cuts in 2026.

US: House Of Representatives On Brink Of Passing Big Beautiful Bill

At around 03:30 ET 08:30 BST this morning, House Speaker Mike Johnson (R-LA) broke the deadlock on a procedural vote to adopt the rule and advance the GOP's One Big Beautiful Bill towards a final vote on the House floor.

- Consistent with previous votes, Johnson kept the rule vote open while he worked in concert with President Donald Trump to flip holdouts with political threats and promises to work on conservative priorities in future legislation.

- With the rule adopted, the House is now on a glide path to holding a final vote on the massive reconciliation bill that could come as soon 06:30 ET 11:30 BST. Debate on the bill is underway in the House and can be followed on C-Span.

- The process played out largely as expected, with conservative hardliners in House registering their displeasure with the Senate-passed package, but ultimately unwilling to torpedo a bill that covers the bulk of Trump’s domestic agenda.

SOFR: Mix Of Positioning Swings Seen During Wednesday’s Twist Steepening

OI data points to a mix of net long setting and short cover in the SOFR whites on Wednesday, before a mix of net short setting and long cover came to the fore further out the strip.

| 02-Jul-25 | 01-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,316,114 | 1,315,336 | +778 | Whites | +22,099 |

SFRU5 | 1,117,977 | 1,130,359 | -12,382 | Reds | -8,971 |

SFRZ5 | 1,291,858 | 1,258,423 | +33,435 | Greens | +9,718 |

SFRH6 | 974,807 | 974,539 | +268 | Blues | +10,958 |

SFRM6 | 870,288 | 862,808 | +7,480 |

|

|

SFRU6 | 821,030 | 829,539 | -8,509 |

|

|

SFRZ6 | 940,259 | 940,325 | -66 |

|

|

SFRH7 | 698,371 | 706,247 | -7,876 |

|

|

SFRM7 | 649,137 | 649,694 | -557 |

|

|

SFRU7 | 460,339 | 455,599 | +4,740 |

|

|

SFRZ7 | 411,106 | 409,837 | +1,269 |

|

|

SFRH8 | 315,049 | 310,783 | +4,266 |

|

|

SFRM8 | 232,084 | 230,270 | +1,814 |

|

|

SFRU8 | 208,396 | 204,922 | +3,474 |

|

|

SFRZ8 | 187,929 | 185,378 | +2,551 |

|

|

SFRH9 | 141,830 | 138,711 | +3,119 |

|

|

US TSY FUTURES: Mix Of Short Setting & Long Cover Seen Wednesday

OI data points to a mix of limited net short setting and long cover through US futures during Wednesday's downtick. The only real positioning swing of note (in DV01 terms) came via net short setting in WN futures.

| 02-Jul-25 | 01-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,288,343 | 4,309,391 | -21,048 | -806,798 |

FV | 7,104,318 | 7,118,937 | -14,619 | -634,680 |

TY | 5,055,134 | 5,045,935 | +9,199 | +612,284 |

UXY | 2,433,118 | 2,444,182 | -11,064 | -974,872 |

US | 1,804,099 | 1,808,052 | -3,953 | -501,130 |

WN | 1,956,969 | 1,942,744 | +14,225 | +2,617,367 |

|

| Total | -27,260 | +312,172 |

STIR: Hawkish Adjustments In GBP STIRs Surrounding Reeves' Future

GBP STIR curves have also hawkishly steepened on speculation surrounding the future of Chancellor Reeves.

- The potential departure of Reeves could result in a watering down of the UK’s fiscal rules, limiting the BoE’s room to ease.

- BoE-dated OIS now little changed to 2bp less dovish on the day across ’25 meetings.

- Over 80% odds of a 25bp cut still priced for August, with such a step fully discounted through the September meeting.

- December meeting pricing shows ~53bp of cumulative cuts after failing to move decisively through 55bp of cuts in recent sessions.

- SONIA futures last 0.5-16.0 lower.

- SFIZ5/Z6 steepens away from year-to-date lows in the -25.0 area to print -20.0 last.

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Aug-25 | 4.010 | -20.7 |

| Sep-25 | 3.945 | -27.2 |

| Nov-25 | 3.777 | -44.0 |

| Dec-25 | 3.690 | -52.7 |

| Feb-26 | 3.561 | -65.6 |

| Mar-26 | 3.530 | -68.7 |

EUROPE ISSUANCE UPDATE:

Spain auction results

- E2.159bln of the 2.40% May-28 Bono. Avg yield 2.159% (bid-to-cover 1.91x).

- E2.132bln of the 3.15% Apr-35 Obli. Avg yield 3.163% (bid-to-cover 1.90x).

- E1.758bln of the 3.50% Jan-41 Obli. Avg yield 3.671% (bid-to-cover 1.68x).

- E735mln of the 1.15% Nov-36 Obli-Ei. Avg yield 1.47% (bid-to-cover 2.14x).

France auction results

- E7.674bln of the 3.20% May-35 OAT. Avg yield 3.27% (bid-to-cover 2.32x).

- E2.355bln of the 3.60% May-42 OAT. Avg yield 3.72% (bid-to-cover 2.77x).

- E1.923bln of the 3.75% May-56 OAT. Avg yield 4.05% (bid-to-cover 2.91x).

FOREX: Vol Markets Isolate JPY, CHF, ZAR, MXN in NFP Reaction

- Headed into today's NFP print, overnight G10 FX vols are seeing solid support, with markets isolating JPY and CHF as being particularly sensitive via a sizeable pre-data implied vol premium. USD/JPY and USD/CHF vols have been marked higher by ~2.5 points into today's print, notably higher than the YTD average across both pairs and blowing out the break-even on an overnight USD/JPY, USD/CHF straddle to 120 pips and 60 pips respectively (see table below).

- For the USD Index, markets are looking to test whether prices have successfully formed a base at 96.377 - this week's low - which could prompt a S/T correction and recovery for prices off oversold levels. Nonetheless, prices are through the bottom-end of the falling wedge formation formed in the DXY. This coincides with the gradual build of pricing for a Fed rate cut in July, priced at 25% of a 25bp rate cut. Markets may look to resolve this pricing one way or the other on today's NFP.

- We wrote earlier this week that the oversold position in the USD Index does raise the possibility that either; a correction unfolds soon, or that the pace of the trend slows down, resulting in more volatile price action going forward. The next key long-term support to monitor is 95.24, 76.4% of the Jan '24 - Sep 22 bull phase.

FOREX: GBP Holds Bounce as Starmer Backs Up Chancellor, Affirms Fiscal Rules

- GBP is holding the entirety of the bounce off Wednesday lows, with GBP/USD over a point off yesterday's lows as the UK PM looks to bolster the Chancellor's position and reinforce to markets that she will remain in place for the long-term, despite rampant speculation over her departure during the Wednesday session.

- The durability of today's GBP strength will depend on the market buying into the view that the government have sufficient fiscal options to head off any market instability later this year, particularly as the fiscal headroom available into the Autumn Budget was much diminished by the passage of a watered down welfare bill earlier this week.

- GBP spot volatility this week serves as a further reminder that there remains a considerable political risk premium on the currency, and surprising political newsflow can still hold sway over both rates markets and the currency. This keeps markets on alert for further upside risks in EUR/GBP, which sees resistance at 0.8670 and 0.8715.

- The USD Index is flat-to-higher headed through the crossover. Markets are looking to test whether prices have successfully formed a base at 96.377 - this week's low - which could prompt a S/T correction and recovery for prices off oversold levels. With Fed pricing for the July meeting indicating 25% chance of a rate cut, the market may look to resolve this pricing one way or the other on today's jobs print.

- The US jobs report is the primary for the US session, brought forward by one day from its usual release due to the July 4th market holidays on Friday. Markets expect the US to have added 106k jobs over the month, but downside risks pervade after ADP Employment Change missed expectations and the market whisper number continues to drift: now at +95k.

OPTIONS: Expiries for Jul03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E2.1bln), $1.1600(E3.8bln), $1.1625(E1.2bln), $1.1650-60(E1.8bln), $1.1700(E2.7bln), $1.1720-25(E1.2bln), $1.1750(E1.1bln), $1.1775(E2.2bln), $1.1800(E5.1bln), $1.1825(E1.2bln), $1.1850(E880mln), $1.1900(E1.2bln)

- USD/JPY: Y142.00($1.1bln), Y143.95-00($1.0bln), Y144.50($540mln), Y145.00-10($1.2bln)

- EUR/GBP: Gbp0.8640-50(E787mln)

- AUD/USD: $0.6500(A$802mln), $0.6600(A$958mln)

- AUD/NZD: N$1.0775(A$597mln)

- USD/CAD: C$1.3600($1.7bln), C$1.3640-45($505mln), C$1.3690-10($736mln)

- USD/CNY: Cny7.4000($3.0bln)

EQUITIES: Short-Term Trend Signals in Eurostoxx 50 Futures Remain Bearish

- Short-term trend signals in Eurostoxx 50 futures remain bearish, however, the recovery from the Jun 23 low appears to be a reversal and the contract is holding on to its most recent gains. Price has traded through the 20- and 50-day EMAs. A clear break of both EMAs would strengthen a reversal theme. This would open 5486.00, the May 20 high and bull trigger. On the downside, a breach of 5194.00, the Jun 23 low, reinstates a bearish theme.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract continues to appreciate. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirms a resumption of the uptrend that started Apr 7. Note too that a key resistance and a bull trigger at 6277.50, the Feb 21 high, has been pierced. Clearance of this hurdle would open the 6300.00 handle. Key support is at the 50-day EMA - at 5987.53.

COMMODITIES: Gold Recovery Highlights Possible False Break of Trendline

- WTI futures maintain a softer tone following the reversal from the Jun 23 high. Wednesday’s gains - for now - appear corrective. Support to watch is the 50-day EMA, at $64.75. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high.

- Recent weakness in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low. A clear break of both trend tools would signal scope for a deeper correction - this would expose $3245.5, the May 29 low. The metal has recovered from Monday’s low and for now, this highlights a possible false trendline break. Stronger gains would refocus attention $3451.3, Jun 16 high. The bear trigger is $3248.7, the Jun 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 03/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 03/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 03/07/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 03/07/2025 | 1230/0830 | *** | Employment Report | |

| 03/07/2025 | 1230/0830 | ** | Trade Balance | |

| 03/07/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/07/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/07/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/07/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 03/07/2025 | 1500/1100 | Atlanta Fed's Raphael Bostic | ||

| 03/07/2025 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill | |

| 03/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 04/07/2025 | 2330/0830 | ** | Household spending | |

| 04/07/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 04/07/2025 | 0645/0845 | * | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Unemployment | |

| 04/07/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/07/2025 | 0800/1000 | * | Retail Sales | |

| 04/07/2025 | 0800/1000 | ECB Elderson Speech At IMF OEDNE/World Bank Meeting | ||

| 04/07/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/07/2025 | 0900/1100 | ** | PPI | |

| 04/07/2025 | 1500/1600 | BOE Taylor Speech On Natural Interest Rate |