MNI US MARKETS ANALYSIS - Equity Weakness Weighs on AUD, NZD

Highlights:

- Dented equity/metals sentiment is weighing on higher beta currencies in the G10, with the likes of AUD, NZD and the Scandies all underperforming.

- The US calendar is heavy with productivity, jobless claims, goods trade, and wholesale inventories scheduled.

- Fed's Miran should be expected to keep his dovish tone, in line with his MNI interview earlier this week. Focus then turns towards tomorrow's December NFP.

US TSYS: Gains Reversed, Labor Updates Watched for Final Pre-NFP Clues

Treasuries have more than reversed gains seen in Asia hours with some downward impetus from EGBs under modest pressure from heavy corporate and sovereign supply. Today’s calendar focus is on various labor updates but with tomorrow’s NFP report looming large.

- Cash yields are now 0-1.5bp higher on the day, with 20s leading the increase.

- TYH6 is one tick above recent session lows of 112-12 (-06+) on reasonable cumulative volumes of 335k.

- Yesterday’s high of 112-22, aided by a small miss for ADP, cleared resistance at 112-19+ (50-day EMA) but stopped short of 112-25+ (Dec 30/31 high). Support meanwhile is still seen at 112-01+ (Dec 23 low) before the bear trigger at 111-29 (Dec 10 low).

- Data: ULCs/Productivity Q3 prelim (0830ET), Weekly jobless claims (0830ET), Revelio labor stats Dec (0830ET), Chicago Fed u/e rate nowcast Dec final (0830ET), International trade Oct (0830ET), Wholesale inventories/sales Oct F/Oct (1000ET), NY Fed Inflation expectations Dec (1100ET), Consumer credit Nov (1500ET)

- Fedspeak: Miran on Bloomberg TV (0800ET), Miran in Athens (1500ET) – see STIR bullet

- Bill issuance: US Tsy $80B each 4W & 8W bill auctions (1130ET)

- Politics: Trump in intelligence briefing (1100ET) and policy meeting (1730ET) – both closed to press

MNI US PAYROLLS PREVIEW: Cleaner, But Not Quite Fogless

- Friday’s nonfarm payrolls report for December (released 0830ET) should see a return to a more normal update, after last month’s dual payrolls figures and single month for the household survey in November with its missing October values and well-touted technical issues clouding it.

- Consensus looks for nonfarm/private payrolls growth of 69k/75k with primary dealer analysts a touch higher for nonfarm. It would see similar monthly rates to those in November after nonfarm payrolls fell heavily in October on federal government deferred resignations showing up.

- There could be a mild drag from colder than usual early December weather.

- The government shutdown shouldn’t have had a direct impact on payrolls in either Nov or Dec although it would have indirectly from contractors affected by it. However, it’s possible that those in the household survey incorrectly identified themselves as unemployed in November with a correction due this month.

- The unemployment rate is seen rounding down to 4.5% after its surprise increase to 4.56% in Nov to extend its latest increase to 4.44% back in September. There’s a wide range to primary dealer analyst views of 4.3-4.7% although risks are generally perceived as tilting higher.

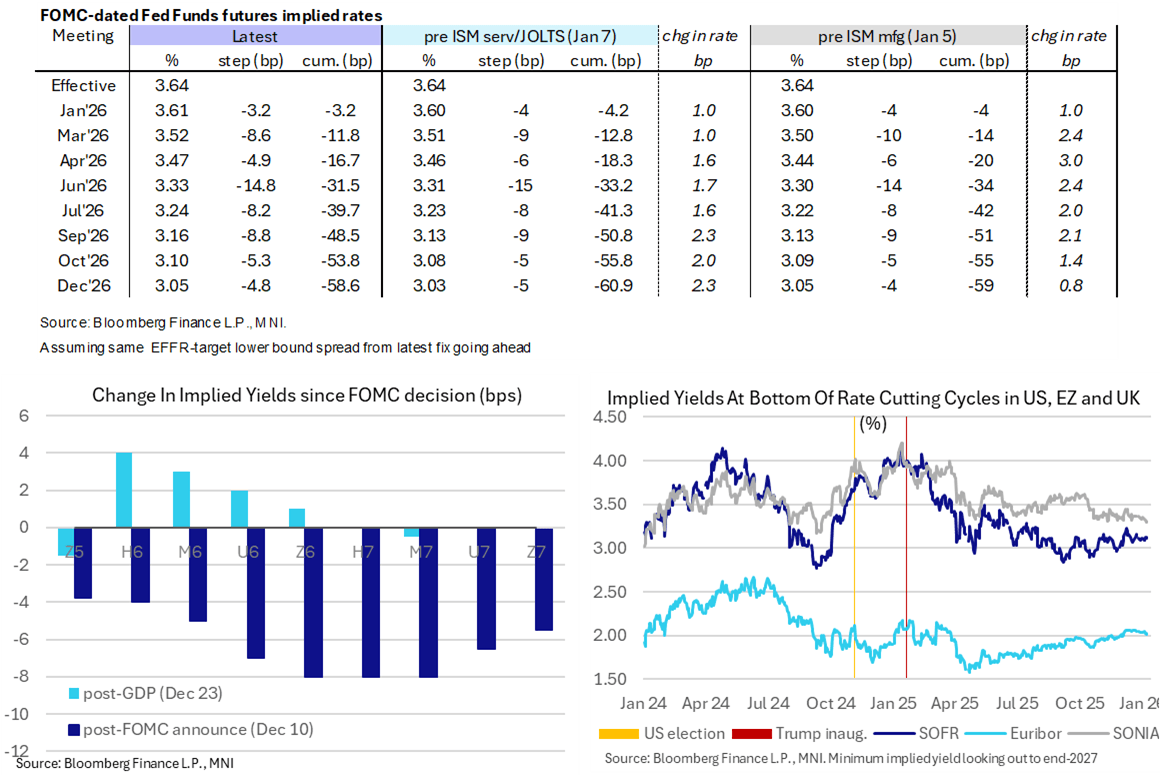

STIR: Just 3bp of Cuts Priced for Jan FOMC, More Pre-NFP Labor Data Today

- Fed Funds implied rates hold most of yesterday’s modest hawkish shift on a stronger than expected ISM services report that was only partly offset by a mixed JOLTS release.

- Cumulative cuts from 3.64% effective: 3bp Jan, 12bp Mar, 16.5bp Apr, 31.5bp Jun, 48.5bp Sep and 58.5bp Dec.

- SOFR futures have pared earlier gains and are now up to 1.5 ticks lower in most 2027 contracts for minor outperformance of Euribor.

- The SOFR terminal implied yield of 3.12% (Z6, +1bp) keeps to recent reasonably tight ranges.

- The NFP report looms large tomorrow but we see further labor updates today with weekly jobless claims, the final Chicago Fed u/e rate nowcast for December and Revelio data.

- Scheduled Fedspeak is limited to two Gov. Miran (voter) appearances, on Bloomberg at 0800ET before speaking at an economic forum in Athens at 1000ET (text tbd). He has spoken recently on the need for substantial rate cuts this year, having told MNI on Jan 5 that he penciled in an implied 150bp of rate cuts in the Dec SEP.

US TSY FUTURES: Mix of Net Long Setting & Short Cover on Wednesday

OI data points to a mix of net short cover (TU & WN) and net long setting (FV, TY, UXY & US) as futures ticked higher on Wednesday, with the latter dominating in curve-wide terms owing to the move in TY positioning.

| 07-Jan-26 | 06-Jan-26 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,522,508 | 4,567,206 | -44,698 | -1,723,983 |

| FV | 6,736,111 | 6,734,736 | +1,375 | +60,142 |

| TY | 5,575,280 | 5,530,541 | +44,739 | +2,984,661 |

| UXY | 2,581,838 | 2,572,660 | +9,178 | +826,796 |

| US | 1,871,687 | 1,868,904 | +2,783 | +386,007 |

| WN | 2,091,415 | 2,092,728 | -1,313 | -240,806 |

| Total | +12,064 | +2,292,816 |

SOFR: Mix of Positioning Swings Seen in Futures on Wednesday

OI data points to a mix of net long cover (SFRZ5) and short setting (SFRH6) in the very front end of the SOFR futures strip on Wednesday, before a mix of net long setting and short cover became apparent in SFRU6 and beyond.

| 07-Jan-26 | 06-Jan-26 | Daily OI Change | Daily OI Change In Packs | ||

| SFRZ5 | 1,468,037 | 1,475,045 | -7,008 | Whites | +37,328 |

| SFRH6 | 1,318,857 | 1,298,554 | +20,303 | Reds | -4,518 |

| SFRM6 | 1,174,618 | 1,172,726 | +1,892 | Greens | -7,495 |

| SFRU6 | 1,242,437 | 1,220,296 | +22,141 | Blues | +898 |

| SFRZ6 | 1,219,618 | 1,194,582 | +25,036 | ||

| SFRH7 | 864,715 | 866,112 | -1,397 | ||

| SFRM7 | 755,007 | 758,442 | -3,435 | ||

| SFRU7 | 768,257 | 792,979 | -24,722 | ||

| SFRZ7 | 849,037 | 864,386 | -15,349 | ||

| SFRH8 | 473,534 | 469,958 | +3,576 | ||

| SFRM8 | 421,547 | 420,456 | +1,091 | ||

| SFRU8 | 370,578 | 367,391 | +3,187 | ||

| SFRZ8 | 348,907 | 346,578 | +2,329 | ||

| SFRH9 | 218,247 | 215,390 | +2,857 | ||

| SFRM9 | 215,510 | 216,288 | -778 | ||

| SFRU9 | 165,969 | 169,479 | -3,510 |

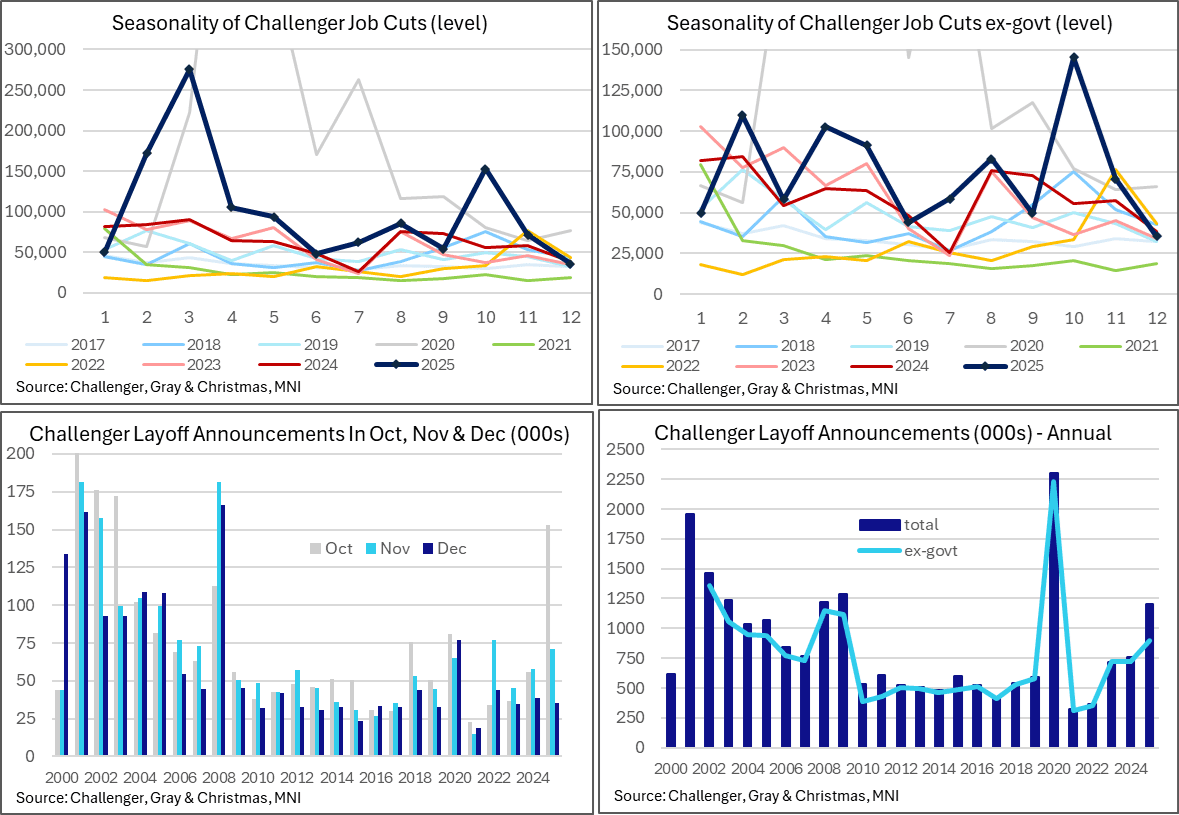

US DATA: Challenger Job Cuts Trimmed in Dec, Strong Increase in 2025 Confirmed

The Challenger jobs report saw a modest Y/Y decline in December as they moderated further after a particularly sharp increase in October. Private job cut announcements increased 24% to nearly 900k across 2025, confirming its highest since 2008 aside from 2020. Warehousing and retail have provided the largest annual increase for private industries whilst an impressive 12 of 30 industries saw lower job cut announcements than a year ago, led by aerospace/defense.

- An early release for the Challenger jobs report in December shows job cut announcements at 35.6k for a -8% Y/Y decline from the 38.8k in Dec 2024.

- It follows the particularly sharp 175% Y/Y increase in Oct to a huge 153k (highest for an October since 2003) and a more measured 24% increase to 71k in Nov.

- Some mixed but not particularly large industry changes on a Y/Y basis in Dec: the largest decline came from food (3.6k vs 10k), health care (1.8k vs 4.3k), tech (0.9k vs 3.3k) and retail (1.0k vs 3.3k) whilst the largest increase came from services (5.7k vs 2.4k) and transportation (3.1k vs 1.0k). Services include companies that provide support to other businesses such as cleaning, staffing, and outsourcing firms.

- Away from monthly noise, the annual total jumped 58% to 1.21mn vs 0.76mn in 2024. The government had an unusually large contribution, adding 217k in March alone on DOGE efforts and 308k for 2025 as a whole.

- Indeed, the private sector reported a more modest but still notable 24% increase to 898k after two years at ~720k. Exclude the 2020 pandemic and this is a fresh high since the 1.1mn in both 2008 and 2009 on this private basis.

- The largest contributors to this private annual increase were warehousing (95k vs 23k in 2024, +72k), retail (93k vs 42k, +51k), services (75k vs 44k,+30k), telecomms (38k vs 11k, +28k), non-profits (29k vs 6k, +23k) and tech (154k vs 134k, +20k).

- 12 of the 30 industries reported by Challenger saw annual declines meanwhile, led by aerospace/defense (4k vs 30k, -25k), autos (32k vs 48k, -16k) and entertainment/leisure (25k vs 35k, -11k).

UK DATA: DMP Data for December Include Something for Everyone

The BOE's Decision Maker Panel (DMP) data for December shows no major moves either higher or lower in the most important categories. There is still something for both the hawks and doves in here: realised wage growth continues to decelerate but only slowly while expected wage growth still remains higher than the around 3.5% levels reported from early Agents' expectations. CPI expectations and perceptions all fell a little, but remain above target. Employment growth was positive in December after some soft recent prints but expected employment growth over the next year is still negative. More details:

- Realised employment growth was 0.5%Y/Y on the single month measure - not as concerning as the -1.8%Y/Y rate seen in November but the 3-month average is now -0.4%Y/Y with the single month print the highest since May. Looking at expected employment growth the single month measure is negative at -0.2%Y/Y, but less so than seen in either November (-0.7%) or October (-0.4%). This is still enough to move the 3-month average down to -0.4%Y/Y, the lowest since October 2020.

- Expected wage growth was 3.7%Y/Y on the single month figure. This compares to 3.6% in November and 3.8% in October. Indeed, it is also a tenth lower than when the same cohort was asked the question in September. This puts the 3-month average at 3.7% (after rising to 3.76% in the 3-months to December and rounding up to 3.85).

- Realised wage growth was 4.3% on the single month print and saw the 3-month average fall a tenth to 4.4%Y/Y.

- Turning to prices, mean expected price growth on the single month measure was 3.5%Y/Y - the same as in November and May; outside of August 2024 we have not seen a single month print below 3.5% since August 2021. The 3-month average ticked down a tenth to 3.6% but has remained in a tight 3.6-3.7% range since May.

- 1/3-year ahead single-month CPI expectations, as well as single month perceptions of current CPI were all lower than in November (and September when this cohort was last asked this question). 3-year ahead CPI expectations on the single month measure have remained between 2.9-3.0% since August. 1-year ahead single month expectations fell to 3.2%Y/Y after four consecutive 3.4%Y/Y prints. Current CPI perceptions fell to 3.6% on the single month measure after three prints at 3.8%.

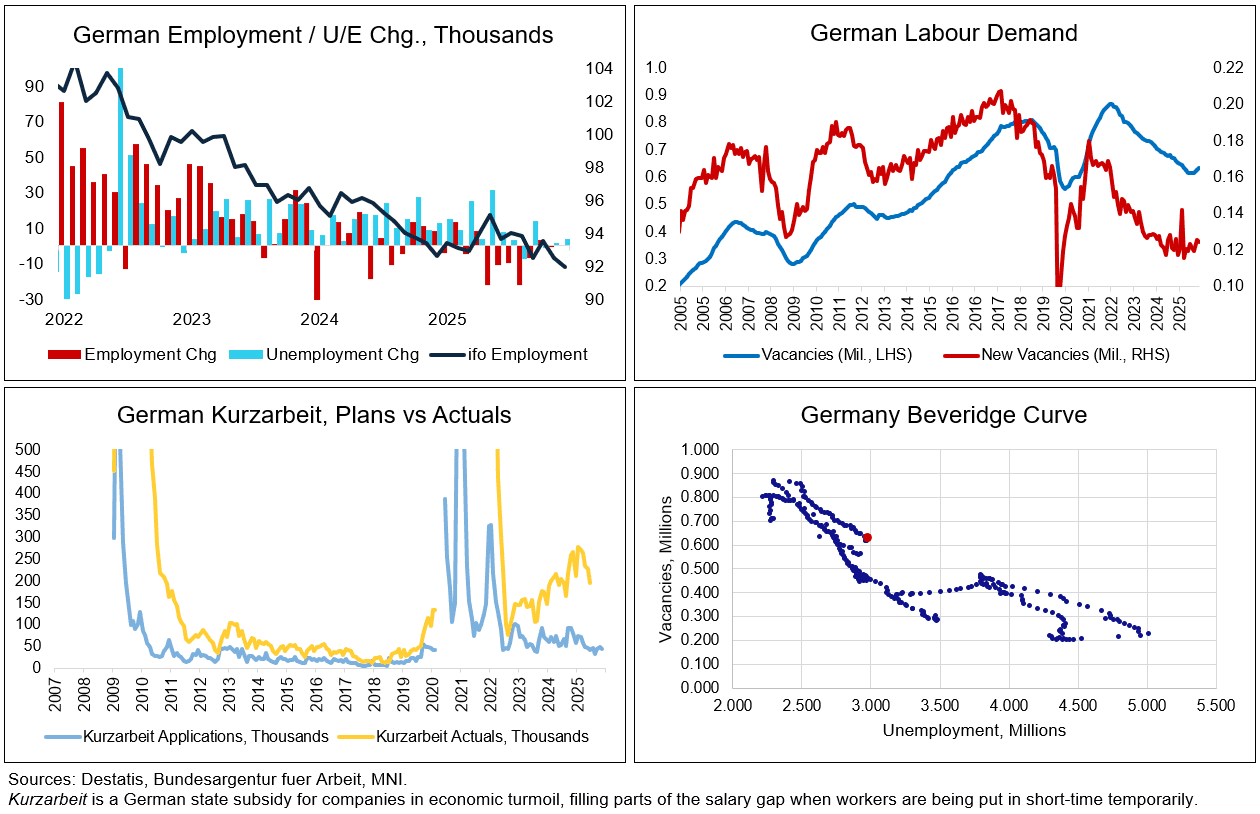

GERMANY DATA: Is the German Labour Market as Soft as Market Participants Think?

Any softening in the German labour market seems slower than previously. There are quite a few individual datapoints pointing towards stability in the quantities side of the German labour market towards year-end. Individually we wouldn't pay too much attention to any of these but collectively these data do challenge the wider narrative that the German economy and in particular the labour market are softening. We have looked at four such indicators below:

- Unemployment rose less than expected in December (+3k vs 5k cons, 1k November) on a seasonally-adjusted basis. The unemployment rate meanwhile, as expected, remained at 6.3% for the tenth consecutive month - by far the longest holding period since it started an uptrend in early 2022.

- Employment was materially unchanged in November (latest), falling 1k over the month, at 45.8mln (third consecutive month of almost no movement, seasonally-adjusted Destatis data).

- The expected number of employees impacted by 'Kurzarbeit' (which has to be reported in advance by companies and can be interpreted as an early indicator for future use of state benefits) has remained roughly stable in recent months (43.5k most recently), while the actual number of employees impacted indeed trended down but the data here here is much delayed (195.4k June).

- Vacancies ticked up for the second consecutive month in December, for the first time since they topped out in 2022, at 633k vs 626k November (August - September all saw the post-pandemic low of 616k). Also new vacancies seem to have at least stabilized.

- In contrast to the above four indicators, the main indicator that is still pointing to weakness is the IFO employment barometer which fell to 91.9 points in December, to its lowest level since May 2020, from 92.5 in November.

FOREX: AUD and NZD Reverse Lower, EURGBP Downtrend Remains Intact

- Geopolitics remain in focus on Thursday after the US's interception of a Russian shadow fleet tanker yesterday as well as ongoing concerns on any action on Greenland. Dented equity/metals sentiment on Thursday is weighing on higher beta currencies in the G10, with the likes of AUD, NZD and the Scandies all underperforming.

- For AUDUSD, 0.4% declines this morning come on the back of comments from RBA Deputy Governor Hauser, who offered little guidance on possible tightening, which was interpreted as dovish at the margin considering the recent hawkish repricing. Corrective price action has narrowed the gap to initial firm support, which intersects at 0.6674, the 20-day EMA.

- Despite stabilising over the past two sessions and edging back towards 0.8700, the sharp recent sell-off in EURGBP confirmed a resumption of the current bear cycle, with moving average studies highlighting a dominant downtrend. This comes amid the BOE's Decision Maker Panel (DMP) data for December showing something for both the hawks and doves in the MPC. Scope remains for a move to 0.8597, the Aug 14 low, while on the upside, resistance to watch is at 0.8736, the 50-day EMA.

- EURCHF meanwhile remains around the 0.9300 handle following December CPI as well as the release of the summary of the December SNB meeting. On balance, it remains that the most likely path for the SNB is to remain on hold for the foreseeable future.

- The US calendar is heavy with productivity, jobless claims, goods trade, and wholesale inventories scheduled, while the EC's economic sentiment index is also due. Fed's Miran should be expected to keep his dovish tone, in line with his MNI interview earlier this week. Focus then turns towards tomorrow's December NFP.

OPTIONS: Expiries for Jan08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1560(E1.0bln), $1.1600-05(E824mln), $1.1650-60(E1.9bln), $1.1670-75(E1.2bln), $1.1800(E1.8bln)

- USD/JPY: Y156.15($2.2bln), Y156.50($849mln), Y157.00($2.9bln), Y158.00($1.6bln), Y159.00($1.2bln)

- EUR/GBP: Gbp0.8565(E594mln)

- AUD/USD: $0.6500(A$1.3bln), $0.6600(A$701mln), $0.6620-25(A$1.0bln), $0.6730(A$1.1bln)

- USD/CNY: Cny7.0469($1.2bln)

EUROPEAN ISSUANCE UPDATE

Portugal syndication: Launch

- E4bln (in line with MNI expectation). Books in excess of E49bln record for Portuguese syndication. Spread set at MS + 34bps (guidance was MS+36bps area).

Italy dual tranche syndication: Launch

- E15bln (even higher than the E12-14bln range MNI expected) of the New 7-year Mar-33 BTP. Books in excess of E150bln, this is a record for an Italian syndication. Spread set at 3.25% Nov-32 BTP +7bps (guidance was +9bps area)

- E5bln WNG of the 4.10% Apr-46 BTP Green. Spread set at 4.45% Sep-43 BTP +8bps (guidance was+10bps area)

Spain auction results:

- E6.285bln sold at today's Bono/Obli auction, just below the top of the E5.5-6.5bln range. E2.814bln of the Jan-30 Bono was sold. Bid-to-cover ratios were a little lower than the previous re-openings for the 2033 and 2043 lines, but the auction sizes were larger.

- Lowest accepted prices were comfortably above pre-auction mid prices across lines

- E2.814bln of the 2.70% Jan-30 Bono. Avg yield 2.508% (bid-to-cover 2.21x).

- E2.012bln of the 3.00% Jan-33 Obli. Avg yield 2.938% (bid-to-cover 2.08x).

- E1.458bln of the 3.45% Jul-43 Obli. Avg yield 3.806% (bid-to-cover 1.87x).

- E726mln of the 1.15% Nov-36 Obli-Ei. Avg yield 1.508% (bid-to-cover 1.90x).

France auction results:

- Top of the E11.5-13.5bln range sold at today's large long-term OAT auction, with E6.866bln of the on-the-run 3.50% Nov-35 OAT sold. The secondary price of the 10-year line fell following publication of the results, but have since moved away from session lows.

- Bid-to-cover ratios were mixed relative to the previous re-openings (2035, 2042 lower; 2040, 2056 higher), but lowest accepted prices were comfortably above pre-auction mid prices across lines.

- E6.866bln of the 3.50% Nov-35 OAT. Avg yield 3.53% (bid-to-cover 1.98x).

- E2.757bln of the 0.50% May-40 OAT. Avg yield 3.95% (bid-to-cover 2.37x).

- E2.679bln of the 3.60% May-42 OAT. Avg yield 4.05% (bid-to-cover 2.12x).

- E1.198bln of the 3.75% May-56 OAT. Avg yield 4.46% (bid-to-cover 3.40x).

EQUITIES: E-Mini S&P Targets Key Resistance at 7014.00, the Oct 30 High

- A bull cycle in Eurostoxx 50 futures remains intact and a fresh cycle high this week reinforces the bull theme. The move higher confirms a resumption of the primary uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on the 6000.00 handle next. On the downside, initial firm support to watch is 5809.54, the 20-day EMA. A pullback would be considered corrective.

- The trend condition in S&P E-Minis remains bullish and price continues to trade above key near-term support at 6771.50, the Dec 18 low. Clearance of this level is required to signal scope for a deeper retracement and would also highlight a possible short-term reversal. For bulls, sights are on key resistance at 7014.00, the Oct 30 high. A move through this hurdle would confirm a resumption of the primary uptrend.

COMMODITIES: Trend Structure for WTI Futures Remains Bearish

- The trend structure in WTI futures remains bearish and recent gains appear to have been corrective. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A clear resumption of the bear leg would signal scope for a move towards $53.77, a Fibonacci projection. Key short-term resistance is $61.25, the Oct 24 high. First resistance is at $58.31, the 50-day EMA.

- The trend structure in Gold is unchanged, it remains bullish and a sharp sell-off late December appears to have been a correction The trend is overbought and any deeper retracement would allow this condition to unwind. First support at $4361.9, the 20-day EMA, has been pierced. A clear break of the average would expose the 50-day EMA at $4225.3. For bulls, a resumption of gains would open $4578.3, a Fibonacci projection.

| Date | GMT/Local | Impact | Country | Event |

| 08/01/2026 | 1330/0830 | *** | Jobless Claims | |

| 08/01/2026 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 08/01/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 08/01/2026 | 1330/0830 | ** | Trade Balance | |

| 08/01/2026 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/01/2026 | 1500/1000 | ** | Wholesale Trade | |

| 08/01/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 08/01/2026 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/01/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 08/01/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 08/01/2026 | 2000/1500 | * | Consumer Credit | |

| 09/01/2026 | 2330/0830 | ** | Household Spending | |

| 09/01/2026 | 0130/0930 | *** | CPI | |

| 09/01/2026 | 0130/0930 | *** | Producer Price Index | |

| 09/01/2026 | 0700/0800 | ** | Trade Balance | |

| 09/01/2026 | 0700/0800 | ** | Industrial Production | |

| 09/01/2026 | 0700/0800 | ** | Private Sector Production m/m | |

| 09/01/2026 | 0700/0800 | *** | CPI Norway | |

| 09/01/2026 | 0745/0845 | * | Industrial Production | |

| 09/01/2026 | 0745/0845 | ** | Consumer Spending | |

| 09/01/2026 | 0800/0900 | ** | Industrial Production | |

| 09/01/2026 | 0800/0900 | ** | Unemployment | |

| 09/01/2026 | 0900/1000 | * | Retail Sales | |

| 09/01/2026 | 1000/1100 | ** | EZ Retail Sales | |

| 09/01/2026 | 1200/0700 | ** | Brazil Final CPI | |

| 09/01/2026 | 1245/1345 | ECB Lane Keynote at Danish Economy Conference | ||

| 09/01/2026 | 1330/0830 | *** | Labour Force Survey | |

| 09/01/2026 | 1330/0830 | *** | Housing Starts | |

| 09/01/2026 | 1330/0830 | *** | Employment Report | |

| 09/01/2026 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 09/01/2026 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 09/01/2026 | 1500/1000 | Minneapolis Fed's Neel Kashkari | ||

| 09/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/01/2026 | 1835/1335 | Richmond Fed's Tom Barkin |