MNI US MARKETS ANALYSIS - Equities Hold Bounce

Highlights:

- Quiet start to week, with cash Treasury trade closed for Columbus Day

- Equities hold bounce after Trump moderates China language over the weekend

- AUD bid, JPY offered on reversal in risk appetite

US TSYS: Cash Closed For Columbus Day, On Headline Watch

- Treasury futures have modestly pulled back off highs seen at Friday’s close after President Trump threatened new 100% tariffs on China and the imposition of its own export controls on “any and all critical software” on Nov 1 following China’s earlier export curbs on its rare earth metals.

- The threats were subsequently somewhat downplayed over the weekend, prompting this paring of moves, but Treasuries remain firmer on net.

- Cash markets are closed today for the Columbus Day holiday but with a full session for Globex.

- The holiday likely limits volumes later on and Trump flies back from the Middle East. Focus will be on any further US-China headlines plus a mention for Philly Fed’s Paulson, albeit overshadowed by Powell’s NABE appearance tomorrow.

- TYZ5 trades at 113-01+ (-03) on cumulative volumes of 265k, higher than some recent overnight sessions but still on the low side.

- Friday saw a high of 113-09, opening 113-12 (Sep 18 high) after which lies the bull trigger at 113-29 (Sep 11 high). Support meanwhile is seen at 112-14 (50-day EMA).

- Data: None scheduled

- Fedspeak: Paulson (1255ET) – see STIR bullet

- No issuance

- Politics: Trump in Middle East Peace Ceremony, Egypt (0730ET), Trump departs Egypt en route to The White House (1000ET with travel pool).

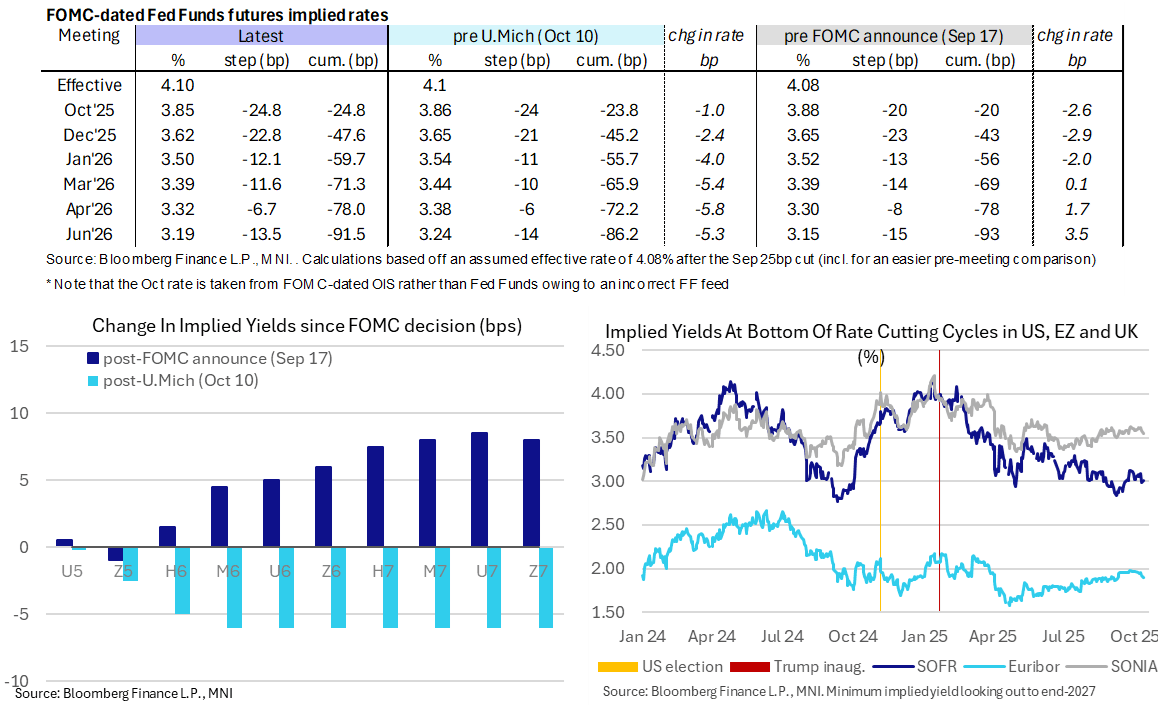

STIR: Friday Risk-Off Only Somewhat Pared, Paulson’s First Comments Watched

- Fed Funds implied rates have lifted off late Friday lows after Trump on Sunday somewhat downplayed Friday’s tariff threats on China, although they still hold the majority of Friday’s sharp risk-off move.

- The Dec 2025 implied rate for example sits close to levels seen after the surprisingly weak ADP report two weeks ago.

- Cumulative cuts from 4.10% effective: 25bp Oct, 47.5bp Dec, 59.5bp Jan, 71.5bp Mar, 78bp Apr and 91.5bp Jun.

- SOFR futures are modestly lower from Friday’s close, -0.015 through H6-U6 before tapering to -0.005 in the Z7.

- The SOFR implied terminal yield of 3.005% (-1.5bp) continues to flicker between the Z6 and H7, currently implying ~110bp of cuts ahead.

- Today’s Fedspeak is on the thin side, and clearly overshadowed by tomorrow’s appearance from Powell, but we’ll still watch it closely to hear Philly Fed’s Paulson (’26 voter) first remarks on monetary policy since replacing Harker when he retired in June. She delivers a keynote address on the economic outlook at the NABE annual meeting (text + Q&A).

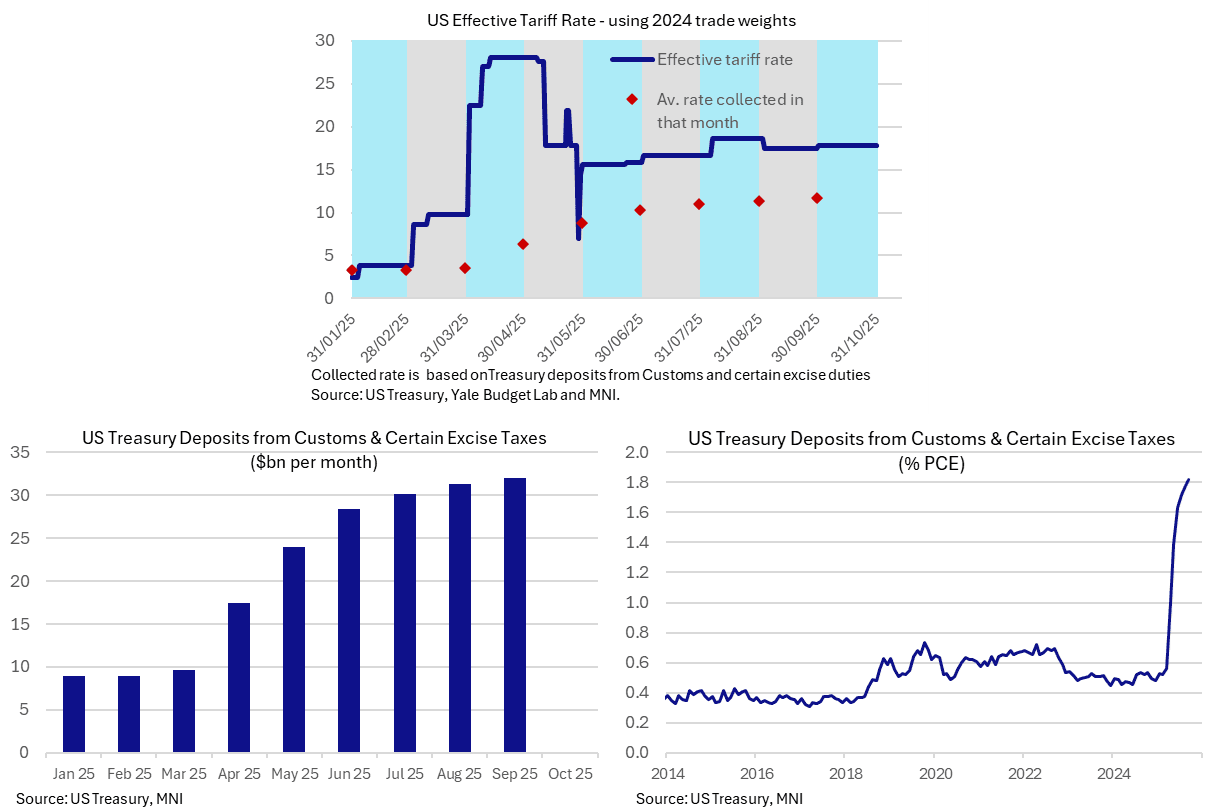

TARIFFS: Taking Stock Of Realized Tariff Rates After US-China Tensions (1/2)

- President Trump on Friday threatened new 100% tariffs on China and the imposition of its own export controls on “any and all critical software” on Nov 1 following China’s earlier export curbs on its rare earth metals.

- Trump has since appeared to downplay these threats, posting on Truth Social on Sunday “Don’t worry about China, it will all be fine! Highly respected President Xi just had a bad moment.”

- The speed with which apparent watering down of rhetoric has come after high tariff threats suggests low likelihood of effective tariff rates pushing north of 25% as was the case in April after Chinese retaliation to reciprocal tariffs sparked a surge in the China tariff rate to 145%. This of course is in a static sense as such levels of tariff rates are broadly seen as halting trade between the two countries.

- Nevertheless, it’s worth taking stock of latest tariff rates from both proposed rates and actual collection of customs duties.

- The latest Yale Budget Lab report from Sep 26 had an effective tariff rate of 17.4% at end-Sept, expected to have increased to 17.9% into October.

- Customs duties meanwhile have seen a stalling in progress in recent months, up to $32bn in September ($384bn annualized) after $31.3bn in Aug and $30.0bn in Jul. For context, this was in the $8-9bn region prior to the second Trump administration.

- It leaves an implied tariff rate either side of 11.5% depending on which period of trade you use for the denominator vs closer to 11.25% in Aug or 3.0% back in Dec.

- Alternatively, customs duties have increased by 1.3pps to ~1.8% of personal consumption expenditure, with most of this cumulative increase having come by June when it was worth an additional 1.1pp. These figures give an idea of the system-wide impact, whilst Goldman Sachs analysis in the second part of this post goes into detail as to how much might actually show up in consumer prices.

TARIFFS: Goldman On Tariff Passthrough Estimates (2/2)

- Goldman Sachs write that the customs duties implied US effective tariff rate “had risen by 9pp through August, or by nearly 11pp net of frontloading effects.”

- “Following recent tariff increases on some products and countries and hints of exemptions for others, we now expect it to rise by 12pp in total in 2025 and by another 3.5pp or 15.5pp in total through 2026, a bit less than we previously assumed.”

- They estimate that foreign exporters are “absorbing some of the tariff cost, unlike in 2019, though some of the decline likely reflects underreporting of import value to evade tariffs”. Meanwhile, passthrough to consumer prices has reached “55% after six months, meaningfully lower than at the same point in 2019.”

- They estimate that “US consumers would eventually absorb 55% of tariff costs, US businesses would absorb 22%, foreign exporters would absorb 18%, and 5% would be evaded.” US businesses are likely bearing a larger share currently though.

- GS estimate that “tariff effects have raised core PCE prices by 0.44% so far this year”. Their forecast, which assumed peak passthrough will rise from 55% to 70% “implies a further 0.6% boost from tariffs through next year”. That leaves core PCE inflation at 3.0% Y/Y in Dec 2025 and 2.4% in Dec 2026.

- To give an idea of sensitivity, core PCE inflation would be 3.1% and 2.7% respectively if passthrough peaks at 100%, or 2.9% and 2.2% if passthrough holds at 55%.

SOFR: Long Setting & Short Cover Seen In Futures On Friday

OI data points to net long setting dominatin in the whites, reds and blues, while net short cover was more prominent in the greens as the SOFR futures strip bull flattened on Friday in reaction to the increase of Sino-U.S. trade tensions.

| 10-Oct-25 | 09-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,430,329 | 1,424,311 | +6,018 | Whites | +8,794 |

SFRZ5 | 1,531,713 | 1,531,691 | +22 | Reds | +37,014 |

SFRH6 | 1,172,773 | 1,187,832 | -15,059 | Greens | -4,770 |

SFRM6 | 1,033,596 | 1,015,783 | +17,813 | Blues | +10,430 |

SFRU6 | 1,008,351 | 990,203 | +18,148 |

|

|

SFRZ6 | 1,018,275 | 1,004,947 | +13,328 |

|

|

SFRH7 | 806,967 | 791,555 | +15,412 |

|

|

SFRM7 | 776,549 | 786,423 | -9,874 |

|

|

SFRU7 | 678,414 | 678,380 | +34 |

|

|

SFRZ7 | 746,480 | 759,000 | -12,520 |

|

|

SFRH8 | 432,431 | 433,217 | -786 |

|

|

SFRM8 | 374,639 | 366,137 | +8,502 |

|

|

SFRU8 | 301,608 | 298,323 | +3,285 |

|

|

SFRZ8 | 333,395 | 331,185 | +2,210 |

|

|

SFRH9 | 194,386 | 191,742 | +2,644 |

|

|

SFRM9 | 171,839 | 169,548 | +2,291 |

|

|

US TSY FUTURES: Net Long Setting Further Out The Curve Dominated On Friday

OI data points to a mix of net long setting (TU, TY, US & WN) & short cover (FV & UXY) as Tsy futures bull flattened on Friday.

- The net long setting in US & WN futures tilted the curve-wide positioning bias in that direction.

| 10-Oct-25 | 09-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,608,833 | 4,588,576 | +20,257 | +791,916 |

FV | 6,738,869 | 6,763,480 | -24,611 | -1,076,876 |

TY | 5,393,544 | 5,388,428 | +5,116 | +347,166 |

UXY | 2,451,982 | 2,457,634 | -5,652 | -514,160 |

US | 1,919,327 | 1,908,839 | +10,488 | +1,358,314 |

WN | 2,062,865 | 2,044,211 | +18,654 | +3,557,670 |

|

| Total | +24,252 | +4,464,031 |

UK FISCAL: Weekend roundup of Budget press stories

- Bridget Phillipson, the Education Secretary who is running for Labour Deputy Leader, said on Sky News in an interview over the weekend that she was "confident that we as a Government will do the right thing by children growing up in poverty in our country." She followed by saying that "There's an urgency to this. With every year that passes more children are moving to poverty because of the two-child limit." Note that this policy is expected to cost more than GBP3bln and is not included in most estimates of the fiscal shortfall of around GBP30bln that Chancellor Reeves is expected to be needing to raise in the 26 November Budget.

- There were also a number of reports that Reeves is looking to increase fiscal headroom above the c. GBP10bln seen in the last two fiscal events. The Guardian is reporting a Treasury source stating "We would like more headroom. We want to try to insulate ourselves better against the volatility in the bond markets." More headroom is something that the MNI Markets team has been advocating for some time. If headroom is not sufficient then even small economic disappointments can lead to concerns that taxes will need to increase further down the line which creates uncertainty for both consumers and businesses (potentially delaying investment).

- There are reports that the Treasury is considering responding to farmers' concerns through a proposal put forward by CenTax over the inheritance tax reforms. At present the reforms are due to kick in at 20% after the first GBP1mln (half the normal 40%) but the report notes that thresholds of between GBP1.5-5.0mln may be considered with the standard 40% tax rate applicable after that. This would undoubtedly be a popular policy in rural communities.

- There are lots of opinion pieces on how stamp duty and council tax could be reformed (with the former particularly in focus after Badenoch stated that the Conservatives would abolish it). But at present it is unclear whether any reforms to either of these taxes are seriously under consideration.

- Furthermore, see our bullet earlier on the IFS options for the budget (7:45BST).

UK FISCAL: IFS Outlines Options for the Budget

- There has been a lot of focus in the weekend press on the IFS' "Options for Tax Increases" document that was published in full overnight (full text here)

- Some of the options included an additional tax on income separate to income tax and employee NIC (and hence not technically breaking the manifesto but clearly breaking the spirit). We note that this would be similar to the "Health and Social Care Levy" that was announced in September 2021 under the Johnson/Sunak premiership. In its first year (from April 2022) it was implemented as a 1.25ppt increase to employee NIC with the intention that it would apply to those 65+ from April 2023 when it was collected as the new levy. However, the levy was cancelled in October 2022 before its full implementation with the temporary NIC increase also reversed under the Truss/Kwarteng government.

- The IFS said that restricting tax relief on pension contributions should be avoided and noted that reforming the lump sum or levying some NIC on employers contributions was preferable. We would caution a little here that if firms had to pay some level of employers NICs on pension contributions it would be very unpopular following the employer NIC increase in April, and would likely be passed through to higher output prices and higher inflation once again.

- The IFS also "caution against introducing an annual wealth tax" stating that there are other, better options, such as removing the capital gains death exemption and more closely aligning capital gains taxes with income taxes. We note that larger increases to capital gains taxes were reportedly said to potentially reduce revenue in previous OBR costings.

- The IFS also sums this all up by saying that "It would be difficult, but not impossible, for the Chancellor to raise tens of billions of pounds more revenue without breaking Labour’s manifesto promise... Just because large sums could be raised elsewhere does not mean it would be sensible. Many of the tax-raising options outside the ‘big three’ would have particularly damaging effects on growth and welfare."

FOREX: AUD Rallies, JPY Offered on Smoother China Language

- US markets are partially closed for Columbus Day on Monday, leaving no cash Treasury trade - which should also limit volumes and price action across currency markets. With the US still in government shutdown, data releases this week are further limited: although the BLS confirmed on Friday that this Wednesday's scheduled release of US CPI will go ahead on October 24th. Modestly stronger risk sentiment today has been fueled by the more complementary tone from Trump on China over the weekend, keeping low-yielders on the back foot while Antipodean currencies outperform.

- BoE's Greene & Mann are both set to appear today in speeches that could set the tone for UK trade this week. No fewer than 14 MPC appearances are on the schedule, and with no rate cut fully priced until April next year, markets will look to see if any speeches suggest this timeline can be brought forward, particularly if this Tuesday's jobs data comes in weaker-than-expected.

- Into the MPC speeches and the run of UK data, GBP/USD is off last week's lows, but inside the Friday range. This leaves the 1.3262 low as key support this week, a break below which exposes the 200-dma of 1.3178 and levels last seen at the beginning of August. It remains difficult to see a protracted GBP/USD sell-off absent a move in the USD however, and with an October Fed rate cut fully priced, there may be limits on how much further the greenback can rally from here.

- As was the case last Monday, the JPY is the weakest currency in G10. USD/JPY is back above 152.00, but a further rally above 152.64 will be needed to erase the sell-off triggered by Trump's threats to raise tariffs on China on Friday. Politics remains a key driver of the currency, with opposition parties set to meet tomorrow to discuss the collapse of the governing coalition last week. These meetings could help determine whether Takaichi goes ahead with a minority government, or looks to bring forward elections.

- The AUD/USD bounce, triggered by Trump's softer China language over the weekend, has the pair again either side of the 0.6532 100-dma. The 0.6560 50-day EMA marks the next upside level, which would go further in erasing last week's sell-off. This comes after Friday's support breaks undermined a recent bullish theme, potentially signaling scope for a deeper retracement towards key support at 0.6415, the Aug 21 and 22 low.

- Further newsflow and tone by both US and Chinese administrations in terms of rare earths and trade have the potential to induce volatility in the coming sessions. Polymarket odds for the US government to remain shut down until at least October 31st rose to above 2/3 over the weekend - suggesting that most official US data may be set for a continued absence.

OPTIONS: Expiries for Oct13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E804mln), $1.1570-75(E931mln), $1.1650(E772mln), $1.1700-15(E1.4bln), $1.1750-60(E3.6bln)

- USD/JPY: Y151.00($757mln)

- EUR/JPY: Y174.95-00(E560mln)

- AUD/USD: $0.6550-55(A$930mln)

EQUITIES: Recent Sharp Sell Off in E-Mini S&P Considered Corrective, For Now

- The trend condition in Eurostoxx 50 futures is unchanged, the direction is up and the latest pullback is - for now - considered corrective. The key support zone to monitor is 5549.76 - 5474.21, the area between the 20- and 50-day EMAs. A clear break of the 50-day average would highlight a stronger reversal. On the upside, the bull trigger has been defined at 5689.00, the Oct 2 high. Clearance of this hurdle would confirm a resumption of the uptrend.

- A sharp sell-off in S&P E-Minis on Friday is - for now - considered corrective. The contract has found support below the 50-day EMA, currently at 6598.55. Friday’s low of 6940.25 has been defined as a key short-term support. Note that moving average studies remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Sep 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

COMMODITIES: Friday's Move Lower in WTI Futures Confirms Resumption of Bear Leg

- A bearish theme in WTI futures remains intact. Friday’s move down confirmed a resumption of the bear leg - support at $60.40, the Oct 2 low, has been breached. This highlights an extension of the bearish price sequence of lower lows and lower highs. The move down opens $57.50 next, the May 30 low. On the upside, initial key resistance is at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal.

- A bull cycle in Gold remains intact and today’s fresh cycle marks a bullish start to this week’s session. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4100.00 handle, and $4113.5, a Fibonacci projection point. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support to watch is $3836.5, 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 13/10/2025 | 1105/1205 | BOE Greene at Society of Professional Economists Conference | ||

| 13/10/2025 | - | ECB Lagarde and Cipollone at IMF/World Bank Meetings | ||

| 13/10/2025 | 1655/1255 | Philly Fed's Anna Paulson | ||

| 13/10/2025 | 1910/2010 | BOE Mann in MonPol Panel, National Association of Business Economists | ||

| 14/10/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0750/0950 | ECB Cipollone Speech on Digital Euro | ||

| 14/10/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 14/10/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 14/10/2025 | - | *** | Money Supply | |

| 14/10/2025 | - | *** | New Loans | |

| 14/10/2025 | - | *** | Social Financing | |

| 14/10/2025 | - | ECB Lagarde and Cipollone at G20 Meeting | ||

| 14/10/2025 | 1200/1300 | BOE Taylor Remarks and Fireside Chat at University of Cambridge | ||

| 14/10/2025 | 1230/0830 | * | Building Permits | |

| 14/10/2025 | 1245/0845 | Fed Governor Michelle Bowman | ||

| 14/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/10/2025 | 1610/1210 | BOC Sr Deputy Rogers fireside talk in Vancouver | ||

| 14/10/2025 | 1620/1220 | Fed Chair Jerome Powell | ||

| 14/10/2025 | 1700/1800 | BOE Bailey Fireside Chat at Institute of International Finance | ||

| 14/10/2025 | 1925/1525 | Fed Governor Christopher Waller | ||

| 14/10/2025 | 1930/1530 | Boston Fed's Susan Collins |