MNI US MARKETS ANALYSIS - Data Outage, Early Close Crimps Vol

Highlights:

- CME data outage leaves futures, options trade disrupted

- Early US close, market disruption leaves volumes light, flow muted

- Canada GDP data should confirm tepid bounce in growth for Q3

CROSS ASSET: CME Outage Persists, Exchange Will Notify on Pre-Open

- CME continues to advise that: "Due to a cooling issue at CyrusOne data centers, our markets are currently halted. Support is working to resolve the issue in the near term and will advise clients of Pre-Open details as soon as they are available."

- As a result, there are broad outages across US futures and options trading, impacting markets as diverse as US bond futures, commodities and equity index futures. As such, prices are absent for futures markets across Treasuries, crude oil and equity index futures.

- These technical issues are further reducing liquidity and volumes on what was already a quieter-than-average session. This will likely stymie the lagged return for US markets today, which are set for an early close due to the Thanksgiving holidays. There remains no schedule or indication for when trading across US equity and Treasury futures will resume.

CROSS ASSET: MNI Tech Trend Monitor - November Refresh

- We refresh our Global Tech Trend Monitor, adding longer-term techs for USDMXN, EURHUF, Bitcoin and the USD Index as well as refreshing levels for Spot Gold, Silver, USDJPY, UK Gilt Yields and the Europe Banking Stock Index (SX7E).

See full document here: https://emedia.marketnews.com/marketnewsintl/TechTrendMonitorNov.pdf

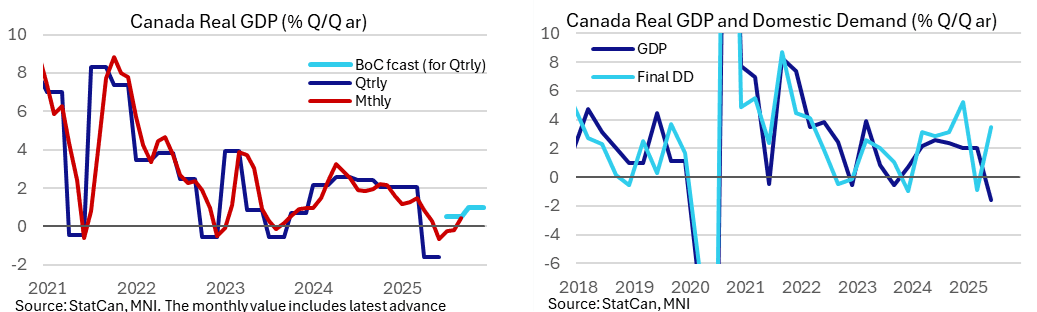

CANADA DATA: GDP Expected To Confirm Tepid Bounce In Q3 After Q2 Trade Hit

Tomorrow sees real GDP growth for Q3 and separate monthly data for the Sep/Oct advance report. The BoC puts more weight on the expenditure-based quarterly data, although the production-based monthly data still offer a valuable idea of momentum into Q4. However, both are likely more susceptible than usual to US trade-related revisions.

- Canadian GDP data is released tomorrow at 0830ET for Q3 along with the monthly report for September and its advance estimate for October.

- Bloomberg consensus eyes real GDP growth of 0.5% annualized in Q3, with a range of -0.4% to 0.8%, after a heavy decline of -1.6% in Q2 when net exports dragged ~7.5pp from GDP.

- Six of the seven largest Canadian banks all look for 0.5% (BMO, Desjardins, National, RBC, Scotia and TD), with CIBC the exception at 0.7%. RBC doesn’t currently show in the Bloomberg survey.

- As for the monthly series, Bloomberg consensus of 0.2% M/M sees upside risk to the 0.1% indicated in last month’s advance estimate, following upward revisions to manufacturing and wholesale trade.

- It follows two noisier months with -0.3% M/M in Aug and 0.3% M/M in Jul, but the prior trend had been weaker with three consecutive -0.1% M/M prints through Apr-Jun.

- Analyst estimates on Bloomberg range from -0.1% to 0.2% M/M, with seven estimates for 0.2%, but RBC is again not included here and looks for a stronger 0.3% M/M.

- As for potential advance estimates for October, CIBC pencil in a “small 0.1% increase” on the back of “little information regarding October available as yet”.

- The BoC at last month’s MPR pencilled in a 0.5% increase in Q3 before 1.0% in Q4. More broadly, it sees real GDP growth of 0.5% Y/Y in 4Q25 before 1.6% in both 4Q26 and 4Q27.

- Helping put these numbers into context, the BoC estimates potential output growth of 1.6% in 2025, 1.0% in 2026 and 1.3% in 2027.

- The Bank opted for a hawkish cut last month, signalling pause ahead with the overnight rate of 2.25% deemed “about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment."

- BoC-dated OIS has nothing priced for the Dec 10 meeting although there is nearly another half a 25bp cut priced out in mid-2026. We suspect risk to nearer-term pricing from this release alone is to the downside.

GERMANY: Pensions Package Freezes Current Payments Through 2031

The German coalition has agreed on passing a pension package freezing the current level of payments through 2031 according to matching local media reports, according to Handelsblatt.

- The pension reform has been on the edge of failing internally in CDU as backbench support for the bill faded.

- The approval should stabilize the coalition for now after labour minister Bas (SPD) indirectly warned against a breakup of the coalition should CDU not manage to keep mentioned subgroups voting in favour, letting the reform fail.

- "In addition, the coalition partners have drafted a resolution calling for work to begin on a further pension package. In order to ease the burden on the younger population and probably also to accommodate the young group within the Union, which recently rebelled against the coalition's pension plans, the capital markets are also to play a greater role in old-age provision in future. The federal government is to use a E10 billion share package to support wealth accumulation. These are to be federal government holdings." - HB

FOREX: USDJPY Holds Close to Unchanged This Week, Ueda Speech Monday

- Perhaps to be expected given the US Thanksgiving holiday, USDJPY has traded in a much more contained manner this week, remaining within a 1% range. Spot is currently down just 10 pips from last Friday’s close, as firmer risk sentiment has been offset by a softening dollar.

- Overall, the trend set-up in USDJPY remains bullish. The pair has recently entered overbought territory and a deeper retracement, if seen, would allow this condition to unwind. We assessed the longer-term USDJPY trend more in the MNI Tech Trend Monitor sent out earlier today: https://mni.marketnews.com/48nuO63

- Late Thursday, BOJ board member Asahi Noguchi reinforced the view that a near-term interest rate hike is in the pipeline while avoiding a clear hint that it will come in December – very much in line with recent communication from other BOJ officials. All focus turns to BOJ Governor Ueda’s speech to business leaders in Nagoya City on Monday.

- November Tokyo CPI did little to move the needle overnight. Headline rose 2.7%y/y, in line with the consensus (while the Oct outcome was also revised down to this level, from 2.8%). The job to applicant ratio ticked down further to 1.18, versus 1.20 forecast. The continued trend decline in the job-to-applicant ratio points to further upside in the unemployment rate, all else equal. This will be a watch point for the authorities, given on-going focus around positive real wage gains and the importance of this in sustainably reaching the 2% inflation target.

FOREX: Greenback Tilts Higher Friday, GBPUSD Edges Back Towards 1.3200

- Despite remaining below the 100.00 mark, the USD index has been drifting higher on Friday morning, paring a portion of this week’s downswing. This has helped the likes of EUR and GBP to underperform across G10, while NZD trims its impressive post-RBNZ advance. The moderate greenback optimism has also prompted a punchy turnaround for gold, falling from overnight highs of $4,193 to session lows of $4,155 around 8am London.

- For NZDUSD, the pair kicked on through its 20-day EMA resistance this week, but importantly has found solid supply at the next touted resistance zone around 0.5725/30, which represents both the 50-day and prior trendline support turned resistance.

- It is worth flagging that yesterday’s EURUSD candle pattern is a doji - a potential reversal signal, and highlighting that this week’s recovery appears corrective – for now. Short-term technical parameters appear well defined; key short-term resistance to monitor at 1.1656, the Nov 13 high and key support at 1.1469, the Nov 5 low.

- Concerns surrounding the degree of fiscal tightening that will ultimately be deployed and likely BOE easing in December remain headwinds for the pound. GBPUSD highs of 1.3269 Thursday closely coincided with a test of 50-day EMA resistance, and today’s move back towards 1.3200 keeps the dominant downtrend in place for now.

- The highlight on the Economic calendar is Canada GDP, while volumes may remain on the low side owing to the US Thanksgiving holiday.

OPTIONS: Expiries for Nov28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1570(E779mln), $1.1600(E799mln)

- USD/JPY: Y154.00($1.3bln), Y156.50($516mln), Y157.80($510mln)

- GBP/USD: $1.3200(Gbp758mln)

- AUD/USD: $0.6545-50(A$545mln)

EQUITIES: E-Mini S&P Back Above 20-, 50-Day EMAs Following This Week's Recovery

- The move higher in Eurostoxx 50 futures this week undermines a recent bearish theme and the contract is holding on to its gains. The contract has traded above the 20- and 50-day EMAs, signalling scope for a stronger recovery near-term. A continuation would open 5691.30 and 5742.40, Fibonacci retracement points. For bears, a reversal lower would instead expose the key S/T support and bear trigger at 5475.00, the Nov 21 low.

- S&P E-Minis are holding on to their latest gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

COMMODITIES: First Short-Term Bull Trigger for Gold at $4245.23

- Recent weakness in WTI futures highlights a bearish theme. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. The contract has recovered from its latest low, resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- The trend condition in Gold remains bullish and the bear phase between Oct 20 and 28 appears to have been a correction. This allowed a recent overbought condition to unwind. Key support to watch lies at the 50-day EMA, at $3981.6. Clearance of this EMA would signal scope for a deeper retracement. The first short-term bull trigger has been defined at $4245.23, the Nov 13 high.

| Date | GMT/Local | Impact | Country | Event |

| 28/11/2025 | 0700/0800 | *** | GDP | |

| 28/11/2025 | 0700/0800 | ** | Retail Sales | |

| 28/11/2025 | 0700/0800 | ** | Import/Export Prices | |

| 28/11/2025 | 0700/0800 | ** | Retail Sales | |

| 28/11/2025 | 0745/0845 | *** | HICP (p) | |

| 28/11/2025 | 0745/0845 | ** | PPI | |

| 28/11/2025 | 0745/0845 | *** | GDP (f) | |

| 28/11/2025 | 0745/0845 | ** | Consumer Spending | |

| 28/11/2025 | 0745/0845 | Payrolls | ||

| 28/11/2025 | 0800/0900 | *** | HICP (p) | |

| 28/11/2025 | 0800/0900 | ** | KOF Economic Barometer | |

| 28/11/2025 | 0800/0900 | *** | GDP | |

| 28/11/2025 | 0855/0955 | ** | Unemployment | |

| 28/11/2025 | 0900/1000 | *** | GDP (f) | |

| 28/11/2025 | 0900/1000 | *** | Bavaria CPI | |

| 28/11/2025 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 28/11/2025 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 28/11/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 28/11/2025 | 1000/1100 | *** | Italy Flash Inflation | |

| 28/11/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 28/11/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 28/11/2025 | 1330/0830 | *** | GDP - Canadian Economic Accounts | |

| 28/11/2025 | 1330/0830 | *** | Gross Domestic Product by Industry | |

| 28/11/2025 | 1330/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 28/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 28/11/2025 | 1600/1100 | Finance Dept monthly Fiscal Monitor (expected) |