CANADA DATA: GDP Expected To Confirm Tepid Bounce In Q3 After Q2 Trade Hit

Tomorrow sees real GDP growth for Q3 and separate monthly data for the Sep/Oct advance report. The BoC puts more weight on the expenditure-based quarterly data, although the production-based monthly data still offer a valuable idea of momentum into Q4. However, both are likely more susceptible than usual to US trade-related revisions.

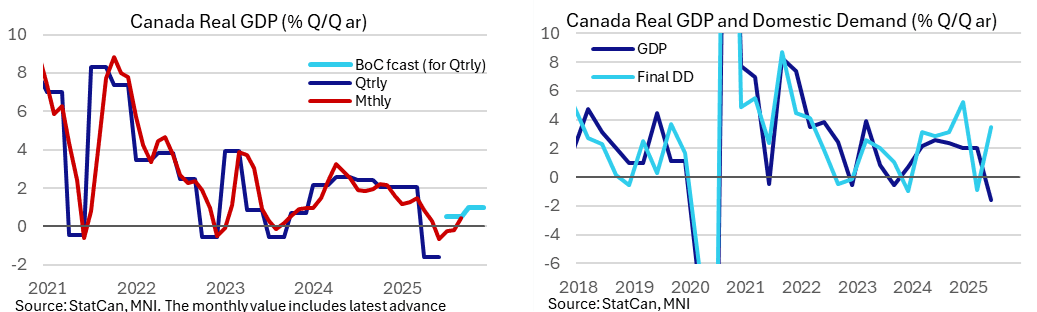

- Canadian GDP data is released tomorrow at 0830ET for Q3 along with the monthly report for September and its advance estimate for October.

- Bloomberg consensus eyes real GDP growth of 0.5% annualized in Q3, with a range of -0.4% to 0.8%, after a heavy decline of -1.6% in Q2 when net exports dragged ~7.5pp from GDP.

- Six of the seven largest Canadian banks all look for 0.5% (BMO, Desjardins, National, RBC, Scotia and TD), with CIBC the exception at 0.7%. RBC doesn’t currently show in the Bloomberg survey.

- As for the monthly series, Bloomberg consensus of 0.2% M/M sees upside risk to the 0.1% indicated in last month’s advance estimate, following upward revisions to manufacturing and wholesale trade.

- It follows two noisier months with -0.3% M/M in Aug and 0.3% M/M in Jul, but the prior trend had been weaker with three consecutive -0.1% M/M prints through Apr-Jun.

- Analyst estimates on Bloomberg range from -0.1% to 0.2% M/M, with seven estimates for 0.2%, but RBC is again not included here and looks for a stronger 0.3% M/M.

- As for potential advance estimates for October, CIBC pencil in a “small 0.1% increase” on the back of “little information regarding October available as yet”.

- The BoC at last month’s MPR pencilled in a 0.5% increase in Q3 before 1.0% in Q4. More broadly, it sees real GDP growth of 0.5% Y/Y in 4Q25 before 1.6% in both 4Q26 and 4Q27.

- Helping put these numbers into context, the BoC estimates potential output growth of 1.6% in 2025, 1.0% in 2026 and 1.3% in 2027.

- The Bank opted for a hawkish cut last month, signalling pause ahead with the overnight rate of 2.25% deemed “about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment."

- BoC-dated OIS has nothing priced for the Dec 10 meeting although there is nearly another half a 25bp cut priced out in mid-2026. We suspect risk to nearer-term pricing from this release alone is to the downside.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MACRO ANALYSIS: US Macro Developments Since The Last FOMC Decision

Download Full Report Here

What would have been a lighter inter-meeting period for top tier data releases has been reduced even further with, at typing, the second longest US government shutdown in history. It has seen the FOMC going without some major official releases, including the nonfarm payrolls, retail sales and PPI reports for September. The BLS made an exception for the September CPI report on social security payment grounds otherwise both the Fed and markets alike have been going off alternative data sources when assessing latest economic developments.

- Inflation: A Lone CPI Report Surprises Softer, Data Quality Concerns Increase

- Growth: Robust Official Data Before More Mixed Private Surveys

- Labor: Various Indicators Point To Signs Of Slack Still Slowly Building

US TSYS/SUPPLY: 7Y Sees Widest Tail In Over A Year In Soft Auction

October's $44B 7Y note auction tails 0.8bp with a high yield 3.790% vs when-issued yield of 3.782%, for the widest tail for this tenor since August 2024 (1.0bp tail). This was also the 3rd tail in a row (0.5bp the prior 2 auctions), the longest such streak since Nov 2023-Jan 2024.

- Periphery stats were mixed-to-weak vs prior.

- Bid/cover of 2.46x improved from September's 2.40x, but the latter was the lowest since March 2023.

- However, primary dealer takeup of 13.1% was a little higher than September's 12.0% for the highest since April, while directs took down 27.9% (31.6% prior) and indirects 59.0% (56.4% prior).

- Relatively limited market reaction in Treasuries.

- That concludes October's nominal coupon auctions - they resume on Nov 10 with 3Y Note, coming after next week's Refunding announcement.

FED: US TSY 7Y NOTE AUCTION: HIGH YLD 3.790%; ALLOTMENT 71.90%

- US TSY 7Y NOTE AUCTION: HIGH YLD 3.790%; ALLOTMENT 71.90%

- US TSY 7Y NOTE AUCTION: DEALERS TAKE 13.14% OF COMPETITIVES

- US TSY 7Y NOTE AUCTION: DIRECTS TAKE 27.85% OF COMPETITIVES

- US TSY 7Y NOTE AUCTION: INDIRECTS TAKE 59.01% OF COMPETITIVES

- US TSY 7Y AUCTION: BID/CVR 2.46