MNI US MARKETS ANALYSIS - Curve Steepens Ahead of Weekly ADP

Highlights:

- Curve sits bull steeper, Dec FOMC pricing remains a close call

- Carney secures new Budget for first time since taking office; CAD outperforms

- USDJPY looks through Takaichi-Ueda meeting; affirms gradualism

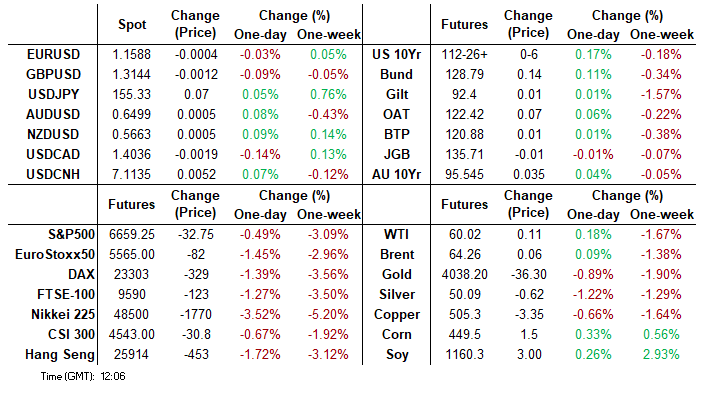

US TSYS: Bull Steeper - Weekly ADP, Factory Orders & Trump-MBS Meeting In Focus

Treasuries sit bull steeper heading into the US session on decent cumulative volumes, with some eyeing a rise in WARN notices even though it broadly corroborated a similar report from Challenger two weeks ago.

- Today’s immediate focus is likely on the weekly ADP report as markets still get used to this higher frequency measure with an eye on Thursday’s BLS nonfarm payrolls report for September (MNI Preview here).

- Cash yields are 1.7-3.9bp lower, with the belly leading declines.

- TYZ5 trades at 112-27 (+06+) on solid overnight volumes of 400k, a little off an earlier high 112-29.

- It has moved back closer to resistance at 113-04+ (Nov 14 high) after which lies 113-18+ (Oct 28 high) but support remains exposed, starting with 112-10 (100-dma).

- The quarterly roll is starting to get underway, with TY estimated at ~7% complete.

- Data: Weekly ADP (0815ET), Weekly Redbook retail sales (0855ET), NAHB housing index Nov (100ET), Durable goods/Factory orders Aug f/Aug post-shutdown catch-up (1000ET), potential release of Federal budget balance

- Fedspeak: Barr on bank supervision (1530ET), Barkin on economic outlook (1100ET), Logan closing remarks (1955ET) - see STIR bullet.

- Bill issuance: US Tsy to sell $95bn 6-w bills (1130ET)

- Politics: Trump in bilateral meeting with Crown Prince of Saudi Arabia (1145ET), Trump dinner with Crown Prince of Saudi Arabia (1915ET)

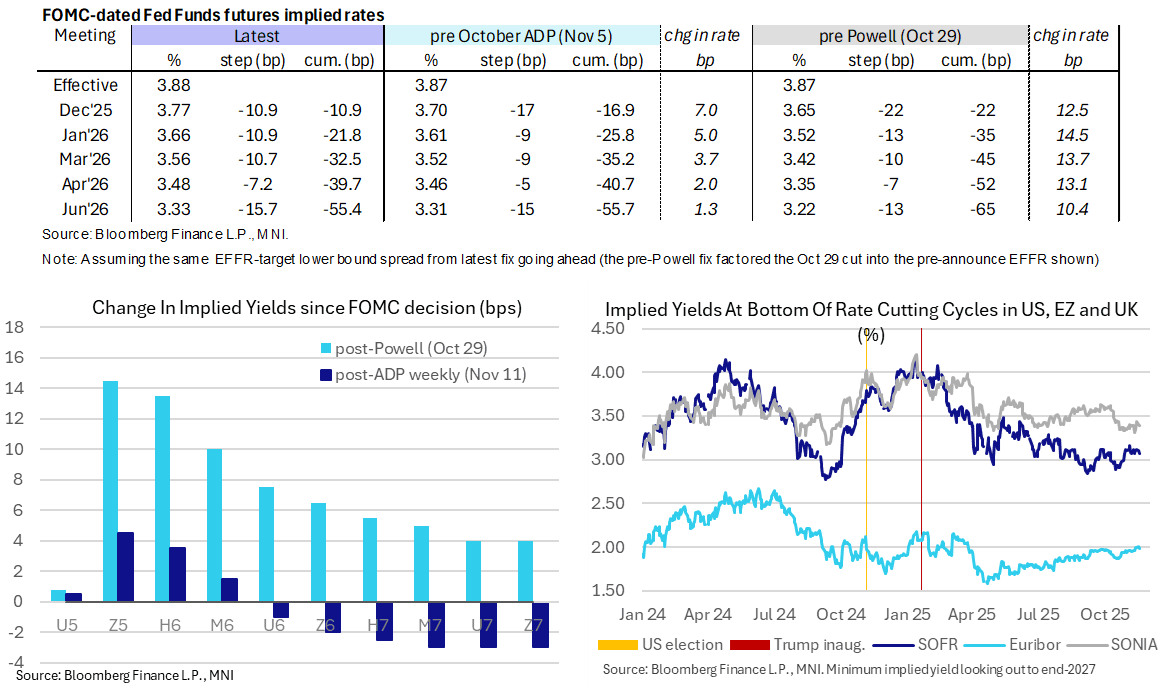

STIR: Fed Rates Soften But Keep Dec A Close Call, Labor Data In Spotlight

- Fed Funds implied rates have softened 0.5-3bp overnight for meetings out to mid-2026, although a December pause is still seen a marginally more likely than another cut.

- There has been some reference to a Bloomberg piece from late yesterday on higher WARN notices in a Cleveland Fed tally for October, but we note that this somewhat chimes with the Challenger report from two weeks ago which showed its highest layoff announcements for an October since 2003.

- Cumulative cuts from 3.87% effective: 11bp Dec, 22bp Jan, 32.5bp Mar, 39.5bp Apr, 55.5bp Jun.

- SOFR futures are up 3.5 ticks firmer in 2026 and 2027 contracts, with the terminal yield of 3.075% (H7) at the lower end of the 3.065-3.16% range for closes seen in recent weeks.

- The weekly ADP report will be watched closely.

- Today’s Fedspeak highlights likely come from Richmond Fed’s Barkin on the economic outlook at 1100ET (text + Q&A). However, the fact he doesn’t hold a voting role in 2025 or 2026 should limit the market reaction considering heightened attention on near-term rate cut prospects.

- He hasn’t materially touched on the outlook since September. We suspect he was one of the six dots back at the September SEP looking for no further rate cuts in the year (i.e. would have preferred not to cut last month) but we have lower conviction there than for some others.

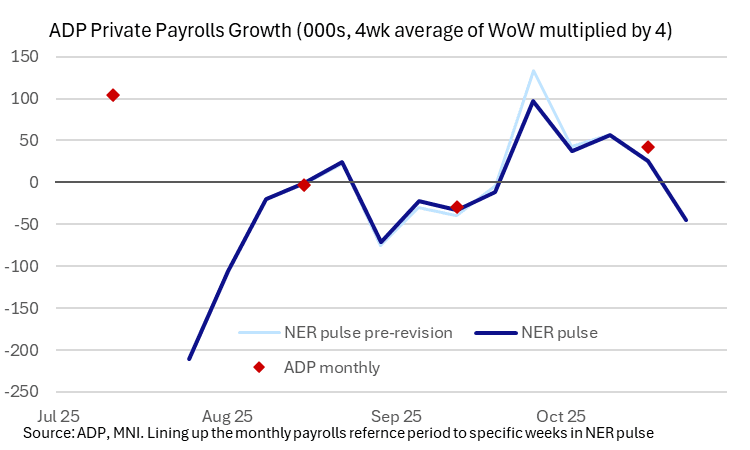

US OUTLOOK/OPINION: Weekly ADP Watched After Renewed Rolling Over

The weekly ADP report offers another timely update on labor conditions, watched to see if last week’s decline is revised and for latest momentum heading into November.

- The weekly ADP report will be released today at 0815ET, covering the four weeks up to Nov 1.

- Last week’s release was the first one when we knew it would be published and saw some dissemination issues.

- It was first published here: https://www.adpresearch.com/the-ner-pulse/ although ADP said beforehand that it would be published here: https://www.adpresearch.com/category/mainstreet-macro/. We’ll monitor both but expect a smoother release this week.

- Last week’s release suggested a return of private sector job losses in data up to Oct 25 with a four-week average decline of -11.25k jobs on a week-on-week basis. On its own it points to renewed sizeable deterioration in net job creation after some stabilization in the monthly October report with its +42k (for its reference week including the 12th of the month).

- ADP has warned that these data are preliminary and can be revised although last week’s release made it difficult to accurately assess these revisions in a timely manner.

- Fed Governor Waller (voter, dove), who is one of the leading voices calling for further cuts including at next month’s meeting, has referenced ADP data for some time. That included in yesterday’s speech (link): “While the ADP data are quite volatile and have some other shortcomings that make them less reliable than government statistics, I do think these data are telling us something. And in September and October, ADP reported that businesses created a net total of only 6,500 jobs a month. And the latest weekly data are even weaker.”

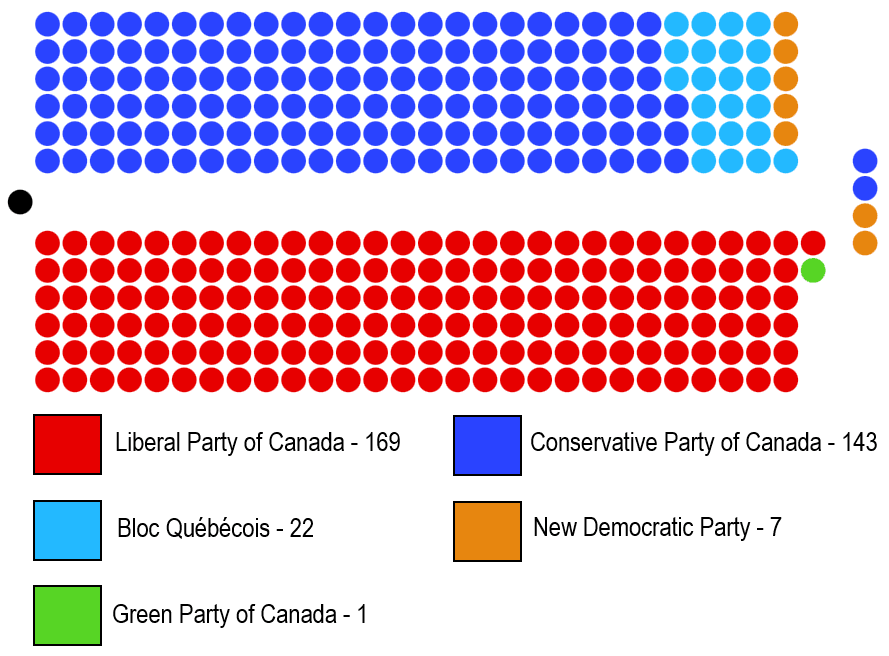

CANADA: Gov't Secures Budget Passage w/Little Appetite For Snap Election

PM Mark Carney secured passage of the first federal budget of his tenure on 17 Nov. This was by a two-vote margin, and only thanks to the backing/abstention of opposition MPs. The budget passed with 170 votes in favour to 168 against, with Carney's centre-left Liberal Party of Canada (LPC) being joined by the sole environmentalist Green MP, Elizabeth May, in supporting the package.

- Even with May's support, if all other opposition MPs had voted against the budget, it would have been enough to defeat it. Given that federal budget votes are deemed confidence motions, this would have sparked a snap federal election. Instead, two MPs from the main opposition centre-right Conservatives (CPC) and two from the left-wing New Democratic Party (NDP) abstained on the vote.

- While the margin of victory may seem slim, there appears to be little desire from many parties in parliament for an early election.

- Carney is still looking to establish himself as a national leader after taking over from PM Justin Trudeau in April, and the pressure on the economy from US tariffs makes it an inopportune time for an election.

- CPC leader Pierre Poilievre is still smarting from a disastrous election campaign, where Poilievre lost his seat, and the defection of Chris d’Entremont to the LPC. Poilievre faces an internal review of his leadership in January, amid record-low personal approval ratings.

- The NDP's collapse in April was so severe that it lost official party status in the Commons, and is in the first stages of a rebuild amid an ongoing leadership contest.

- While there will be at least one other opportunity for a confidence vote in 2025 before the House rises on 12 Dec (a vote on approving day-to-day departmental spending). However, it looks as though, despite external headwinds, the political environment will remain relatively stable in the short-to-medium term.

Chart 1. Federal Budget Vote in House of Commons 17 November 2025

Source: CBC, MNI. N.B. Black dot indicates non-voting Speaker. Dots on right indicate abstentions.

UKRAINE: US' Witkoff To Join Zelenskyy In Looking To Restart Talks w/Russia

Earlier this morning, President Volodymyr Zelenskyy confirmed that he would travel to Turkey on Wednesday, 19 November, to hold talks with officials and seek to "reinvigorate negotiations" with Russia. This has been followed by a headline on Reuters claiming that, according to a Turkish source, US Middle East envoy Steve Witkoff will travel to Turkey to join the talks with Zelenskyy.

- Posting on X, Zelenskyy said, "We are preparing to reinvigorate negotiations, and we have developed solutions that we will propose to our partners. Doing everything possible to bring the end of the war closer is Ukraine’s top priority. We are also working to restore POW exchanges and bring our prisoners of war home."

- The visit comes two days after a Russian drone was suspected of striking a Turkish-flagged LNG carrier in Ukraine's Odesa region on the Black Sea, setting the vessel ablaze and leading to evacuations in nearby Romania. This came a day after Zelenskyy signed a deal in Athens to import US LNG via the northern port of Alexandroupolis from Jan 2026.

- The presence of Witkoff may not be viewed by Ukraine and its allies of indicative of a harder US push for Russian concessions. As Politico noted on 17 Nov, "EU officials have been aghast at Witkoff’s lack of understanding of the complexities of the Russia-Ukraine war. One senior European official who requested anonymity to speak candidly about diplomatic matters said they have zero confidence that Witkoff can even relay messages between Moscow and Washington reliably and accurately."

FOREX: USDJPY Uptrend Remains Intact as Takaichi - Ueda Meet Affirms Gradualism

- Ongoing weak risk sentiment underpins low yielding haven currencies JPY and CHF in a session seeing limited volatility so far. Markets await key official economic data reducing uncertainty about the macro picture - clearing up the Fed policy path for the rest of the year.

- CAD outperforms after PM Mark Carney secured passage of the first federal budget of his tenure, suggesting that despite external headwinds, the Canadian political environment will remain relatively stable in the short-to-medium term. Expectations for a further Bank of Canada cut in this cycle let alone December are pretty much eliminated by now, with the short-term outlook for USDCAD appearing bearish form a technical perspective. Firm core indicators in yesterday's CPI report, in conjunction with earlier stronger-than-expected labour market data have combined to pretty much eliminate expectations for a further Bank of Canada cut in this cycle.

- USDCAD is trading inside a bull channel drawn from the Jul 23 low. The top of the channel - currently at 1.4170 - provided a firm resistance on Nov 11. The subsequent move down highlights scope for a bear extension towards the base of the channel at 1.3893. Initial key support to watch is 1.3968, the 50-day EMA.

- USDJPY price action meanwhile confirmed the resumption of an uptrend and extension of recent gains, with sights on 155.53, a Fibonacci projection. Comments following the meeting between Japanese PM Takaichi and BoJ Governor Ueda did not move the needle, with Ueda noting that he told Takaichi that the Bank is operating a process of gradually adjusting its monetary easing, which the PM "seemed to acknowledge". Initial firm support in USDJPY would be 153.49, the 20-day EMA, a clear breach of which would signal scope for a corrective pullback.

- Fed's Barr and Barkin, the ECB's Pereira and Dolenc, as well as the BoE's Pill and Dhingra are scheduled to speak. Barkin is due to comment on the economic outlook having not commented directly on policy since the last Fed decision.

- The US data calendar is starting to pick up, with weekly ADP, November NY Fed services, weekly redbook retail sales, November NAHB housing index, August factory orders, and September TIC flows likely being released today ahead of tomorrow's UK CPI. A roughly inline UK inflation print with a non-inflationary budget may ensure key voter Bailey will support December cut, which could keep the pressure on GBP.

OPTIONS: Expiries for Nov18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-05(E915mln), $1.1675(E1.4bln), $1.1700(E1.0bln)

- USD/JPY: Y153.00($1.3bln)

EQUITIES: E-Mini S&P Maintains a Softer Short-Term Tone

- A M/T bull trend in Eurostoxx 50 futures remains intact, however, the latest sell-off highlights a stronger corrective cycle. The move down this week has resulted in the breach of two key support points; 5606.50, the 50-day EMA, and 5604.50, the base of a bull channel drawn from the Aug 1 low. The breach signals scope for a deeper pullback and opens 5503.00, a Fibonacci retracement. Initial resistance to watch is 5675.90, the 20-day EMA.

- S&P E-Minis maintain a softer short-term tone. The below support at 6655.70, the Nov 7 low cancel recent bearish signals and signals scope for an extension of the current corrective cycle. Note that price has also breached support at the 50-day EMA. An extension would open 6540.25, the Oct 10 low and the next key support. Initial firm resistance to watch is 6793.65, the 20-day EMA.

COMMODITIES: Key Support to Watch for Gold at $3932.10, the 50-Day EMA

- A sell-off in WTI futures on Nov 12 strengthens a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Clearance of this level would confirm a resumption of the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $62.59, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction.

- The downleg in Gold between Oct 20 and 28 appears to have been a correction and has allowed an overbought condition to unwind. Recent gains suggest that correction is over. With the metal retracing from last week’s high, the key support to watch lies at the 50-day EMA, at $3932.1. Clearance of this EMA would signal scope for a deeper retracement. The short-term bull trigger has been defined at $4245.23, the Nov 13 high.

| Date | GMT/Local | Impact | Country | Event |

| 18/11/2025 | 1300/1300 | BOE Pill Fireside Chat on MonPol | ||

| 18/11/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 18/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/11/2025 | 1415/0915 | *** | Industrial Production | |

| 18/11/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1530/1030 | Fed Governor Michael Barr | ||

| 18/11/2025 | 1600/1100 | Richmond Fed's Tom Barkin | ||

| 18/11/2025 | 1700/1700 | BOE Dhingra on Income Growth and Consumption | ||

| 18/11/2025 | 2100/1600 | ** | TICS | |

| 18/11/2025 | 2300/1800 | Dallas Fed's Lorie Logan | ||

| 19/11/2025 | 2350/0850 | * | Machinery orders | |

| 19/11/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 19/11/2025 | 0030/1130 | *** | Quarterly wage price index | |

| 19/11/2025 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 19/11/2025 | 0700/0700 | *** | Producer Prices | |

| 19/11/2025 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 19/11/2025 | 0900/1000 | ** | EZ Current Account | |

| 19/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 19/11/2025 | 1330/0830 | ** | Trade Balance | |

| 19/11/2025 | 1330/0830 | ** | Trade Balance | |

| 19/11/2025 | 1500/1000 | Fed Governor Stephen Miran | ||

| 19/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 19/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 19/11/2025 | 1730/1230 | BOC Deputy Vincent speaks in Quebec City (Time TBC) | ||

| 19/11/2025 | 1745/1245 | Richmond Fed's Tom Barkin | ||

| 19/11/2025 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 19/11/2025 | 1900/1400 | New York Fed's John Williams | ||

| 19/11/2025 | 1900/1400 | *** | FOMC Minutes |