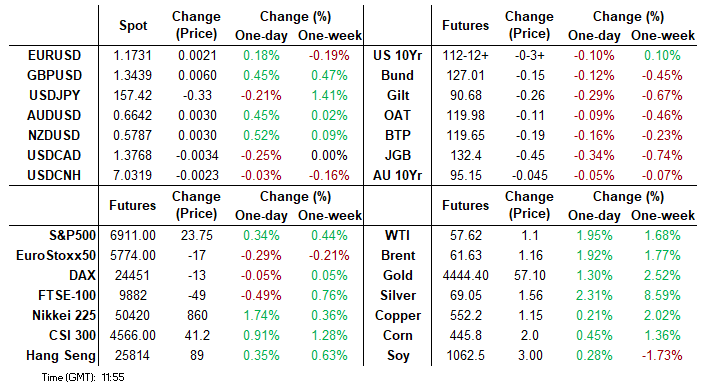

MNI US MARKETS ANALYSIS - Curve Mildly Steeper on Light Volume

Highlights:

- Volumes thin out on path to holiday period; Treasury curve sits modestly bear steeper

- Gold, silver rush to new highs as price insensitive buyers remain the key driver

- Scant data due Monday, with focus on 2y US Treasury supply

US TSYS: Modestly Bear Steeper On Particularly Thin Volumes, 2Y Supply Ahead

Treasuries are modestly bear steeper on very thin volumes after the weekend, helped lower by a further sizeable sell-off in JGBs after last week’s BoJ hike to leave Treasuries underperforming EGBs. Moves are aided by further increases for crude oil and US equity futures, ahead of a light docket headlined by 2Y supply.

- Cash yields are 0.5-2.4bp higher, with increases led by 20s.

- 2s10s at 67.5bps (+1.3bp) remains close to last week’s high of 69.1bp at interesting levels that prior to a brief spike to 73.8bp in early April was last higher in early 2022.

- TYH6 trades close to session lows of 112-11+ (-04+) on particularly low volumes of 165k.

- It has pulled back from recent highs, leaving a key short-term resistance level at 112-31 (Dec 18 high). Support is seen at 112-06 (Dec 16 low) whilst downside focus would be on a bear trigger at 111-29 (Dec 10 low).

- Data: Chicago Fed National Activity Index Sep (0830ET) – data picks up tomorrow including long-awaited Q3 GDP data

- Coupon issuance: US Tsy $69B 2Y Note auction - 91282CPS4 (1300ET). Last month’s auction saw a small 0.2bp tail although details firmed with bid-to-cover of 2.68 after 2.59 and indirect take-up rising to 58.1% from 53.65%.

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump’s schedule hasn’t been released yet

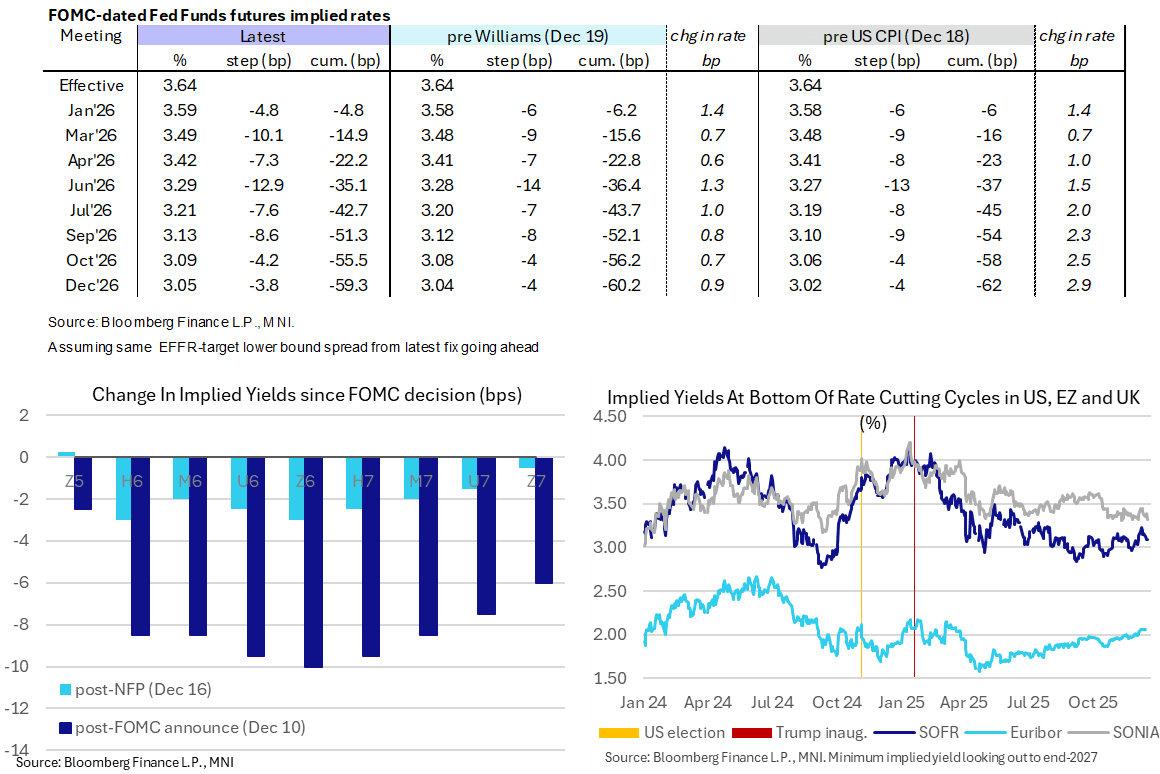

STIR: US Rates Mostly Fade Latest Climb In Oil Futures

- Fed Funds implied rates are broadly unchanged since Friday’s close, with little material spillover from WTI futures climbing a further 1.8% or Cleveland Fed’s Hammack admittedly sticking to the hawkish script over the weekend.

- It holds a small hawkish move after Williams on Friday, with low odds of a fourth consecutive cut in January (5bp) and with a next cut still leaning to but not fully priced for April (cumulative 22bp).

- Cumulative cuts from 3.64% effective: 5bp Jan, 15bp Mar, 22bp Apr, 35bp Jun (new Fed chair), 51.5bp Sep and 59.5bp Dec.

- SOFR futures are 0-1.5 ticks lower looking to end-2027, with the terminal implied yield of 3.10% (Z6) remaining with ranges over the past month.

- Re-upping several rounds of flow worth highlighting from early London trade: SFRZ6 ~6.5K given at 96.900, SFRH7/H9 ~3.3K given at 40.5 and SFRH6 96.56/96.43/96.37/96.18 broken put condor 4K given at 5, desks point to closing out of an existing position.

- Cleveland Fed’s Hammack (’26 voter, hawk) in WSJ remarks over the weekend said a pause in rates is her base case for now, waiting to see “clearer evidence that either inflation is coming back down to target or the employment side is weakening more materially”. She doesn’t put much weight on any single economic report and said that last week’s inflation data includes “noise” due to the lack of sampling during the shutdown. “It’s just one number and I want to take some time. Fortunately, we have a lot of time before our next meeting to see how the broader picture comes in.”

SOFR: Fed’s Williams Helped Tilt Bias To Short Setting In Futures On Friday

OI data also points to net short setting dominating in the U.S. short end as SOFR futures ticked lower on Friday.

- Inputs from wider core global FI markets and hawkish leaning commentary from NY Fed President Williams factored into the hawkish move.

- Some contract-specific instances of net long cover were seen, but they were comfortably outweighed by short setting in all packs through the blues.

| 19-Dec-25 | 18-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,537,890 | 1,535,453 | +2,437 | Whites | +27,444 |

SFRH6 | 1,313,196 | 1,316,490 | -3,294 | Reds | +45,552 |

SFRM6 | 1,169,333 | 1,158,660 | +10,673 | Greens | +9,162 |

SFRU6 | 1,200,393 | 1,182,765 | +17,628 | Blues | +27,437 |

SFRZ6 | 1,152,251 | 1,128,350 | +23,901 |

|

|

SFRH7 | 876,408 | 849,752 | +26,656 |

|

|

SFRM7 | 759,413 | 764,279 | -4,866 |

|

|

SFRU7 | 808,058 | 808,197 | -139 |

|

|

SFRZ7 | 839,069 | 835,178 | +3,891 |

|

|

SFRH8 | 468,577 | 468,770 | -193 |

|

|

SFRM8 | 397,597 | 393,979 | +3,618 |

|

|

SFRU8 | 383,121 | 381,275 | +1,846 |

|

|

SFRZ8 | 336,970 | 326,093 | +10,877 |

|

|

SFRH9 | 210,655 | 205,374 | +5,281 |

|

|

SFRM9 | 218,974 | 209,705 | +9,269 |

|

|

SFRU9 | 178,917 | 176,907 | +2,010 |

|

|

US TSY FUTURES: Net Short Setting Dominated On Friday

OI data points to net short setting dominating during Friday’s downtick in Tsy futures, with that theme only interrupted by fairly limited net long cover in WN futures.

- TU futures saw the biggest net positioning swing (in both outright and DV01 terms) on the day.

| 19-Dec-25 | 18-Dec-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,555,759 | 4,466,893 | +88,866 | +3,505,725 |

FV | 6,719,244 | 6,718,203 | +1,041 | +45,963 |

TY | 5,498,834 | 5,479,934 | +18,900 | +1,267,614 |

UXY | 2,515,262 | 2,513,848 | +1,414 | +127,812 |

US | 1,852,620 | 1,837,907 | +14,713 | +2,035,395 |

WN | 2,071,641 | 2,075,399 | -3,758 | -678,263 |

|

| Total | +121,176 | +6,304,246 |

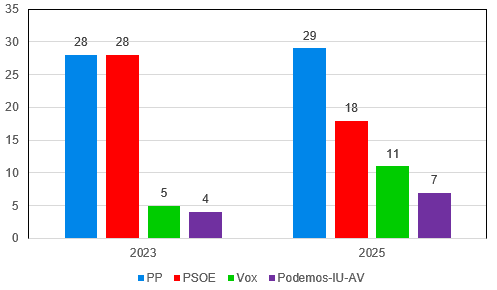

SPAIN: Blow To PM Sanchez As PSOE Suffer's Regional Election Losses

Prime Minister Pedro Sanchez suffered another blow to his position on 21 December, when his centre-left Spanish Socialist Workers' Party (PSOE) suffered significant losses in the election to the autonomous region of Extremadura's Legislative Assembly. Historically one of the PSOE's strongholds, the party won just 18 of the 65 seats on offer, down from 28 previously and representing an all-time low. The centre-right People's Party (PP) of regional President Maria Guardiola won 29 seats, up one from 28 previously.

- The main gains came on the far right, with Vox winning 11 seats, representing an increase of six, and on the far left, with the Podemos–IU–AV alliance taking seven seats, up from four previously. The result leaves the PP short of a majority, with Guardiola facing the choice of re-forming the coalition with Vox, or governing as a minority administration.

- A poor result in Extremadura comes with Sanchez under pressure amid a raft of scandals within the PSOE that have hit low-level activists and high-ranking officials, with the PM's wife and brother also subject to a probe into alleged influence peddling.

- Three regional elections are due in H126. Aragon, Castile and Leon, and Andalusia are all currently led by gov'ts headed by the PP. Nevertheless, further losses could further damage Sanchez's standing as the next general election approaches by August 2027 at the latest.

- On predictions market site Polymarket, bettors assign a 33% implied probability that Sanchez is out as PM by July 2026, and a 50% chance that he leaves office by the end of next year.

Chart 1. Extremadura Election, Seats

Source: congreso.es, MNI

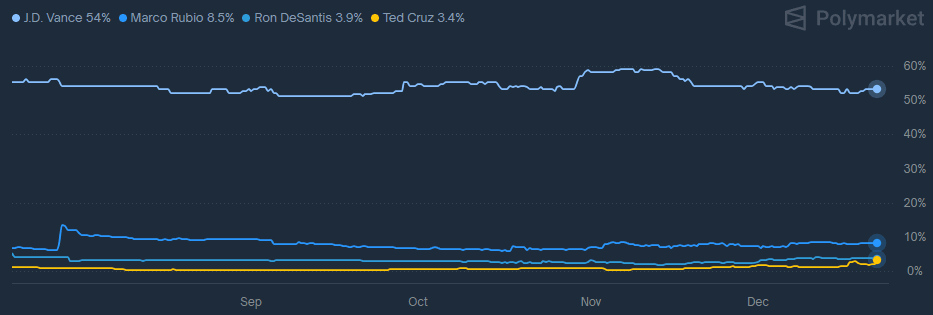

US: WaPo - Sen. Ted Cruz Considering Run For GOP Presidential Nomination In '28

The Washington Post reports that Senator Ted Cruz (R-TX) is considering another run for the US presidency in 2028. If he does run, it would mark his second attempt to win the Republican presidential nomination, after coming in second place behind Donald Trump in 2016. WaPo reports that "Cruz has in recent months positioned himself as a loud voice for a more traditional, hawkish Republican foreign policy. [...] A White House run would be politically risky for Cruz, 55, putting him on course to collide with Vice President JD Vance, who many Republicans expect to enter the 2028 race. [...] Some political observers are skeptical that another Cruz run would gain much traction. He can no longer run as an outsider and alienated some conservatives with his fight against Trump in the 2016 campaign."

- Data from predictions market site Polymarket shows Vance as the strong favourite among bettors to win the GOP nomination, with an implied probability of 54%. Secretary of State Marco Rubio sits in a distant second place on an implied probability of 8.5%. Third favourite is term-limited incumbent Donald Trump on 4.3%, with Florida Governor Ron DeSantis fourth on 3.9%. Cruz is in fifth place with an implied probability of 3.4%.

- During his first Senate run in 2012, Cruz positioned himself as a Tea Party fiscal conservative, anti-establishment candidate, and was one of the political drivers behind the 2013 gov't shutdown. Since his 2016 presidential campaign, Cruz has become more representative of 'traditional Republican' stances on the economy (more capitalist than populist), and as a vocal supporter of Israel, in contrast to some wings of the MAGA movement.

Chart 1. Predictions Market Implied Probability of Winning 2028 Republican Presidential Nomination, %

Source: Polymarket

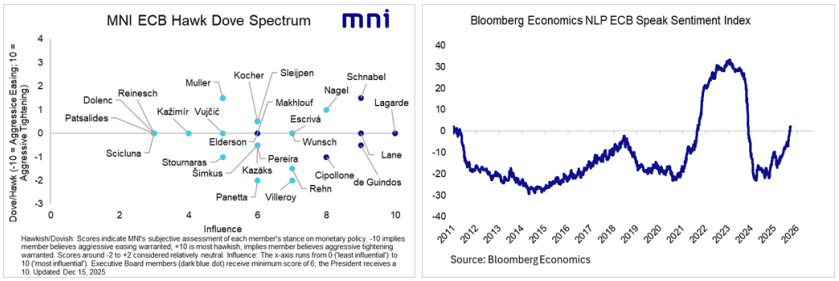

ECB: Vujcic Maintains Position At Centre Of ECB Hawk-Dove Spectrum

Speaking in Zagreb, ECB’s Vujcic maintains his position at the centre of the ECB’s hawk-dove spectrum, with his view seemingly unchanged after the new economic projections unveiled last week.

- He offered little directional bias, saying the next move on rates could be in either direction and that inflation and growth risks are balanced.

- There’s little to get into in today’s comments but it confirms his pre-meeting view and implies that the larger than expected upward revisions seen for headline and core HICP inflation in 2026 and real GDP growth for both 2027 and 2028 haven’t swayed him.

- These pre-meeting remarks from Nov 26 offered a little more colour: "I don't have a special scenario in mind for a rate cut or a rate hike. Everything is circumstantial. We have many things we look at to determine the inflation outlook and interest rate action […] As I said, for the time being we are in a good place"

- On the then upcoming December projections: "If you don't see large enough persistent deviation or an increasing downward trend, then it is fine. Thinking two or three years ahead, you always have increasing uncertainty. We better stick to the more visible future and make sure that the data we get is consistent with our projections. If they are, we are fine."

The latest MNI Hawk-Dove Spectrum taken from the ECB Preview:

FOREX: USD Index Softer, Helping Flatter Gold Rally

- The US dollar is the main underperformer Monday, although the USD Index is holding within Friday's range while attention was on gold trading firmly to fresh all-time highs. Geopolitics remain in focus for FX markets with the US oil blockade of Venezuela continuing and US-European-Ukraine-Russia talks ended without a breakthrough with special envoy Witkoff saying that they were “productive and constructive".

- Antipodean currencies outperform despite mixed risk sentiment on Monday. NZDUSD hovering around Thursday's 0.5788 high as markets continue to pare expectations for 2026 RBNZ tightening. More important resistance stands at 0.5831, the Dec 11 high.

- AUDUSD meanwhile remains in a bullish trend structure ahead of tomorrow's RBA minutes. The minutes will be scrutinised for more information around the board's degree of concern about upside inflation risks as well as how much this translates to the RBA's stance being skewed to the upside. Resistance stands at the 0.6686 December 10 high.

- GBPUSD narrows the gap to last week's 1.3456 highs on the back of the weaker dollar, while UK Q3 GDP came in as expected this morning. A break higher would strengthen the ongoing bull theme in GBPUSD and open 1.3527, the Oct 1 high. Initial firm support is 1.3300, the 50-day EMA. Clearance of this average would highlight a possible reversal.

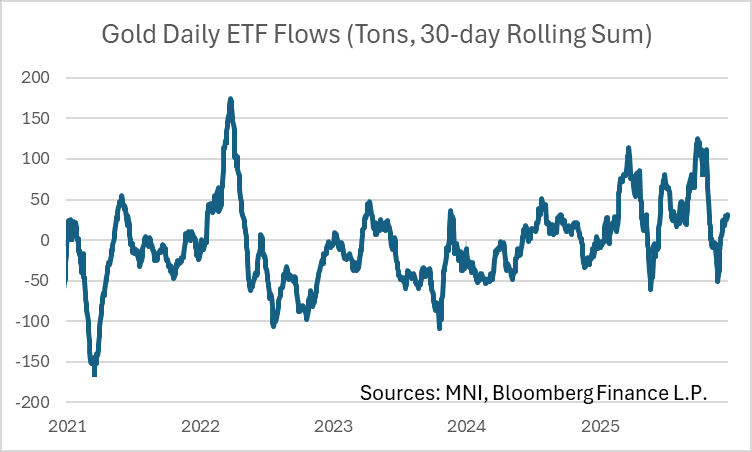

GOLD: ETF Flows Underpin All-Time Highs But Other Drivers Also At Play

Spot gold (+1.67%) made light work out of previous $4381.52/oz all-time highs this morning, extending to around $4420/oz in early European trade. While some may conjecture over further Fed easing, geopolitical tensions, a slightly weaker dollar and year-end hedging flows, a clear headline driver for the today's move remains scant - highlighting the market's appetite for further long positioning in gold which while ending the previous corrective cycle.

- ETF flows have turned positive again in late November as a rolling 30-day sum, but interestingly have not made up for sales following the October 21 holdings peak. This suggests non-retail buyers had a net-positive effect on spot since late October.

- More broadly, decomposing gold returns into changes of real yields, the dollar index, ETF flows and a risk proxy shows large unexplained residuals towards the end of this year. This would point towards price-insensitive buyers remaining in play.

- JP Morgan meanwhile report on Friday that "debasement trades (Gold up & USD/JPY up duals) are consensus". They see gold at $5,055/oz by the final quarter of 2026, rising toward $5,400/oz by the end of 2027 as "the long-term trend of official reserve and investor diversification into gold has further to run".

- In parallel, Silver also remains in a bull cycle, setting fresh $69.45/oz all-time highs this morning. Recent returns here have been even more pronounced, bringing the gold/silver ratio down below 64 for the first time since February 2021. A break below 62.34 would mean its lowest level since July 2014.

COMMODITIES: Trend Structure in Gold Goes From Strength to Strength

- The trend structure in Gold is unchanged, it remains bullish and today’s fresh cycle high reinforces current conditions. The break higher confirms a resumption of the primary uptrend.

- The trend condition in WTI futures remains bearish and short-term gains are considered corrective. MA studies are in a bear-mode position, highlighting a dominant downtrend.

EQUITIES: Pullback Exposes S/T Bear Threat

- A pullback in S&P E-Minis has resulted in a breach of both the 20- and 50-day EMAs. This strengthens a short-term bear threat and signals scope for a deeper retracement of the recent bull phase between Nov 21 - Dec 11.

- A bull cycle in EUROSTOXX 50 futures remains intact and the latest pullback appears to have been a correction. The first key support to watch lies at 5681.57, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 22/12/2025 | 1330/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 22/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 22/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 22/12/2025 | 1800/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 23/12/2025 | 0700/0800 | ** | PPI | |

| 23/12/2025 | 0700/0800 | ** | Import/Export Prices | |

| 23/12/2025 | 0800/0900 | ** | PPI | |

| 23/12/2025 | 0800/0900 | *** | GDP (f) | |

| 23/12/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 23/12/2025 | 1330/0830 | *** | Gross Domestic Product by Industry | |

| 23/12/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/12/2025 | 1330/0830 | *** | GDP / PCE Quarterly | |

| 23/12/2025 | 1330/0830 | *** | GDP / PCE Quarterly | |

| 23/12/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 23/12/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 23/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 23/12/2025 | 1415/0915 | *** | Industrial Production | |

| 23/12/2025 | 1500/1000 | ** | Richmond Fed Survey | |

| 23/12/2025 | 1630/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 23/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 23/12/2025 | 1800/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 23/12/2025 | 1830/1330 | Bank of Canada meeting minutes |