US TSYS: Modestly Bear Steeper On Particularly Thin Volumes, 2Y Supply Ahead

Treasuries are modestly bear steeper on very thin volumes after the weekend, helped lower by a further sizeable sell-off in JGBs after last week’s BoJ hike to leave Treasuries underperforming EGBs. Moves are aided by further increases for crude oil and US equity futures, ahead of a light docket headlined by 2Y supply.

- Cash yields are 0.5-2.4bp higher, with increases led by 20s.

- 2s10s at 67.5bps (+1.3bp) remains close to last week’s high of 69.1bp at interesting levels that prior to a brief spike to 73.8bp in early April was last higher in early 2022.

- TYH6 trades close to session lows of 112-11+ (-04+) on particularly low volumes of 165k.

- It has pulled back from recent highs, leaving a key short-term resistance level at 112-31 (Dec 18 high). Support is seen at 112-06 (Dec 16 low) whilst downside focus would be on a bear trigger at 111-29 (Dec 10 low).

- Data: Chicago Fed National Activity Index Sep (0830ET) – data picks up tomorrow including long-awaited Q3 GDP data

- Coupon issuance: US Tsy $69B 2Y Note auction - 91282CPS4 (1300ET). Last month’s auction saw a small 0.2bp tail although details firmed with bid-to-cover of 2.68 after 2.59 and indirect take-up rising to 58.1% from 53.65%.

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump’s schedule hasn’t been released yet

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: Moody's Upgrades Italy To Baa2 From Baa3, Still A Notch Below Others

The Moody's upgrade to Italy's credit rating announced late Friday was the first from the agency since 2002 but shouldn't be considered a major surprise. Among the 3 major ratings agencies, Moody's had the lowest rating on Italy - by two notches (Fitch and S&P both BBB+).

- So this upgrade to Baa2 from Baa3 represents something of a closing of that gap rather than a major breakthrough for Italy.

- From the release:

- "The rating upgrade reflects a consistent track-record of political and policy stability which enhances the effectiveness of economic and fiscal reforms and investment implemented under the National Recovery and Resilience Plan (NRRP). It also points to prospects of further policy actions supporting growth and fiscal consolidation beyond the plan's deadline in August 2026. As a result, we expect that Italy's high government debt burden will gradually decline from 2027 onwards."

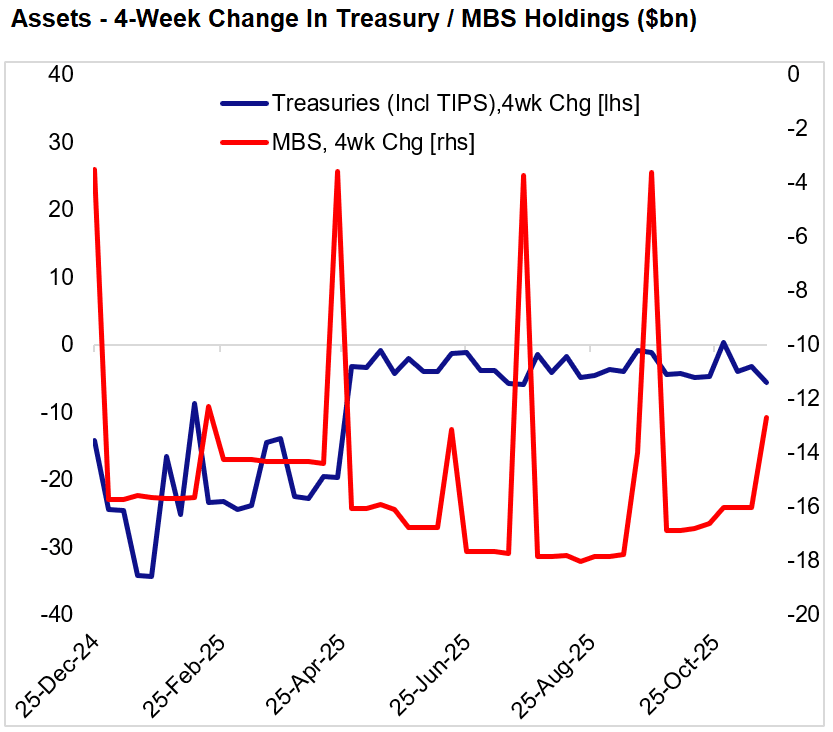

FED: Heading Into Its Final Weeks, QT Pace Remains At $20B/Month (2/2)

On the asset side of the Fed balance sheet, we saw a $25B drop in assets, of which just $2B could be attributed to QT in one of its final weeks (ends Dec 1).

- Instead it was a $6B drop in dealer repo operations vs a week earlier, and $17B in "other" areas that aren't related directly to monetary policy and typically don't have any significant impact on the size of the balance sheet (such changes are largely due to items such as bank premises, accrued interest, and other accounts receivable.)

- Discount window takeup edged up $0.3B to $6.1B but remains relatively low.

- QT has totaled just under $21B over the last month, around the expected pace, though as noted this will flatline in December with a pickup in net bills as MBS proceeds are rolled over into T-bills.

LOOK AHEAD: US Week Ahead: Retail Sales, PPI & Claims Headline Thanksgiving Week

A Thanksgiving-condensed week sees data highlights from delayed retail sales and PPI reports for September on Tuesday (Nov 25) before a Wednesday release for weekly jobless claims (Nov 26). Aside, the Fed’s Beige Book should also offer another important update on Wednesday for latest liaison reporting, with no Fedspeak currently scheduled around the holiday and the FOMC media blackout due to start on Saturday, Nov 29.

- As we regularly comment in this weekly publication, Redbook and Chicago Fed CARTS indicators point to solid nominal growth in retail sales, something broadly reflected in analyst consensus for the release.

- PPI inflation will offer a useful albeit not overly timely update on input cost pressures.

- Jobless claims will be watched particularly closely, both for latest initial claims for signs of layoffs and a notable update for continuing claims. The latter covers the payrolls reference period for November and will be an important reference point for FOMC members trying to get a sense of latest unemployment rate clues with the next payrolls reports coming after the Dec 9-10 FOMC decision (going into it with this week’s 0.12bp rise to 4.44% back in September).