MNI US MARKETS ANALYSIS - Claims in Brief Focus Before Fri CPI

Highlights

- NFP reaction holds in implied Fed funds, claims in focus briefly before CPI tomorrow

- Kremlin says next round of US-Ukraine-Russia talks could take place "soon"

- CHF outperforms in partial reversal of recent fade

US TSYS: Strong Payrolls Dents But Doesn't Alter Bullish Phase, CPI On Horizon

Treasuries sit slightly firmer as US desks filter in after a steady overnight session that has kept to narrow ranges with yesterday’s nonfarm payrolls report digested. Today’s focus should be on latest weekly claims data before 30Y supply after yesterday’s 10Y was poorly received, with tomorrow's CPI report for January looming large.

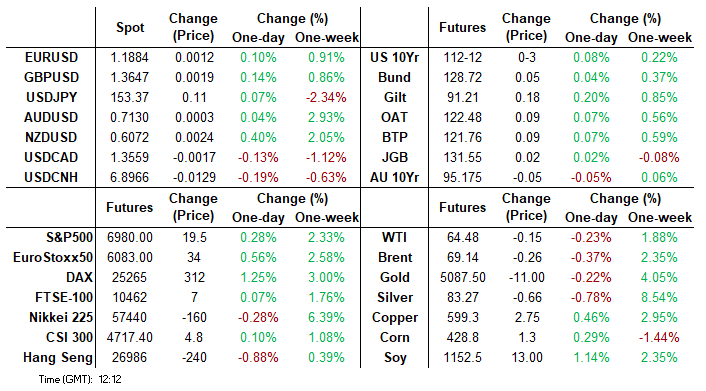

- Cash yields are 0.6-1.6bp lower on the day.

- TYH6 trades at 112-11+ (+02+) in narrow ranges on reasonable cumulative volumes of 310k.

- It sits between yesterday’s latest high at 112-20 and the post-NFP low of 112-00, which probed support at 112-01 (20-day EMA). It does however continue to trade closer to recent highs and suggests the current bull cycle is intact, leaving subsequent resistance at 112-25 (61.8% retrace of Nov 25 – Jan 20 bear leg).

- Data: Weekly jobless claims (0830ET), Existing home sales Jan (1000ET)

- Fedspeak: Logan opening remarks (1900ET), Miran moderated discussion (1905ET) – see STIR bullet

- Coupon issuance: US Tsy $25B 30Y Bond auction - 91281UR7 (1300ET). Yesterday’s 10Y auction saw a 1.5bp tail (largest at a 10Y refunding since Aug 2024), the bid-to-cover slipping from 2.55x to 2.39x and the lowest indirect take-up since Aug 2025.

- Bill issuance: US Tsy $105B 4W, $95B 8W bill auctions (1130ET)

- Politics: Trump makes announcement with EPA Administrator (1330ET), Trump in policy meetings (1500ET and 1730ET).

STIR: NFP Reaction Holds, Claims In Brief Focus Before CPI Tomorrow

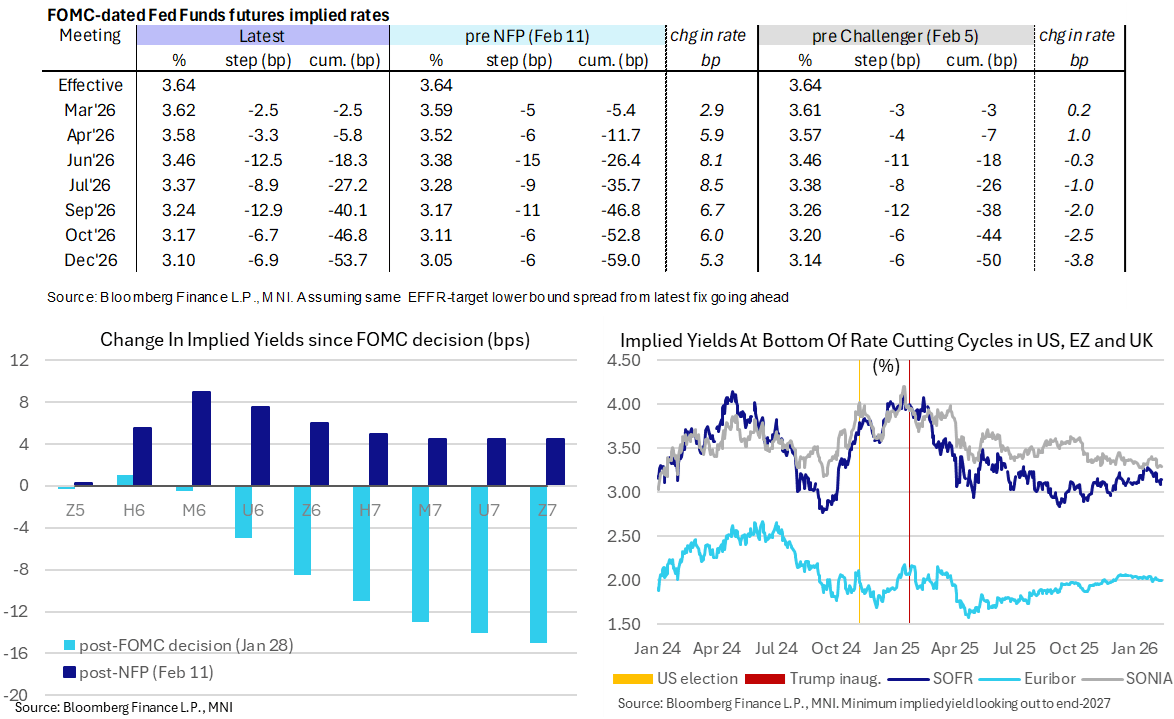

- Fed Funds implied rates still hold yesterday’s front-loaded hawkish reaction to payrolls, with today’s data focus on jobless claims as a minor stepping stone before tomorrow’s CPI release (MNI CPI Preview https://mni.marketnews.com/3OayQs6)

- Initial jobless claims were much higher than expected last week but were potentially boosted by extreme winter weather across much of the country in the last weeks of the month. They also appear to continue to see residual seasonality that could bias the trend higher heading into February.

- Cumulative cuts from 3.64% effective: 2.5bp Mar, 6bp Apr, 18.5bp Jun, 27bp Jul, 40bp Sep, 47bp Oct and 53.5bp Dec.

- SOFR futures are broadly unchanged on the day, with the terminal implied yield of 3.145% (H7) +5bp since NFPs. Still, it holds towards the lower end of the ytd range of 3.09-3.285% for closes.

- Today’s scheduled Fedspeak comes late on and we imagine won’t move the needle.

- 1900ET – Dallas Fed’s Logan (’26 voter, hawk) opening remarks. The nature of remarks should heavily limit any notable comments and she earlier this week said she needs to see “material” weakness in the labor market to support cuts.

- 1905ET – Gov. Miran (voter, dove) in moderated conversation at the Dallas Fed. He said briefly after yesterday’s NFP report that there are still a variety of reasons to lower rates, with a number of factors pushing supply side growth in the US.

FED: Republicans Suggest Senate, Not DoJ, Could Investigate Powell - Semafor

Highlights from the piece:

- "In a closed-door meeting with Senate Republicans Wednesday, Treasury Secretary Scott Bessent agreed with lawmakers who suggested the Senate Banking Committee could investigate Federal Reserve Chair Jerome Powell, instead of the Justice Department, people in the room told Semafor."

- "One of the sources, a lawmaker, said they interpreted the exchange as “testing the waters” to see if the arrangement could get Sen. Thom Tillis, R-N.C., to lift his blockade on Fed nominees".

SOFR: Net Short Setting Most Prominent In Futures After NFPs

OI data points to net short setting dominating during the hawkish repricing that followed yesterday's NFP report, with only one round of net long cover and one round of net long setting seen in front 14 SOFR futures contracts (only SFRZ5 finished higher on the day). As a result, net short setting dominated through the greens, while net long cover was most prominent in the blues.

| 11-Feb-26 | 10-Feb-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,350,563 | 1,343,638 | +6,925 | Whites | +81,724 |

SFRH6 | 1,310,706 | 1,302,211 | +8,495 | Reds | +123,396 |

SFRM6 | 1,434,771 | 1,403,076 | +31,695 | Greens | +157,704 |

SFRU6 | 1,408,885 | 1,374,276 | +34,609 | Blues | -8,359 |

SFRZ6 | 1,445,805 | 1,387,124 | +58,681 |

|

|

SFRH7 | 963,140 | 968,923 | -5,783 |

|

|

SFRM7 | 925,988 | 883,299 | +42,689 |

|

|

SFRU7 | 869,922 | 842,113 | +27,809 |

|

|

SFRZ7 | 1,038,268 | 917,978 | +120,290 |

|

|

SFRH8 | 535,695 | 527,169 | +8,526 |

|

|

SFRM8 | 462,688 | 441,973 | +20,715 |

|

|

SFRU8 | 401,621 | 393,448 | +8,173 |

|

|

SFRZ8 | 383,930 | 383,440 | +490 |

|

|

SFRH9 | 223,420 | 222,680 | +740 |

|

|

SFRM9 | 199,699 | 206,352 | -6,653 |

|

|

SFRU9 | 170,759 | 173,695 | -2,936 |

|

|

US TSY FUTURES: Net Short Setting Dominated After NFPs

OI data points to net short setting dominating in the wake of yesterday's NFP report, with ~$5.5mln of fresh net short DV01 exposure being added in curve-wide terms on the day and only modest long cover in UXY futures interrupting the wider theme.

| 11-Feb-26 | 10-Feb-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,674,168 | 4,656,489 | +17,679 | +648,424 |

FV | 6,864,635 | 6,835,483 | +29,152 | +1,247,598 |

TY | 5,434,362 | 5,419,794 | +14,568 | +958,617 |

UXY | 2,535,779 | 2,546,507 | -10,728 | -957,975 |

US | 1,748,303 | 1,733,810 | +14,493 | +2,016,227 |

WN | 2,195,297 | 2,186,904 | +8,393 | +1,554,223 |

|

| Total | +73,557 | +5,467,114 |

EU: Macron & Merz Look To Downplay Rift On EU Preference At Leaders' Summit

Speaking alongside German Chancellor Friedrich Merz following a bilateral discussion on the sidelines of the informal meeting of EU leaders taking place in Belgium presently, French President Emmanuel Macron said that he shares Merz's "feeling of urgency" with regard to making the EU more competitive. Says "We must go quickly...We must have very concrete decisions by June, regarding how to make Europe more competitive."

- Politico reports "While agreeing on the need to cut red tape and diversify trade partners, France and Germany have been at odds on the rest of the bloc’s economic agenda over the past days, from eurobonds to the definition of new “Made in Europe” measures." This chimes with reporting from MNI's Policy team earlier in the week (see MNI: EU Leaders To Seek To Protect Firms, Build Scale).

- Speaking at the European Industry Summit on 11 Feb, Macron referred to Europe as a "naive continent" due to its inability or unwillingness to protect its own industrial base against competition from the US, China and elsewhere (see EU: Macron Talks Up EU Strategic Autonomy As Essential For Economic Security). However, in something of a rebuttal, Merz, speaking immediately after Macron, said Europe was neither “naive nor defenceless”. As Euractiv notes, "Merz’s response to Macron’s call for a ‘European preference’ scheme to boost domestic manufacturing was similarly direct, calling it “too narrow” while pitching a lighter “made with Europe” scheme that would also provide preferential access to EU trade partners."

UKRAINE: Kremlin-Next Round Of Ukr-US-Rus Talks 'Could Take Place Soon'

There is still no sign of when or where a second round of tripartite talks between Ukraine, Russia and the US could take place. Russia's state-run Tass reports comments from Kremlin spox Dmitry Peskov stating that the Kremlin "has an understanding" about the next round of talks and that they "could take place soon", but gives no further details. On 11 Feb, Ukrainian President Volodymyr Zelenskyy said to Bloomberg News that a second round of talks could take place on 17 or 18 Feb in the United States, but that it was unclear if Russia would participate.

- The US's potential proposal of a 'free economic zone' in the Donbas to bridge the divide over territorial control - the key issue in the talks - looks to be a non-starter. BBG reports Zelenksyy saying, “None of the sides is keen on the idea of the free economic zone — neither the Russians, nor us”.

- There has been no further development or comment on the FT story claiming that on 24 Feb the Ukrainian gov't could call a presidential election and referendum on a peace deal to take place in May. Ukraine's Mezha Media reported the country's election commission had refuted the claims in the story, noting that "under current law any elections and referendums are possible only after the abolition or termination of martial law, and no new documents concerning the organization of postwar voting have been submitted to the CEC."

EUROPE ISSUANCE UPDATE

Italy auction results

- E3.5bln of the 2.40% Mar-29 BTP. Avg yield 2.36% (bid-to-cover 1.53x).

- E1.25bln of the 3.25% Jul-32 BTP. Avg yield 2.92% (bid-to-cover 1.98x).

- E1.5bln of the 3.15% Mar-33 BTP. Avg yield 3.02% (bid-to-cover 1.69x).

FOREX: Bear Trigger Halts USDJPY Decline, For Now

- Given the magnitude of the moves since Sunday’s vote in Japan, it is perhaps unsurprising to see USDJPY generate some demand in the low 152’s, with the 3.5% decline in just four sessions falling just shy of 152.10 support, and the technical bear trigger. A solid turnaround from the 152.27 lows prompted a 153.55 session high just ahead of the European open, with the pair subsequently consolidating around the 153 mark. If the price action following yesterday’s US employment report is anything to go by, the pair’s inability to consolidate any meaningful upward momentum could be a sign that further downside is imminent.

- While moderately lower on the session, AUD extended its bullish cycle overnight, with 0.7147 coming within 11pips of the 2023 peak. “The overall picture of [labour market] persistent tightness is important because it is consistent with there still being some inflationary pressure in the economy”, RBA's Hunter said overnight. A renewed push higher for AUDUSD would put sights on 0.7208, a Fibonacci projection.

- Swiss Franc resilience has resumed today, with EURCHF seeing a renewed push back towards 0.9125. USDCHF also edges closer to cycle lows which are located 0.7605, with participants awaiting inflation data from both Switzerland and the US on Friday.

- In emerging markets, EURHUF briefly extended an intraday rally to 0.5%, with weakness for the forint stemming initially from the below-expectations CPI print and then from an EU Court opinion on frozen funds. We flag key short-term resistance at 383.04, the 50-day EMA.

- Today's US data calendar is rather light, with weekly claims and home sales scheduled. Fed's Logan and Miran are set to appear, while a set of ECB speakers is unlikely to move the needle.

CHF: EURCHF Weakness Resumes, Back Below 0.9125

- Swiss Franc resilience has resumed today, with EURCHF seeing a renewed push back below 0.9125 in recent trade, narrowing the gap to Tuesday’s cycle lows at 0.9095. The overall bearish dollar narrative is also weighing notably on USDCHF today, which edges closer to cycle lows, located 0.7605.

- Markets will await inflation data from both Switzerland and the US on Friday. The Swiss reading will be interesting on the back of the annual January services repricing in a larger cluster of categories. The next SNB meeting is not scheduled until March 19.

- UBS have recently flagged that "asset managers are buying CHF at the fastest pace in a decade", one factor leading to their call for USDCHF reaching 0.75 at the end of Q1, and "consistent with deeper EURCHF downside towards 0.90 by year-end and beyond".

- Danske meanwhile think “the bar is relatively high for the SNB to intervene [...] also note the shift taking place in safe-haven dynamics the past year which has favoured a stronger CHF [...] stick to our call of being bullish CHF FX."

- As a reminder, Morgan Stanley also put out a bullish franc call earlier this week, targeting a move for EURCHF to 0.8700. They highlighted that inflation dynamics differ from 2020 and reduce the case for SNB level defence.

OPTIONS: Expiries for Feb12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1750-60(E2.4bln), $1.1875-80(E637mln)

- USD/JPY: Y153.00($605mln), Y154.00($2.4bln)

- USD/CNY: Cny6.9000($1.1bln)

POLAND: Consensus Forms Around 25bp March Cut and 3.50% Terminal Rate

We have heard from several MPC members this week, with their comments cementing consensus around the outcome of the NBP's monetary policy meeting in March (25bp cut) and the terminal rate (3.50%). The NBP meet next on March 4 - a meeting which will include updated inflation and GDP projections.

- MPC's Henryk Wnorowski told Dziennik Gazeta Prawna that 'there are currently no strong arguments against a rate cut in March, therefore, the probability is higher than it was three weeks ago,' even if there is no absolute certainty. He expressed preference for loosening policy in 25bp increments.

- Meanwhile, Przemysław Litwiniuk told Bloomberg that the MPC could delay the next rate reduction until April and then deliver a double-barrel 50bp cut, which would give policymakers more time to assess inflation trends and annual adjustments to the CPI basket. Alternatively, the MPC could deliver two 25bp cuts starting in March and in either case the terminal rate would be 3.50%, with potential for further easing 'after the summer holidays' if the economic outlook deteriorates.

- In an interview with Reuters, Marcin Zarzecki said March may be an appropriate moment for an interest rate cut in Poland, and the forecast of the main interest rate at 3.50% this year is "sensible", but said decisions will depend on incoming data and forecasts. "March may be the right time for an interest rate cut. The considered range is 25 basis points. However, I would like to emphasise that this decision will be directly dependent on incoming data and, in particular, on the results of the March inflation projection," Zarzecki said.

- MPC's Gabriela Masłowska told PAP newswire that if headline inflation drops in 1Q26 and the new projection suggests that it will stay within target in coming quarters, there is a 'real chance of a rate cut in March'. In such a case, the Council would likely trim the reference rate by 25bp, following up with another 25bp cut in 2H26 or possibly earlier. In line with recent comments from her colleagues, Masłowska saw the terminal rate at 3.50%.

- PAP then circulated comments from Ludwik Kotecki who signalled that March 'will be a very good moment to make a 25bp cut' and suggested that the target rate is around 3.75-3.50%, adding that the MPC 'should pause for longer' after reaching this level.

EQUITIES: 6100 Handle Provides Next Resistance for EuroStoxx 50 Futures

- The medium-term trend condition in EuroStoxx 50 futures remains bullish and this week’s fresh cycle high reinforces the bull theme. The move higher paves the way for an extension towards 6100.00, and 6134.00, a Fibonacci projection point. Key support to watch lies at the 50-day EMA, at 5896.83. Clearance of this average would highlight a short-term top and signal scope for a deeper pullback.

- The firm reversal higher on Feb 6 in S&P E-Minis refocuses attention on the primary uptrend and the key resistance at 7043.00, the Jan 28 high. Clearance of this level would confirm a resumption of the trend and mark the end of a flat correction in the contract. Key short-term support has been defined at 6751.50, the Feb 6 low, where a break is required to highlight a top and a stronger short-term reversal.

COMMODITIES: Bull Cycle in WTI Futures Remains Intact

- A bull cycle in WTI futures remains intact. However, the reversal from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $62.55. The 50-day EMA lies at $60.79. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger to watch has been defined at $66.48, the Jan 30 high. Clearance of it would resume the uptrend.

- The recent recovery in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high still highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

| Date | GMT/Local | Impact | Country | Event |

| 12/02/2026 | - | BOE MPG Meeting | ||

| 12/02/2026 | 1330/0830 | *** | Jobless Claims | |

| 12/02/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 12/02/2026 | 1345/0845 | BOC's Rogers panel talk on productivity | ||

| 12/02/2026 | 1500/1000 | *** | NAR existing home sales | |

| 12/02/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 12/02/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/02/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/02/2026 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/02/2026 | 1830/1930 | ECB's Lane At The World Ahead 2026 Gala Dinner | ||

| 12/02/2026 | 0000/1900 | Fed's Lorie Logan, Stephen Miran | ||

| 13/02/2026 | 0700/0800 | * | Wholesale Prices | |

| 13/02/2026 | 0730/0830 | *** | CPI | |

| 13/02/2026 | 0800/0900 | *** | HICP (f) | |

| 13/02/2026 | 1000/1100 | *** | EZ GDP 2nd (Flash) | |

| 13/02/2026 | 1000/1100 | * | Employment | |

| 13/02/2026 | 1000/1100 | * | Trade Balance | |

| 13/02/2026 | 1000/1100 | ECB's de Guindos Lecture At Academia Europea Leadership | ||

| 13/02/2026 | 1200/1300 | ECB's de Guindos Remarks and Q&A At Círculo de Confianza | ||

| 13/02/2026 | 1200/1200 | BOE's Pill Fireside Chat At Santander Macro Event | ||

| 13/02/2026 | - | BOE MPG Minutes Released | ||

| 13/02/2026 | - | *** | New Loans | |

| 13/02/2026 | - | *** | Money Supply | |

| 13/02/2026 | - | *** | Social Financing | |

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1330/0830 | ** | US CPI Annual Revised | |

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/02/2026 | 1630/1730 | ECB Lagarde Roundtable on Trade Dependencies and Global Supply Chains |